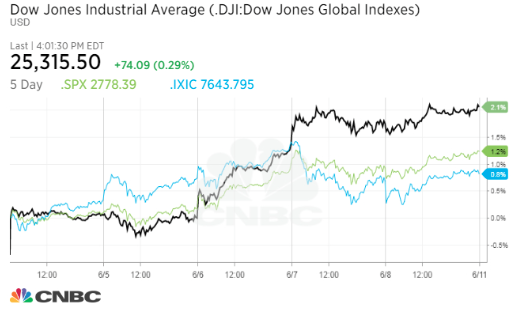

It was a decent start to the month of June for the major averages last week. Equity futures are pointing to a higher open on Wall Street for Monday June 11th and after a tumultuously media headline weekend. We’ll get to some of those headlines in a moment, but firstly, let’s take a brief look back at last week’s market performance. Stocks rose on Friday, adding to solid weekly gains, but their rise was kept in check amid increasing tensions between the U.S. and key trade partners as the G-7 summit kicked off.

The Dow Jones industrial average closed 75.12 points higher at 25,316.53. The S&P 500 gained 0.3% to 2,779.03 as consumer staples rose more than 1 percent. The Nasdaq composite closed 0.1% higher at 7,645.51. For the week, the major averages all rose at least 1.2 percent. That’s a pretty strong start when compared to the 10 previous yearly results for the totality of June trading for the major averages.

This week is a jam-packed week that will be littered with geopolitical and U.S. centric headlines as key events battle for center stage in the minds of investors. After what appeared to be a G-7 Summit that would end on a positive note and all 7 contributing parties signing the Summit’s communiqué, a post Summit Canadian press conference proved damaging to the group of 7 nations. President Trump and his economic advisors took up the reaction to Canada’s Prime Minister’s statements with aggression.

“Trudeau “held a press conference and he said the U.S. is insulting. He said that Canada has to stand up for itself. He says that we are the problem with tariffs. The non-factual part of this is – they have enormous tariffs,” Kudlow said on CNN’s “State of the Union.”

“Here’s the thing,” he added. “He really kind of stabbed us in the back,” Kudlow added.”

The resulting animosity between the U.S. administration and the Canadian Prime Minister led President Trump to back out of supporting the G-7 communiqué. Some trade and economic experts believe the recent ire of the U.S. administration in response to the comments made by the Canadian Prime Minister are simply advanced negotiating tactics of convenience, as the U.S. desires to keep trade pressures on its allies in order to evoke a more conciliatory response on tariffs and trade barriers.

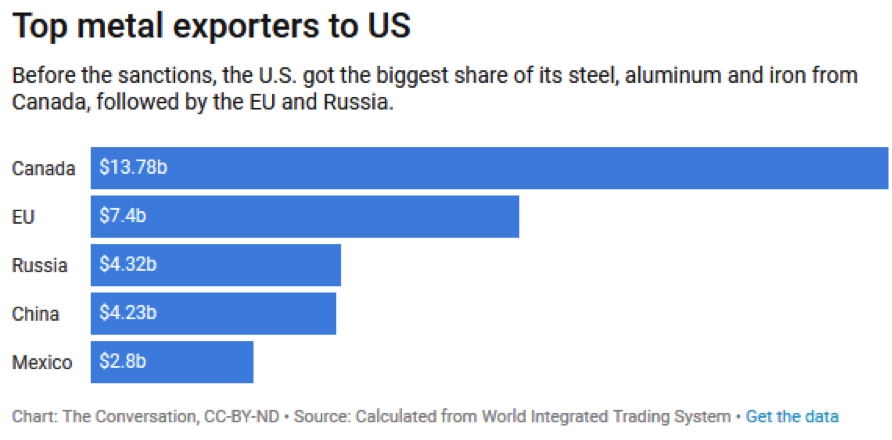

Trade rhetoric between the U.S. and its allies erupted over the last few months with the U.S. imposing tariffs on aluminum and steel exports. Below is a chart that identifies some of the leading trading nations with regards to steel, aluminum and iron:

The EU is the single biggest market for exported U.S. goods, buying US$270 billion of American products in 2016, followed closely by Canada and Mexico. By comparison, China buys just $116 billion.

On the flip side, Americans purchase more from those countries than they sell, creating bilateral trade deficits that the president hates – even as most economists say they don’t matter. The U.S. imports $417 billion in goods from the EU, $294 billion from Mexico and $278 billion from Canada. With that, on to the Fed and with the widely expected .25% rate hike set to be delivered, as trade issues will likely continue to linger for weeks and months ahead.

While a .25% rate hike is a given, the pace of rate hikes and the Fed’s outlook will remain in question prior to the Fed’s press conference. Along with the quarter-point increase in the Fed’s benchmark short-term target, the policymaking Federal Open Market Committee is likely to announce another change that would signal an early exit from its program to reduce the level of bonds being held on its balance sheet. There is a growing suspicion among economists that the Fed will not wind down it’s balance sheet to the degree most assumed. What once appeared to be an operation to shrink the amount of bonds the Fed owns, that would have run well into the next decade, could be wrapped up next year, or early 2020 at the latest.

Instead of reducing the balance sheet from its peak of $4.5 trillion to $2.5 trillion or so as some Fed officials indicated, the impact could be less, to $3.5 trillion or even a little more.

“There is a very active debate, and it’s probably really going to take hold at the August meeting, about how far the balance sheet contraction should really go,” said Fed expert Lou Crandall, chief economist at research service Wrightson ICAP.

According to minutes from the May meeting, FOMC officials are concerned that the funds rate is rising a bit more quickly than anticipated, causing a tightening in money markets that would make a more aggressive unwind of the balance sheet problematic.

Only the Fed knows how long and to what degree it will unwind its balance sheet. But the Fed has the unenviable task of doing so into a tightening money market while the 2-10yr Treasury yields threaten inversion. Moreover, it is increasingly unlikely that as the Fed actively ponders and executes on its tightening policy, a 4th rate hike in 2018 becomes improbable.

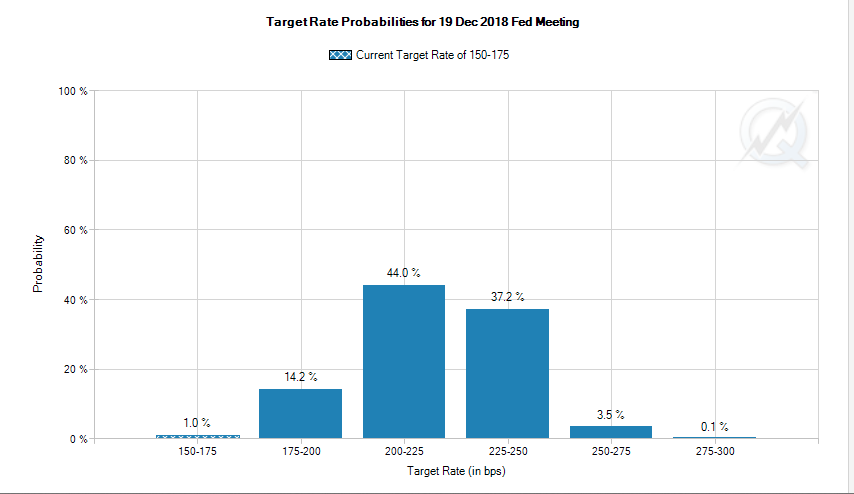

The interest-rate decision will come at 2 p.m. Wednesday after two days of talks. The Fed will also be releasing updated economic forecasts for the economy and interest-rate policy alongside Chairman Jerome Powell’s press conference. Markets will be focusing on the central bankers updated “dot-plot” projections for interest rates. The dot-plot will go a long way to defining the probability of a 4th rate hike in 2018, which currently stands at roughly 37 percent probability. And then there is the European Central Bank…

ECB President Mario Draghi will likely be forced to field questions about both the discussion surrounding the timetable for winding down bond purchases as well as the situation in Italy. The key point for U.S. investors will have to do with the outlook for the eurozone economy, which saw a significant softening of first quarter data after a strong 2018 performance. If the ECB holds off on laying out a timetable for QE exit, it could be taken as a sign of concern by policy makers about the economic outlook, which could be something of a negative for markets. At present, many economists are of the opinion the ECB will end its QE policy in September. The ECB will announce their outlook and rate decision ahead of the market open on Thursday.

Every investor around the globe is likely going to be pinned to their favorite media outlet on Monday and Tuesday as the historical N.Korea/U.S. Summit takes place. As such, the markets are likely to key off of any significant statement coming from the Summit. The U.S. administration has started to play down and lower the expectations from the historic Summit.

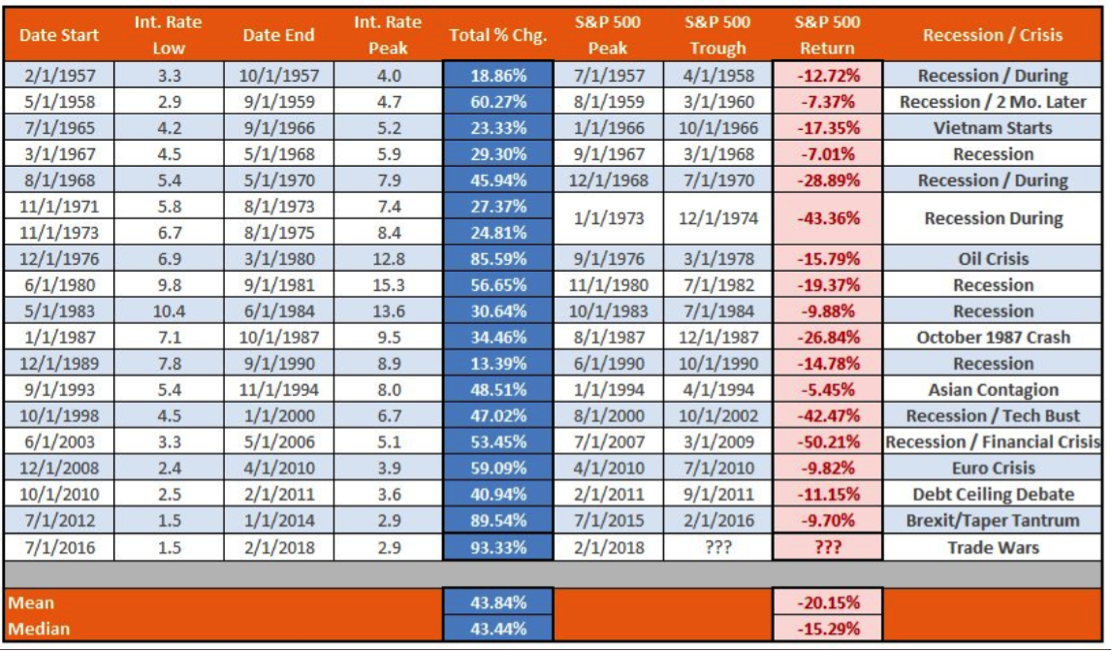

Why is this week so important? Well, the central banks have dominated the equity trade participation since the financial crisis. The major central banks from around the globe are all at a turning point with the FOMC, ECB and Bank of Japan all making policy statements and decisions on tightening this week. Many equity market participants believe that central bank rate hikes lead to market declines. As such, the chart below identifies that while CBs hike rates, the reality is that markets tend to rise in lock step, to a point.

The stock market tends to go up while the Fed is hiking rates, and fall after the Fed stops hikes. As such, avoiding the stock market right now just because “the Fed is hiking rates” is an investment/trading thesis that is found without logic or appropriate analysis. Will the market crash some day? Absolutely! When will that day come, I’m absolutely certain nobody knows with any reliable degree of certainty. As such, following the economic data of the week proves prudent with efforts to ascertain a greater probability of when that crash is, at least, forthcoming.

Given the amount of geopolitical, binary factors that will affect the market this week, the implied move for the S&P 500 has greatly increased with respect to previous weeks. The implied moves in the S&P 500 over the last several weeks have been right around $33.

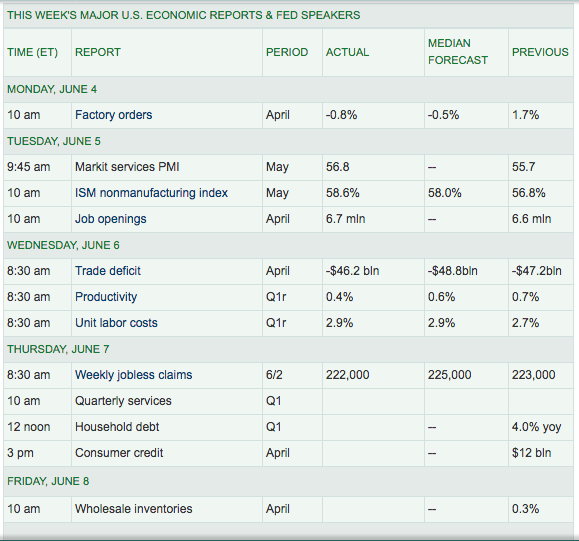

But all of a sudden, for this week the implied move for the S&P 500 is around $36. This is a jam-packed week that is littered with binary events. Fortunately, with all the geopolitical and central bank news set to impact the trading week, for better or for worse, the economic data calendar is rather light and found with little consequential data released this week. Below is a table from MarketWatch, outlining the economic data schedule for the week of June 11th.

Finom Group expects bouts of volatility in the market this week given the aforementioned risk events. It may prove optimal to remain risk neutral and not step in front of such event risks. Having said that, the underpinnings of the economy remain quite strong and suggest a higher yielding equity market by year’s end with the probability of new all-time highs ahead for the major averages. As such, the long game remains the focus for disciplined investors and traders alike.