By St. Louis Federal Reserve Bank and David Andolfatto

In the second quarter of 2008, U.S. federal debt held by the public totaled about $5.3 trillion, or 35% of gross domestic product (GDP). This figure grew to $20.5 trillion—or 105% of GDP—by the second quarter of 2020. To put it another way, the national debt has increased 400% in 12 years, while over the same period, national income has grown by only 30%.

Since the Congressional Budget Office projects that federal budget deficits of 4%-5% of GDP will persist in the foreseeable future, a growing number of analysts and policymakers are raising alarms about whether this fiscal situation is sustainable.

Most people have a very personal view of the nature of debt. We know that high levels of debt and deficit spending at the household level are not sustainable. At some point, household debt has to be paid back. If a household is unable to do so, its debt will have to be renegotiated. It is natural to think that the same must hold true for governments. But this “government as a household” analogy is imperfect, at best. The analogy breaks down for several reasons.

Debt Issuance

While a household has a finite lifespan, a government has an indefinite planning horizon. So, while a household must eventually retire its debt, a government can, in principle, refinance (or roll over) its debt indefinitely.

Yes, debt has to be repaid when it comes due. But maturing debt can be replaced with newly issued debt. Rolling over the debt in this manner means that it need never be “paid back.” Indeed, it may even grow over time in line with the scale of the economy’s operations as measured by population or GDP.

Unlike personal debt, the national debt consists mainly of marketable securities issued by the U.S. Treasury as bonds. It is of some interest to note that the Treasury Department issued some of its securities in the form of small-denomination bills, called United States Notes, from 1862-1971 that are largely indistinguishable from the currency issued by the Federal Reserve today.

Today, U.S. Treasury securities exist primarily as electronic ledger entries. These securities are used extensively in financial markets as a form of wholesale money. The cash management division of a large corporation, for example, may prefer to hold Treasury securities instead of bank deposits because the latter are insured only up to $250,000.

If cash is needed to meet an obligation, the security can either be sold or used as collateral in a short-term loan called a “sale and repurchase agreement,” or repo, for short. Because investors value the liquidity of Treasury securities, they trade at a premium relative to other securities. So, investors are willing to carry Treasury securities at relatively low yields, the same way we are willing to carry insured bank deposits at very low interest rates, or the same way we are willing to carry securities that bear zero interest like the ones displayed above.

Ultimately, the federal government has control over the supply of the nation’s legal tender. Both of the notes above have been legal tender since the gold recall of 1933. Now, consider the fact that the national debt consists of U.S. Treasury securities payable in legal tender. That is, imagine the national debt consisting of interest-bearing versions of the U.S. Note shown above.

When the interest comes due, it can be paid in legal tender—that is, by printing additional U.S. or Federal Reserve Notes. It follows that a technical default can only occur if the government permits it. The situation here is similar to that of a corporation financing itself with debt convertible to equity at the issuer’s discretion. Involuntary default is essentially impossible. This aspect of U.S. Treasury securities renders them highly desirable for investors seeking safety—a property which again serves to drive down their yields relative to other securities.

Debt as Currency

To the extent that the national debt is held domestically, it constitutes domestic private sector wealth. The extent to which it constitutes net wealth can be debated, but there’s not much doubt that at least some of it is viewed in this manner. The implication of this is that increasing the national debt makes individuals feel wealthier.

When this “wealth effect” is generated by a deficit-financed tax cut (or transfers) in a depression, it can help stimulate private spending, making everyone better off. When the economy is at or near full employment, however, such a policy is instead more likely to increase the price level, which can lead to a redistribution of wealth.

Together, these considerations suggest that we might want to look at the national debt from a different perspective. In particular, it seems more accurate to view the national debt less as form of debt and more as a form of money in circulation.

Investors value the securities making up the national debt in the same way individuals value money—as a medium of exchange and a safe store of wealth. The idea of having to pay back money already in circulation makes little sense, in this context. Of course, not having to worry about paying back the national debt does not mean there is nothing to be concerned about. But if the national debt is a form of money, wherein lies the concern?

Debt Service

Unlike the U.S. Notes issued in the past, Treasury securities bear interest (or sell at discount, in the case of Treasury bills). So even if the national debt doesn’t have to be paid back, it still needs to be serviced. The interest expense associated with carrying debt is called the carry cost.

Debt management strategies employed in government treasury departments seem heavily influenced by corporate practices. But corporations have to worry about rollover risk, whereas governments can always (if they choose) have their central banks support refinance operations. As well, corporations operate in the interests of a smaller set of constituents than a federal government. Given these considerations, it is not immediately clear whether corporate debt management principles apply to the Treasury Department.

If one had to draw on the corporate sector for analogy, an example might be a bank. A significant amount of debt issued by banks is in the form of insured deposit liabilities. Because insured deposits are safe and because they constitute money, investors are willing to carry deposits at low yields. As a result, deposits are a very cheap source of funding for banks.

This low-cost source of funds is used to carry higher return assets, like mortgages and business loans. One might say that the net carry cost of debt, in this case, is negative. To the extent that the federal government invests in programs designed to enhance productivity (e.g., healthcare and infrastructure), the same thing might apply to the national debt, which is willingly carried by investors at relatively low yields.

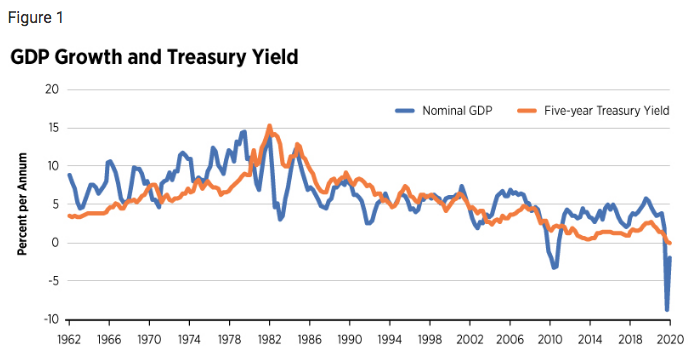

But even if government expenditures do not generate high pecuniary rates of return, the federal government may still be in a position to carry its debt at an effective negative rate. This would be true, for example, if the interest rate on the national debt was on average less than the growth rate of the economy or, as the condition is expressed in more technical terms, if r ‹ g.

It follows as a matter of simple arithmetic that if r ‹ g, then the government is in position to run a primary budget deficit indefinitely—that is, the effective carry cost of the debt is negative, even if the interest rate on the debt is positive. Figure 1 plots the year-over-year growth rate in nominal GDP against the five-year Treasury constant maturity rate.

Monetizing the Debt

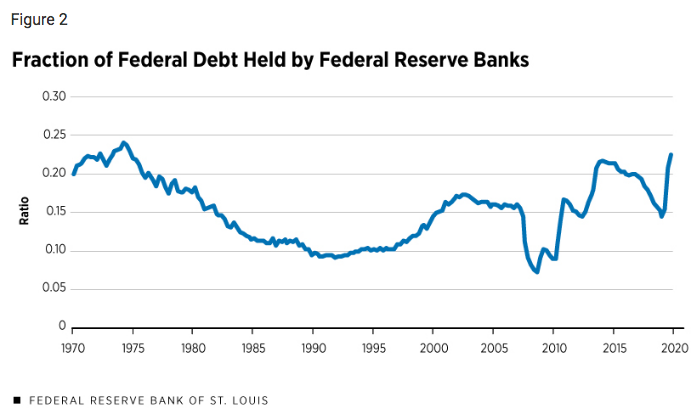

The average interest expense of the federal debt is influenced by the composition of the debt between currency, reserves, bills, notes and bonds. The composition of the debt is determined in part by monetary policy. In particular, when the Federal Reserve purchases Treasury securities, it is in effect swapping lower-yielding reserves for higher-yielding Treasury securities (sometimes called “monetizing the debt”). The composition of Federal Reserve liabilities between reserves and currency in circulation is determined by the demand for currency, which can be thought of as a zero-interest government security.

The recent increase in Federal Reserve holdings of Treasury securities is manifesting itself primarily in the form of interest-bearing reserves. The implication of this is that private banks are now holding large quantities of interest-bearing reserves that are, to a first approximation, not much different from interest-bearing Treasury securities. So, the “monetization” of debt now is not the same as in the past (see the figure below), when Federal Reserve liabilities mainly took the form of zero-interest securities (currency).

Exactly how large of a primary deficit the government can run (say, relative to GDP) depends on the debt-to-GDP ratio. The debt-to-GDP ratio is not determined by the government; it is determined by the market demand for debt, which, in turn, depends on the structure of interest rates either determined or influenced by the Federal Reserve.

An increase in debt obviously increases the numerator of the debt-to-GDP ratio. But how the debt-to-GDP ratio responds depends on the denominator too. It is possible, for example, that an increase in debt causes the price level to rise by an even higher amount, which, for a given level of real GDP, would cause the nominal GDP to rise and the debt-to-GDP ratio to fall.

There is presumably a limit to how much the market is willing or able to absorb in the way of Treasury securities, for a given price level (or inflation rate) and a given structure of interest rates. However, no one really knows how high the debt-to-GDP ratio can get. We can only know once we get there.

Inflation

The purchasing power of nominal wealth is inversely related to the price level. That is, a higher price level means one’s money buys fewer goods and services. Inflation refers to the rate of change in the price level over time.

It is helpful to keep in mind the difference between a change in the price level (a temporary change in the rate of inflation) and a change in inflation (a persistent change in the rate of inflation). It is admittedly difficult to disentangle these two concepts in real time, but it remains important to make the distinction.

The amount of nominal government “paper” the market is willing to absorb for a given structure of prices and interest rates is presumably limited. A one-time increase in the supply of debt not met by a corresponding increase in demand is likely to manifest itself as a change in the price level or the interest rate, or both. An ongoing issuance of debt not met by a corresponding growth in the demand for debt is likely to manifest itself as a higher rate of inflation. How the interest rate on U.S. Treasury securities is affected depends mainly on Federal Reserve policy.

As long as inflation remains below a tolerable level, there is little reason to be concerned about a growing national debt. Like a firm that finances itself with convertible debt, the prospect of involuntary default is never a concern.

Of course, in reality, a firm that exercises its conversion option is likely to experience share dilution. Similarly, a government that exercises its power to monetize debt is likely to experience a jump in the price level.

But in both cases, the resulting dilution is likely to have more to do with the underlying events triggering the option, rather than the conversion itself. A company or government that suddenly finds itself under fiscal pressure (e.g., because of an emergent rival or a war) will have to deal with that pressure one way or another, whether through cost-cutting measures, outright default or dilution.

Inflation Target

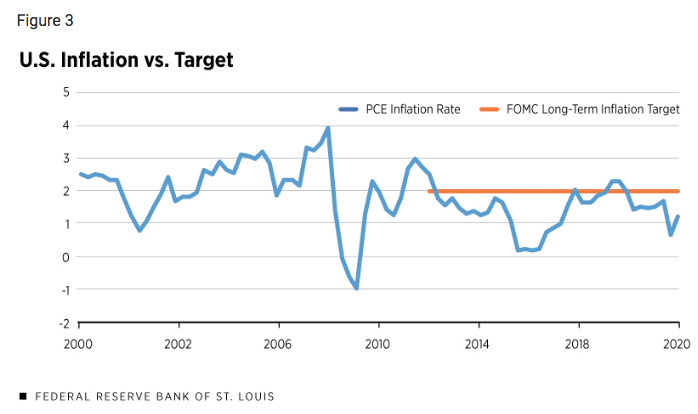

The Federal Reserve has had an official 2% inflation target since 2012. In the recent review of their monetary policy framework, Fed officials expressed the willingness to let inflation overshoot its target if it meant accommodating an improving labor market.

However, there is the question of what will happen if inflation rises to and remains above a tolerable level. At some point, the Federal Reserve may be compelled to cut back on its purchases of U.S. Treasury securities, the effect of which would be to put upward pressure on bond yields of all maturities.

Higher interest rates would reduce private sector wealth and increase the cost of borrowing, both of which would serve to reduce private sector spending, slowing economic growth. It would also serve to increase the government’s carry cost. This, in turn, could result in a set of government austerity measures, which could propel the economy into a deep recession.

Of course, all this might be avoided if the pace of debt-issuance is slowed beforehand. But, as mentioned above, there is no way of knowing beforehand just how large the national debt can get before inflation becomes a concern.

Since the financial crisis of 2008-09, the Personal Consumption Expenditures (PCE) inflation rate has averaged around 1.5%. All we can say for now is that inflationary pressures appear contained. It would be wise, however, for the government to have a plan in place to deal with this contingency should it arise. The plan might allow for inflation to remain elevated for a period of time as tax-and-spend legislation is recalibrated.

COVID-19 Pressures

The recession induced by the COVID-19 pandemic differs in some ways from those induced by monetary-fiscal contractions or asset-price collapses. In these latter cases, private sector spending tends to decline far more than what might be justified by any change in underlying fundamentals. The COVID-19 shock, in contrast, induced a contraction in some sectors of the economy that served a clear social purpose; namely, preventing the spread of the virus.

A fundamental shock in one sector should naturally lead to changes in the level of economic activity in other sectors. While some sectors may even expand, aggregate net output is likely to decline. To the extent that this rearrangement of activity constitutes a desirable response to the pandemic shock, fiscal stimulus designed to boost overall aggregate demand is not in order.

On the other hand, a shock of this nature also disrupts and generally tightens credit conditions. An uncertain economic outlook naturally leads individuals and businesses to cut back on their spending to build precautionary savings. To the extent that this fear is self-fulfilling, some fiscal stimulus may be in order.

But even absent the need for fiscal stimulus, it seems clear enough that social insurance is necessary. A program designed to maintain the incomes of individuals and businesses disproportionately affected by the pandemic is something most people would likely have wanted for themselves if they were so afflicted. To the extent that aggregate output declines and income support is financed by a one-time increase in the national debt, the result is likely to be a one-time increase in the price level.

In other words, Americans should prepare themselves for a temporary burst of inflation. To be clear, a higher price level is not inevitable, since much depends on how the demand for U.S. Treasury securities responds going forward.

But should the inflation rate suddenly spike, this is not a signal to tighten monetary or fiscal policy, as long as the spike is temporary. The higher price level that would accompany this event should be understood as the mechanism through which purchasing power is redistributed over the course of the pandemic.7

The author thanks Federal Reserve Bank of St. Louis colleagues Subhayu Bandyopadhay, Andrea Terzi, Christopher Sims and David Wheelock for their perspective on this article.