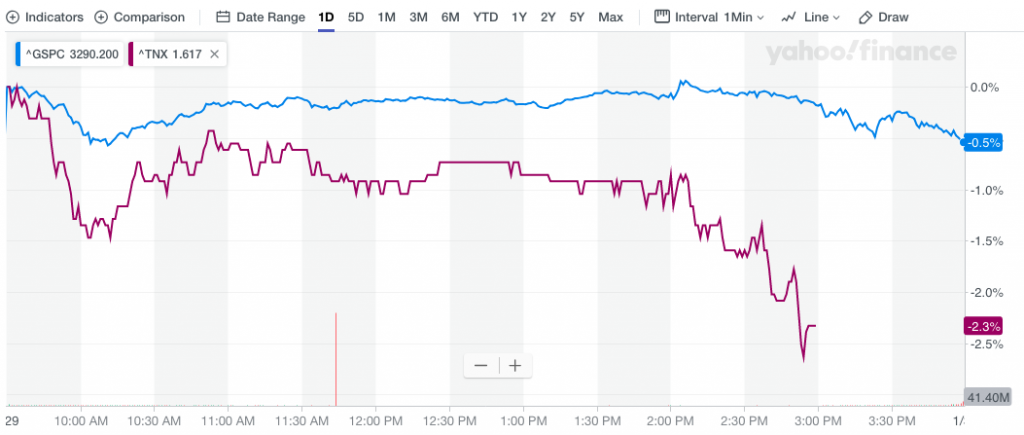

On Wednesday, and heading into the FOMC rate announcement, the S&P 500 (SPX) was near its high of the session. Once the press conference commenced, however, the mood on Wall Street shifted and equities fell along with bond yields. As FOMC chairman Jerome Powell discussed a desire for the Fed’s price stability/inflation mandate to find greater achievement, the 10-year Treasury yield fell below 1.60% and to an intraday low below 1.59% before a slight rebound at the end of the session. The fear of the yield curve further flattening brought about a flight to safety and avoidance of risk.

Beyond the inflation comments by Jerome Powell, he was also forced to field a number of questions regarding the Repo market operation and balance sheet. It was asked of Powell during the conference as to whether or not he believed the large asset purchases and expansion of the balance sheet was reason for risk assets rising. First, of course, correlation isn’t the same as causation. Just because 2 things are moving together doesn’t mean that one causes the other. Second, and more importantly, the notion that the Fed’s actions are fueling a stock market bubble isn’t supported by how the Fed’s T-bill purchases are affecting short-term interest rates or how the Fed’s actions are increasing liquidity in the financial system. Thirdly the main reason stocks have been rising through the Fed’s balance sheet expansion is that the risk premia has shifted more heavily in favor of risk assets that are projected to express an earnings rebound that coincides with an expansion cycle.

At the beginning of September, before the upward pressure on repo rates and the Fed’s decision to buy $60 billion of bonds per month, the spread between the effective fed funds rate and the rate that the Fed pays on reserve balances was about three basis points, or three-hundredths of a percentage point. Today, that spread has fallen to roughly zero. When the supply of bank reserves increases substantially, this puts modest downward pressure on the fed funds rate because more of the trading activity occurs between banks and the government-sponsored enterprises that cannot earn interest on their cash balances at the Fed, rather than trading among banks.

Similarly, the Fed’s bond purchases have had only a small impact on the level of yields relative to the fed funds rate and the interest rate that the Fed pays on reserves. Even here it is hard to discern much impact from the Fed’s asset purchases. At the beginning of November, after the Fed’s last rate cut, the spread between the four-week yield and the effective fed funds rate was three basis points. That spread now is close to zero.

So it isn’t rates. But couldn’t it be that the rise in bank reserves is increasing liquidity, fueling the equity market? The problem with this argument is that when the Fed buys bonds and increases the amount of reserves in the banking system, that liquidity can’t go elsewhere. It can’t move from bank to bank as households and businesses shift where they hold their bank balances. The only exception is if bank customers decide to increase their holdings of cash. But if they do that, that reduces the amount of excess reserves in the banking system.

The Fed’s bond purchases substitute a bank reserve (essentially equivalent to a one-day bond) for a slightly longer risk-free asset (bond) that the Fed now holds in its portfolio. There are no funds created to purchase equities.

If we review quantitative easing, this was a very different operation. The quantitative easing by the Fed from 2009 to 2013 removed long-duration, fixed-income assets (bonds) from the market. This pushed down long-term bond yields significantly and made equities relatively more attractive.

There are much better explanations for the recent rise in the U.S. stock market than the Fed’s T-bill purchases. I would put three developments front and center:

- The Fed cut its fed funds rate target by 75 basis points in 2019 to a range of 1.5% to 1.75%. Monetary policy is more accommodative now than a year ago. Longer-dated yields are also lower as a consequence.

- The Fed has signaled that it is unlikely to raise rates until inflation climbs meaningfully above the central bank’s 2% inflation target. As a result, both the Fed and market participants believe that monetary policy will remain on hold in 2020.

- The risk of a U.S. economic slowdown seems to have subsided. Most notable is the abatement of trade tensions with China and the expectation that in an election year, they will remain subdued this year.

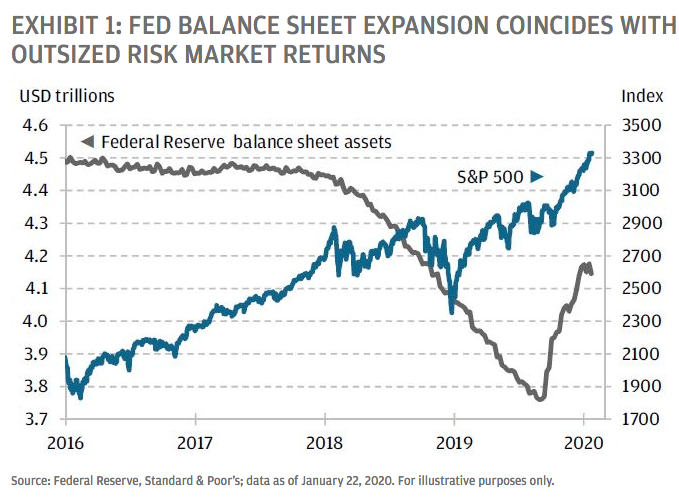

As we can see from the chart above, the Fed’s Repo operation began in Q4 2019, but the S&P 500 was rising since Q1 2019. The Fed was curtailing its balance sheet throughout 2018 and yet for much of 2018 the S&P 500 was rising as well. Again, this demonstrates that just because two things are moving together doesn’t suggest causation, but rather coincidence. We’re not going to go so far as to suggest that the Fed’s Repo operation or balance sheet expansion aren’t prohibitive to equity market sentiment, but that’s about all these issue can lend to equity markets, sentimental favor. With all that being outlined, let’s take a look at what changed in the Fed’s statement:

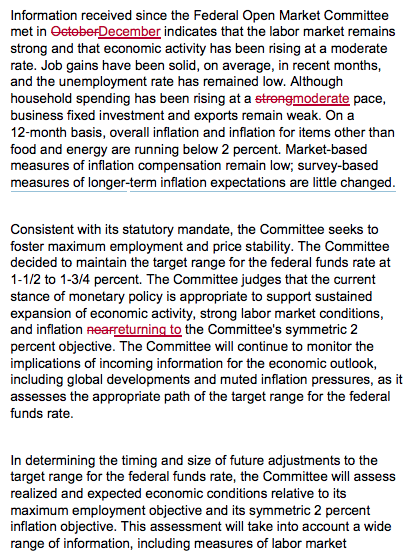

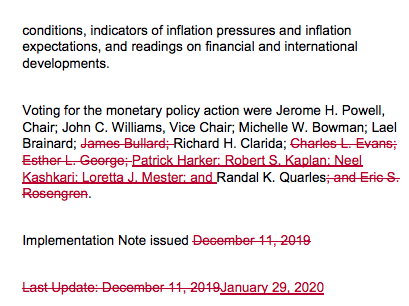

In keeping rates unchanged, the FOMC adjusted the language to reflect that policy is geared toward “inflation returning to the Committee’s symmetric 2 percent objective.”

That language differed from the long-standing statement that the Fed was looking to get inflation “near” the benchmark that it considers healthy for a growing economy.

In recent months, Fed officials have expressed concern over the inability to get inflation to the 2% level. While consumers welcome low prices, the Fed worries that low expectations will continue to keep inflation and, consequently, interest rates at below-normal levels. The reality of the situation is the inability to stoke meaningful or sustained inflation has become an impossibility and now more concerning for the Fed.

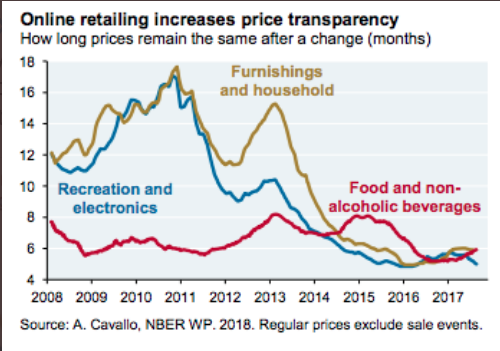

Technology and the information technology era have stifled inflation and pricing initiatives and forced traditional brick and mortar retailers into a position whereby they are constantly found without pricing power and discounting in perpetuity. Through the invent of mobile technology, the consumer can essentially determine the best price of any non-exclusive good and service.

The following chart from J.P. Morgan on pricing trends since smartphones and tablets have attracted mass market consumer adoption is at the heart of the trend in retail pricing in-elasticity and at the heart of the Fed’s inability to create any inflation without stoking economic growth.

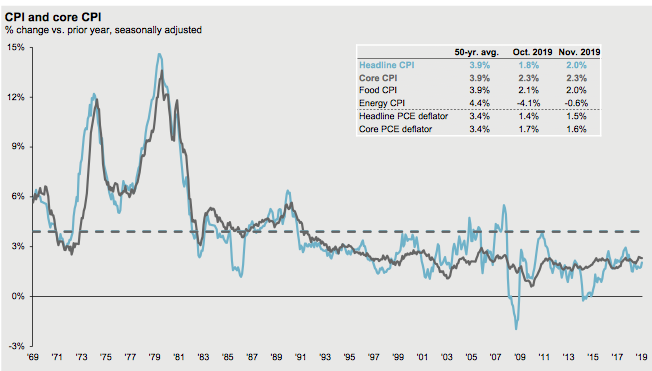

A more broad-based measure of inflation can be viewed in the long-term trend of the Consumer Price Index. The CPI shows a slow but steady decent in consumer prices over time. It wasn’t until 2011 that smartphones became popularized, which coincides with the peak in CPI prior to 2008.

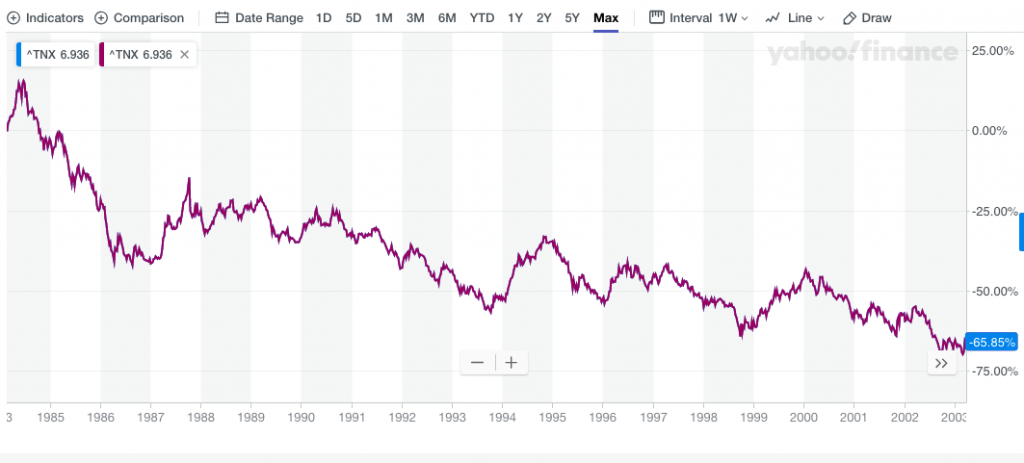

The Fed is stuck, like it or not and for those who think they are able to get in front of the inflation battle, that’s simply not what the history of the 10-year yield proves. If one looks at the chart of the 10-year yield since the errand monetary policy experiments of the 1980s, they come to find that interests rates are determined by the psychology of the consumer in a consumer-driven economy. And based on the charts displayed above, the consumer has a firm understanding of former rates compared to the rates of today.

And this brings us back to the sell-off within the S&P 500 Wednesday and the continued drop in bond yields through Thursday morning. The bond market heard read the Fed’s revised statements regarding it’s inflation mandate and hear Jerome Powell indicate the Fed’s desire to achieve the 2% symmetric, inflation target. So what is it you think the Fed is going to do to stoke inflation and achieve its inflation mandate?

In the recent past, lowering rates hasn’t brought about a return to the 2% inflation target. One would think that by lowering rates, this would boost economic activity, right? Unfortunately, the latest bout of easing only proved to stabilize economic activity given the broader cause for lowering rates, a global economic slowdown brought about by the protracted trade feud between the U.S. and China. Simply put, bad timing for the Fed which would otherwise likely find that lowering rates improves economic activity and lifts prices/inflation. To this point, the Fed had been harping on a message in it’s semi-annual testimony before Congress, suggesting that fiscal policies would be needed to improve pricing power and economic growth longer-term. So again, what is the Fed to do in order to return to the 2% symmetric inflation target? There really is only one thing for the Fed to do in Finom Group’s opinion, lower rates further.

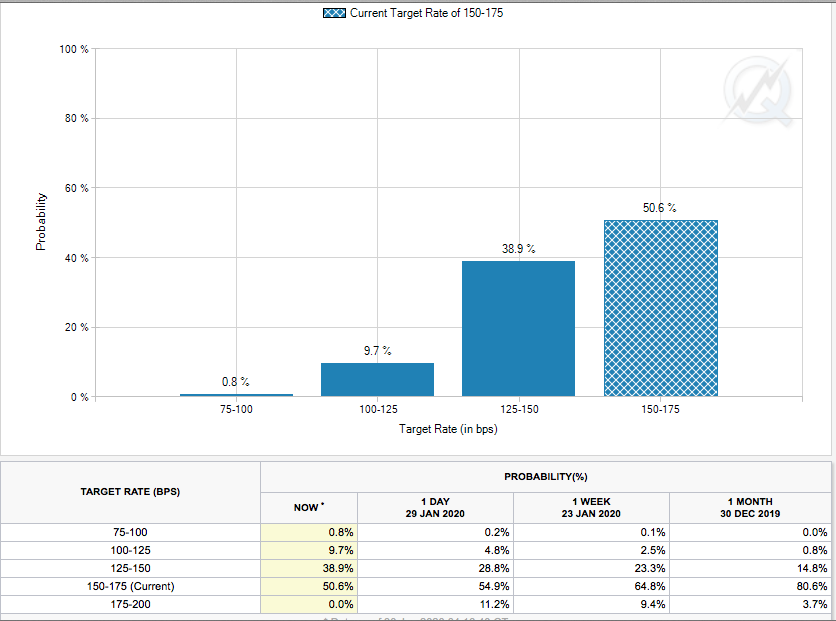

During Tuesday’s press conference, we believe that Jerome Powell was setting the stage for another rate cut at some point in 2020. While most economists and strategists hadn’t been projecting any rate moves in 2020, we think that will quickly change. In fact, Fed Fund Futures are already adjusting to a greater probability for a rate cut come June 2020.

Just one week ago, the probability of a .25 bps rate cut in June was 23 percent. That probability rose to nearly 29% on Wednesday and has grown to nearly 39% as of Thursday January 30th. The bond market has quickly taken up the idea that the only thing the Fed can do is take advantage of the White House administration that is unlikely to upset the economic outlook during a presidential election cycle. Whereas in the past, rate cuts only served to stabilize economic growth from the downturn caused by geopolitical trade tensions, they can now stimulate growth and some inflation with a more amicable White House administration that desires reelection. Finom Group is of the opinion the Fed will choose to heat up the economy later this year and both the bond market and Fed Fund Futures are indicating much the same belief presently.

In addition to all the Repo market and inflation talks, the Fed also recognized issues surrounding the Coronavirus epidemic.

“It’s a serious issue. There is likely to be some disruption of activity in China and probably globally. We’ll just have to wait to see what the effect is globally.”

So far, more than 7,700 people, mostly in China, have been infected and 170 individuals have died from the new coronavirus since it was identified in December. The quickly spreading virus is weighing on the economic outlook of China, Hong Kong and other countries, as global and domestic travel is curtailed and companies close factories, cancel flights and take other steps to contain the virus’s spread.

The outbreak could cause China’s real GDP growth to slow to below 4% from the 6% pace in the fourth quarter, with a bigger impact than SARS in 2003, Nomura economists led by Lu Ting wrote in a report to clients late Wednesday. Here is what Wells Fargo Portfolio Management team had to offer:

“In conclusion, we do not think the coronavirus is a catalyst for reallocating portfolios, but it has provided an opportunity to reposition specific exposures. We also believe it will likely provide opportunities to get into stocks with strong fundamentals. We expect to see high earnings risk for vulnerable sectors, but some of these risks will, in our view, be well-compensated risks.”

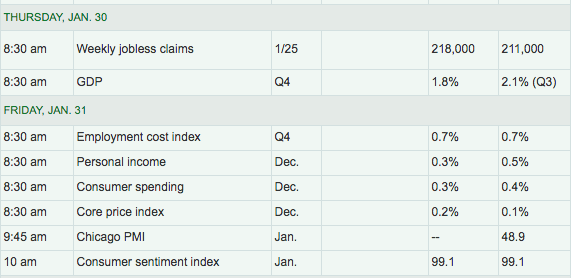

As Asian markets continue to fall due to the Coronavirus economic impairment potential, U.S. equity futures are also sharply lower on Thursday and ahead of the first look at U.S. Q4 2019 GDP.

After the release of the U.S. trade deficit data showed the deficit jumped 8.5% in December as tensions with China eased and imports surged, forecasts for Q4 2019 GDP have been revised lower. The gap in goods climbed to $68.3 billion in the final month of 2019 from $63 billion in November, the government said Wednesday.

JPMORGAN: “We are lowering our forecast for 4Q real GDP growth from 1.7% to 1.4% .. This downward revision comes with today’s numbers pointing to weaker net exports, inventories, and equipment investment than we had previously anticipated ..”

Goldman: “Following today’s data, we lowered our Q4 GDP tracking estimate by one tenth to +1.8% (qoq ar) ahead of tomorrow’s advance release.”

Merrill: “The data sliced 0.4pp from our 4Q GDP tracking estimate, bringing us down to 1.6% qoq saar-as a reminder, the advance 4Q GDP estimate will be released tomorrow morning (1/30) at 8:30 am ET.”

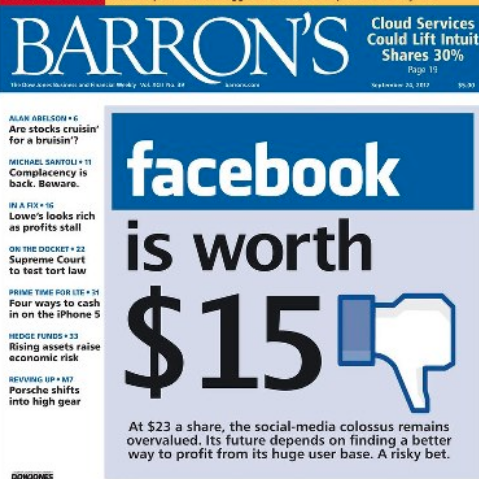

As investors await earnings after the closing bell Friday from Amazon, it’s FANG brethren Facebook (FB) found a severe reaction to the social media’s Q4 2019 results. Facebook said it earned $7.35 billion, or $2.56 a share, against expectations of $2.53 a share, according to analysts polled by FactSet. Facebook revenue rose 25% to $21.08 billion, beating estimates of $20.9 billion. (photo from Sept, 24, 2012)

“We had a good quarter and a strong end to the year as our community and business continue to grow,” Chief Executive Mark Zuckerberg said in a statement announcing the results. “We remain focused on building services that help people stay connected to those they care about.”

Monthly active users improved 8% to 2.5 billion, compared with expectations of 2.49 billion. User growth in North America was a concern, however, as Facebook gained just 1 million new users in the U.S. and Canada from the previous quarter, to 248 million. In the same quarter a year ago, the figure was 242 million.

Facebook Chief Financial Officer David Wehner acknowledged during a conference call with analysts late Wednesday that the company is experiencing “slower growth in more mature markets.”

“The market expects more from Facebook,” Forrester analyst Melissa Parrish told MarketWatch in a phone interview. “Its impressive revenue and user gains just don’t seem to be good enough.”

Analysts also pointed at continuing increases in Facebook’s costs and expenses, which jumped 34% to $12.2 billion from $9.1 billion a year ago. As a result, operating margins eroded to 42% in the just-concluded quarter, from 46% a year ago and 57% two years ago.

Evercore analysts suggested that investors were expecting much more than the analysts in a Facebook earnings preview, suggesting that the buy side was expecting revenue growth of 27.5% to 28.5% and margins of 43.5%. Instead, revenue growth came in lower than 25%, and margin was about 42 percent.

Baird analyst Colin Sebastian suggested that the realities facing Facebook in a note just after the numbers were released, writing, “the modest size of the revenue and EPS beat may disappoint some investors accustomed to bigger outperformance.”

All Facebook investors are accustomed to bigger outperformance than what they received in Wednesday’s earnings report. Finom Group is of the opinion that Facebook is simply a victim of it’s own success and the rate of growth for a mature company is slower than that from its adolescent years. Analysts will be out with their bandwagon-share price sentiment, but the reality is akin to the screenshot from the Barron’s 2012 cover page, naysayers are consistently proven wrong about Facebook’s earnings prowess. It may simply take some time before investors get accustomed to a slower rate of growth, which we believe patient investors will be rewarded for with time.

More tech earnings are being delivered on Thursday, but potentially none more important or widely anticipated as Amazon. Not only is Amazon a key tech titan, but it lends itself as a consumer metric as well, given it dominates the e-commerce retail market.

The market and investors/traders remain with hurdles ahead, some of which are being discounted during the current market pullback. Uncertainties facing investors presently are outlined below:

- Coronavirus

- Iowa Primary

- Fed rate outlook

- Yield curve

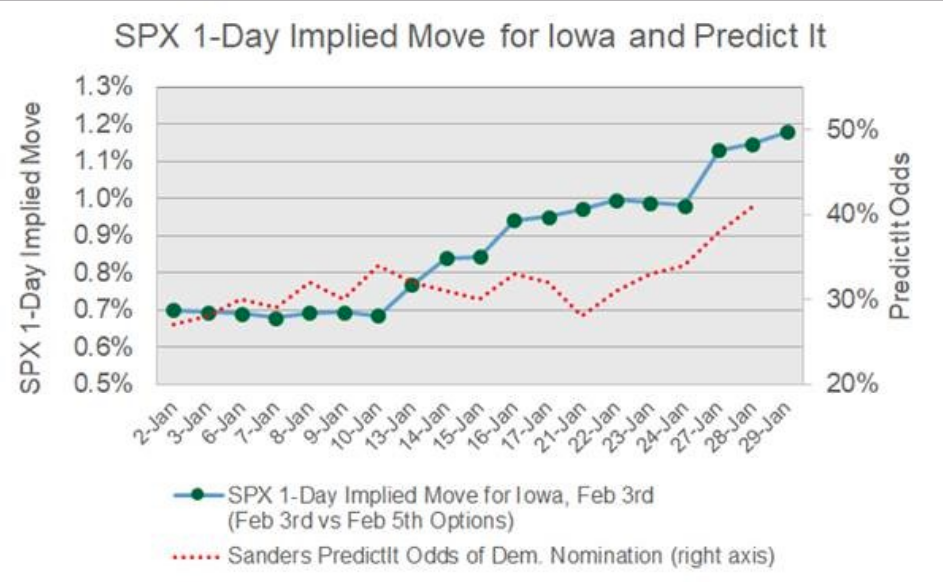

The market/investors are clearly concerned about the upcoming Iowa Primary event. For Super Tuesday .SPX short dated options are now pricing a +/- 1.2% move following the Iowa results, up from just 0.7% move in early January. This has increased along with candidate Bernie Sanders surging in the polls.

The last bullet point is likely the rational for future concerns about the economy. The yield curve has been flattening through the first month of 2020. As the yield curve flattens, it brings about fears of another inversion, which fuels speculation of a recession.

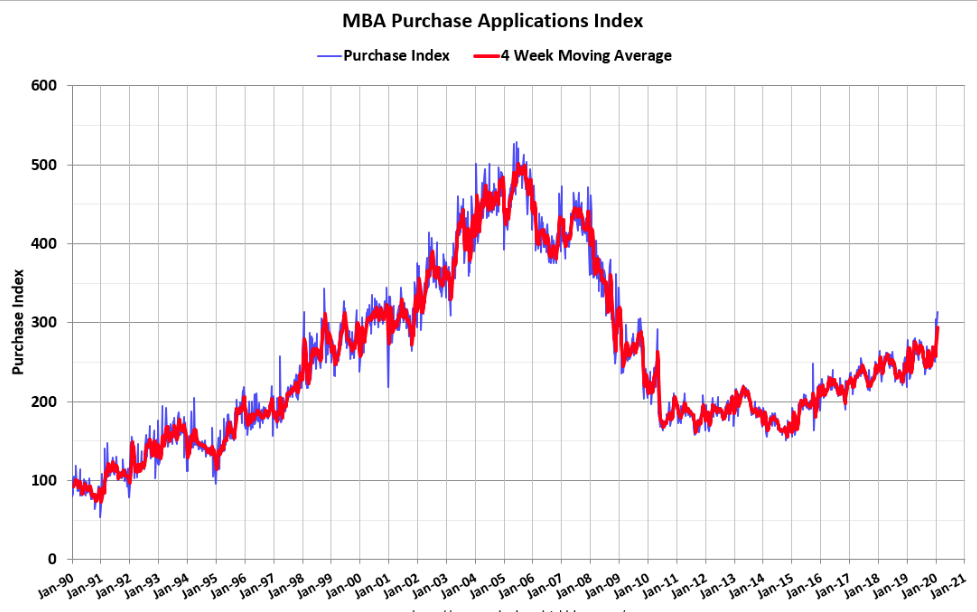

We believe, again, that these fears will be proven “overblown”. As rates edge lower, they are simply providing a positive feedback loop within the mortgage market and housing sector.

“Mortgage applications continued their strong start to the year, as borrowers acted on the drop in mortgage rates last week. Rates were driven lower by investors’ increased concern about the economic impact from China’s coronavirus outbreak, in addition to existing concerns over trade and other geo-political risks,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting. “With the 30-year fixed rate at its lowest level since November 2016, refinances jumped 7.5 percent. Purchase applications grew 2 percent and were more than 16 percent higher than the same week last year. Thanks to low rates and the healthy job market, purchase activity continues to run stronger than in 2019.”

Just this week, new home sales for December were reported at 694,000 on a seasonally adjusted annual rate basis (SAAR). Sales for the previous three months were revised down. Annual sales in 2019 were at 681,000, up 10.3% from annual sales in 2018, and the best year for new home sales since 2007. This was well above analysts forecast for sales in 2019, and the growth mostly happened in the second half of the year.

Thursday’s market activity may be found with more selling pressure, recapturing the gains from “turnaround Tuesday”. Nonetheless, Finom Group remains in the bullish camp longer-term and believe earnings are trending positively despite the issues of the day concerning Coronavirus, the yield curve/Fed and the Iowa Primary. Stay nimble and look for those high probability trades and investments as near-term equity market weakness is likely a longer-term opportunity.