After an outside reversal trading day last Friday that found the Nasdaq going from up 1% to negative .23% and the Dow and S&P 500 basically flat for the day, index futures are in the red and following the lead of Asian markets. Friday’s late day reversal came on the announcement from the Robert Mueller investigation that resulted in the indictment of 13 Russian nationals. The indictments certified that these Russian nationals meddled in the 2016 U.S. elections. U.S. investors may have jumped to the conclusion, on the announcement, that this may lead to continued investigations and possible U.S. 2016 campaign involvement. Naturally, the Kremlin has dismissed the accusations.

The last time the U.S. major indexes experienced an outside reversal day it foreshadowed the markets greater than 10%+ correction. Investors will be on edge this shortened trading week as the 10-year Treasury is back to yielding above 2.91 percent and with inflation concerns abound. But it’s not just rising rates that have Goldman Sachs concerned as they discussed a sea of red ink that they are seeing. Goldman released their latest commentary on the markets and the economy over the weekend that raises concerns on growing debt levels.

“In the wake of an ambitious infrastructure plan and a budget that drew fire from virtually all sides, Goldman Sachs said in a note to clients that the federal deficit would reach 5.2 percent of U.S. growth by 2019, and would “continue climbing gradually from there.”

“The fiscal expansion should boost growth by around 0.7pp in 2018 and 0.6pp in 2019, but will likely come to an end after that”—listing a litany of reasons why spending and debt would conspire to undermine the world’s largest economy.

Coming into the trading week it’s quite clear that fears is elevated ahead of the release of the latest Federal Reserves minutes due out this Wednesday. Last week, new Fed Chair Jerome Powell suggested that the Fed would push ahead with scheduled rate increases. The central bank is expected to increase the cost of borrowing in March to keep the economy from overheating, but now investors wonder if the Fed will raise rates four times in 2018 instead of three as previously planned. Philadelphia Federal Reserve Bank President Patrick Harker and Minneapolis Federal Reserve Bank President Neel Kashkari are scheduled to speak on Wednesday. New York Federal Reserve Bank President William Dudley is slated to speak on Thursday, while Cleveland Federal Reserve Bank President Loretta Mester and San Francisco Federal Reserve Bank President John Williams have speaking engagements on Friday. Other than Fed speeches the economic calendar is relatively light this week, highlighted by existing home sales also due out on Wednesday before the opening bell.

While U.S. equity futures are notably lower this morning and Goldman Sachs has issued a dire outlook for fiscal policy in the years to come, BlackRock is urging investors to take notice of the effects from the recent tax overhaul. We have upgraded our tactical view of U.S. equities to overweight from neutral,” says the company’s global chief investment strategist, Richard Turnill.

“The reason: Impending fiscal stimulus is supercharging U.S. earnings growth expectations.”

Even though the market has retraced more than half of its February losses, BlackRock believes the impact of tax law changes and company spending plans are still underappreciated by investors. They expect earnings growth and dividends to fuel returns going forward.

“What happened to the U.S. on the back of tax cuts and fiscal stimulus is something we’ve never observed. All regions are showing improvements in positive earnings revisions but nothing like the U.S.”

Bulls and bears will continue this tug-of-war through much of 2018 and as higher rates persist along the same path of Fed rate hike speculation. With the backdrop of increased deficits and consumer debt levels spirited higher by the tax overhaul, the bears have taken back some control of the markets in the early portions of 2018. Fears of increased debt burdens as rates are edging higher bring about recessionary concerns.

As shown in the chart above, the Fed Funds rate can be a useful tool for determining the potential of a near-term recession. The chart shows that since the 1950’s, the fed funds rate rose to a peak before each recession. At present, the Fed is fiercely focused on whether or not it’s formerly hoped upon inflation targets would finally come to fruition. While the Fed has desired to see it’s 2% target hit in previous years, this may prove to derail the longstanding trend for U.S. equities. The latest CPI and wage inflation results have brought into question the path for the Fed and heightened inflation fears. The latest CPI report showed month over month inflation was up 0.5%. The annualized inflation was 2.1%. Core inflation was up 0.3% month over month and the annualized result was 1.8%. On this metric, the Fed’s target wasn’t hit, but it’s getting pretty darn close and forces investors to follow the reporting for developing trends.

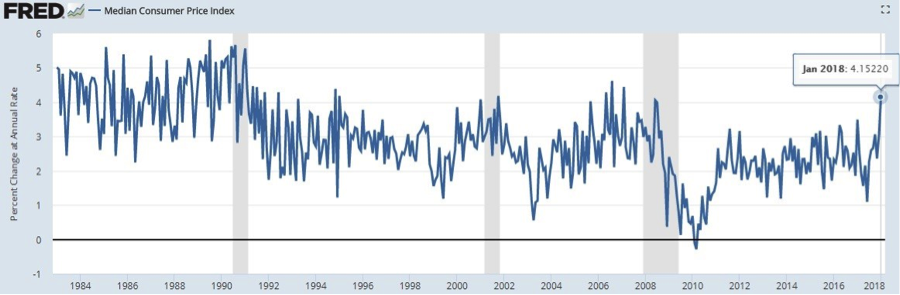

Moreover, as the chart below shows, the median CPI increased 4.15%, which was the highest level since February 2007. This type of result makes some analysts think the Fed will raise rates 4 times in 2018. If the Fed raises rates 100 basis points, the Fed funds rate would be at 2.25-2.5%.

One thing seems for certain in this environment of inflation and fiscal policy concerns, elevated levels of volatility in the market may persist. At present, the VIX or fear gauge suggests daily moves of greater than 1%, which seems unsustainable. Nonetheless, until a clear path for equities is realized, investors should brace themselves for a bumpy ride in 2018.