Italy has caused a good deal of market gyrations over the last 2-trading sessions. On Tuesday, the Dow fell as much as 500+ points before finishing the day lower by 391 points. Global equity markets and investors were troubled over Italy’s inability to form a government as well as soaring debt levels. But in the Wednesday trading session, investors were able to rationalize the weight of Italy’s political strife against the nations ability to cause contagion in the United States. Thus, U.S. equities were able to bounce back hard on Wednesday. The Dow was up just over 300 points yesterday. But now investors are confronted with another geopolitical issue, trade tariffs.

“President Donald Trump announced in March global tariffs of 25% on imported steel, and 10% on aluminum, based on national security concerns. The White House delayed implementation for some countries, giving those trading partners a chance to offer concessions to avoid the tariffs. The U.S. is now planning to let the EU’s exemption lapse. One person familiar with the matter said the administration’s plans could still change, particularly if the two sides are able to cobble together a last-minute deal, though both sides suggest such a deal is unlikely.”

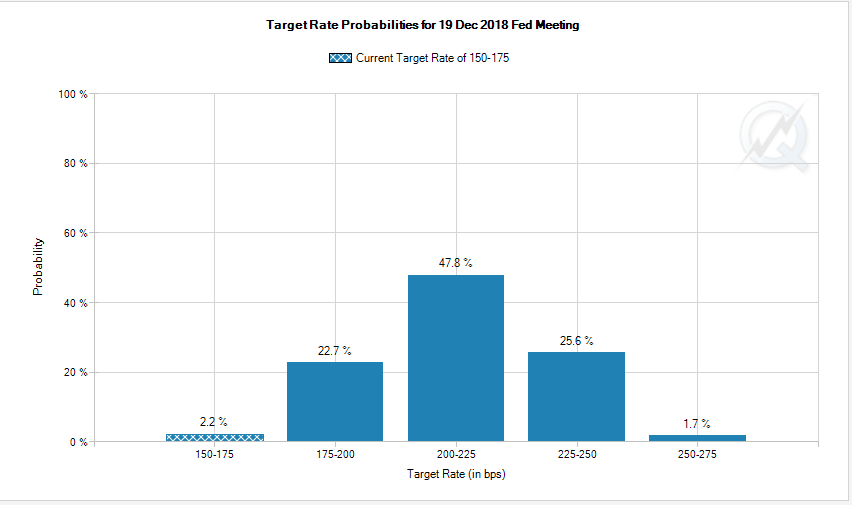

The only benefit from the ongoing trade negotiations and consternations and Italy concerns is that U.S. bond yields have fallen. The 10-yr. Treasury note fell below 2.8% on Tuesday before rebounding somewhat. Moreover, the probability that a 4th Fed rate hike in 2018 has diminished greatly in recent weeks and since the Fed minutes were released last week.

Equities are likely to confront the headwinds over the trade tariff news today, but an all-out trade war is still very unlikely. Even so, the headwind will serve to limit the potential for equities to advance much on the day. Having said that, investors may do themselves the favor of considering the “long game”. Credit Suisse argues the backdrop for equities is such that the S&P 500 Index deserves to trade up 10% by year-end to 3000.

Here are the four components to their call

- Rising profit estimates by Wall Street banks are often a tailwind to stocks.

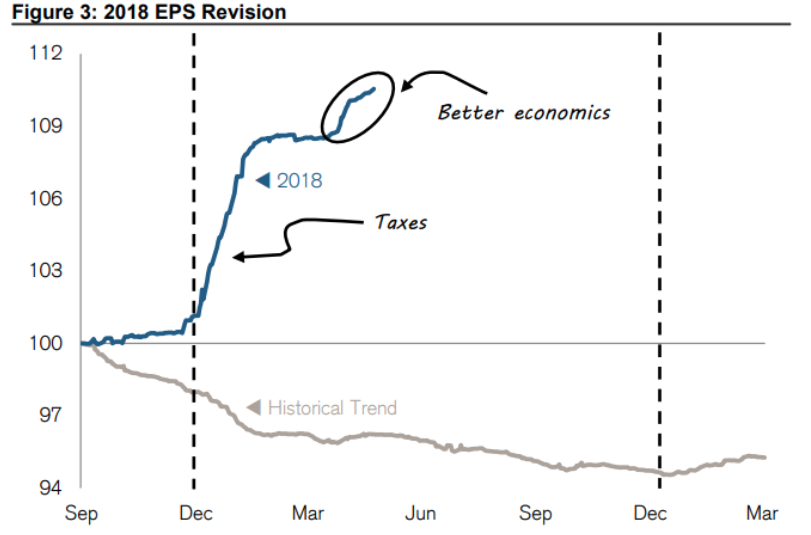

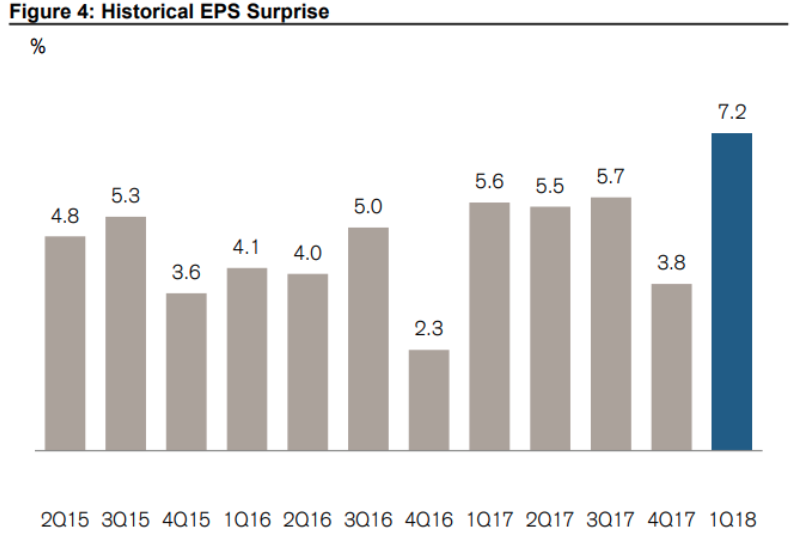

- Despite jacked up Wall Street profit forecasts, Corporate America managed to beat estimates nicely in the first quarter. Credit Suisse thinks that could continue into the second half of the year.

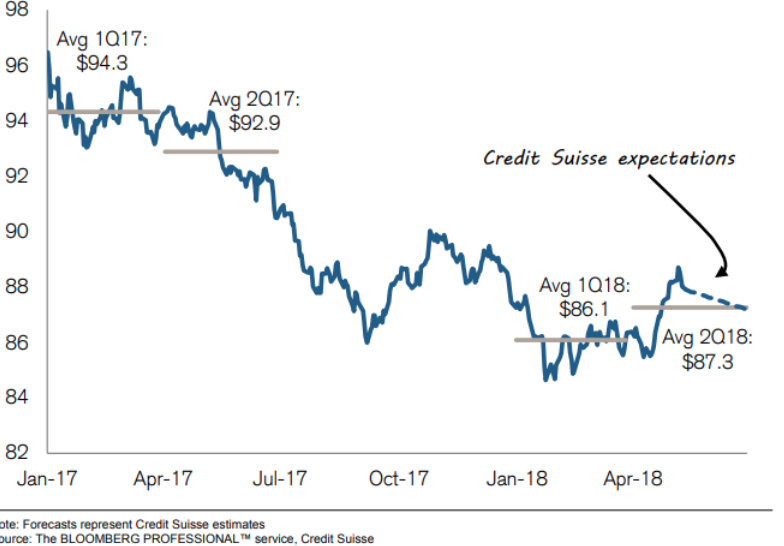

- Credit Suisse believes commodities prices are tame enough to support further gains in operating profit margins.

- While the dollar has rallied about 5% since early May, Credit Suisse anticipates dollar weakness resuming soon.

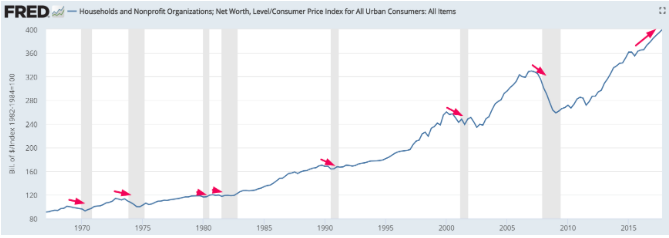

Getting to SPX 3,000 is going to be a rough road in 2018, especially if trade tariffs are actually implemented. Investors will likely not appreciate the measured risk by the U.S. administration that aims to bolster U.S. manufacturing. Nonetheless, the U.S. economy is found with a strong foundation and expected to grow through 2018. Nearly 2/3 of the U.S. economy is driven by the consumer. The consumer is strong as shown in the latest consumer sentiment readings, which are trending higher as well. Moreover, Households’ net worth continues to make new highs in 2018, which is a bullish sign for the stock market and economy. The Federal Reserve releases quarterly data on Households and Nonprofit Organizations’ Networth. Dividing by CPI gives us real (inflation-adjusted) net worth.

As one can see, inflation-adjusted Households Networth has been trending higher, which is a medium-long term bullish sign for the stock market.

More insights concerning the U.S. economy will be forthcoming from Personal Income and Consumer Spending data due out today. On Friday, investors will see just how many jobs were created during the month of May via the Nonfarm Payroll report. Expectations are for the economy to have created another 200,000 jobs during the month of May with a modest uptick in hourly wages.

Undoubtedly, 2018 is proving to be a difficult road to navigate for investors. The heightened levels of volatility have weighed heavily on investor sentiment. The bad days for the market are significantly worse than the good days. A recent article by Bloomberg demonstrated that the “bad days” in 2018 have been really bad. The average down day this year has been 21% bigger than the average up day.

“Only one thinghas been constant in 2018, that every few weeks equities get hammered. U.S. companies are in the midst of one of the biggest earnings expansions ever, everything from buybacks to capital spending is surging and forward valuations are cheap. But it’s proving little barrier to intermittent wipe-outs.”

Don’t take our eyes off the ball investors! Despite the consistent week-to-week market volatility and intermittent very bad market days, corporate earnings are growing significantly. Historically, earnings’ growth drives equity markets higher, just not in a straight line.