So we had a pretty strong rally in the major indices on Monday. By now, everyone is aware that a “trade truce” between China and the U.S. has resulted in the latest market uptick. The media has taken to task the trade truce, describing it as lacking substance and less likely to prove an actual deal and/or outcome within the 90-day period outlined by the 2 participating parties. Seems rather timely that the media throws cold water on the trade truce given the subdued market sentiment since October and with the S&P 500 still in correction territory. With regards to the trade truce and to be clear, that 90-day period will commence on January 1, 2019. The key investor takeaway from the trade truce is quite simple: NO ADDITIONAL TARIFFS, INCLUDING THOSE PREVIOUSLY THREATENED BY THE WHITE HOUSE, WILL BE IMPLEMENTED DURING THE 90-DAY NEGOTIATING PERIOD! Finom Group believes that regardless of how the media portrays the trade truce, it is a net positive for sentiment, at least until something materially changes in the negotiations.

But the rally in global equities and domestically on Monday is already fading; as Finom Group expected it do so, but only to a degree. In our weekly research report (subscription needed) titled Does the Trade Truce Produce a Change in Analysts’ Earnings Estimates?, we offered subscribers the following expectation regarding the potential for markets to rally initially, but find resistance and sellers rather quickly.

“More importantly with respect to where the S&P 500 rests, if that is a positive move come Monday that does achieve the expected move for the day, it takes the SPX above 2,800. Pretty key level folks, pretty key level. But even if the S&P 500 breaks above 2,800, Finom Group isn’t of the belief that sellers would not step in and lighten up positions at that point/level. It’s always important to plan ahead and that’s why we’re referencing the Monday expected move and the possibility of what institutional traders could already have in mind.”

As one can clearly see from the chart of the S&P 500 above, the benchmark index gapped higher at the opening bell, achieving 2,800 and before sellers stepped in. Nearly half of the daily gains on Monday were removed by the afternoon trading hours, but the S&P 500 still managed a healthy 1% gain on the day, led by tech stocks.

While the percentage gain of the market yesterday was strong, the rally didn’t’ seem as spectacular as what the pre-market activity suggested it would be. The “sell the rip” sentiment is still in place, but we think that will prove advantageous for the bull market and investors who maintain a healthy discipline. Two of the major headwinds and dark clouds hanging over the market have been either removed or put on the back burner with a more dovish Fed and a trade truce between the world’s 2 biggest economies. Crude oil prices rose sharply yesterday and are proving to further its rally on Tuesday and ahead of Friday’s OPEC meeting, which is largely expected to bring about production cuts. And with all these headwinds being removed or finding some semblance of resolution, corporate earnings haven’t changed, haven’t worsened and have only found the possibility of improved sentiment for 2019. Citigroup’s Tobias Levkovich’s recent notes take the earnings outlook into consideration when forecasting the potential for equity markets in 2019.

“Back in September, we were deeply concerned that investors were too optimistic,” Levkovich, the bank’s chief U.S. equity strategist, wrote in a note to clients. “But sentiment has shifted following the rout of the past two months. Low-end neutral readings argue for a 90% probability of gains in the next 12 months versus September’s 70% chance of a down market – a very marked change.

Our normalized earnings yield gap work, which incorporates both cyclically adjusted P/E ratios and the five-year forward swap contract’s 10-year Treasury yield levels … it implies a 90% chance of an up market in 12 months.”

Despite how quickly market sentiment shifts, seemingly from one week to the next, it remains keenly important that investors focus on the fundamentals. The fundamentals still promote earnings growth out into 2019 and for the whole of 2019, thus far. While it is true that trade skirmishes can still pop up in 2019 and global economies are slowing, domestic corporate earnings are not expected to decline in 2019 and equity markets follow earnings over time.

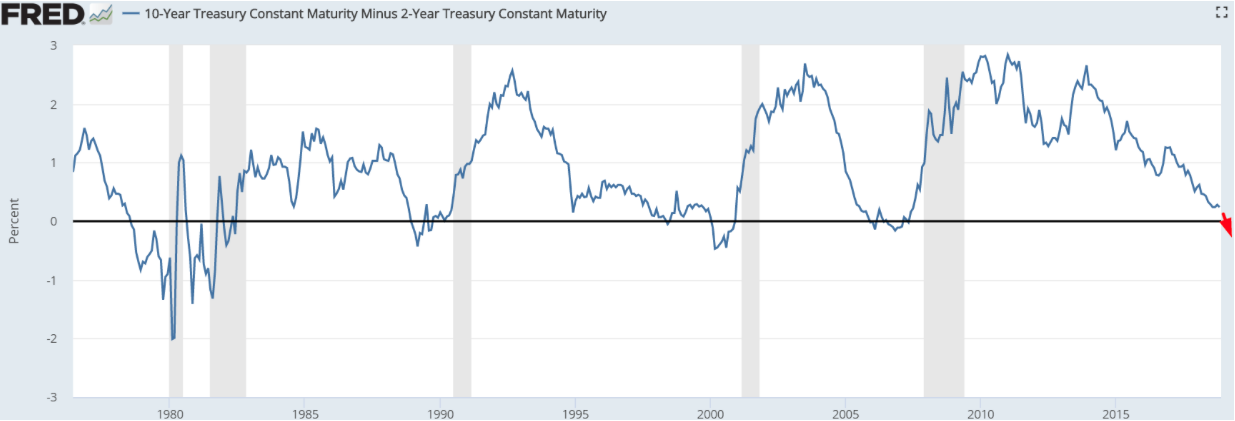

One of the bigger or most obvious reasons the S&P 500 found difficulty breaking through and holding above resistance levels on Monday’s broad market rally was due to the bond market, the yield curve flattening to be more precise. We mentioned this aspect of investor sentiment in our weekly research report as an impediment to investor sentiment and equities. Against the backdrop of a slowing global economy, trade skirmishes and rising rates, the yield curve’s slope as measured by the spread between short-dated and long-dated yields, are closing in on a so-called inversion. An inversion implies investors are selling short-dated bonds at a brisker pace than their long-dated counterparts. Bond prices rise as yields fall.

While Finom Group is of the opinion, which is also the opinion of the Federal Reserve Chairman Jerome Powell, that a yield curve inversion isn’t likely the key recession signal that it has been in the past, the broader participating market still feels as though it is. When an inversion is triggered, this bond market indicator has been an accurate predictor of recessions, though the timing between an inversion and an economic downturn can vary from six months to as much as two years.

During Monday’s equity market rally the yield curve stole much of the trade truce headlines, as the spread between the 3-year Treasury and 5-year Treasury bond inverted. Except for the fact that this isn’t the inversion economists fear or even consider for recessionary signals, the inversion still found equity investors with increasing concern over the yield curve. Why? The last time the 3-year and the 5-year note inverted was back in 2007. That is also the same year that an inversion occurred between the more closely followed 2-year and 10-year Treasurys. And that’s the bigger issue for investors, analysts and economists alike, the current and extreme flattening of the 2-year and 10-year Treasury yield curve. It is the flattest it has been since 2007.

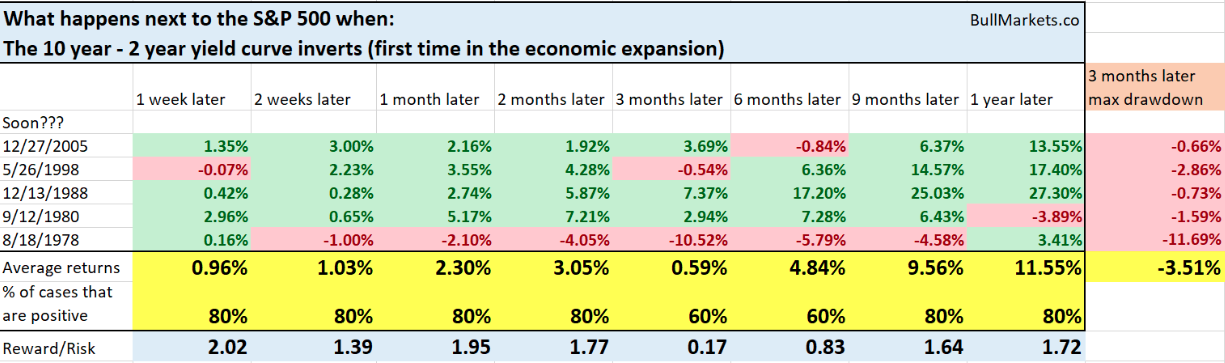

The reality is that even when the priority yield curve between the 2-year and 10-year Treasury yields invert, the market has historically risen over the next 12-month period. Take a look at the following historic chart from each of the last expansion cycles since the 1970s whereby the yield curve had inverted. (Table provided by Troy Bombardia)

As one can see, stocks tend to do well, even after the inversion. Trouble for the stock market tends to start AFTER the Fed stops hiking interest rates, due to a notable slowdown in the economy. At present, the Fed is still hiking rates and plans to do so in 2019.

Finom Group subscribers may have recently benefited from some of the disseminated notes of one our preferred market analysts Marko Kolanovich of J.P. Morgan Chase. Back in November, Kolanovich offered his bullish thesis for the end of the year and during a time when markets were under severe pressure. See these notes below, which were delivered in our research report titled S&P 500 Met With Headwinds and Tailwinds This Week: Which Way?

J.P. Morgan Quant Team Notes

As we’ve done throughout 2018 and when we believed it to be appropriate, we’ve offered some notes from various analysts and firms on Wall Street. One highly valued analyst team is that which is led by Marko Kolanovic of J.P. Morgan Chase’s quant team. In the most recent notes, Kolanovic and his team discuss their market outlook through year’s end.

- Equities are close to triggering upside momentum signals, that could see CTAs re-lever and drive further market upside.

- With fundamentals intact, fundamental and systematic investor positioning more supportive, buybacks strongly re-accelerating post-blackouts, and the market-positive midterm election outcome, we maintain that the recent sell-off is temporary and see further equity upside into year-end. In particular, we favor higher beta exposures and recommend positioning for upside into year-end.

- We believe favorable and credible progress on the China trade war is more likely than not into year-end (i.e. ≥51% probability) as President Trump can no longer count on Congress or the Fed for economically supportive policies. However, the option market appears to be materially underpricing this probability.

- Global Hedge Funds are significantly underperforming the market YTD (HFs down ~4% vs. the market up ~5% YTD through Wed), and their market exposure is below average after their sharp de-leveraging during the October sell-off. Moreover, YTD our Equity Strategy colleagues estimate that just 35% of active managers are beating their benchmarks YTD, a significant deterioration since mid-year (when ~45% were outperforming). As a result, we could be setting up for a year-end performance chase.

“The market has rallied ~8% from its Oct 29th intraday lows, as the exhaustion of systematic selling, reacceleration of buybacks once blackout windows passed for the bulk of companies, and more recently the removal of election tail risks allowed markets to find their footing. Meanwhile, US equity fundamentals remain resilient and corporate sentiment largely unchanged following 3Q earnings, in which ~77% of reporting companies beat EPS expectations and delivered strong 26% y/y growth. Meanwhile, dealer and systematic strategy positioning is now supportive.

Dealer Gamma Positioning: As option positions got rolled to lower strikes and the market recovered from its lows, the S&P 500 gamma imbalance came down from a record put tilt in mid-Oct to a moderate call tilt now (Figure 1). This suggests dealers are likely close to flat or slightly long gamma, and their hedging activity is no longer boosting market volatility (as it was through most of October). Figure 2 below shows the gamma imbalance by spot levels, and suggests short option gamma hedging should remain a non-issue for the time being, as long as the market trades above ~2750. The shift in gamma hedging impact should allow market realized volatility to continue to decline from October’s spike.”

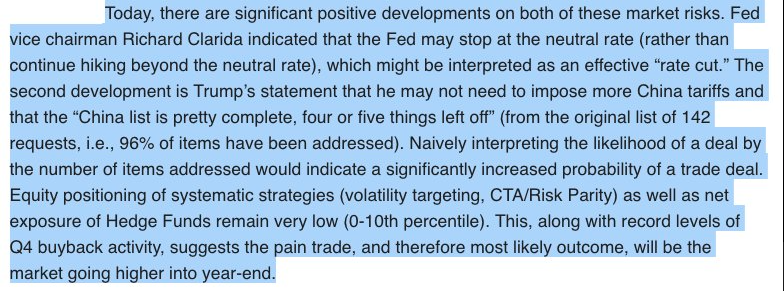

Since that time, Kolanovic and his team updated their thesis to include remarks by Fed Vice Chair Richard Clarida and Donald Trump, who has lambasted the Fed Chair for raising rates in a seemingly autopilot fashion.

Finom Group tackles the task of fact-driven analysis, void of bias and focused on market fundamentals. It’s a difficult task given the job of the contending media headlines. In general, the media is an ad-revenue based business model in search of ever increasing readers, viewers and “clickers”. The news/headlines are often sensationalized to capture the most readers, viewers and clickers. More often than not, the news narrative tends to adopt the market direction, regardless of the facts and logic that are likely to conclude in the long run. We believe it should be the other way around; the news should be fact-driven and less sensationalized with thoughtful analysis. Throughout 2018, this has been an objective, not the objective, but an objective for Finom Group; we aim to deliver the facts and logical analysis. It’s proven a meaningful advantage with regards to factoring out emotion in favor of stable and disciplined investing strategies. The reason we point this out is largely because if investors simply tuned out the media through the highs and lows of the market this year, they would come to find the benchmark has risen roughly 6% on the year, even with all the volatility. Additionally, this was a recent focus of Kolanovic’s latest notes as he has taken on the media. The reasoning; clients have expressed concern.

According to Kolanovic, JPMorgan’s clients have been asking about “the recent uptick in news stories with negative market sentiment.” The Heisenberg explains it as follows:

“Marko attributes that phenomenon to a couple of factors, the first of which is the media chasing stories in order to “fit the recent price action.” In other words, equities are falling, credit spreads are widening, volatility is elevated, so there must be a story to tell and the media being in the story-telling business, they’re of course going to oblige. Kolanovic also suggests that managers who have underperformed are effectively attempting to justify that by conveying negative views. There are specialized websites that are consistently spreading misinformation on geopolitical, social, and market issues.”

It’s a fine line to walk between opinion-based and misinformation-based reporting and analysis. Finom Group has mentioned this on many occasions throughout the year. We’ve highlighted Lance Roberts and Jesse Columbo of Clarity Financial, as representing those “sites” participating in the proliferation of misinformation. To be clear, misinformation can simply be a belief, a belief that what they are distributing in the media landscape is logical and/or accurate. But to the extent Finom Group has found, and on so many occasions, the omission of key facts and input data or the cherry picking of certain facts and input data with the omissions mentioned, there remains little doubt that they misinform the public.

Gluskin Sheff’s chief economist and strategist David Rosenberg is another of these pseudo-analysts that constantly calls for a market crash and promotes “bubblicious” warnings to capture media headlines.

His latest warning invites investors to consider that the Federal Reserve’s balance sheet reduction, not rising interest rates, could have drastic implications for stocks. It’s not that this isn’t a logical headwind for equity price appreciation, but rather the only narrative ever offered from Rosenberg is one that concludes with a market crash. It’s the Rosenberg mantra year-after-year-after-year-after-year! With all that said, let’s take a look at the latest notes from Marko Kolanovich and his team.

“Many clients have asked us about the recent uptick in news stories with negative market sentiment. Our analyses suggest that most of the press (as well as many investors) are ‘trend following’ and fit the fundamental narrative to recent price action. There are other biases – e.g. managers that are underweight or trailing the broad market are more likely to convey negative views. There are specialized websites that are consistently spreading misinformation on geopolitical, social, and market issues. A number of sell-side firms forecasted an escalation of the trade war at the G20 meeting or a looming bear market, and are now defending those views. We think that some of the prominent negative macroeconomic views are entirely inconsistent – for instance, a view that in 2019 we will have a combined economic slowdown, rapid hiking by the Fed, and significant escalation of the trade war. This view has a simple logical mistake: these 3 events are not independent (higher likelihood of one, reduces the likelihood of the others).

We think that the G20 meeting brought significant progress in the US-China relationship and should be positive for the market going into year-end. We stated previously that US-China trade dynamics are largely driven by the US political cycle and performance of the US equity market. We believe, simply speaking, that the administration cannot afford a falling market, large trade related layoffs, and fleeing donors in a pre-election year. The trade war did not yield the desired political results in the US mid-term elections. It did not rally the lower-income and rural base, it crippled middle-income 401(k)s a month before voting, and it alienated the business community and wealthy political donors. After losing the House, the trade war is less likely to be escalated given the inability to pass new fiscal measures to counter an economic slowdown (last year’s fiscal stimulus is wearing off). We often hear that trade is an important economic issue with bi-partisan support. We would like to note that over the past 20 years, global trade was responsible for significant gains in the US economy, stock market, income and wealth of the US population. However, trade with China and the decline of certain US demographic segments can easily be cast into a populist political issue acceptable on both sides of the aisle. This was outlined by Peter Navarro himself in the 1990s while he was still a Democrat and a proponent of free trade. Moreover, some of the issues around trade with China have prejudicial/racial undertones. For example, last week on national television we heard disgraceful statements how the Chinese are ‘not capable of innovating’ and hence have to steal IP, or how proponents of free trade are part of ‘globalist elites’ conspiring against white blue collar workers, etc. Our view is that despite likely additional volatility and more ups and downs, the ill-conceived trade war with China is ending. Ironically, this may have been summarized by Larry Kudlow’s interview last week when he said: “…at the end of that rainbow is a pot of gold. You open up that pot and you have prosperity for the rest of the world, but you’ve got to get through that long rainbow.” We all know that there is no pot of gold at the end of a rainbow, and that searching for one is a misguided effort. To summarize, we expect the easing of trade tensions will be a significant positive for equity markets.

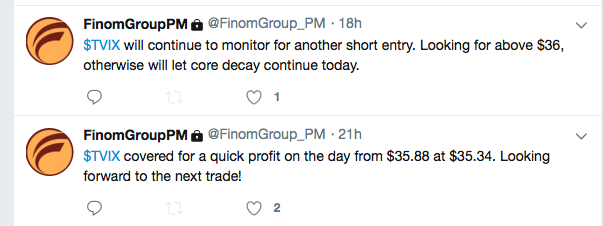

So there’s a lot of noise out there, what else is new with respecting to the media and the investing landscape? What’s most important is establishing and surrounding oneself with strong resources! We encourage our readers to subscribe to our weekly research reports and analysis as it has proven an accurate forecast for the markets. Additionally, readers are also welcome to join our trade alert service. Yesterday’s trade of the day was within the volatility complex as depicted below.