When geopolitical headlines strike and when they have no effect on corporate earnings, it can often bring with it opportunity. The major averages largely finished lower after headlines concerning the proposed U.S./N. Korea summit was cancelled. President Donald Trump scrapped plans for a summit with North Korean leader Kim Jong Un, citing “open hostility” from the North Korean regime, as the White House considered dozens of sanctions on Pyongyang. President Trump canceled the meeting without informing allies, including South Korean President Moon Jae-in.

This headline broke in the early morning, Wall Street trading hours and sent the Dow tumbling. At its lowest point, the Dow was down some 280 points. The VIX rose roughly 10% into this market turmoil. It was at this time that the opportunity was to be realized and acted upon. iPath S&P 500 VIX Short-Term Futures ETN (VXX) has been the preferred VIX-Exchange Traded Product for shorting volatility by Finom Group’s Chief Market Strategist Seth Golden, in 2018. During yesterday’s volatile market, shares of VXX rose sharply and as such Finom Group issued a short trade alert, to subscribers, on shares of VXX as they rose in share price. The trade alert is depicted below.

The issues and relations between the U.S. and N. Korea have been an ongoing dilemma for decades and with similar sentiment, fits and starts. Be it provocative nuclear developments and missile tests by the N. Korean regime or sanction enforcement by the U.S. on N. Korea, the relationship has never impacted U.S. corporate earnings to any degree of worthy consideration. With this historic precedence, the market’s reaction to the cancelled summit was recognizably a “buy the dip” or short the volatility moment. Markets following earnings over time, not headlines lacking consequence.

And this brings us back to that which could actually affect corporate earnings, the Federal Reserve. Investors will be expected to refocus on the U.S. economy as Federal Reserve Chairman Jerome Powell and other central bank officials are in line to speak today. Chairman Jerome Powell will appear on a panel on financial stability and central bank transparency at a conference in Stockholm at 9:20 a.m. Eastern.

The presidents of the Chicago and Dallas Feds, Charles Evans and Rob Kaplan, are expected to speak on a panel at a Dallas Fed conference on technology and disruption at 11:45 a.m. Eastern. Alongside Fed speeches, the economic calendar remains light for the final day of the week. Readings on durable goods orders and core capital-equipment orders, both for April, are due at 8:30 a.m. Eastern Time. The University of Michigan’s consumer sentiment index for May is scheduled for release at 10 a.m. Eastern.

It is often the case that the average investor mistakes media headlines for market drivers over time. Yesterday’s cancelled U.S./N. Korea summit was a perfect example of such a mistake. It doesn’t mean that the market can’t resume a downtrend, but if it doesn’t affect corporate earnings, the market is likely to rebound and “buy the dip” investors would likely be rewarded. In 2018 there have been a plethora of geopolitical issues that have not been found to affect corporate earnings, nonetheless they have shaken a great many investors out of positions and the market altogether. Let’s take a look at some market data that may confirm this subject matter and sentiment toward market participation.

According to the latest monthly AAII Individual Investor Asset Allocation Survey, stock exposure has been creeping lower for months. In April, equity holdings came in at 67.5% of the average investor’s portfolio. That represented the lowest ratio since August, as well as the fourth straight month where the percentage of equity holdings declined. Cash holdings, meanwhile, spiked to 16.6%, their highest level since May 2017. Even so, the average long-term stock position is 60.9%, and even with the jump to a multi-month high, cash holdings are below their historical average of 23.2 percent.

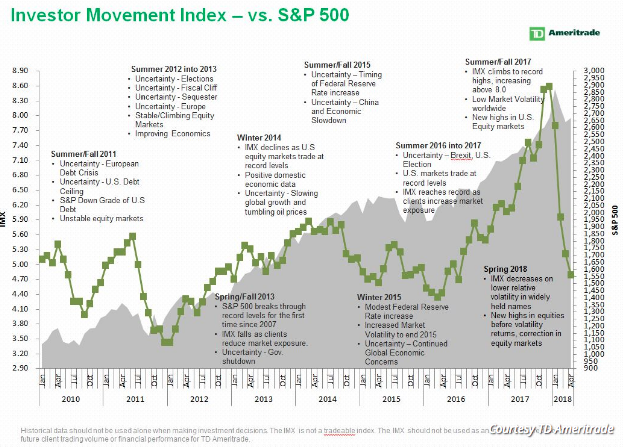

This slide in retail investor confidence can also be found in TD Ameritrade’s latest data. TD Ameritrade’s Investor Movement Index, which measures how retail investors are positioned in the market, fell for a fourth straight month in April, dropping 8% to a reading of 4.79, a 21-month low.

“The primary takeaway is that investors are taking a very conservative approach to the market. They still want to be invested, but they don’t have the will to take the kind of risk they were taking on last year. It’s involvement, but cautious involvement,” said JJ Kinahan, chief market strategist at TD Ameritrade. He added that retail-investor exposure to equities as “a little above average, down from last year’s highly above average.”

The average investor and trader have been confronted with many headwinds for equity price appreciation in 2018 and the first market correction in nearly 2 years, which occurred in February. Volatility has risen off of historically low levels in 2017. The geopolitical picture has been muddied and finding daily and weekly headlines with regards to trade tensions. It has been a rough road for investors and traders to travel in 2018 as the bull market has aged. Concerns are growing that the economy is in a late stage of its expansionary cycle, and the percentage of fund managers who expect the global economy to be stronger a year from now is at its lowest level since February 2016, according to a Bank of America Merrill Lynch survey.

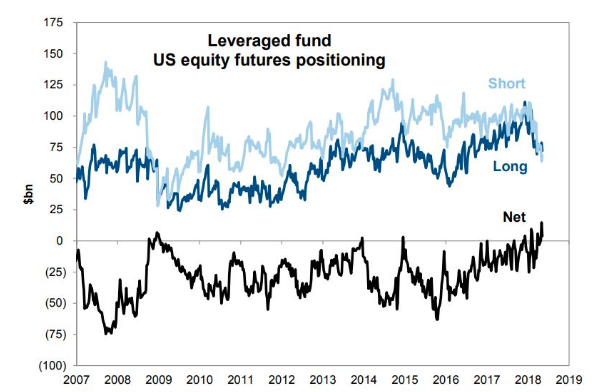

In spite of all the market headwinds, the major averages are still up for the year, even if ever so slightly. Also in spite of the aforementioned turbulence in the markets, hedge funds remain in the market with high margin debt. Margin debt refers to the money that investors borrow to buy stocks; it is viewed as a measure of speculation. According to data from Finra, margin debt came in at $652.3 billion in April, the highest level since January’s $665.7 billion reading.

“According to Goldman Sachs, “Hedge funds have maintained elevated exposures, with net length only slightly lower than at the start of 2018 despite a volatile market,” it wrote in a note to clients. It added that gross and net leverage were “below January levels but elevated relative to history. For the first time since the start of 2009, leveraged hedge funds have a “substantial net long position in U.S. equity futures.”

Given the data at hand and larger institutional equity market participation, the average investor should ask himself or herself if they are trading based on emotion driving headlines or fundamentals. This year will prove to be a more challenging year for the average trader, where simply buying an index fund may not generate double-digit returns as funds had in past years. Stock picking may also prove more relevant than in recent years. But most importantly is the adherence to fundamentally driven investing strategies that focus on what drives markets, earnings. Certainly rising rates and yields cause markets to pause and even compress price-to-earnings/multiples, but historically it has not found equity markets to decline when earnings rise in tandem with rising rates/yields. While risk/reward is not as favorable in a rising rate environment, equities should once again win out in 2018 with S&P 500 earnings expected to rise 17%-19% for the year.

With all that being said, Friday is likely to find market volume lighter than usual ahead of an elongated Memorial Day Holiday weekend. U.S. equity futures are higher this morning as bond yields and oil are both on the decline. Finom Group hopes to find your trading day a profitable one and we salute our fallen soldiers and those who dedicate themselves to the protection of this great nation and its citizens, beliefs and founding principles!