You’ve heard the old adage, “It’s all fun and games until the Fed raises rates”, haven’t you? Of course that’s more a derivative of the more understood adage, but after a market pullback that ensued on the heels of the Fed announcing a .25% rate hike yesterday, I thought it fitting. So here we go and let’s get down to what the Fed announced and discussed in its press conference yesterday.

The Dow Jones industrial average fell 119.53 points to finish at 25,201. The S&P 500 lost 0.4% to close at 2,775.63. The Nasdaq composite rose to a new intraday high early in the session. The index later dropped 0.11% to finish at 7,695.70 following the Fed’s decision.

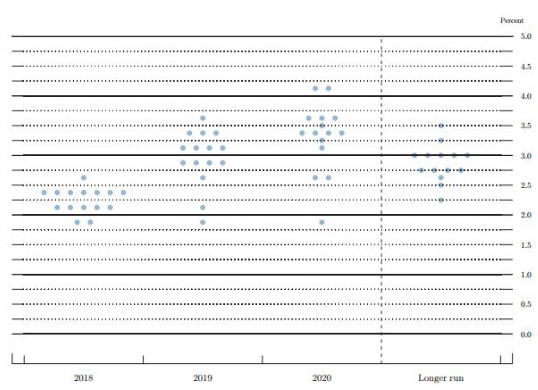

The Fed did indeed raise rates by .25% at its latest policy meeting, but the more important decision was made with respect to the Fed’s dot plot outlook. As depicted in the Fed’s dot plot below, the Fed now forecasts 2 more rate hikes in 2018.

This week’s two-day meeting saw one member shift the estimate to 2.25% to 2.5 percent. Two more increased their estimates a quarter point to 1.75% to 2 percent. Calculating the median of the dots pushed the overall forecast to equate to 2 more hikes this year, which are likely to take place in September and December. Before the meeting, the CME’s FedWatch tool had been pointing to a 46.5 percent chance of a fourth hike. In other words, Fed Funds Futures viewed the latest decisions made by the Fed as being more hawkish than dovish.

“Information received since the Federal Open Market Committee met in May indicates that the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Job gains have been strong, on average, in recent months, and the unemployment rate has declined.

The median real GDP forecast from the FOMC rose to 2.8%, up from 2.7%, for this year. There were no changes for 2019 and 2020, and the longer run median forecast remained 1.8 percent.”

Despite the added hike, officials still see the long-run funds rate at 2.9 percent after peaking at 3.4% in 2020. The extra hike, though, pushes the rate past “neutral” in 2019, a little sooner than anticipated. They still see GDP rising 2.4% in 2019 and 2% the year after, and longer-range growth at 1.8 percent.

Finom Group has openly stated the Fed should not increase its target funds rate for 2018 by adding another rate hike. Having done so, now and with a variety of headwinds that still remain ahead in the fiscal year, the Fed raises the risk of needing to pullback from its more hawkish tone and outlook later in the year. While the present conditions may warrant a more aggressive Fed, the geopolitical environment could bleed into the economy down the road. Within the Fed’s statements and Q&A session with the media, Chairman Powell did offer that business raised concern over the U.S. administrations current trade policies. Such concerns were weighing on these businesses when it comes to capital deployment and hiring.

“You’re beginning to hear reports of companies holding off on making investments and hiring. Right now, we don’t see that in the numbers at all. The economy is very strong. The labor market is strong. Growth is strong. We don’t see that in the numbers,” he said. “I would put it down as more of a risk.”

The final word on the latest Fed outlook and rate forecast from Finom Group could be characterized in one word, disappointing! We are forced to recognize that as Chairman Powell has attempted to quell fears that the Fed would be more hawkish than its actions assume; actions speak louder than words. The takeaway for investors would otherwise recognize this FOMC cycle as being hawkish and hopefully, rightfully so. While the rate decision and outlook are in-line with the present economic conditions and have resulted in a pausing of the equity market rally, it may turn out to be just that when we put things into their more appropriate perspective.

Even if the Fed fulfills its revised forecast, it will likely find rates higher at year’s end, but still below levels achieved in 2007 and with a lower 10-yr Treasury yield. Rising rates and yields will impact the consumer, but the consumer has a plethora of more options when it comes to consumer credit than in past decades. So let’s talk a bit about the impact of further rate hikes on the consumer.

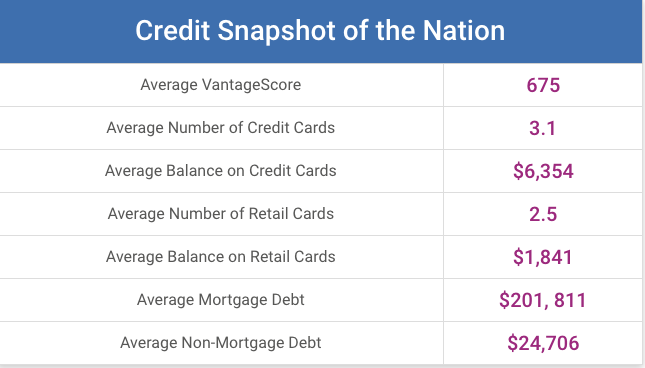

The typical American has a credit card balance of $6,375, up nearly 3 percent from last year, according to Experian’s annual study on the state of credit and debt in America. Total credit card debt has reached its highest point ever, surpassing $1 trillion in 2017, according to a separate report by the Federal Reserve.

Adding on a 25 bps increase will cost credit card users roughly $1.6 billion in extra finance charges in 2018, according to a WalletHub analysis. But even with this added consumer expense, the consumer has greater choice than in past economic cycles where the Fed was raising rates and financial institutions are tripping over themselves in a race to the bottom when it comes to funding and financing. Nowadays, the consumer can shop around for a better rate or a zero-interest balance transfer offer to insulate themself from further rate hikes. Once a zero-interest rate balance is achieved, the consumer can comfortably pay down their outstanding balance. Rising rates are not without their offset.

When it’s all said and done, rates rising from where they are today and where the Fed defines the neutral rate remains quite benign with respect to its affect on the economy. As such, any near term pullbacks in the equity market are likely to be viewed as a “buying opportunity”. The Fed has made it a little harder to own stocks, but there’s no need to panic. Investors should keep in mind that there are other factors that will determine the direction of the equity markets in the mid-term. One of those factors is today’s European Central Bank (ECB) meeting and announcements on their Quantitative Easing program.

The ECB is expected to outline the bank’s plans for winding down its bond-buying program when it meets this morning. The central bank is scheduled to release its monetary policy statement at 12:45 p.m. London time, or 7:45 a.m. Eastern Time. That will be followed by a press conference with ECB President Mario Draghi at 1:30 p.m. London time.

Analysts expect the central bank to gradually taper its asset purchases beginning in September. An official end of asset purchases is expected by the end of 2018. Economists’ don’t expect the ECB to actually raise rates until late 2019. Global markets could have an outsized reaction to the ECB’s announcements today, which may further prove to linger in Friday’s trading session; for better or for worse we will discover.

Some analysts and economists are suggesting that the ECB’s meeting will have greater impact on global equities given the minimal economic growth and high debt to GDP’s in the region. We’ll see what the outcome is ahead of the market’s open on Wall Street. Moreover, investors will also be bracing for the Bank of Japan’s scheduled release of its monetary policy decision on Friday. Most analysts aren’t expecting the bank to shift policy, even as it continues to ease up on monthly buys of Japanese bonds.

As noted earlier, the Fed has recognized that the U.S. administrations trade policies are starting to bleed into business sentiment and capital expenditure decisions on the part of businesses. While not impacting the economy at present, such sentiment can affect the equity markets as we’ve seen with recent headlines surrounding trade tariffs. Such an announcement is now expected on Friday. The following is an excerpt from Politico discussing the potential announcement of trade tariffs on China.

“President Donald Trump is expected to impose tariffs on Chinese goods as soon as Friday or next week, according to two sources briefed on internal deliberations, a move that is sure to further inflame tensions and spark almost immediate retaliation from Beijing. The administration on Friday is planning to publish a final list of Chinese goods that will take the hit.

“I came away thinking that he was suggesting in the press conference in Singapore that although Xi Jinping was a close friend [and] that he’d provided help on North Korea, that the president had no choice but to turn up the heat on China,” said Scott Kennedy, a China expert at the Center for Strategic and International Studies.”

Finom Group believes that imposed tariffs on China will result in a short-term pullback in equities or risk-off scenario for markets. Having said that, trade negotiations that have seemingly pinned the U.S. against more favored, traditional allies, have been shrugged off by investors.

With respect to U.S./China trade spats, it is important to understand that the impact on the U.S. economy will be of little consequence as the U.S. is a net importer of goods. The greatest impact will be levied against China, as it is a net exporter in the relationship. We’ll see how this plays out come Friday.

As we noted earlier in the week, this was always going to be a frenzied week with a focus on central banks with a backdrop of light economic headlines. The Consumer Price Index proved innocuous this week, coming in as expected and ticking up by .2% month-to-month and up 2.7% over a 12-month period. Today’s economic data release will also give investors insights into the strength and confidence of the consumer. Monthly retail sales data is due out at 8:30 a.m. EST today. After growing .3% in April, retail sales are expected to continue this growth in May. Economists expect May retail sales to grow by .4% month-to-month, showing continued strengthening of consumer spending in the 2nd quarter of 2018 and after a slow start to the year.

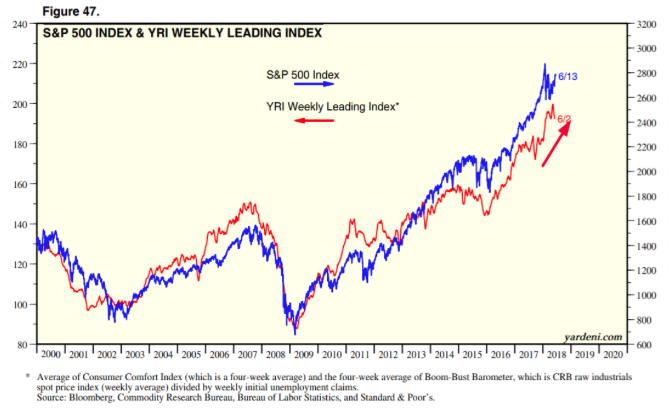

Let’s end this daily market outlook with something of a positive data point or fact surrounding one of Finom Group’s favorite and legendary economists. Ed Yardeni publishes a pretty interesting leading indicator for the stock market: it’s the average of the Consumer Comfort Index and CRB raw industrials index divided by weekly Initial Claims. Take a look at this chart below:

Historically, the stock market always goes up when Yardeni’s leading indicator goes up. What is it you see in the chart right now? It doesn’t mean the leading indicator can’t suddenly shift, but it does relate the importance of the consumer and the labor market quite well. And what drives the U.S. economy forward? Correct, a strong labor market that produces a strong consumer. It’s going to be a wild end of the trading week folks!