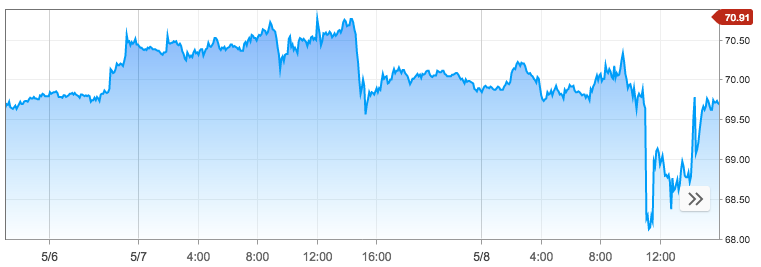

So yesterday was a bit of a nail-biter, right? We had a looming, geo-political announcement that had the potential to rock markets and relationships between the U.S. and its allies… and enemies if we really want to be honest with the situation at-hand. Leading up to the 2:00 hour for which President Trump was to announce the widely expected withdrawal from the 2015, Iran Nuclear Treaty, markets remained rather tame with crude oil prices swinging back and forth leading up to the event. Below is a chart of the last few days of black gold trading.

Oil futures have rebounded early Wednesday, hitting levels near the 3 1/2-year high after bullish data on U.S. oil inventories, and in the wake of the U.S. pulling out of the Iran nuclear deal as of yesterday. Ignoring pleas by allies, President Trump pulled out of an international nuclear deal with Iran that was agreed in late 2015, raising the risk of conflict in the Middle East and casting uncertainty over global oil supplies. I could run through the various scenarios that headline the various news outlets, but the reality is the issues with Iran that forced the President’s hand have always been in place. Iran has always sought after nuclear armament and has always housed and supported terrorists and terrorist acts. Oversight of the regimes compliance with the 2015 treaty was limited and difficult and left largely to the United States. Having said that, the President removing the U.S. from the treaty strains relationships and trade negotiations… but those relationships and trade issues have been strained and for a variety of reasons.

Given the aforementioned issues, it probably should have been no surprise that equity markets finished roughly flat on the day, rising and falling throughout the day. The Dow Jones Industrial Average finished Tuesday’s trade slightly higher, with the average posting its longest streak of gains, at four straight, since mid February. The Dow closed up 2.89 points, or less than 0.1%, at 24,360.21. Meanwhile, the S&P 500 index edged slightly lower, off 0.71 point, or than 0.1%, at 2,671.92, while the Nasdaq Composite Index notched a small gain, up 1.69 point, or less than 0.1%, at 7,266.90.

Historically, while geopolitical issues can move markets here and there, temporarily, earnings and economic strength or weakness move markets long-term. At present, the economy is strong and corporate earnings are growing at their fastest rate in many years. These facts underline why investors might block out much of the noise surrounding foreign policy, especially when they have limited impact on the aforementioned. I attempted to level-set investor/trader expectations in finomgroup.com’s daily market brief yesterday as shown in the text below from the article titled Equities & Crude Oil On 2:00 Trump Decision Watch:

The most fearful element for the U.S. economy regarding the Iran decision is the impact on oil prices, which are widely perceived to move higher should Iranian oil come off the market. Inflating oil prices lead to higher input prices and lower gross margins for corporates. But it is important to put today’s $68 dollar a barrel and $2.85 gasoline at the pump prices into perspective. Prices for both were considerably higher under the Obama Administration and failed to curtail consumer demand, retail sales or corporate profits from rising. In fact, there has never been a time in the modern era whereby higher energy prices impacted the consumer.

My aim was to inform readers of what’s truly important to investors in the market and ultimately what will drive markets longer-term. While leaving the Iran deal, the economic and corporate earnings impact is minimal to non-existent. The issue makes for great headlines and consternation as to what will be and what is possible, but that’s about it. As the world’s largest superpower with one of the strongest economies and financial systems historically, investors focus on what impacts corporate earnings. As such, my former verbiage remains elevated with regards to investor considerations. “What will higher oil prices do to consumer demand and corporate earnings?”

It’s very unlikely that higher energy prices will crimp consumer spending and/or real disposable income. Wages are rising, albeit at a modest pace which aid in consumption by the American consumer. Betting against the American consumer has always proven a bad bet. The majority of consumption comes from retail sales and services and historically goes in one direction: upward long-term, as depicted in the historic retail sales chart below:

Barring recessions and financial collapses resulting from transitory excesses and stress to the economy, retail sales or consumer spending doesn’t falter. When it does, it always rebounds to achieve new high levels. Energy prices have been significantly higher in past years and while the media likes to offer, “Higher gas prices will curtail retail sales”, it simply never does. We heard the same under the Bush and Obama administrations when crude oil was upwards of $110 a barrel and gasoline prices pushed north of $4 a gallon. But retail sales still rose as the chart clearly identifies.

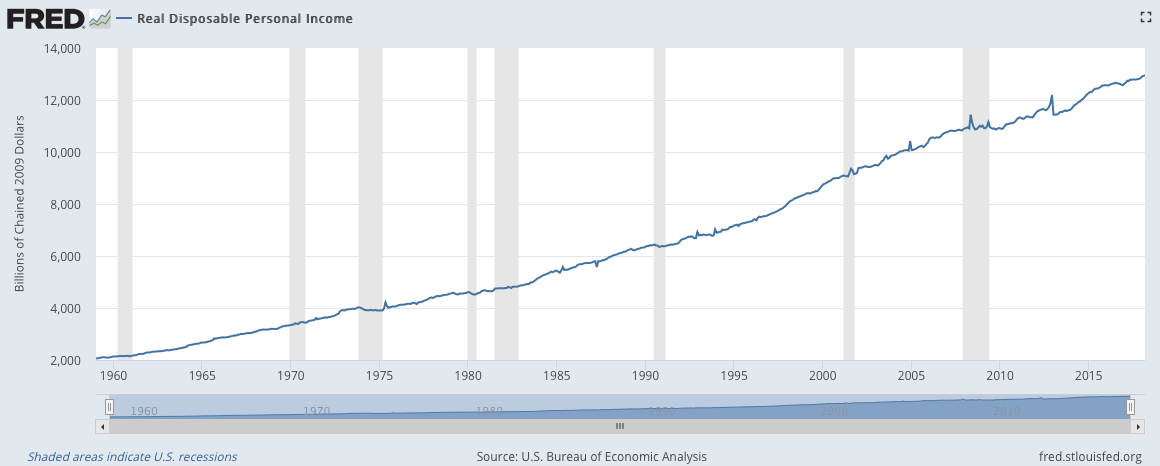

So why do retail sales rise historically? Of course population growth is a factor, “but it’s the economy, stupid”, which James Carville had coined as a campaign strategist of Bill Clinton’s successful 1992 presidential campaign. Jobs grow as the economy expands and wages rise. This gives such rises to disposable household incomes. The chart below shows the historic trend for disposable income, which mirrors that of retail sales. The tail wags the dog; the tail being disposable income and the dog being retail sales.

So when we consider the Iran deal and the angst leading up to the President’s announcement that the U.S. is withdrawing from the treaty, are we really to believe this was a unique geopolitical issue? Of course not! History is littered with such geopolitical issues, turmoil, building of relationships and breaking of such relationships. There will always be geopolitical issues to contend with as an investor/trader, but your job is to know what will or won’t impact the economy and corporate earnings. With that said, while the market didn’t really react to the headline announcement on Iran yesterday, that doesn’t mean it will or wont’ in the coming days. General uncertainty about the next steps for Iran and whether or not the oil market will lose supply that can’t be replaced, in and of itself, may lead to higher crude prices. As such, those inflationary results may hurt investor sentiment and curtail equity markets from appreciating. We won’t know until we know of course. But over time, it’s the economy and corporate earnings that matter most! Long-term investors have little to worry about in this humble economist’s opinion.

We have a lot of issues to contend with, daily, as investors and traders. The fundamental backdrop for investors, however, remains strong and strengthening. The S&P has been consolidating for the last 3 months. The last 3 weeks the S&P has basically gone nowhere. Here are the last 3 weeks’ closing values for the S&P 500:

- 05/4/18: 2,663.42

- 4/27/18: 2,669.91

- 4/20/18: 2,670.14

One of the reasons for the S&P 500’s sideways performance can be correlated to the 10-yr. U.S. treasury yield and fears of inflation. Here are the last 3 weeks’ closing yields on the 10-year Treasury:

- 05/4/18:945%

- 4/27/18:95%

- 4/20/18:95%

Pretty interesting huh? But correlations are made to be… uncorrelated with time. The S&P 500 at some point will either breakout higher or breakdown. One thing is for certain, as earnings come in better/higher than expected, the PE ratio of the S&P 500 has become cheaper. Here is the weekly S&P 500 earnings update from Thomson Reuters:

- Fwd 4-qtr est: $163.10 vs. $162.43

- PE ratio: 16.3x

- PEG ratio: 0.79x

- S&P 500 earnings yield: 6.12% vs. last week’s 6.08%

- Year-over-year growth of fwd est: +20.76% vs. 20.29% last week

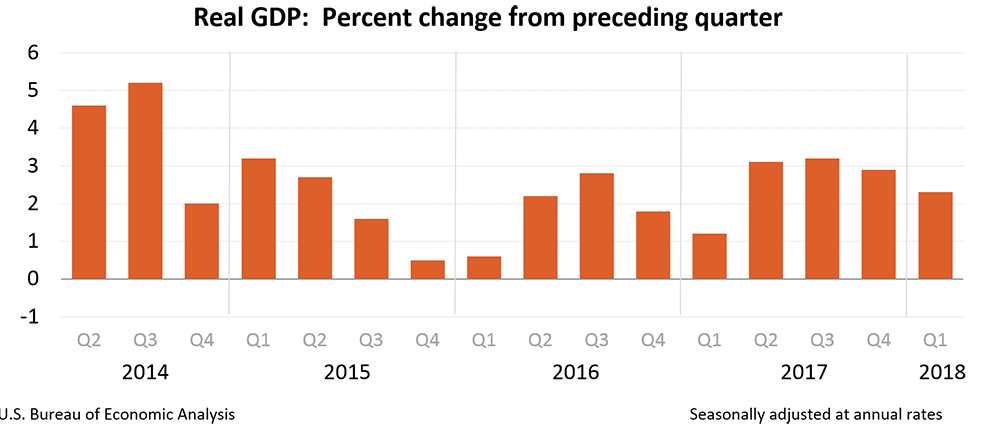

These are pretty strong numbers and while the strength may peak in 2018 as far as earnings growth is concerned, earnings are still expected to grow through 2019. Of course, the growth is supported by a growing economy as identified in the chart of Gross Domestic Product.

For all the cries that the economy is slowing or slowed during the 1st-quarter in 2018, which is true, it’s still the best 1st-quarter performance in 3 years. Moreover, this has proven to be a trend in GDP results, as consumer spending ramps in Q4 and decelerates in Q1, due to seasonality. It’s all about perspective folks and while the geopolitical picture will always be with muddied waters, the economic picture remains the headline of greatest value to investors and investor performance. As such, make wise choices and consider the “long game”!