Pretty much what we expected from the market on Monday, pretty much what we expected. In our weekly Research Report, Finom Group alerted subscribers to the likelihood of markets continuing their retreat from last Friday. We actually considered the selling pressure would worsen given the market’s ability to finally secure an excuse for which to work-off some overbought and overextended conditions that have been building for some 2-3 months now. The following excerpt is from our latest Research Report titled “Will Overbought Conditions Offer a 5% Sale for S&P 500?“

“The coming trading week, in my earnest opinion, is likely to start off rather poorly. In fact, I would expect as much as a 1% intraday drawdown on the S&P 500 to happen either Monday or Tuesday. Simply put, the headlines over the weekend haven’t improved around the Coronavirus and while I believe this to be just another momentary crisis that will be hyperbolized in the media, that’s all it takes for the market to move lower after such an exhaustive move higher through the last 4 months.”

When it was all said and done on Monday, not only did the S&P 500 (SPX) and Dow Jones Industrial Average (DJIA) fall 1.57% on the day, the Nasdaq (NDX) fell some 1.9% ahead of key earnings results on Tuesday from Apple Inc. (AAPL). Additionally, with just one trading day completed this week, it looks like the probability of a 3 sigma move is increasingly probable. Why do we say that you might be asking. Each week Finom Group also discusses the S&P 500’s weekly expected move inside its weekly Research Report. This gives investors and traders an idea of what the options market is pricing in so far as how much they are anticipating the S&P 500 to move for the week and in either direction. For the current trading week, the options market had priced in a $52/point weekly expected move. What actually happened Monday found the S&P 500 already exacting that full week expected move.

Everything the S&P 500 would add to the losses on Monday lends itself to an outsized weekly move, beyond what the options market had already priced.

The good news, if there is some to be gleaned from Monday’s wake-up call on Wall Street, is that the S&P 500 finished the day still more than 1.5% above its 50-DMA. The key support area resides at 3,195 presently and may still yet come into play if the selling pressure picks-up again on Tuesday. Investors will increasingly find themselves focused on this key moving average, support level near-term and given the uncertainty in the market.

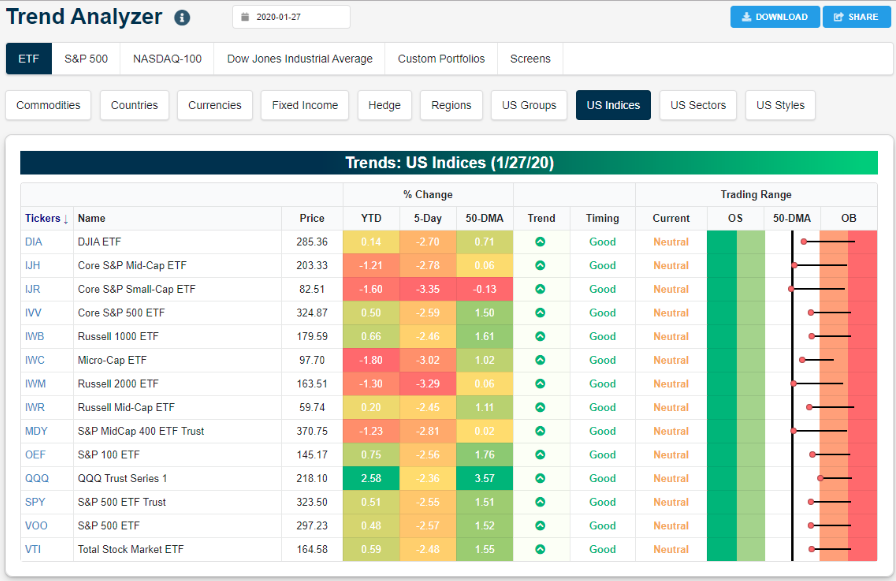

In addition to the benchmark support level coming into focus, while overbought index positions are now less overbought, index ETFs are also less overbought. According to the Bespoke Investment Group Trend Analyzer, like the S&P 500 index, most index ETFs remain above their 50-DMA, which highlights overbought territory.

After Monday’s poor market performance, the S&P 500 is off some 2.6% from its all-time high achieved just last week. The market has taken the stairs up and through the last 4 months, gaining almost 13% since October 2019. Unfortunately, the stairway up is usually pared by the market taking the elevator down and falling more rapidly than it rises.

The other question in focus for investors, as the market aims to work-off some frothy conditions and using the uncertainty from the Coronavirus and upcoming Iowa Primary as an excuse to do so, is how deep of a correction will be achieved? Forest Gump, the famed movie character played by Tom Hanks once said, “Corrections are like a box of chocolates: you never know what you are going to get.” Okay, that’s not really what he was referring to when he articulated now one of the most famous movie phrases, but we thought it would prove fitting… and why? The current pullback could be a shallow pullback, a deep retracement, a sideways range or the a full-blown, textbook 10% correction… possibly even more. There simply no guarantee what the market will do from one day to the next, which is why the statistical probabilities and experience are all we have in our arsenal of tools to guide us forward.

History of markets led us to believe the market was leading to a near-term correction and Finom Group had outlined the increasing probability of a corrective period was afoot. At this point, we are not turning long-term bearish because market breadth models remain bullish and the S&P 500 is well above its rising 200-day SMA. Keeping in mind that the S&P 500 was up some 13% from early October to mid January, a corrective period at this stage would be perfectly normal and even healthy.

With the pullback narrative hitting market’s on the head like a hammer, the index futures are attempting to rebound Tuesday morning. The uncertainty is still freshly being considered by investors, but some strategist are viewing the pullback as little more than having the potential to retrace 5 percent.

While Finom Group has found extreme forecasting and analytical errors throughout 2019 from Michael Wilson, Morgan Stanley’s chief U.S. equity strategist, for the sake of reviewing certain analysts’ market commentary, we offer his latest comments. Of course, Wilson says, “The first major stock market pullback since October may be under way.”

Ahead of the FOMC rate announcement and press conference Wednesday, Mike Wilson said that the market’s slump is likely to be limited to a 5% correction due to a Federal Reserve that has proven quick to provide liquidity to stalled-out markets as well as ultra-low interest rates.

“While near-term risks have increased, we think that corrections at the index level will be contained to 5 percent or less while the defensive skew outperforms both growth and cyclicals until rates show some signs of actually bottoming or hard data suggests the recovery will be more robust than we currently expect.”

While each and every bearish view on the market from Mike Wilson failed to meet the mark in 2019, it’s always a good idea to hear from as many Wall Street analysts as possible. This latest offering from Wilson indicates he has somewhat “caved” to the Fed’s might and ability to secure financial markets’ stability and perceived value, even if the economic data and earnings haven’t proven terribly robust through 2019. In addition to Wilson’s latest thought’s on the market and its potential pullback, Fundstrat’s Tom Lee offering the following on the potential pullback depth:

“We think more weakness likely in the next few weeks towards the [50-day] and probably [100-day] moving average, which is 3,195 and 3,095, respectively (5% to 7%) .. as a cumulative number of factors does heighten the risk that 1H Global GDP comes in the weak side.” – @fundstrat

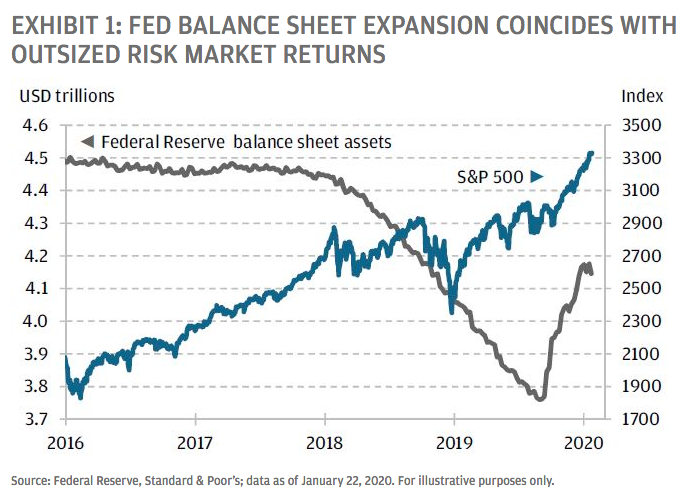

Ahead of the FOMC meeting, Finom Group analyzed and discussed with subscribers the likelihood that as the central bank curtails its repo market and bond buying activities, this would offer the market a sentiment shift, something bearing an adjustment for risk assets. While it’s no secret that the equity market shifted even more positively since the Fed engaged in the expansion of its balance sheet (Q4 2019) the sole reasoning for the market rising isn’t the Fed. This blame is more coincidental than it is whole. Nonetheless, we can’t dismiss the extent of the rise in risk assets has, in part, been fueled by Fed induced credit market liquidity, which lends itself positively to equity markets.

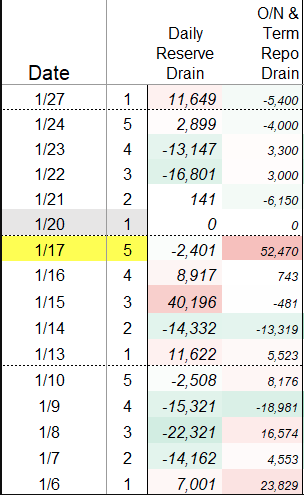

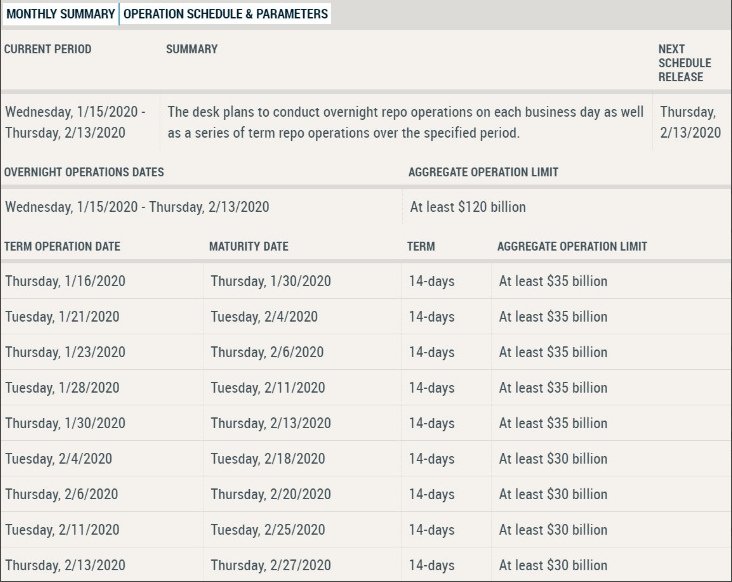

As we can see in the chart above, the S&P 500 had already been rising sharply at the onset of 2019 and through the first half of last year. The added Fed, credit market liquidity simply gave the S&P 500 another boost of sorts. But now that the Fed is curtailing its Repo market and bond buying activities, investors are more forced to rationalize equity market valuations. To be clear, the Fed isn’t reducing its balance sheet as it had been from 2018-Q32019, it’s simply maintaining it going forward, which is less attractive for many investors than broad-based expansion of the balance sheet. The following chart of Fed activities identified that Monday was likely to be a somber day on Wall Street, regardless of the Coronavirus headlines.

Identified in the table of Fed daily reserves, we can see there would be a drain on reserves, which would otherwise reduce liquidity and pervade equity market sentiment and participation. Currently the Fed is scheduled to reduce its bond purchase activity by roughly $20bn a month as shown in the schedule/table below. The next schedule won’t be released until 2/13/2020, after the Iowa Primary results.

As one can see, there are currently 3 uncertainties weighing on risk assets.

- Fed Balance Sheet activity

- Coronavirus

- Iowa Primary

While the impact of those uncertainties are front of mind, they are all expected to find solutions in the interim. As such, a market correction of sorts until these issues are found for remedies is the greatest probability. With this in mind, J.P. Morgan recently weighed in with comments over the seemingly overheated markets, but likely warranted front-running of an economic rebound.

“To be sure, the economic outlook has clearly improved, for two reasons we believe. First, geopolitical headwinds have faded, most visibly in the signing of a “phase one” trade deal between the U.S. and China that signals no further escalation, but also in Congressional approval of the USMCA trade deal between the U.S. and Canada, and greater certainty on Brexit following the UK general election in December. Second, indicators of economic activity have begun to rebound, pushing Citi’s Economic Surprise Index for the global economy to its highest point in nearly two years. Improvement has been most evident in timelier surveys, such as the weighted average of Global Purchasing Managers’ Indices (PMIs), while some data points that caused heightened concern months ago have lately improved These include trade and factory output in Asian bellwether economies like Taiwan and Korea, where officials now point to a pickup in semiconductor demand, in turn a signal for a pickup in global capital expenditures. For the U.S., our team’s qualitative assessment of recession odds over the next 12 months has dropped from 40% in August to 25% in early January.”

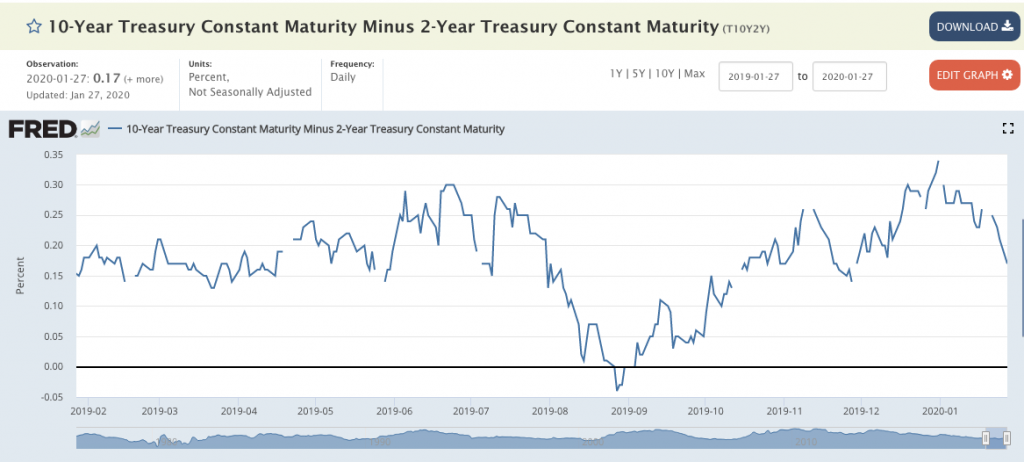

Wow, just 25% probability of a recession over the course of 2020! While many were fearful of a recession after the year curve inverted in mid-2019, since the yield curve has un-inverted, the tide has certainly changed. Of course, de-escalating tensions in the U.S./China trade feud and the signing of a phase-1 trade deal have gone a long way in soothing economists’ fears, but we’ll have to keep an eye on the yield curve which has flattened out over the last week rather robustly.

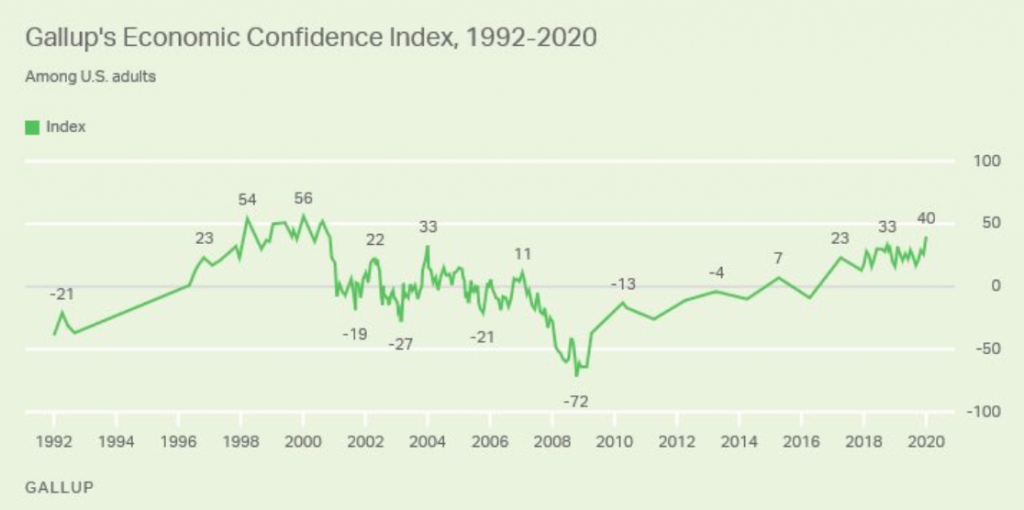

As shown in the chart above, the spread between the 2s/10s peaked on December 31, 2019, but has since flattened to just 17 bps, even with the Fed purchasing bonds. The difference in the recent expansion of the Fed’s balance sheet from the prior period, is that the Fed is buying shorter duration maturities. Even so, the long-end of the curve is still being suppressed by outright demand of longer maturities seeing how the U.S. debt markets are still found with the best yields globally. Should the yield curve continue to flatten, we would expect investor fears of a recession to come into focus. Nonetheless, for the hear and now, it seems recession fears have abated and the average American doesn’t find a recession of much concern. Americans haven’t been this confident in U.S. economy in nearly 20 years in fact and according to the latest Gallup Poll.

While recession fears, are less prominent at the onset of 2020 when compared to 2019, the current path of equity markets remains that of least resistant and underline market uncertainty in our opinion. There’s no one thing that we can point a finger at and say this is why the market has corrected some 2.5% from the all-time high. All we know is that the market had been looking for an excuse and the bond market had been signaling a correction was looming, with yields falling since the New Year.

Moreover, the latest epidemic crisis has simply added fuel to the fire for the upcoming FOMC meeting. While nobody expects the Fed to move on rates, many desire to hear about how the Fed gauges its the efficacy of its latest Repo market activity and what it might be able to do support economic growth should the epidemic curb economic activity. Coming into the year, Fed Fund Futures weren’t pricing-in any rate change for the calendar year. But that has quickly changed in just the last week and as yields have tumbled alongside proliferating Coronavirus headlines. Capital markets are beginning to discount the possibility that the Fed will use interest rates to offset growing economic uncertainty caused by the outbreak.

Fed Funds Futures have moved noticeably in the last week, with increasing odds for a 2H 2020 rate cut (or two):

- Futures discount stable Fed Funds through Q1. The odds that rates remain unchanged through the March meeting have not budged in the last week and run 84% – 86%.

- The story changes when you look at the odds around the June 2020 FOMC meeting. A week ago the probability of a rate cut by then was 14%; now it is 25%.

- Last week’s trend to higher expectations for a 2020 rate cut increase as you look at September’s contracts. A week ago, the odds that rates would be lower than today were 37%; now they are 50%.

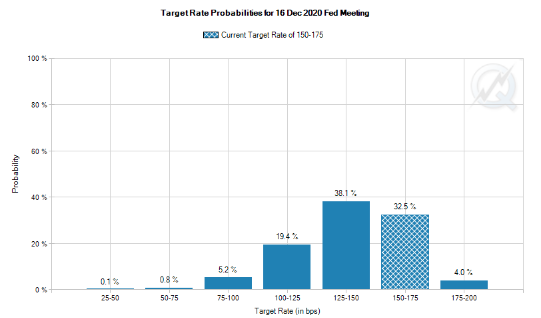

- Fast forward to the December 2020 meeting (chart below, courtesy of the CME FedWatch Tool), and the odds that the Fed cuts rates this year rose last week to 68% from 54%. Moreover, the probability that the Fed cuts by 50 basis points or more rose from 17% to 30% last week.

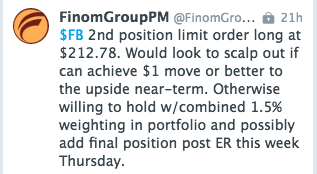

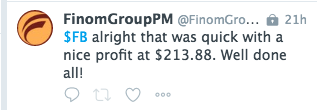

It would appear as though the Cornavirus epidemic, which is not a pandemic at this time, is seeping into every aspect of financial market activities and operations. That’s what headlines cause folks, that’s what headlines cause. But to that cause, what should you do as an investor. Finom Group is of the opinion that patience and discipline are the exercises of the day. Patient and disciplined investors/traders are likely to be rewarded. We outlined our key “game plan” ideas for market participants in our latest weekly Research Report. Now it’s just a matter of execution as we look for opportunities on a daily basis. With the early market gap down on Monday, we took advantage of the opportunity we saw in shares of Facebook (FB) tumbling along with the broader market.

Just like Monday, Finom Group will continue to look for these kind of market opportunities to deliver to our subscribers. But Jim Cramer is of likemindedness regarding patience and discipline. During his daily commentary on CNBC Monday, the Mad Money host offered the following:

“This is the panic people have been waiting for. We’ve been saying over and over if we get an exogenous event that’s when you get the sell off, that’s when you have to buy. I just don’t think today” is the time to buy back into the market. I see the potential for the market to take a “second leg” down if the World Health Organization were to declare a global emergency over the coronavirus.“

The good news about the recent pullback in the equity markets is that it is giving some relief to the overextended conditions not just in price, but sentiment.

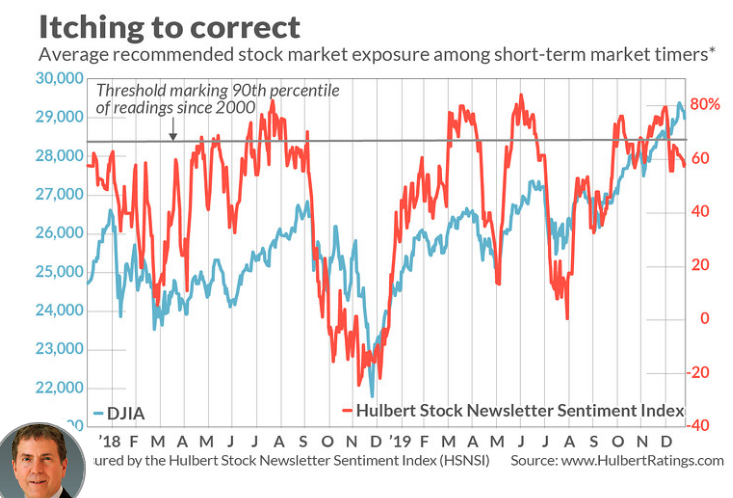

Famed newsletter writer Mark Hulbert says virus and Fed be darned, the real problem for markets was overheated sentiment. In his latest missive, Hulbert offered that it was only a matter of time before sentiment demanded a market pullback and provided a more neutral market sentiment amongst investors/traders.

“That real culprit is market sentiment: Short-term stock market timers, on balance, have been extraordinarily bullish for a couple of months now. Even a few days of such excessive bullishness would normally lead to market weakness, much less a few months of such exuberance. So conditions were ripe for a pullback.

If it weren’t the coronavirus, in other words, something else would have been the straw breaking the camel’s back.”

“Consider the average recommended stock-market exposure level among the several dozen short-term stock market timers I monitor on a daily basis. (This average exposure level is what is reflected in the Hulbert Stock Newsletter Sentiment Index, or HSNSI.) As you can see from the chart above, the HSNSI since October of last year has spent more days above the 90th percentile of past daily readings than below.”

The market was looking for an excuse folks, and as we edged closer to the Iowa Primaries, it found several excuses to bring about a pullback. With Apple and other companies set to report results after the closing bell and through the remainder of the week, it becomes increasingly important to focus in on how results are treated by the broad investor community. Thus far, good or bad, earnings have been met with selling pressure. We’ll see if this trend continues or is met with the belief that earnings will indeed rebound for the whole of 2020.