U.S. equity markets demonstrated another remarkable turnaround on Wednesday as investors returned from the New Year holiday. At its lows the Dow Jones Industrial Average (DJIA) was negative by nearly 400 points, but rallied to finished in positive territory. Volatility, as gauged by the VIX, declined significantly as buyers stepped in to buy what was perceived to be a relatively inexpensive S&P 500 (SPX) at roughly 14.4 X FY19 earnings. But Wednesday’s buying enthusiasm came on the heels of weak Chinese manufacturing data that was thought to be exclusive to the Asian superpower. Investors may have to reconsider this notion in light of the multinational conglomerates with exposures to China. And that brings us to the headlines surrounding one of the world’s largest conglomerates, Apple (AAPL).

While analysts have been lowering their rating, target price and estimates for Apple sales and earnings going forward, the share price has fallen some 30% from its all-time highs. After the closing bell on Wednesday, the smartphone giant warned and lowered its Q1 2019 guidance. Below is a letter from Apple Inc. to investors, indicating the lowered expectations:

To Apple investors:

Today we are revising our guidance for Apple’s fiscal 2019 first quarter, which ended on December 29. We now expect the following:

- Revenue of approximately $84 billion

- Gross margin of approximately 38 percent

- Operating expenses of approximately $8.7 billion

- Other income/(expense) of approximately $550 million

- Tax rate of approximately 16.5 percent before discrete items

We expect the number of shares used in computing diluted EPS to be approximately 4.77 billion. Based on these estimates, our revenue will be lower than our original guidance for the quarter, with other items remaining broadly in line with our guidance.

While it will be a number of weeks before we complete and report our final results, we wanted to get some preliminary information to you now. Our final results may differ somewhat from these preliminary estimates.

When we discussed our Q1 guidance with you about 60 days ago, we knew the first quarter would be impacted by both macroeconomic and Apple-specific factors. Based on our best estimates of how these would play out, we predicted that we would report slight revenue growth year-over-year for the quarter. As you may recall, we discussed four factors:

- First, we knew the different timing of our iPhone launches would affect our year-over-year compares. Our top models, iPhone XS and iPhone XS Max, shipped in Q4′18 — placing the channel fill and early sales in that quarter, whereas last year iPhone X shipped in Q1′18, placing the channel fill and early sales in the December quarter. We knew this would create a difficult compare for Q1′19, and this played out broadly in line with our expectations.

- Second, we knew the strong US dollar would create foreign exchange headwinds and forecasted this would reduce our revenue growth by about 200 basis points as compared to the previous year. This also played out broadly in line with our expectations.

- Third, we knew we had an unprecedented number of new products to ramp during the quarter and predicted that supply constraints would gate our sales of certain products during Q1. Again, this also played out broadly in line with our expectations. Sales of Apple Watch Series 4 and iPad Pro were constrained much or all of the quarter. AirPods and MacBook Air were also constrained.

- Fourth, we expected economic weakness in some emerging markets. This turned out to have a significantly greater impact than we had projected. In addition, these and other factors resulted in fewer iPhone upgrades than we had anticipated.

Despite the revenue shortfall, the company is still expected to report strong earnings growth. Tim Cook noted that Apple still expects to report record earnings per share for the quarter. That figure will be helped by Apple’s record share buybacks though. Apple brought down its forecast for gross margins, from a range of 38% to 38.5% to guidance of “approximately” 38%; raised its expectations for other interest or expense, from about $300 million to about $550 million; and said operating expenses would come in around $8.7 billion, the lower end of the previous stated range of $8.7 billion to $8.8 billion.

The fallout from the Apple shortfall has U.S. and global equity markets pointed lower on Thursday. The ripple affect through the tech-heavy Nasdaq (NDX) is more severe than its peer indices at present, but more importantly is the weight of the Apple news on the FY19 S&P 500 earnings outlook. Apple comprises a significant portion of S&P 500 sales and earnings and as such, investors may prove anxious to see what the iPhone manufacturer actually offers in the way of earnings guidance for 2019.

Several themes or topics that will remain in the spotlight over the coming months were only further exampled in Apple’s latest warnings and letter to shareholders. China, as we already know, is experiencing slowing economic growth. It’s nothing near recessionary levels or concerns, but the rate of change in growth has proven impactful nonetheless. Investors should expect, once U.S. earnings season gets underway, to witness companies with exposures to China discussing this weakness and as having an impact on corporate results. Moreover, we expect much of the commentary to denounce the ongoing trade feud between the U.S. and China as proving to negatively impact U.S. corporate results. For more commentary on the impact from a Chinese economic slowdown, Kenny Polcari of Butcher Joseph Asset Management discusses the topic on CNBC.

Another theme we expect to carry forward through much of Q1 2019 surrounds the Federal Open Market Committee or FOMC/Fed. Apple’s results and letter serve to highlight a weakening global economic condition, which we believe the Fed will need to more keenly recognize within the scope of its monetary policy and rate hike decisions.

Given the uncertainty surrounding global growth and the future of trade between the U.S. and China, the FOMC may find itself pausing rate hikes through much of 2019 and possibly all of 2019. In fact, based on the December 2019 Fed funds futures contract, the market is placing a greater probability on a rate cut than a rate hike by the end of 2019.

Removing the potential for another rate hike in 2019 removes market risk and anxiety and allows for investors to focus more directly on the path of the economy and corporate earnings. Near term Fed speeches are likely to point to the Fed’s newfound dovish stance, despite its forecast of 2 rate hikes for 2019.

In addition to the themes surrounding global growth, the Fed and trade feuds, the U.S. Dollar remains front of mind with investors. The dollar had its best annual gain in about three years after an abysmal 2017. A strong U.S. dollar proves to diminish sales for U.S. multinational companies and negatively impacts corporate results.

The dollar benefited from President Donald Trump’s tax plan, supportive economic data, as well as the Federal Reserve’s increase of benchmark interest rates. Moreover, arguably the most direct catalyst for U.S. currency has been its re-established appeal as a haven currency amid tariff battles between the U.S. and its trade partners. Under the assumption that an increase in import duties would be more detrimental for other international participants, the dollar became a comparatively more attractive investment. Investors might have to reassess their currency positions after the first quarter of 2019.

“It’s all very uncertain,” said Aaron Hurd, senior currency portfolio manager at State Street Global Investors. “The global economic outlook and trade headwinds could add concerns. The U.S. dollar tends to perform well in times of global trouble, and it might defend its bid as a haven. However, a slowdown in the U.S. would likely spell a dollar downtrend”

Safe haven strategies may be removed to some degree and in favor of risk-on strategies and greater exposures to equities. With regards to the U.S. Dollar possibly weakening in 2019, the European economy remains in question given the threat of a “hard Brexit” and the resulting end of the European Central Bank’s Quantitative Easing policy. For a detailed timeline on future Brexit developments, please review them here.

Prime Minister Theresa May has now said the debate on her EU deal will restart on the week of January 7, with the vote scheduled for the week of January 14. The vote is a legal obligation under the UK’s 2018 EU Withdrawal Act, which says it must take place “before the European Parliament decides whether it consents to the withdrawal agreement being concluded on behalf of the EU”.

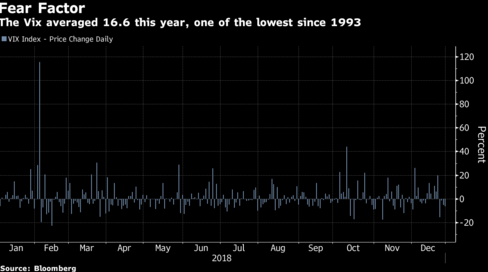

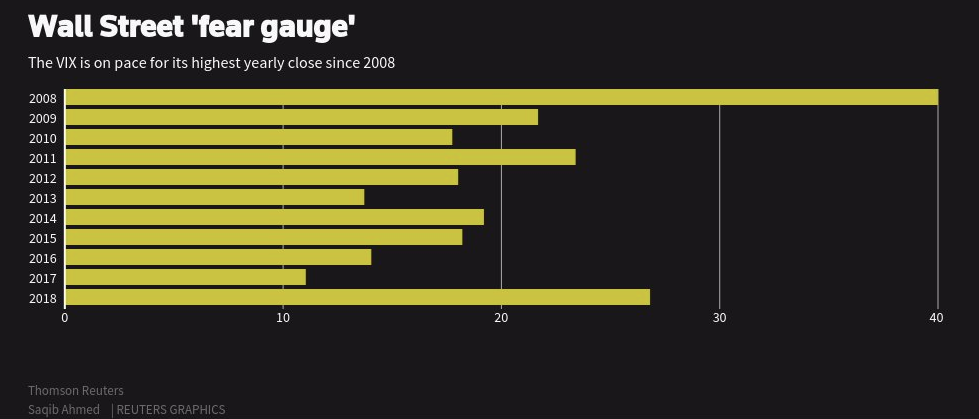

The last theme we desire to touch on with regards to equity markets in 2019 is the apparent rise in market volatility that seemingly persisted through much of 2018. While 2018 seemed to be a very volatile market year, it was only with respect or in comparison to that of 2017, which proved the least volatile market year on record. The VIX averaged 16.6 over the 250 trading days of 2018, the 12th-lowest reading since 1993.

But compare the number with 2017’s average of 11.1, the rate of change becomes disturbing.

As shown in the chart above, 2018 was the most volatile market year since 2008.

“It felt like a much more erratic market because, A, it was, and, B, we were lulled to sleep by last year’s lack of volatility,” said Rick Bensignor, president and founder of the Bensignor Group and a former Morgan Stanley strategist.

There still remains a good deal of uncertainty in the marketplace entering the New Year. Given this backdrop and the fact that many investors haven’t been around to see normal market volatility, we expect similar volatility in the marketplace for at least the first half of 2019. John Spallanzani, portfolio manager at Miller Value Partners offered much the same sentiment in a recent telephone interview.

“Many people in the market have not been around that long,” he said. “All they know is a low rate environment and a low volatility environment, and that’s not the norm. For a healthy market you need both. Few are used to or have experienced a tightening cycle. And even fewer from a level of negative interest rates.”

While Spallanzani may not find the Fed tightening in 2019 to the extent we saw fiscal tightening in 2018, the global economic strength and trade feuds are enough to create market headwinds in the early going. Markets do not perform well during times of uncertainty and investors have been awakened to this reality once again in December 2018.

In light of the recent Apple Inc. headlines, there may be increased risk to the market’s rally, as Apple weighs heavily on the major averages. The U.S. consumer remains strong by all accounts, but as it pertains to profiting from the U.S. consumer and the all-important Holiday shopping period, we’d like to see how the retailers performed during the Holiday period. Last year, many retailers preannounced strong results with raised guidance in January. We’ll have to wait and see if that is the case this January.

Ahead of the opening bell on Thursday, investors will receive economic data related to the labor market in the way of ADP Payroll report and Jobless Claims. At 10:00 a.m. EST the government will release the latest ISM manufacturing data, which is expected to slow from the previous month. The economic data could go a long way toward offsetting the impact from the Apple headlines, or further fuel a risk-off environment.