Research Report Excerpt #1

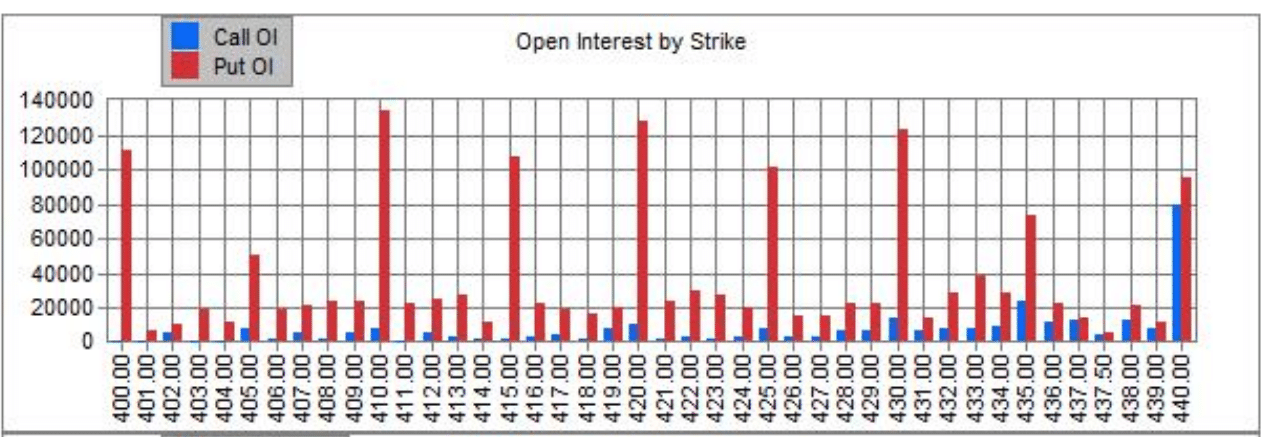

Before we get to that though, recall what Finom Group offered in its most recent weekly State o the Market, and regarding Call and Put Open Interest strikes.

- First time in many, many months that we are vulnerable to a delta-hedge selloff, with:

- 1) heavy put open interest strikes on SPY below market

- 2) Monday’s break of put-heavy 430 strike and…

- 3) Standard October monthly expiry less than 2 weeks away.

- Don’t get too comfortable with the recent rebound in the market folks. Keep an open mind and be ready to act should prices continue to come under pressure through monthly Op/EX. (3rd Friday of every month).

As I often suggest, and it would increasingly become more relevant under price pressure, for every con there is a pro and for every negative there is a positive. If not for any other reason, such truisms of analyzing the whole data spectrum should reinforce the need for an investor to remain flexible, unbiased and with a long-term time horizon… when acting on local price pressure. (stocks, bonds and ETFs)

Research Report Excerpt #2

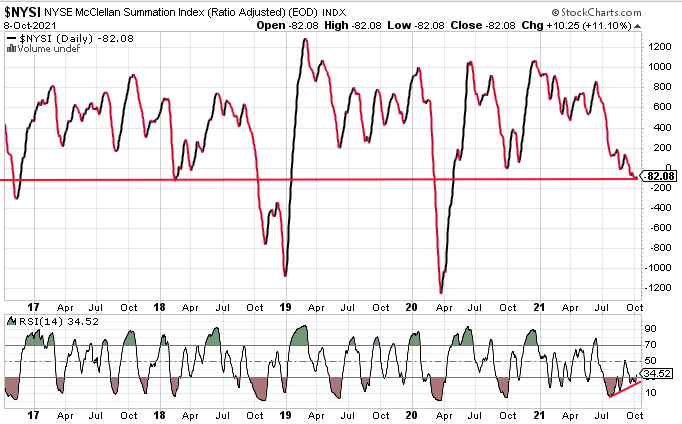

The negative reading in the NYSI over the last 6 weeks, but recent 2-day advance might indicate that many stocks have bottomed and turned higher. The following chart of the NYSI offers one last perspective on broad market, long-term breadth (5-yr. chart)

Our understanding, and as suggested already, is that many stocks have been downtrending for some time while the indexes have been held up by the mega-cap stocks. The long-term NYSI shows that absent a more severe index correction, this is usually where the many stocks that have already corrected, stabilize and turn higher and with the mega-cap names. In 2018, the NYSI bounced at precisely this level and post a 12% S&P 500 correction. The drop below again in Q4 2018 was a technical bear market, born of a Fed rate hike and government shutdown into year-end.

Research Report Excerpt #3

There are definitely many strategists, economists, and market participants who are of the opinion that the have nots will outweigh the haves into year-end, producing a grand market correction or reset. Keeping in mind that this would prove normal, given that most new cyclical bull markets and economic expansion cycles begin with great strength, but then transition to normalized growth rates with a bigger market correction. The equity market aims to price in this transition, usually. That has largely been the call from Morgan Stanley’s chief equity strategist for many, many, many months now.

“The typical mid-cycle “fire” outcome would lead to a modest and healthy 10% correction in the S&P 500. However, the “ice” scenario is starting to look more likely, and could result in a more destructive outcome – i.e. a 20%+ correction. As a result, we continue to recommend a barbell of more defensively oriented quality (Healthcare and Staples) to protect from the “ice” scenario while keeping a leg in Financials to participate in the “fire” outcome as higher rates materialize. The ice scenario would be worse for markets and we are leaning in that direction given the fall in consumer confidence and reset lower in PMIs we expect.”

Research Report Excerpt #4

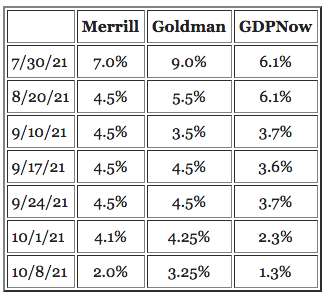

The laws of large numbers always loom, large! It was highly improbable that growing Q2 GDP at 6.7% would find like growth in subsequent quarters based on normalization of economic conditions, which was only expedited by the Delta wave of Covid-related issues. With Covid infections, hospitalizations and deaths all well-off there September highs, don’t be too surprised if the weaker than expected Q3 GDP normalizes at a higher level in Q4 2021.

Research Report Excerpt #5

The labor reporting period, along with much of the slower growth economic data disseminated through the Q3 period may simply prove a trough spurred by the Delta variant which has receded. Knowing this, the Fed sees other data that will likely prove beneficial to employment going forward in many of the high frequency data points.

The Oxford Economics U.S. recovery tracker reached a post-pandemic high at the end of September. High frequency data point to economic resilience entering Q4 despite Covid, supply chain, inflation headwinds and the like. While we know supply line bottlenecks will hit many consumer facing goods company’s in the 3rd and 4th quarter of 2021, we see the issues here subsiding into year-end and providing a tailwind to growth by the 2nd half of 2022.

Research Report Excerpt #6

At this point, it’s probably a good idea to remind ourselves that the market isn’t the economy and the economy isn’t the market in real time. Nonetheless, the forward discounting mechanism that is the stock market aims to price in slower earnings growth. Therefore it should not be surprising that stocks and the whole of the stock market have consolidated through the latter portion of Q3 2021. But the most important consideration hence forth, and given this discounting mechanism, would be what the market discounts next. Given that we have seen strengthening high frequency economic data, retail sales and even certain PMIs… a re-acceleration of growth and earnings in Q4 2021 would suggest the market risk is to the upside, assuming the re-acceleration of growth.

Research Report Excerpt #7

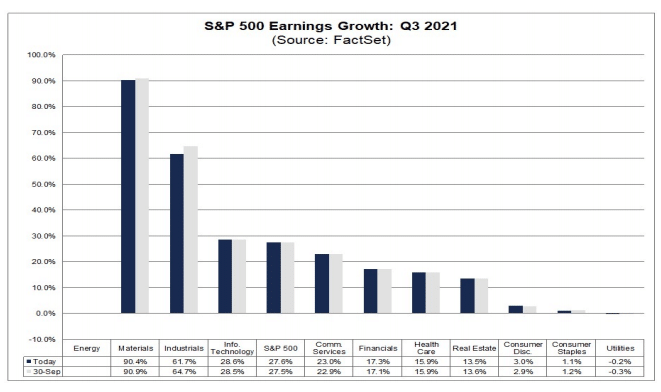

For Q3 2021, forty-seven S&P 500 companies have issued negative EPS guidance and fifty-six S&P 500 companies have issued positive EPS guidance.

- For the third quarter, S&P 500 companies are projected to report earnings growth of 27.6% and revenue growth of 14.9%.

- For Q4 2021, analysts are projecting earnings growth of 21.8% and revenue growth of 11.5%.

- For CY 2021, analysts are projecting earnings growth of 42.8% and revenue growth of 15.0%.

- For Q1 2022, analysts are projecting earnings growth of 5.5% and revenue growth of 8.4%.

- For CY 2022, analysts are projecting earnings growth of 9.7% and revenue growth of 6.8%.

- The forward 12-month P/E ratio is 20.5.

Research Report Excerpt #8

You’ve probably become familiar with this popular truth fashioned by Peter Lynch: “Far More Money Has Been Lost By Investors Trying To Time Corrections Than In All Corrections Combined!” Mike Wilson, the lead equity strategist at Morgan Stanley has been calling for a 10% correction and suggesting investors prepare for that potential since May of 2020.

Imagine missing out on nearly 1,000 points of S&P 500 forward returns since May 2020? Far more money has been lost planning for corrections than the correction itself indeed! Here is another interesting study from Peter Lynch depicted below. The reason for the dissemination of the study is because avoiding a correction is one thing and just one reason that investors choose to sit on their hands while the market’s primary trend passes them by. Another reason is that many investors are fearful of buying the top.

Research Report Excerpt #9

This may be a new 2021 issue regarding the power crunch in China, but it is not a new issue FOR China altogether. See the headlines from past years below:

Many investors see such headlines as ominous without the appropriate comparisons or juxtapositions. At times like that, and for those less resourced, I would like to offer the following acronym and advisement of becoming resourced: FEAR: False Evidence Appearing Real.

Yes, there is likely going to be some impact from the China energy crunch, but within the scope of a $60trn global economy? And as another saying goes; As goes China goes the Asia Pacific…

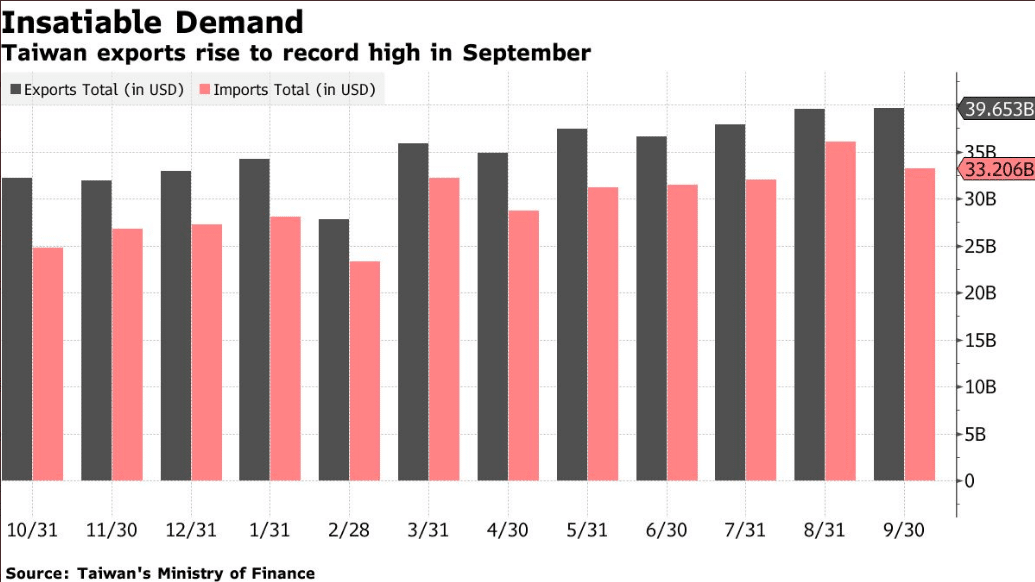

Taiwan’s exports grew faster than even the most bullish economist forecast last month, fueled by ongoing global demand for semiconductors. Exports rose 29.2% in September from a year earlier to a record $39.7 billion, according to a statement from Taiwan’s Ministry of Finance on Friday. That compares to a median estimate of 25% in a Bloomberg survey of economists. Imports surged 40.4% to $33.2. September’s figures benefited from resurgent worldwide demand, especially for electronic devices and new technologies such as 5G, according to the ministry’s statement. The decision by several major chipmakers to raise prices in recent months also bolstered figures. That’s a lot of crap going into and out of Taiwan is it not, crudely asked?