At its worst levels of the day on Wednesday, the Dow (DJIA) was down some 550+ points, the Nasdaq (NDX) was down some 120+ points and the S&P 500 (SPX) had fallen back to 2,886 or 1.5 percent. By the end of another wild trading day on Wall Street, however, the Nasdaq finished higher by nearly 30 points and the S&P 500 gained 2.2 points on the day. The last time the S&P 500 erased an intraday decline of 1.5% or more and finished positive was on May 10th.

What sent the markets on this roller coaster ride on Wednesday? Investors rushed for the safety of government bonds and dumped stocks on Wednesday, as traders around the world settled in for a U.S.-China trade war without an end in sight.

Some of the fear that forced investors to seek the safety of government bonds came on the heels of seemingly dire German industrial production data that was delivered before the opening of trade. German industrial production has suffered its biggest annual decline in nine years after the escalating trade war between the US and China took its toll on exports.

Europe’s economic engine, which has increasingly relied on exports to Asia to bolster factory output, was left teetering on the edge of recession in the second quarter after a 1.5% fall in industrial production in June, which is expected to be repeated in July.

Output fell across the three months to June by 1.8% compared with the first quarter of the year, driven by steep drops in metal production, machinery and automobile manufacturing, the economy ministry said.

“Industry remains in an economic downturn,” the ministry said. Production in construction fell 1.1% in the second quarter while energy output dropped 5.9% in the same period.

The yield on the German 10-year bund hit a new all-time low of -0.6% while the 30-year bund also hit a record at -0.137%. The 2-year German yield touched -0.849%.

In addition to the German economic data, 3 central banks had cut rates overnight, India, New Zealand and Thailand. The flight to safety sent the yield on the 10-year Treasury note, used as a benchmark for mortgage rates and auto loans, falling to a low of 1.595%, the lowest since autumn 2016. The yield on the 30-year Treasury bond bottomed around 2.12%, near its all-time low reached in 2016.

The U.S. Treasury yield curve also further flattened and inverted, with the spread between the yield on the 3-month Treasury bill and that of the 10-year Treasury note close to -40 basis points. The 10yr/3m yield curve inverted by an additional 8 bps earlier in the day, but only finished with 1 bps steeper. The spread between the 2-year Treasury yield and the 10-year yield, a longtime recession gauge, hit a low of 7.4 basis points, its lowest level since June 6, 2007. By the end of the day the 10-yr. yield finished flat on the day.

“The flattening in 2s/10s should be expected in a world of rising global macro risk, coupled with falling forward inflation expectations,” Jon Hill, rates strategist at BMO Capital Markets, said in an email to CNBC. “There is an element of fear here that the Fed won’t cut as much as necessary to keep the cycle going and maintain inflation near 2%. This keeps front-end rates elevated while long-tenor yields fall.”

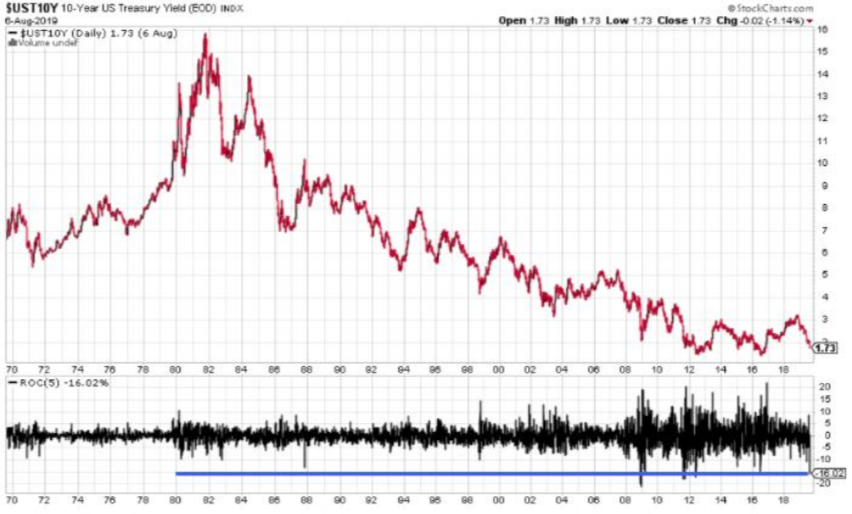

The moves in the bond market have been nothing short of staggering of late. The 10 year Treasury yield’s 5 day rate-of-change fell below -16 percent.

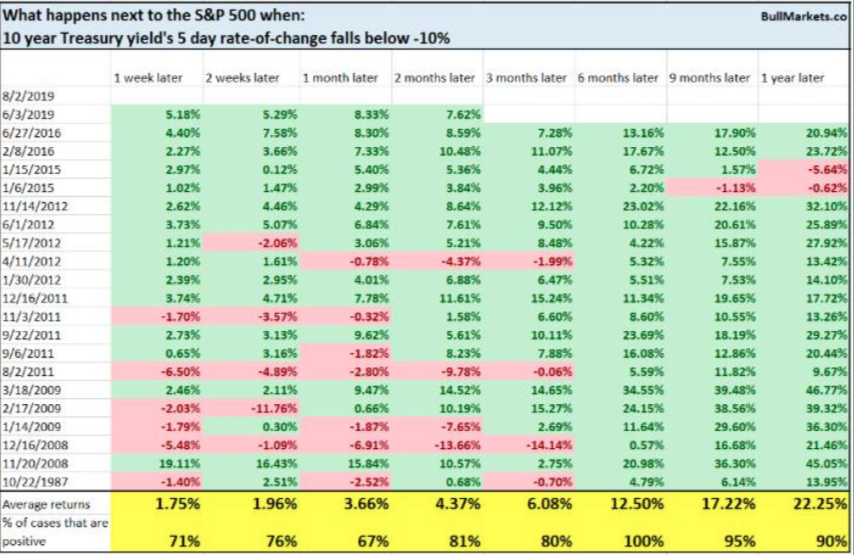

The day with the biggest negative reading for this spread indicator is not necessarily the final bottom day for stock prices. The prior extreme low reading came on Dec. 18, 2018, which was 4 trading days ahead of the lowest closing low for the S&P 500 on Dec. 24, 2018. So while we are getting a message that an important price low is forming now, it does not have to be here yet. Having said that, we aim to understand how the S&P 500 might perform given the rate of change in the 10-year Treasury yield.

As shown in the table above from Bullmarkets.co, S&P 500 returns are positive across all-time frames. In reviewing the ROC, it’s relevant to note that the bond ETF (TLT) rate of change over the trailing 4 weeks has only twice exceeded the current period: 2008-09 Great Financial Crisis and 2011-12 European debt (PIIGS) and during the U.S. fiscal cliff debacle.

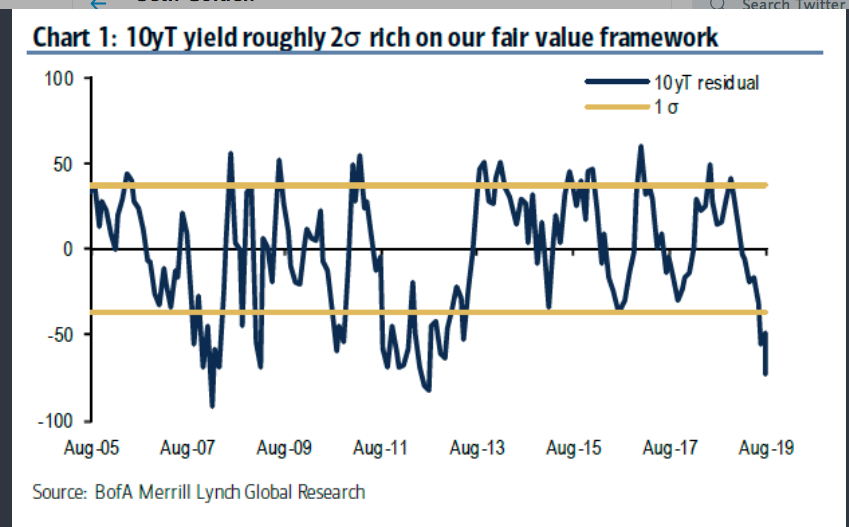

BAML’s fair value model of U.S. Treasuries pegs the 10-year at 2.5% based on current economic fundamentals. The yield is actually at 1.71%, implying the market sees a big deterioration ahead, similar situation the 2011 panic.

The stock market’s recent sell-off has been fairly brisk. Just 10 days ago on July 26, the S&P 500 reached a new all-time high, supported by Federal Reserve (Fed) rate cut hopes, improving economic data, and cooling trade tensions. Since then, the Fed’s rate cut and messaging wasn’t met with investor enthusiasm, the United States threatened tariffs on $300 billion in Chinese goods, and China pulled prior commitments to purchase U.S. agriculture goods. In addition, China’s central bank let its currency (the yuan) fall below the key 7 per dollar level that some view as a line in the sand and the U.S. Treasury Dept. subsequently labeled China as a currency manipulator.

The fundamental picture for stocks hasn’t really changed all that much and in the face of the issues noted. Economic growth has exceeded expectations, inflation and interest rates are low, and second quarter earnings have been better than expected. Trade uncertainty continues to weigh on global markets, but tariffs haven’t significantly affected the domestic economy and the Fed has indicated willingness to loosen policy as needed. While there are still geopolitical risks, including trade, a review of all of the above fundamentals suggests to us that the odds of an imminent recession are significantly low. With the treasury market possibly signaling a recession in 2020, however, recession risks and an actual recession can take hold rather quickly and if sentiment were to worsen in the face of imposed tariffs.

At this stage in the year-long trade feud, the U.S. economy has remained rather ebullient. Even so, damage is and will likely take a further toll on the economy should an escalation of tariffs take place. A staggering 74% increase in tariffs since last year added $6 billion in extra costs for U.S. consumers and businesses, a pro-trade group said on Wednesday as it warned additional tariffs threatened by President Donald Trump would further hit demand and hurt jobs.

The trade group, called Tariffs Hurt the Heartland, which includes the Americans for Free Trade coalition and Farmers for Free Trade, disagreed with Trump’s position. It said the 74% rise from the same period a year ago was one of the highest monthly jumps on record.

“We are at a very dangerous pivot point with the tariff strategy,” David French, senior vice president of government relations at the National Retail Federation, a coalition member, said in a conference call with business leaders on Wednesday.

The trade coalition said American taxpayers have paid over $27 billion in extra import tariffs from the beginning of the trade war in 2018 through June of this year based on data collated from the U.S. Census Bureau and the U.S. Department of Agriculture.

Jo-Ann Stores, an Ohio-based arts and craft retailer, hit by tariffs introduced in September 2018, said it has already been forced to raise prices, and has seen that decrease demand.

“It’s an enormous financial burden,” said Jo-Ann Chief Executive Officer Wade Miquelon, who previously served as chief financial officer of Walgreens. “These tariffs will cut into our profit margins and force us to take very tough decisions including job eliminations and further store closings.”

Some analysts and economists are of the opinion that absent the tariffs that had been imposed since July 2018, the economy would be growing about .2% higher and the stock market might also be 10% higher than where it was at its peak this year.

President Donald Trump may “tariff” the U.S. into a recession that could have been avoided, says economist Ryan Sweet of Moody’s Analytics, who won the Forecaster of the Month contest for July with his accurate predictions on monthly and quarterly economic data.

Sweet remains optimistic that Trump will veer away at the last minute, and that the expansion could continue through the end of 2020, at least.

“If Trump backs off, the economy will take off again,” he says. The Federal Reserve will likely cut interest rates a couple more times, but rate cuts won’t save the economy if Trump escalates further.There’s only so much the Fed can do to cushion the economy.”

At this point in the trade feud between China and the U.S., the question on many investor, economist and strategist minds is whether or not a deal can be done before matters become worse. Forget restraining ourselves to the calculous of “before”. Finom Group wouldn’t suggest a deal is able to become manifested at this stage, regardless of the political implications. While many have suggested, even Finom Group’s Seth Golden, that an escalation of the trade feud would hurt President Donald Trump’s chances of reelection, his actions seem to discard the circumstances in favor of taking a hardline on trade with China.

The U.S./China trade standoff has escalated to a point where restriction on Huawei and China’s support for its currency are being monitored outside of the tariff impositions. These are tentacles not initially on the radar with regards to the trade feud that have since impacted the global economy. On the same subject matter of “will a deal be found”, here is what LPL Financial had to offer in its latest notes to clients:

“If this trade war escalates further and drags on into the 2020 campaign season, President Trump could hurt his re-election chances,” said LPL Chief Investment Strategist John Lynch. “The pressure on the president could intensify if the global economy slows further, consumers are forced to pay higher prices, and corporate profits get hit by tariffs and disruptions to supply chains.” Some of that pressure may come from the farm belt where the President generally enjoys good support. Consumer incomes have historically been the best predictors of presidential election outcomes but presidential approval ratings also matter.

While the impetus to avoid further an escalating trade feud are abound, the situation hasn’t deterred the President from raising the level of tariffs on China in May of this year, nor altered his rhetoric since the first imposition of tariffs in 2019. Reelection doesn’t seem to be the determining factor behind the President’s actions on trade, regardless of the logic indicated by LPL Financial, which otherwise might prove prescient with other Presidents from the past.

Again, at this stage of the trade feud, many simply can’t figure out and don’t desire to forecast the endgame of this trade feud. The chronology of events that have unfolded since July 2018, haven’t followed a path that would logically produce a deal of sorts. Trade truces that are reneged with the threatening of further tariffs don’t exactly bring about fruitful negotiations. It’s hard to imagine anything productive from talks between the feuding parties near-term, but anything is possible. At best, investors might consider that the U.S. simply repeals the threatened 10% tariff on the remaining $300bn in goods from China. This would not likely improve conditional talks, as the damage of the threats are likely already embedded in psyche of both parties.

On Thursday, however, equity futures are continuing their roller coaster ride with futures pointing to a higher open on Wall Street while yield move slightly higher. Cornerstone Macro’s Carter Worth thinks it’s time to harvest gains from the outsized bond moves in response to the surge in 10-year Treasury and play for a tactical bounce in yields.

As bond yields rebound, European markets climbed on Thursday after a surprise boost in Chinese exports lifted global sentiment. This rebound in exports was largely unexpected. Exports rose 3.3%, beating expectations of a 1% decline, but shipments to the U.S. fell 6.5% from the previous year.

Shipments to Europe and Southeast Asia, China’s top two trading partners, also bounced back, while the decline in exports to the U.S. eased after President Trump and Chinese President Xi Jinping struck a conciliatory tone on trade at the Group of 20 summit in Japan in June.

China’s exports to the U.S. fell 6.5% in July from a year earlier, compared with a 7.8% decline in June, customs data show. Imports from the U.S. fell 19.1% from a year earlier, compared with a 31% drop the previous month. China’s trade surplus with the U.S. also narrowed, totaling $US27.97 billion in July compared with $US29.92bn in June.

“While July’s trade headlines showed improvement, China’s foreign trade remains on the downward trend in coming months. Weakening exports will still be the biggest headwinds for Chinese economy,” said Larry Hu, an economist with Macquarie Capital.

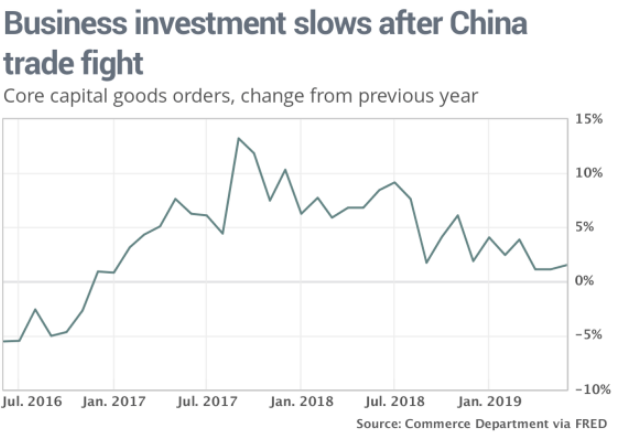

We’ve seen blips in various economic data points throughout the trade feud and from both countries, China and the United States. Make no mistake about it, however, both countries will express weakening economic growth as the trade spat moves forward. Business sentiment has taken the biggest and most notable hit thus far, with manufacturing PMIs in contraction globally. Capital goods orders have fallen since the first imposition and subsequent retaliatory tariffs were levied in July 2018.

So more tariffs must improve economic activity? NO, sorry that’s not how it works. At some point, business investment curtailment will result in businesses slowing wage increases and job growth before job cuts become relevant in order to sustain profit levels.

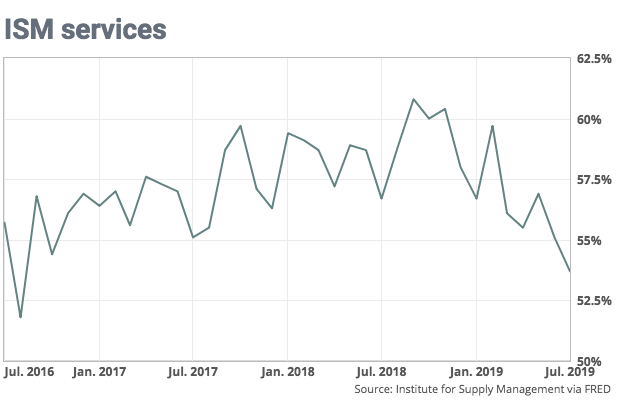

Some of the bright spots in the U.S. economy, like services and domestic transportation have recently shown signs of fading under the pressure produced from a deteriorating business community. The Institute for Supply Management’s nonmanufacturing, or services, index slowed to a reading of 53.7% in July from 55.1% in June, the slowest reading since August 2016. The index stood at 59.7% in February. The reading came in below consensus estimates of 55.5%, according to a poll from MarketWatch.

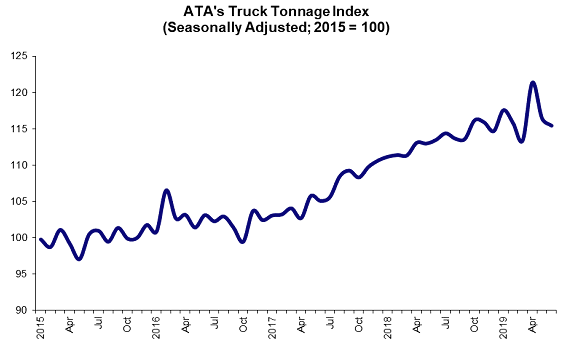

In addition to the service sector rolling over recently, trucking tonage has suffered consecutive monthly declines. American Trucking Associations’ advanced seasonally adjusted (SA) For-Hire Truck Tonnage Index decreased 1.1% in June after falling 4% in May. In June, the index equaled 115.2 (2015=100) compared with 116.5 in May.

“Tonnage continues to show resilience as it posted the twenty-sixth year-over-year increase despite falling for the second straight month sequentially,” said ATA Chief Economist Bob Costello. “The year-over-year gain was the smallest over the past two years, but the level of freight remains quite high. Tonnage is outperforming other trucking metrics as heavy freight sectors, like tank truck, are witnessing better freight levels than sectors like dry van, which has a lower average weight per load.”

May’s reading was revised up compared with our June press release. Compared with June 2018, the SA index increased 1.5%, the smallest year-over-year gain since April 2017.

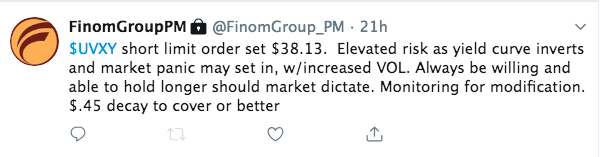

Regardless of what happens going forward, Finom Group anticipates a bit more market volatility over the next few weeks, given the likelihood of trade headlines. Even with the VIX rising 100% from its lows over the last 8 trading days, before falling back below 20 on Wednesday, Finom Group anticipates trading the volatility complex and trading it short. Seems counterintuitive, but trying to time a long-VOL spike is a dangerous and foolish game that often is found with capital loss.

As the market seemingly was on its way to retracing its Tuesday recover yesterday, and with volatility spiking once again, Finom Group issued a short trade alert on shares of UVXY.

In fact, this was Finom Group’s 5th such short on UVXY this week that proved profitable. Subscribe to Finom Group today and trade with us in our Live Trading Room.

To round out today’s daily market dispatch, analysts are scurrying to calculate the possible fallout from the potential raised tariffs on September 1st. The impetus for the FOMC to further cut rates is part of the calculous in determining the economic and earnings impact for investors. But at the end of the analysis and modeling are few simple facts that Tony Dwyer of Canaccord Genuity outlined on Wednesday in the following TDNetwork Live interview.

Tony Dwyer outlines that his long-term outlook on the market remains bullish as part of the impact from the trade war, which is lower rates and refinancing of debt that serves to put more cash in the pockets of businesses and consumers. Dwyer has an S&P 500 price target of 3,300 over the next 12 months and given the easing cycle that should produce more economic stimulus despite the trade feud escalations.