By Alexander Osipovich March 5, 2020 6:00 am ET

Trading conditions have sharply deteriorated in a popular vehicle for betting on swings in the S&P 500, exacerbating the volatility in the stock market in the past two weeks.

E-mini S&P 500 futures play a huge, if little understood, role in financial markets, with hundreds of billions of dollars of trading activity each day. They track the S&P 500 and typically move in lockstep with the broad-based index.

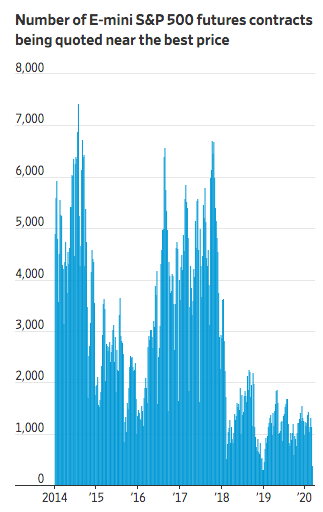

For reasons that aren’t fully clear, liquidity in the E-mini market has been unusually depressed during the past two years. It eroded to near record lows during the coronavirus-fueled selloff of late February, and it is still thin—a sign of potential turbulence going forward.

For most of 2017, the average number of E-mini contracts available to be bought or sold within a tight band around their current price, corresponding to a one-point move in the S&P 500, hovered between 3,000 and 6,000, Deutsche Bank data show.

But over the past two years, that number has rarely climbed above 2,000 contracts. On Friday, it fell to just 163 contracts—down more than 80% from a week earlier—before slipping even further, to 132 contracts, on Tuesday, according to Deutsche Bank.

The term “liquidity” refers to the ability to execute a big trade without affecting the price of an asset. In layman’s terms, lower liquidity means that when a wave of selling hits a particular market, prices drop more sharply than they would have otherwise. In the case of the E-mini, heavy selling has a knock-on effect on the stock market itself—and on investors’ portfolios.

There are various ways to measure liquidity, and it is a matter of debate which is best. A simple approach is to look at the trading volume of a particular market. By that standard, liquidity in E-minis has never been better, hitting a record on Friday with more than $850 billion traded that day.

But the liquidity metric tracked by Deutsche Bank’s analysts—the number of contracts available to be bought or sold—offers a measure of how fragile a market is. When there are lots of traders posting quotes to buy E-mini contracts, they effectively act as a buffer against sellers putting downward pressure on the S&P 500.

And by that standard, the buffer is now very thin.

“Markets have been walking on thin ice, on and off, for more than a year,” said Shankar Narayanan, head of trading research at Quantitative Brokers, a financial-technology company that provides software for executing futures trades to banks and hedge funds.

Futures are contracts that allow traders to bet on future price moves in many markets, including oil, gold and U.S. Treasury notes. Currently, the most active E-mini contract is tied to the value of the S&P 500 on March 20. But in practice, it moves in tandem with the index’s current value.

Unlike stocks or exchange-traded funds, E-mini futures trade nearly around the clock, five days a week. Traders use them for a variety of strategies, including hedges to protect against market declines.

Kevin Davey, an independent futures trader in Cleveland, was among those who retreated from the market last week because of the vanishing liquidity. Mr. Davey runs a number of trading algorithms in E-minis, some of which shut down or dialed back their activity as measures of liquidity or volatility got too extreme.

“The sheer depth and extremity of the move caught me and a lot of people off guard,” he said. “When things get too squirrelly in terms of movement, sometimes it is best to stay on the sidelines.”

Exchange operator CME Group Inc., which runs the market, says $342 billion worth of E-mini S&P 500 futures changed hands on an average day so far this year. By comparison, average daily trading volume of the entire U.S. stock market has been about $433 billion, according to research firm Tabb Group.

A CME spokeswoman pointed to the futures contract’s strong volume figures as evidence of its health. Last week, “a record number of market participants turned to the E-mini futures market to manage their risk,” she said.

It is unclear why E-mini liquidity has been in retreat. It appears to have never recovered from the shock of Feb. 5, 2018, when the Dow Jones Industrial Average slid 4.6% and the Cboe Volatility Index spiked 116%, blowing up a number of popular volatility-linked trades in an event that some dubbed “volmageddon.”

Some market veterans say E-mini liquidity has deteriorated because of fundamental shifts in the futures world. In recent years, traders at banks and hedge funds have become increasingly likely to buy and sell futures using automated algorithms, which tend to chop up large trades into many smaller ones. That has resulted in smaller orders being placed on futures exchanges, for shorter amounts of time, according to a study released last year by the U.S. Commodity Futures Trading Commission.

Meanwhile, the number of market makers active in futures has dwindled as the industry has consolidated, with a few electronic trading giants such as Citadel Securities, DRW Holdings and Jump Trading expanding as smaller rivals have shut down or been acquired.

Precise numbers on futures market-making aren’t publicly available. But Rick Lane, chief executive of financial-software firm Trading Technologies, estimates that about half a dozen market makers now dominate the business. A decade ago, he said, there were at least 10 times as many market makers.

“That concentration likely has an impact on the volatility and likelihood of swings in the market,” Mr. Lane said.