While “sell in May and go away” didn’t exactly play out for a 6th consecutive year, it didn’t quite feel as though the month finished on strong footing for the major averages. It’s been quite the turbulent week for the major averages and as they finished the month. The Dow Jones Industrial average has had wild swings all week and finished the final trading day of May by closing down 252 points or 1.02 percent. Nonetheless, May was still positive for equities, with the Dow booking a 1.1% monthly rise, the S&P 500 gaining 2.2% and the Nasdaq Composite advancing 5.3 percent.

It was announced yesterday that the U.S. will impose tariffs on steel and aluminum imports from Canada, Mexico and the European Union starting on Friday. Both European and U.S. markets took a hit on the news that broke in the early morning hours. Of course, the U.S. imposed tariffs did not come without hints of retaliatory measures from allies.

“Canadian Prime Minister Justin Trudeau on Thursday said Ottawa will impose billions of dollars of tariffs on steel, aluminum and a wide range of other U.S. goods, including some food and agricultural products. Canada said it would hold consultations for two weeks before imposing the tariffs on July 1, which would remain until the U.S. levies are removed. Trudeau said the fallout from its moves would be “more significant” than it realizes.

The EU said it is also planning to hit back with billions of dollars of levies on U.S. exports which could go into effect staring June 20 and launch a case against American measures at the World Trade Organization on Friday. “This is protectionism, pure and simple,” the EU’s top executive, European Commission President Jean-Claude Juncker, said Thursday. “We will defend the Union’s interests, in full compliance with international trade law.”

Mexico’s Economy Ministry said it would target several U.S. goods in response, including some steel and pipe products, lamps, berries, grapes, apples, cold cuts, pork chops and various cheese products “up to an amount comparable to the level of damage” linked to the U.S. tariffs.”

Much of the concerns surrounding the implementation of tariffs on our ally nations are that not only will it hurt these relationships, but also that it will hurt U.S. consumers. However, this may be sensationalistic fear of tariffs more so than researched, logical impact on consumers and the economy. Here’s what Goldman Sachs had to say about the potential impact from the imposing tariffs.

From Goldman Sachs:

“The incremental inflation effect of these tariffs should be small. We estimate that adding Canada, Mexico, and the EU to the countries facing a tariff of 25% on steel and 10% on aluminum could boost core PCE by roughly 1bp.

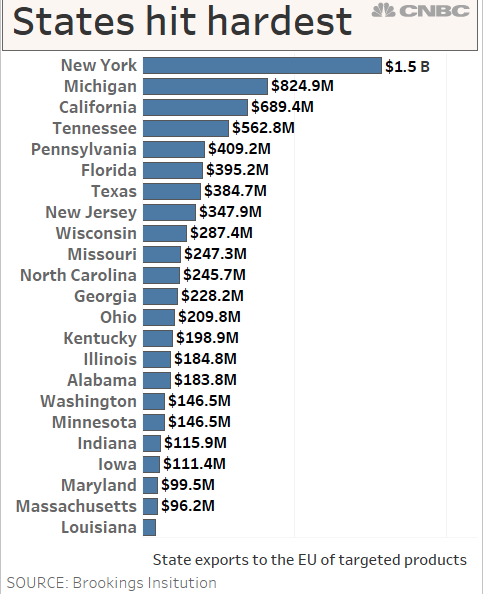

CNBC offered the following with efforts to demonstrate which states will be hit by the EU’s retaliatory targets.

While the numbers look big (absolute #), they are very small as a percent of the U.S. economy. The damage is minuscule because U.S. GDP is almost $19 trillion.

Trade tariff rhetoric and gamesmanship is likely to stick with markets until new headlines are found favorable and as a NAFTA deal hangs in the balance. As investors are now forced to infer the implications of a lingering trade conflict, some good news came out of Italy late yesterday. Recall, the inability of Italy’s political parties to formulate a government found global equity markets spiraling lower on Tuesday. But yesterday afternoon, Italy’s 2 large antiestablishment parties, the League and the 5 Star Movement, struck a deal on reviving a coalition government, according to a 5 Star official, a development that could bring an end to a political crisis. The 5 Star Movement and the nativist agreed to form a government, ending a five-day impasse, said the 5 Star official who declined to be named. The new government will have as its premier Giuseppe Conte. The news out of Italy has the FTSE MIB up nearly 3% on the trading day and the STOXX600 up nearly 1% in early trade.

Despite global trade tensions, which investors should not dismiss out of hand, global equity markets are rebounding thus far on Friday. What will likely be the highlight of the U.S. trading day is the all-important Nonfarm Payroll data set to be released at 8:30 a.m. EST. Economists predict the U.S. likely added 225,000 new jobs in May, according to economists polled by MarketWatch. Thomson Reuters is expecting that 188,000 jobs were created in May. The yearly growth in worker pay is likely to stick near the current pace of 2.6-2.7 percent. So far there’s little evidence of extreme wage increases. Some workers are making out better, but companies continue to keep a lid on labor costs for now. Wages have typically risen between 3.5% to 4.5% in the past when the unemployment rate is as low as it is now.

“That’s the only number that matters really,” said Aaron Kohli, fixed income strategist at BMO. The market continues to consider whether the Fed will raise interest rates three or four times this year, and that wage data could be a factor driving the argument for a fourth if it is higher than expected.”

The Fed’s rate hike path is still hotly contested and carefully scrutinized as to how many times the Fed will hike in 2018. Given the geopolitical instability as of late, investors will key off of the wage inflation data as to signaling the probability of a 4th rate hike in 2018. Having said that, the recent beige book commentary from the Fed may have offered some clues in the forthcoming data, due out this Friday morning. In the beige book, the Fed said that companies are responding to the talent shortage by raising wages as well as in compensation packages. However, “wage increases remained modest in most Districts,” the Fed said, adding that it does expect to see more wage gains showing up in coming months.

There is a great deal of geopolitical and economic information to digest this morning, keeping investors on their game. What may be tipping the scale in favor of the bulls, despite the whipsawing markets, is that volatility has been somewhat subdued in spite of the many daily, concerning headlines. With U.S. equities lower across the board yesterday, the VIX was only modestly higher as an offshoot. And for all the VIX had advanced in yesterday’s trading session, it has taken that back and then some prior to the market’s open. The VIX is down .72 to 14.71 as investors await the Nonfarm Payroll data. With regards to the VIX-Exchange Traded Products, Credit Suisse announced reverse splits yesterday for 2 of these products. Credit Suisse AG will implement a 1-for-10 reverse split of its VelocityShares™ VIX Medium Term ETNs (“VIIZ”) and a 1-for-10 reverse split of its VelocityShares™ Daily 2x VIX Short Term ETNs (“TVIX”), each expected to be effective as of June 8, 2018.

The reverse splits will be effective at the open of trading on June 8, 2018. VIIZ and TVIX will each begin trading on the Nasdaq Stock Market on a reverse split-adjusted basis on June 8, 2018. Holders of VIIZ and TVIX who purchased such ETNs prior to June 8, 2018 will receive one reverse split-adjusted ETN for every ten pre-reverse split ETNs, respectively. In addition, such purchasers that hold a number of ETNs not evenly divisible by ten will receive a cash payment for any fractional ETNs remaining (the “partials”). The cash amount due on any partials will be determined on June 14, 2018 based on the respective closing indicative values of VIIZ and TVIX on such date and will be paid by Credit Suisse AG on or about June 19, 2018.

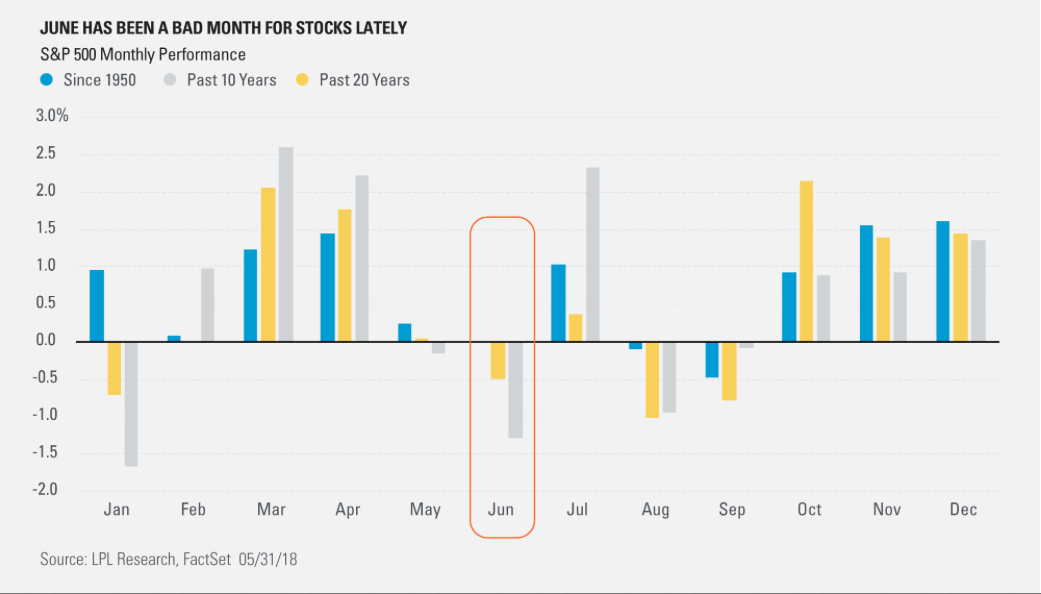

Out with May and in with June investors and traders! May proved, once again, to buck the colloquialism of sell in May and go away for a 6th straight year. However, June has had a trend of several poor performing years.

As shown in the chart above, over the last 10 years the month of June has produced a negative return of greater than 1 percent. Let’s see if June 2018 can buck this unfavorable trend. Any favorable news on global trade might go a long way to facilitating a positive performance for markets in June 2018.

{kind=link}