Long-term investing is largely about corporate earnings, sales and the ability of a corporation to deliver a reasonable return on invested capital to its respective shareholder base. Sometimes, however, investors do need to calculate other variables as a means of setting investing goals and expectations for invested capital returns. While economic conditions should always be considered as part of the fundamental reasoning behind invested capital, there are times when the political environments are measured as well. Now is that time given the circumstances surrounding the White House.

The top economic advisor to President Trump, Gary Cohn, found his departure met with a sharp, albeit quickly relieved market downturn a couple weeks prior. The latest media speculation indicated that national security adviser H.R. McMaster was on his way out of the President’s administration. Secretary of State Rex Tillerson was replaced with Central Intelligence Agency Director Mike Pompeo last week. Attorney General Jeff Sessions has been speculated to be on the President’s “hit list” for some time, but has managed to stay in position to date. Late in the week, the Attorney General fired FBI Director Andrew McCabe. The biggest political elephant still in the room remains the Mueller investigation. On Thursday, Mueller subpoenaed the Trump Organization to turn over documents, including some related to Russia. In 2018 and as the U.S. Presidential administration seems to be in a state of flux, with various cabinet and official positions being vacated for various reasons, it seems as though the equity markets have taken notice. This is a break from the norm or the decision to favor improving corporate earnings over political strife.

According to Saxo Bank’s head of commodity strategy Ole Hansen, one measure of political risk is at its highest level since 2003, during President George W. Bush’s invasion of Iraq. While the war was initially supported by the American people, the angst around the decision loomed large and found equities in an uncertain environment leading up to the “Shock and Awe” military campaign.

Late in 2017, Hansen’s Geopolitical Risk Index (GRI) was at its peak and during a period of conflict between the North Korean leader and the United States. This after several failed missile tests from the North Korean regime. The chart below indicates Hansen’s GRI that is now above that peak in August of 2017.

While the political environment seems contentious, this coming week, barring any political headlines of course, will be all about the Fed. The 2-day meeting, which concludes Wednesday with the rate hike announcement and press conference, is expected to deliver 2018’s first .25 bps rate hike. This is what the market has largely based into valuations to date. As such, the verbiage Fed Chair Jerome Powell offers in his press conference will be of greater importance than the rate hike itself.

At present, Fed funds futures market expects three rate increases by the end of the year, with a more than a 30% chance of four. Whether the Fed raises 3 or 4 times in 2018 will largely depend on the strength of the economy, the rate of inflation and the Fed’s decisive indicator, Personal Consumption & Expenditures or PCE. In the last projection from December 2017, only four of 16 Fed officials forecast four rate hikes in 2018.

Furthermore, Bank of America Merrill Lynch senior economists offered her thoughts on the Fed and its upcoming rate hike decisions.

“It is not a bold forecast to argue that there will be a hawkish undertone from the meeting…[but] they will be baby steps rather than moving in leaps and bounds,” said Michelle Meyer, senior U.S. economist at Bank of America Merrill Lynch, in a note to clients. Meyers said the Fed is likely to stick to its December forecast of three rate hikes.

Between uncertainty surrounding the White House and the number of times the Fed will hike in 2018, the major averages have failed to recapture all-time highs. The S&P 500 is still up 2.9% in 2018, but remains 4.2% below its all-time closing high set on Jan. 26. Last week the S&P 500 closed with weekly losses on Friday. In speaking to the S&P 500’s attempt to recover from its recent February correction of greater than 10%, Finom Group’s Technical Analyst, Edward Cordoba, offered his following analysis:

“As it stands, we remain in a corrective state until we see a breach of new highs to comfortably say the upward trend continues.

As mentioned previously, markets are experiencing uncertainty and Cordoba’s technical analysis mirrors this sentiment. Russell Investments Senior Portfolio Manager Douglas Gordon believes uncertainty is the biggest headwind affecting investors right now.

Gordon said a trade war is his biggest risk because it could push the world into a recession. But, he believes it has a “relatively low probability.”

Other analysts mirror the sentiment offered by Douglas Gordon such as the quant team at J.P. Morgan. The team, led by Marko Kolanovic, recently released their latest notes on the overall market titled Game theory implies low risk of trade wars; if equities follow 2015 flow patterns, new highs may come soon.

Kolanovic is quite definitive when outlining the quant team’s approach to “looking at the markets”. The reality of the trade war rhetoric fundamentally aligns with the team’s forecast, as there are currently no trade tariffs being implemented, only proclaimed and with favor by the President. Having said that, the rhetoric and proclamation have opened the door for further negotiations on trade between the U.S. and other nations, which may prove favorable to the U.S. in the future. Going forward, we are likely to hear a good deal more about the proposed trade tariffs. U.S. officials have said they will seek to work with “like-minded” countries at the Group of 20 finance leaders meeting next week in Argentina. But investors may soon become numbed to the subject matter the more it proves innocuous and without resolution near term.

While Kolanovic is forecasting the S&P 500 to achieve new, all-time highs near term, Finom Group sees a more gradual recapturing of all-time highs and before new, all-time highs are achieved. The recent firing of FBI Director McCabe has the potential to produce a response that may find equities pressured or within their current range, with volatility following suit. Additionally, Finom Group’s Chief Market and Volatility Strategist, Seth Golden, believes markets will experience heightened levels of volatility in 2018 when compared to 2017. With the VIX at roughly 16 presently and after peaking above 50 already in 2018, the S&P 500 could express 1% moves on a daily basis. This is a clear indication of a lack of stability in the equity markets presently or at least a reversion to a more normalized level of market volatility. Having said that, short-VOL strategies can do very well through all market environments when performed in a risk-controlled manner.

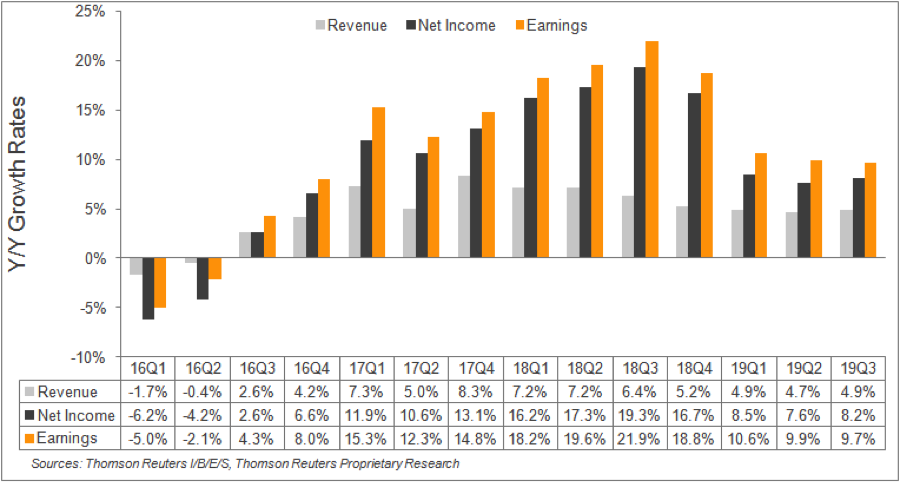

Absent the discussion of the political environment, the earnings picture remains solid and provide for sound market footing over the scope of the full year. Earnings are expected to rise double-digits in 2018 as tracked by Thomson Reuters and depicted in the table below.

First quarter 2018 earnings are expected to increase 18.2% from Q1 2017. Excluding the energy sector, the earnings growth estimate declines to 16.3%. Reuters’ Q1 2018 forecast remains unchanged from the prior week’s forecast. High teens earnings growth is expected to persist through much of 2018 and will likely find a sharp deceleration in 2019 as the “laws of large numbers” present a formidable challenge.

In addition to the corporate earnings outlook for 2018, briefly discuss the economic data to be reported alongside the FOMC 2-day meeting this coming week. The data calendar is quite inconsequential this coming week and when compared to the highly anticipated press conference from the Fed Chair on Wednesday. This coming week may find the benchmark S&P 500 “bar belled” by the Fed and White House rhetoric on trade. The unknown, yet still feared by investors, remains the ongoing Mueller investigation, but many analysts and investors may look beyond this variable in the coming week. The uncertainty… remains apparent!