Everything bounced on Monday on… well there really wasn’t any significant news for which the market could reactively bounce. Sure the UK and EU agreeing on a Brexit format/plan was a positive, but it’s highly unlikely that would cause a greater than 1.5% move higher in the S&P 500 (SPX). No, we simply found some buying activity that was likely produced from optimism centered on the market’s current valuation being relatively cheap, even when considering a slowdown in global economic activity and a potential slowdown in U.S. earnings out in 2019. Valuations matter in good times and bad times. More importantly, however, is whether or not Monday’s relief rally has legs. With that in mind, here’s what we need to see happen in order for a more sustainable rally higher:

- The G-20 meeting, where President Trump and President Xi Jinping will meet, needs to have some semblance of a positive tone on trade between U.S. and China. A deal is unlikely to come out of the G-20 meeting as there simply isn’t enough time to generate one at the Summit, but restarting trade negotiations as part of a framework for a future trade agreement would be a net positive for the market.

- Apple Inc. (AAPL) shares need to stabilize, form a base and begin to trend higher. Some of this could be tied to the G-20 Summit meeting sentiment. AAPL’s weighting is simply too big for the market to ignore and has weighed it down significantly. Without AAPL stabilizing, the Financials will have a lot more heavy lifting to do, something not to overlook.

- Oil prices also need to stabilize, which in turn can also prevent the U.S. Dollar from surging and help the USD form a peak. Saudi Arabia raised oil production in November to 11.3mm barrels per day, an all-time record high. An oil production cut is expected when the Organization of the Petroleum Exporting Countries(OPEC) meets in Vienna next week amid worries over a U.S.-China trade war, a supply glut and demand slowdown, according to Johannes Benigni, chairman and founder of consultancy JBC Energy Group.

“OPEC will probably manage to stabilize the oil market by choosing the right language. They will indicate a cut of between 1 million and 1.5 million, and that will do, the market probably will stabilize.”

- Federal Reserve Chairman Jerome Powell will be speaking publically on Wednesday and market watchers will be playing close attention to the Chairman’s words. Some Fed officials including Vice Chairman of the Fed, Richard Clarida, have already begun to pronounce a more dovish tone when it comes to future rate hikes. Powell simply needs to follow through. A December rate hike is already baked into the market, but the market wants to hear that the Fed will be looking more closely at the economic data in light of a slowing global economy, a slowing domestic housing market and tame inflation that finds the Fed closer to its neutral rate than previously thought.

If the market gets all these issues resolved favorably, which is not a hard achievement, just a quantitative one, the market can find a natural equilibrium in valuation and future expectations from earnings growth in 2019. The variables above are all man-made problems and can be managed by more favorable rhetoric, but will they is the question still in play.

In Finom Group’s weekly research report (delivered Sunday mornings), we noted each of these issues were in need of resolution while also focusing on the current market valuation that seemed unreasonable even with slowing growth expectations.

“Thomson Reuters also anticipates Q4 2018 earnings to grow around 19% and roughly 9% in 2019. With the S&P declining since October, the market multiple has contracted, making equities more attractive than they have been in quite some time. The current S&P 500 forward 12-month P/E ratio is at 15.3 percent. This P/E ratio is below the 5-year average (16.4). On the other hand, the S&P 500 trailing 12-month P/E is roughly 18.7% and at its lowest level since 2014. Anyway you slice it, forward or backward, the market is relatively cheap.

G-20 Could Hold the Cards For Year-End Rally

The G-20 Summit will kickoff this Friday and with mixed headlines heading into the event. All eyes and ears will be tuned into President Donald Trump and China President Xi Jinping in Buenos Aires, as the two will hold court at the Summit. There is hope that both sides will show a willingness to negotiate and hold off on a further escalation of tariffs. Stakes are high for the talks between Trump and Xi, and traders have been awaiting that meeting as a potential catalyst that could shake the market out of its current slump.”

CNBC’s Jim Cramer agreed with much of Finom Group’s highlighted market issues that need resolution, as he discussed them Monday on “Mad Money”.

“Stocks got “very oversold” on Friday amid a plunge in oil prices and technology-led weakness. The paid S&P oscillator hit the minus-5 level during Friday’s trading, a signal that the selling was too rash. That’s the crux of this move. In this particular bear market, we’ve had three significant declines where the oscillator’s gone below minus 5, and each time, the selling got too aggressive and it’s produced, roughly, about a 5-percent bounce.”

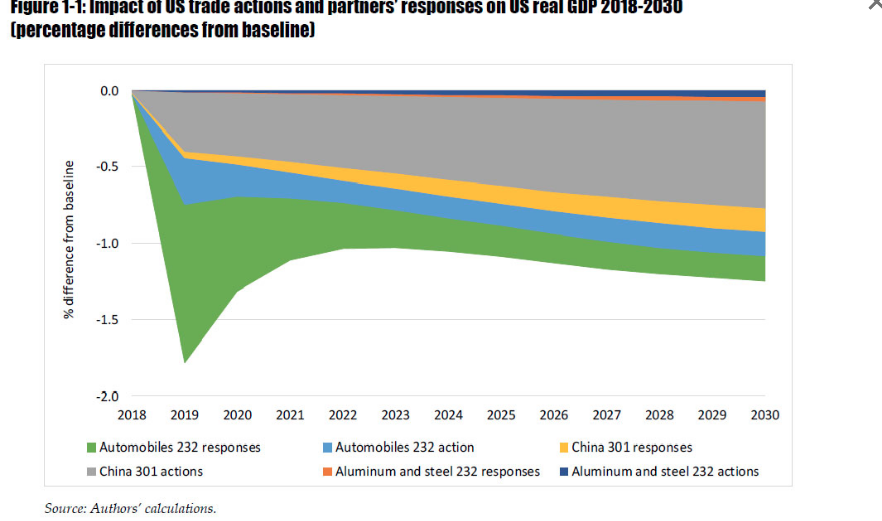

When it comes to the ongoing trade war and the affects from implemented tariffs, a new study from Koch Industries says could cost Americans $915 each, or $2,400 per household, in the form of higher prices, lower wages and lower investment returns in 2019. The study also predicts steep long-term job losses.

While strong economic growth in the U.S. initially will protect workers from job losses, the tariffs will lead to the loss of 2.75 million American jobs, the study predicts. Low-skilled workers in agricultural and manufacturing jobs would be hit the hardest under this scenario. In addition, the study figures an additional 700,000 workers will lose jobs but be able to find work in other industries. The study expects the tariffs to sap $365 billion from U.S. GDP next year. Overall, it expects GDP losses to total $2.8 trillion from 2019 to 2030.

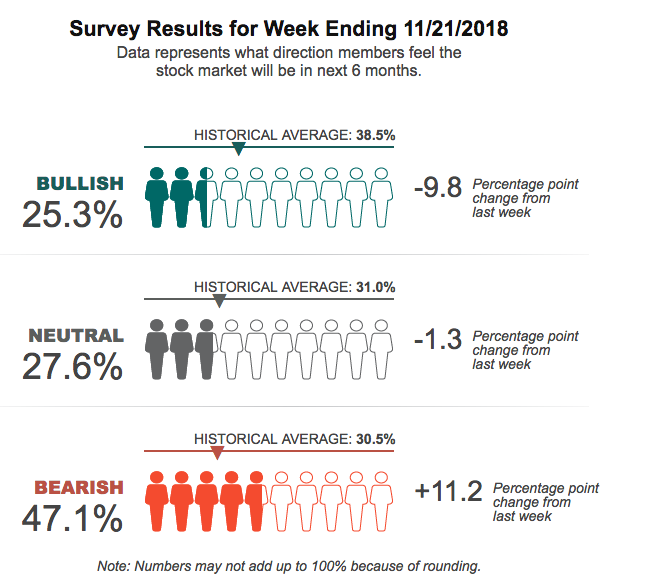

The market is currently in a contentious period whereby it has to weigh a great many issues in order to find stability and otherwise choose a longer-term trend. Markets don’t take kindly to uncertainty and where there is great uncertainty there tends to be lackluster or very unfavorable investor sentiment. We’ve seen that in recent investor surveys, most notably the American Association of Individual Investors survey.

Such are the times that investor sentiment finds historically low levels and whereby some analysts and economists further layer onto such negative sentiment with negative forecasts for the market in 2019. Morgan Stanley’s chief equity strategist, who called for the current rolling bear market, outlined his forecast for 2019 as follows.

“I see more of the same” stagnant performance from the major indexes in 2019 and forecasts the S&P 500 finishes next year at 2,750, just 3 percent above current levels. His 2019 target is the equivalent to his 2018 target, implying no growth over 12 months.

After a roller coaster ride in 2018 driven by tighter financial conditions and peaking growth, we expect another range-bound year driven by disappointing earnings and a Fed that pauses,” Wilson wrote in a note to clients Monday. “We think there is a greater than 50 percent chance we experience a modest earnings recession in 2019 defined as two quarters of negative year-over-year growth for S&P 500 EPS.

The recent strong run of growth we have seen in earnings may have lulled the market into complacency on the forward outlook, but with decelerating topline and building cost pressures, we are highly confident that earnings growth will be below consensus expectations next year and believe there is elevated risk of an outright earnings recession.”

While the forecasting of an earnings recession by Morgan Stanley isn’t promising, a relatively flat market forecast may prove promising, given the state of the market currently and with many issues that have the potential for resolution near term. Having said that, the rhetoric from the White House continues to be one that presses the patience of the markets. In a newly published article from the Wall Street Journal, the magazine outlines its recent interview with President Donald Trump. Within the interview, president Trump said he expects to move ahead with boosting tariff levels on $200 billion of Chinese goods to 25%, calling it “highly unlikely” that he would accept Beijing’s request to hold off on the increase.

“If we don’t make a deal, then I’m going to put the $267 billion additional on,” at a tariff rate of either 10% or 25%,” Trump said. Trump said tariffs could also be placed on iPhones and laptops imported from China. “Depends on what the rate is,” Trump said, referring to a possible consumer reaction if tariffs were applied to mobile phones and laptops. “I mean, I can make it 10%, and people could stand that very easily.”

Immediately following the published interview, equity futures dove in the U.S., although it didn’t seem to affect Asian markets overnight. Finom Group believes the “tough talk” continuing to come from the White House administration is more about seeming tough than being tough. What we’ve continued to see is a strategy whereby the White House makes demands on trade and even implements tariffs or sanctions, but thereafter issues a plethora of waivers or takes the lesser percentage of tariffed goods. Be it with tariffs on steel & aluminum or the former NAFTA agreement, there was much recoiling from the initial “tough talk” that ultimately found new agreements on trade or waivers for implemented tariffs. Nonetheless, U.S. equity futures are under pressure due to the “tough talk” once again.

So while there’s still a good amount of uncertainty and dark clouds hanging over the market, despite the strong bounce on Monday, let’s try to interject some market participation that may prove more positive. One of Wall Street’s biggest bulls predicts a sharp Santa Claus rally will revive the stock market. According to Blackstone investment strategist Joe Zidle, a sentiment problem is behind the latest downturn, not warning signals from U.S. businesses or the economy. Here’s what he put forth in an interview with CNBC late last week.

“If this cycle were to end today, it would mean that some really serious fundamental laws of economics and markets have been broken. Underlying fundamentals argue we should see a Santa rally, and we should be bullish.”

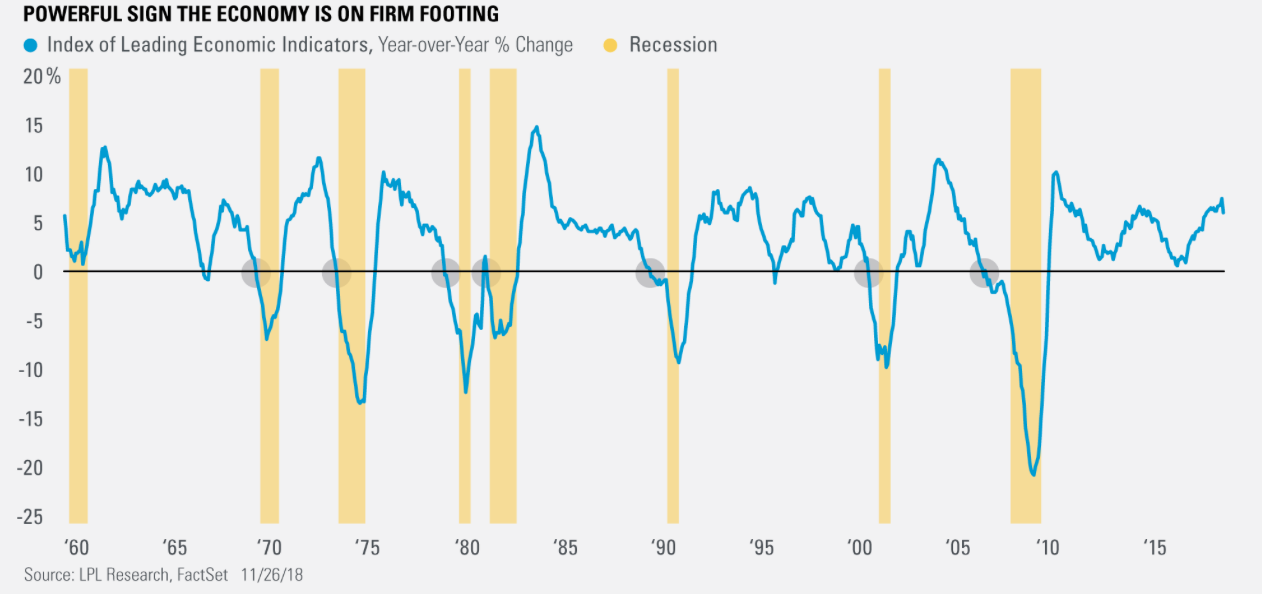

Zidle sees yield curves, leading indicators and average hourly earnings as the three strongest predictors of a bear market. Right now, he said, they’re not suggesting trouble. Speaking of those leading indicators…

Last week, the Leading Economic Indicators (LEI) painted a continued strong backdrop for future economic growth, as it rose slightly above the previous month and 5.9% year over year (YOY). The LEI has risen or been flat for 29 consecutive months, the longest streak in more than 30 years. While the yield curve, peak earnings, Federal Reserve (Fed) worries, and trade issues with China have been getting all the attention recently, all recessions going back to the early 1970s first saw the LEI turn negative YOY.

“The fact that the LEI has been very successful at forecasting recessions, and is one of the few forward-looking economic indicators, make it one of our favorites. The continued strong data suggest a recession is nowhere in sight and signal solid underlying fundamentals in the U.S. economy,” said Ryan Detrick, LPL senior market strategist.

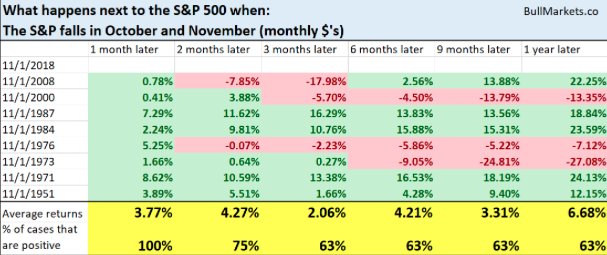

So what’s next? Well, we will have to wait and see, but here’s an interesting study given the state of the market, which may find itself with 2 consecutive monthly declines, occurring in October and November. The study comes from Troy Bombardia. If the market doesn’t climb significantly this week it will find itself in the rare situation where it does indeed have decline in October and November and here is what the statistics show happens next to the market:

The most recent occurrence was in 2008 and proved a notable bounce higher in the following 1-year period. But historically, there is no middle ground. Over the next 1 year, the stock market either declined significantly, or rallied significantly.