That was a pretty bullish end to an otherwise fear littered week that centered on two major points of interest, trade tariffs that could possibly lead to a trade war and the Nonfarm Payroll report that brought with it wage inflation data. Prior to these two highly hyped market realizations coming into focus I offered my views on the markets to David Lincoln in a YouTube interview.

About 40 minutes into the interview, I stated that if the markets could withstand the realization of the details from the trade tariffs alongside a tamer wage inflation number, then markets could rally. And surely enough, or maybe fortunately enough the markets did rally on a more subdued trade tariff proclamation and a more tame wage inflation number that was supported by a bump in the labor force participation rate.

Although the headline number for the Nonfarm Payroll report was nothing short of awesome, at 313,000, the supporting data was subdued and allowed for the relaxing of fears that inflation was rampant and here to stay. The unemployment rate was unchanged at 4.1%. Hourly pay rose 4 cents, or 0.1%, to $26.75 an hour. The 0.1% wage rise was significantly less than the 0.3% expressed in January. Immediately after the data was released, equity futures rallied sharply.

On Friday, the Dow Jones Industrial Average surged 440.53 points, or 1.8%, to end at 25,335.74 for a weekly gain of 3.3 percent. The S&P 500 index climbed 47.60 points, or 1.7%, to close at 2,786.57, ending the week 3.5% higher. The Nasdaq Composite Index added 132.86 points, or 1.8%, to finish at 7,560.81, up 4.2% for the week and ending the week with a record close. It remains to be seen if last weeks rally has given the all-clear signal for equity buyers and with previous, correction territory lows much farther off than new S&P 500 highs.

It was a welcome sight for the markets to rally as strongly as they did Friday and after declining, almost on par with the way they did when trade tariffs were introduced in the previous week. More importantly, however, was the reduction of fear or volatility in the market to end the week. The VIX fell for much of the week and ended the week at just 14.64% or down 11.5% Friday. This was the lowest VIX reading since prior to the Feb 5 VIX event that found the VIX reaching beyond 50 and with the DOW falling some 1,000 points.

In a conversation at finomgroup.com , I was asked as to what levels of the VIX I saw being a probability near term. At the time, the markets were struggling with the trade tariffs, 3 or 4 rate hikes and the potential for persistent wage inflation. With the VIX achieving my forecast of 14 on Friday, we’ll have to see where it goes from here. I have my forecast for finomgroup.com subscribers and hope to share more thoughts on the VIX with the general public in the near future. But for now, the markets have overcome key concerns and may continue to find stability in the coming weeks. Again, it remains to be seen.

The jobs report was strong and with that came some adjustments to fed-funds futures market. It’s pretty much a guarantee, at this point, that in a couple weeks the Fed will indeed increase rates by a quarter basis points and from the current target range of 1.25%-1.50%. This rate hike will take place at the March 20-21 FOMC meeting. But the big question is whether or not a 4th rate hike is in the cards. At present, the chances are slim for 4 rate hikes, but should economic data continue to come in strongly and corporate profits rise to the degree they are currently being estimated by Thomson Reuters, fed-fund futures may adjust for a 4th rate hike in 2018. It’s this looming variable that will likely keep equity markets on edge for much of the year or in a higher, YOY volatility regime.

An interesting aspect to the current market sentiment and general market direction is the lack of historical bond-equity correlation. In other words, historically bonds have proven a hedge and a means of diversification for portfolio and asset managers. What we are experiencing in 2018, however, is entirely different. Bonds are not behaving adversely to equities. Usually when equities decline, especially in a disorderly or rapid manner, bonds tend to rally. But we’re really not seeing that to any degree of significance and as bond yields indicate somewhat of a flat lining over the last few weeks. Things may very well be different this time and as central banks are tightening fiscal policy and reducing their balance sheets. The Fed, the European Central Bank, and the Bank of Japan will aim to cumulatively cut back their purchases this year.

This year has seen an end to this negative correlation between Treasuries and equities, Jim Bianco told clients in a conference call last week. As such, it calls into question just how portfolio managers will diversify and hedge going forward, or maybe they have already figured it out by using expensive .SPX options and the VIX complex.

What equity and bond markets will do next is less about guessing and more about paying attention and paying attention to “the right things”. What are the right things though? Historically, equities follow earnings over time and earnings expectations continue to ratchet up for 2018. But before we take a closer look at S&P 500 expected earnings, let’s take a gander at what J.P. Morgan’s quant team said last Friday.

“We believe the current U.S. administration has a vested interest in rising and stable U.S. equity markets ahead of important November mid-term elections.”

I tend to agree with the quant team at J.P. Morgan who are lead by Marko Kolanovic. Marko had suggested, even prior to the trade tariff and wage inflation fears found relief, that investors should be buying the pullback in equities. In the quant team’s research notes released on March 2, 2018, they depicted the extreme levels of corporate buybacks set to take place in 2018. Some $800bn in gross share repurchases is already slated for this year with room for upside to that number. With such levels of corporate buybacks accompanied by rising corporate earnings, Marko and his team advised clients to be buying the dips in equity prices.

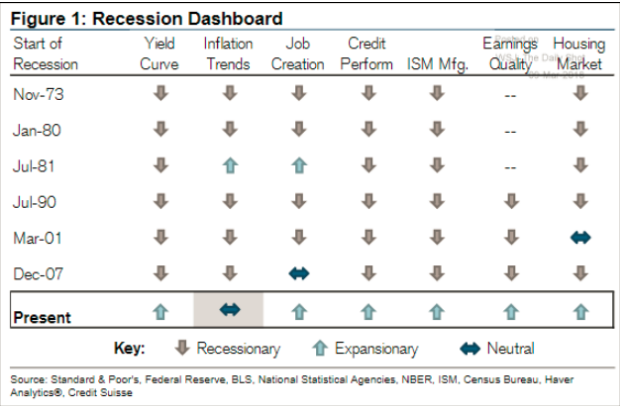

Moreover, recessionary fears continue to loom, but may ultimately be found…early, or too early I should say. A recent Credit Suisse chart reviewed the onset of recessions with variables such as the yield curve, ISM manufacturing job creation and more. Below, Credit Suisse defines the risk of a near term recession across these variables.

I don’t think equity markets are “out of the woods” just yet. As Finom Group’s Chief Technical Analyst Edward Cordoba pointed out several weeks ago and post the market correction, in order for equity markets to satisfy the that the 12% correction would not lead to a broader market decline or bear market, the S&P 500 would need to recapture and surpass its previous highs. Next week’s start of trading will be critically important as it will likely set the trend for the broader indices and ahead of the highly anticipated first rate hike of the calendar year.

The “wall of worry” may still persist in the form of inflation fears, but that is not to suggest that equity prices can’t appreciate during an inflationary/reflation period. Historically, equity prices have appreciated during such periods, but up until a point where interest rates impact lending, consumer credit and debt portfolios. Admittedly, credit card debt levels are at all-time highs and beg to question how higher interests rates will affect consumer spending in the future. https://www.cnbc.com/2018/01/23/credit-card-debt-hits-record-high.html .

As stated previously, the debate will likely persist throughout the year regarding inflation and just how many rate hikes will occur in 2018. I’m of the opinion that 4 rate hikes will take place, but open to being proven in error with this forecast. I am also of the opinion that equity markets will continue to march higher in 2018 and with intermittent fits and starts such as what we’ve seen in the first quarter of the year already. At Finom Group we continue, as always, to focus on the corporate earnings picture.

Aggregate Estimates and Revisions

- Fourth quarter earnings are expected to increase 14.8% from Q4 2016. Excluding the Energy sector, the earnings growth estimate declines to 12.6%.

- Of the 493 companies in the S&P 500 that have reported earnings to date for Q4 2017, 75.9% have reported earnings above analyst expectations. This is above the long-term average of 64% and above the average over the past four quarters of 72%.

- Fourth quarter revenue is expected to increase 8.3% from Q4 2016. Excluding the Energy sector, the revenue growth estimate declines to 7.2%.

- 0% of companies have reported Q4 2017 revenue above analyst expectations. This is above the long-term average of 60% and above the average over the past four quarters of 63%.

- For Q1 2018, there have been 67 negative EPS preannouncements issued by S&P 500 corporations compared to 55 positive, which results in an N/P ratio of 1.2 for the S&P 500 Index.

- The forward four-quarter (1Q18 – 4Q18) P/E ratio for the S&P 500 is 17.3.

- During the week of Mar. 12, seven S&P 500 companies are expected to report quarterly earnings.

As investors and traders can clearly see, the outlook for corporate earnings continues to improve on a weekly basis. And 2018 is proving to be favorable thus far for corporate earnings. Reuters is forecasting Q1 2018 corporate earnings growth of 18.2% from the year ago period.

In 2018, investors and traders should expect higher volatility levels than in 2017 and the choppiness that has characterized the first two trading months of the year to also persist. For the full-scale report, feel free to subscribe to finomgroup.com