While equity markets around the globe hit the pause button ahead of an onslaught of central bank announcements and press conferences, the beat must go on. In yesterday’s trading action, the Dow finished basically flat with the S&P 500 up .17% to 2,786. The tech-heavy Nasdaq was the outperformer once again, finishing higher by .57 percent to 7,703. The small cap Russell 2000 Index was only slightly behind the Nasdaq, finishing higher by .46% on the day. Ahead of the Federal Open Market Committee (FOMC) rate hike decision today, we did get some insight into the consumer inflation picture with the release of the Consumer Price Index (CPI) ahead of the opening bell on Wall Street yesterday.

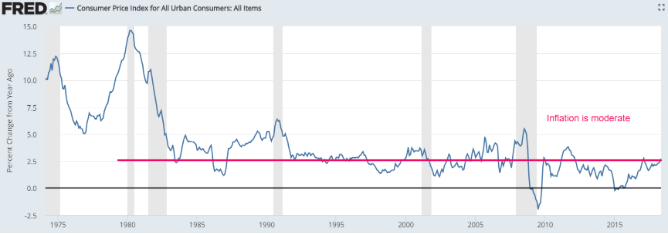

The consumer price index increased 0.2% in May, the government said Tuesday, in line with Wall Street’s forecast. The consumer price index has risen 2.8% in the past 12 months, up from 2.5% in April. That’s the fastest rate since early 2012. While this is the fastest rise since 2012, it is not breakaway inflation and nothing investors should be fearful of as we look at the broader chart below of CPI over the decades.

There is no “surging inflation”. Putting things into perspective demonstrates that inflation is, at best, moderate.

The yearly increase in the core rate edged up to 2.2 percent. The rise in consumer prices largely came from those components surrounding the cost of living, gasoline, medical care, rent and home prices. Consumers are paying less for new and used cars, airline fares and communications services such as wireless and cable. The fears surrounding rising wages earlier in 2018 have been alleviated in recent months, but may mount a comeback, as wages are now seemingly not rising quickly enough to offset rising prices. Real or inflation-adjusted hourly wages rose a scant 0.1% in May, and they are unchanged over the past year.

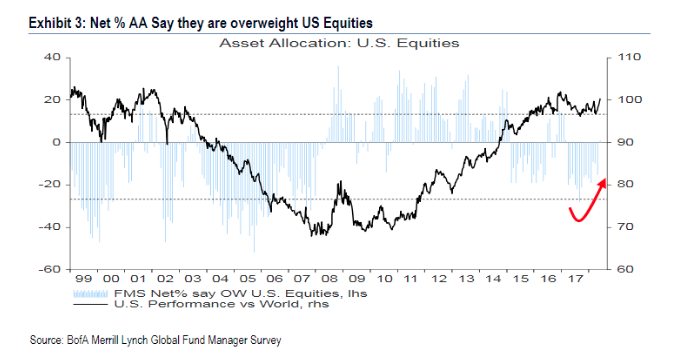

As the S&P 500 has broken out of consolidation zone that has muddied its performance in 2018, equity investors are feeling more confident. Bank of America Merrill Lynch said Tuesday that its June survey of global fund managers found equity investors are overweight U.S. stocks for the first time in 15 months, with two out of three respondents saying the U.S. has the best outlook for corporate profits.

Investors identified “trade war” as the biggest “tail risk” for markets, the survey found, with BAML noting that “trade tensions” have been the dominant macroeconomic worry for investors in 2018. Some of the finer points from the BAML survey are bulleted below:

- The survey found that cash levels dipped by 0.1 percentage point to 4.8%, which remains above the 10-year average of 4.5%. That is a positive for stocks, according to the survey’s “cash rule,” which holds that an average cash balance above 4.5% constitutes a contrarian buy signal. A cash level below 3.5% is viewed as a contrarian sell signal.

- Investors expect the S&P 500 to peak at 3,040, according to a weighted average of survey responses, upside of around 9% from Monday’s close near 2,780.

- Investors don’t expect a recession until the first half of 2020.

Low volatility and low correlation have given a boost to investor confidence, with stock prices gaining ground so far in the second quarter. The S&P 500 is up more than 5% quarter-to-date, largely driven by a rally in technology stocks that make up more than a quarter of the entire index. Keeping the Fed in focus, we’ll have to wait and see if this quarterly surge in the S&P 500 can remain on course after the Fed’s press conference today.

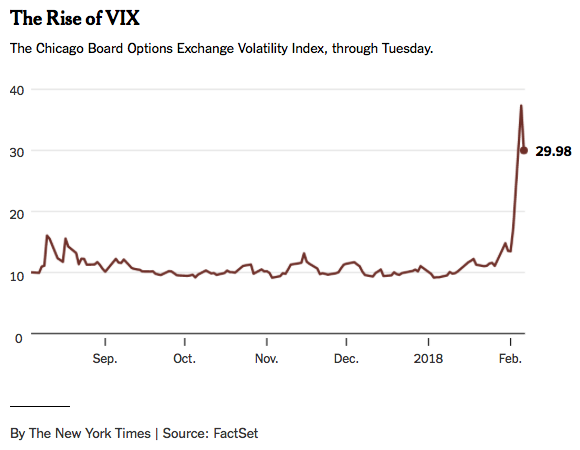

The Cboe Volatility Index or VIX has fallen 40% since early April, settling at 12.34 on Tuesday, near its 2018 lows. The mean correlation for U.S. sectors to the index in 2017 was 0.55, about a third lower than the 2010-2016 average of 0.83. A perfect correlation reading of 1.0 would mean that sectors were moving in lockstep; a reading of 0 would reflect zero correlation, with sectors moving completely independently of one another.

“U.S. equity volatility is seasonal — we could see some churn (and therefore higher correlations) in August or October, the two typical high water marks for volatility,” Colas said.

Finom Group represents one of the more focused volatility trading sources and social platforms. Chief market strategist Seth Golden was highlighted in the New York Times last year for his prowess in the infamously named “short-VOL trade”. As volatility surged in February this year, the New York Times caught up with Golden to get his take on the February volatility event now known as the “volpocalypse”. The VIX spiked above 50 in February, rising more than 100% in a single day and causing the accelerated termination event of Velocity Shares Daily Inverse VIX Short Term ETN. (XIV).

While stating candidly that the volatility event of the time was impacting the short-VOL trade and general trader population in the volatility complex, Golden informed the New York Times of his outlook, which remain unchanged from his many publications over the years on the subject matter.

“Nonetheless, he said on Tuesday that he was still wagering 21 percent of his portfolio, or $600,000, that volatility would fall as it had in the past.”

There are several reasons that volatility falls over time. One such reason is noted above, surrounding correlations. We can see that correlations greatly affect volatility and even as volatility looks cheap with a present reading of 12%, implied volatility over the next 30 days may find volatility still falling. If we step back for a moment and take a look at some of the greatest sector rotation the market has seen in years, we can make such an assertion. Of course, correlations aren’t the only driving factor of volatility, but wow! The retail sector detaching from consumer staples and the usual tech sector decoupling serve to prove that correlations are an important driving force behind volatility or the lack there of volatility.

Seth Golden believes that while correlations are a major driving force behind the rise and fall in volatility, desensitization is another driving force. For much of the last few months, investors have been forced to contend with a host of geopolitical headwinds as fears of rising inflation litter analyst commentary daily. The pairing of these issues with what appears to be an extended bull market and economic cycle has also proven a daunting task for the average investor to overcome. But as many investors can now plainly see expressed in the BAML survey of global fund managers within this article, markets follow earnings over time. If investors would choose history over daily news commentary that sometimes serves to overshadow the earnings outlook, they would also understand why volatility has fallen precipitously since February. But let’s get back to the theory of desensitization and the VIX.

Investors and the markets have overcome some of the most fearful circumstances of our time. The dotcom bubble bursting in 1999 proved a hurdle for investors in terms of trusting the market and its ability to value new technologies and paradigm shifts. Then came 9-11! The horrific attack on the country served to plunge the economy into a shallow recession, with equity markets following suit. And in 2008 investors were challenged like never before during the Financial Crisis. Millions of jobs were lost; homes were abandoned and later foreclosed in record numbers. Banking institutions were liquidated and forced for sale. The auto industry looked into the abyss of its existence. Even with such dire times, the population, industry and financial markets rose from the depths to find equity markets achieving record levels thereafter. One could say investors have become hardened to the supposition of “troubling times” that may lie ahead when compared to the past. This is the desensitization theory Golden refers to in many articles and conversations with the media.

If you were wondering how Golden has done since the February 2018 period, take a look at the noted “wager” and perform the math based on the difference in the VIX. But where are the media pundits now when it comes to detailing Golden’s wager or participation in the short-VOL trade? Crickets! That’s the media folks!

Our society has overcome and grown even through the hardest of times and come to find that we may bend, but… break we shall not! So while the VIX may soon rise from the depths, it will always be found to return once again… in time!

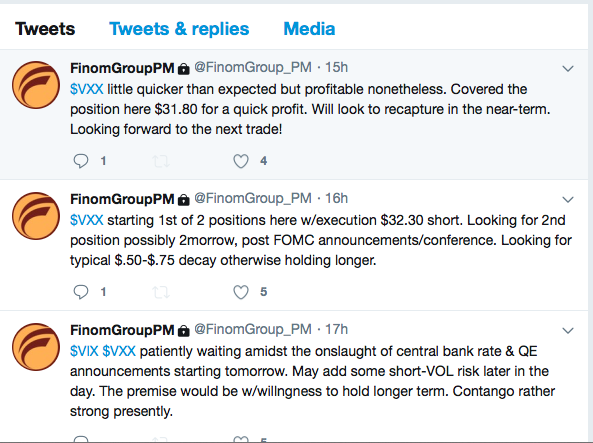

So it is with that, once again, Fimom Group alerted its subscribers to another identified trading opportunity within the volatility complex of VIX-Exchange Traded Products during yesterday’s trade. Late in the trading day the VIX rallied into positive trading territory after spending much of the day in the red. With the Nasdaq rallying and a lack of interest in the .SPX options market, Finom Group shorted iPath S&P 500 VIX Short-Term Futures ETN (VXX), as indicated in the screen shot taken from its private twitter feed (subscription needed).

Today will prove another interesting day for investors and the equity markets with the FOMC set to deliver a .25% rate hike at 2:00 p.m. EST. What will be most important to investors is the Fed’s economic and interest rate outlook.

“So if the Fed optimistic on the economy, raises its interest rate forecast, or even announces that Powell will hold press conferences after every meeting, any and all of those could be viewed as “hawkish.”

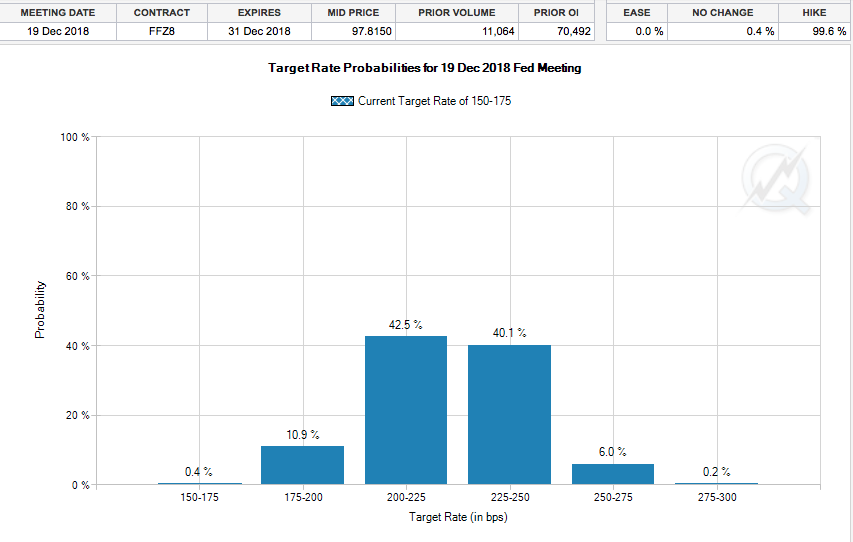

The Fed’s dot plot, a chart with anonymous Fed officials’ forecasts on interest rate expectations will foretell whether or not it intends to raise rates one or two more times this year. The chart currently shows three rate hikes for this year, but it’s a very close call based on the positioning of the dots, so any slight move could add an interest rate hike in December. At present, Fed Funds contracts show a 40% chance of a 4th rate hike in 2018. This could change greatly post the Fed’s announcement this afternoon.

Finom Group does not believe a 4th rate hike should be signaled at present and with nearly 6 months of the economic cycle yet to play out for 2018. The Fed’s primary gauge on inflation, PCE, is running in-line with the Fed’s 2% inflation target, but the Fed has also said it is allowing for inflation to run hotter for the time being in order to also achieve its symmetric inflation objective.

Beyond the FOMC event of the day, investors will also be confronted with the European Central Bank’s announcement on QE on Thursday, only to be followed by the Bank of Japan. It’s a week of central bank headlines that will hit the tape and likely cause…you guessed it, volatility! But heck, a little volatility can be healthy for markets.

*In memory of his fearless genius, Steve Jobs!*