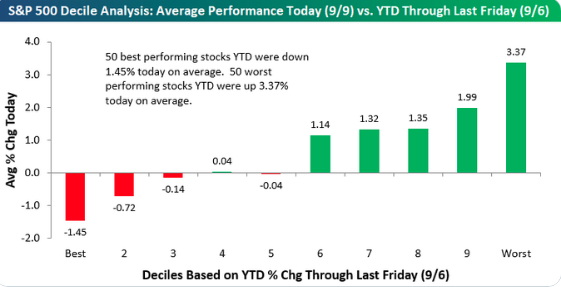

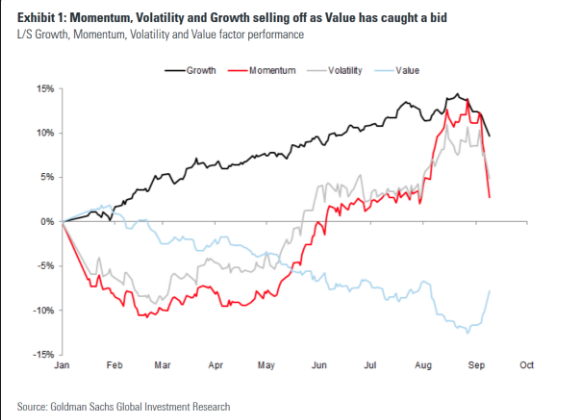

It has been kind of a “funky” trading week thus far and after 2 straight weeks of strong dip buying activity. With the first 2 trading days of the week completed and rather flattish S&P 500 moves, investors have been scratching their heads. Many investors and traders have been watching underperforming sectors and stocks in favor this week while the former beloved sectors and stocks fall very much out of favor. The following chart from Bespoke Investment Group offers a snapshot of what’s been going on in the market as sector rotation is in full force this week.

As depicted in the bar chart, the 50 best performing stocks of the year have all of a sudden sharply reversed while the 50 worst stocks of the year were up nearly 3.5% on Monday alone. That momentum carried forward into Tuesday. Stocks such as Shopify (SHOP) and Chipotle Mexican Grill (CMG) have been absolutely roiled in the last few trading sessions with no headlines other than a price target upgrade on CMG, and yet… The momentum type stocks have simply halted their momentum and are found, like Shopify, filling gaps that were formerly created as their price appreciation ramped earlier in the year.

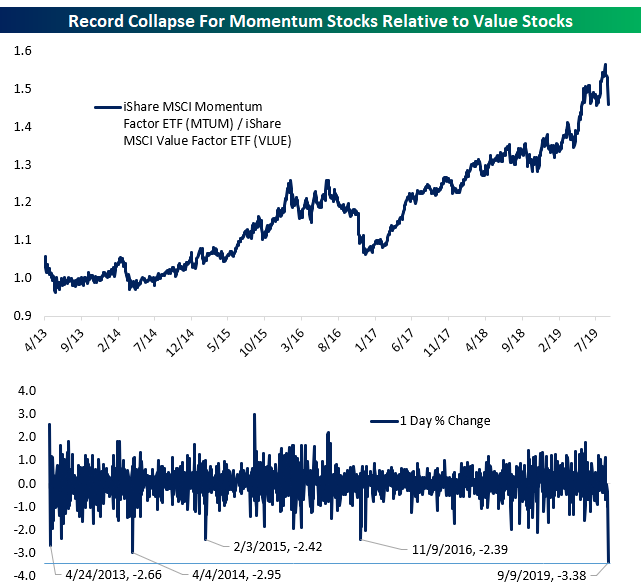

Over the last couple of trading sessions, there was an unprecedented collapse for stocks with high price momentum relative to stocks with value characteristics. These two baskets of stocks are most easily tracked using the iShares Momentum (MTUM) and Value (VLUE) factor ETFs.

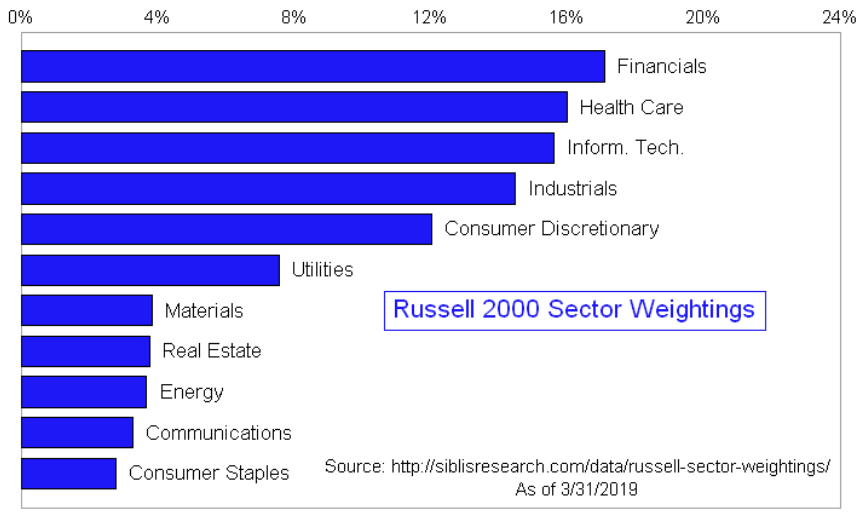

As shown in the chart above, Monday was a demolition day for Momentum (MTUM) relative to Value (VLUE). Part of this was a function of rates, with recent upticks in short and long term interest rates driving utilities and other defensive stocks with strong trailing momentum lower, while banks rallied as rates rallied. This is also why the banking/financial ETFs (XLF and KRE) have rallied in the last few trading sessions along with the Russell 2000, which is heavily weighted with regional banks. Check out the Russell chart below:

Here is the bigger picture takeaway as the Russell, small caps play catch up to the large caps: This is only occurring because yields are moving higher over the last 5 trading sessions. That helps bank profits on net interest margin. Again, look at the heaviest weighted sector within the Russell?

And here’s the “rub”. Recall all the warnings about small caps signaling something ominous on the horizon for the broader stock market? Based on what we’ve seen lately, NO! It turns out this wasn’t about small caps sending some economic signal or warning. It was and has been a sector story, weighing down the index given its reliance on the financials that have been weighed down by declining yields.

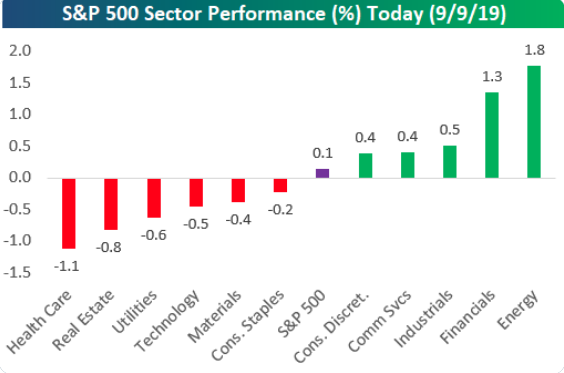

Of course it has been a broader issue than that of late. Software stocks have been rocked while oil & gas stocks surged (XLE), automakers rallied while stable consumer staples (XLP) names took a hit (KO and PEP) Essentially, everything that had been working and while rates were moving lower, had reversed as rates reversed to the upside.

Finom Group had been discussing the possibility of increased market churn and realized market volatility, in the Trading Room with members, once the heavily concentrated and overbought bond market trade began its inevitable unwind. And that is exactly what is being played out in the equity market as sector rotation plays out and investors’ yield considerations shift. Here is what J.P. Morgan’s Marko Kolanovic (the man who moves markets) had to say about the sector rotation underway:

- We believe that the value rotation can continue and the broad market could move higher going into October negotiations, and if real progress is made, continue into a more sustained rally.

- This view is based on positioning, record factor spreads (e.g., value vs low volatility), and an unwind of some of the August technical flows in both rates and equities.

- Given that the S&P 500 is heavy in bond proxies and secular growth, we would expect higher upside potential in small caps, cyclicals, value, and Emerging Market stocks than the broad S&P 500.

- If the October negotiations fail, these moves could be unwound, but given the extreme low positioning and style tilt, we think the downside is limited.

Sanford Bernstein had their own thoughts on the momentum trade carnage over the last few trading sessions as follows:

- The move upwards in yields over the past few days triggered the collapse of Momentum yesterday.

- Momentum has de-coupled from Growth, it no longer represents Growth but represents a cohort of stocks that are dependent on falling yields.

- The rotation out of Momentum yesterday was accompanied by an 8bps move upwards in the US 10 year yield, marking the highest point for the US 10 year since mid-August.

- We note that high momentum stocks remain vulnerable from these high valuations and we expect downward pressure on earnings expectations

Nothing lasts forever in the markets and all trends are bound to break, so while the current momentum trade is unwinding and value above growth has found favor once again, this too shall come to an end. Of course the only question is the unknown, “when”; when will the sector rotation and momentum and growth to value trade come to an end? Nobody what anybody offers to answer in this regard, remember that nobody was forecasting the aforementioned shift in investor/trader appetite. Nonetheless, here is what CNBC “Mad Money” host Jim Cramer had to say about the sector rotations taking shape and what investors should consider:

“People seem to believe we could see some progress in the trade negotiations with China. Personally, I’m skeptical … but hope springs eternal. And, on top of that, there’s a belief that the Federal Reserve has no choice but to cut interest rates after Friday’s not-so-hot employment number.”

Because high-growth “never goes out of style for long, buy the dip in Salesforce.com and the nearly double-digit plunge in Okta.“

E-commerce company Shopify, despite a Baird analyst raising its sales estimates, dropped nearly 6%, and cybersecurity company Crowdstrike, despite reporting strong revenue in its recent quarter and raising its earnings forecast last week, plummeted almost 12%. Shopify is down more than 18% from its August high.

“There’s only one problem [in Shopify]: It doesn’t have much in the way of earnings. This [is a] $358 stock … that’s expected to earn roughly 70 cents a share for 2019. In the way of Crowdstrike, “the company still expects to lose money. Suddenly, this market doesn’t want to see some losses … Instead, it just wants cheap stocks and ones that are turning a bountiful profit.”

“Why not go back to value? The answer is because … they’re now hitting even the companies that have been consistent. Procter has been a massive outperformer, and they’re getting hit. The companies, by the way, that are being hit almost entirely beat the market, beat their estimates, but no one really seems to care.”

The market is a bit unsettling to watch play out on a day-to-day basis, especially when strong performers are being discarded for those underperformers that have underperformed for valid reasons. Macy’s has ralled from $15 to over $17 per share in the last few trading sessions and for what, lowered FY19 guidance, 3 consecutive quarters of gross margin contraction, faltering sales and lower YOY EPS? Target (TGT), on the other hand is down nearly $3 after raising FY19 guidance and beating most every analysts estimate in both reported fiscal 2019 quarters. Things that make you go hmmmmm? But remember, this too shall pass and the market is simply grappling with yields firming and moving higher presently.

The 10-year yield has bounced about 20 bps over the past five trading sessions, spurred by optimistic trade and geopolitical headlines. Finom Group still believes the 10-year yield’s fair value is at least another 20 bps higher than current levels, but we wouldn’t be surprised to see yields take a breather soon, especially before a pivotal European Central Bank decision. Fortunately, the 10-year yield’s ascent has helped normalize the shape of the U.S. yield curve, which was inverted at several points in August and has now re-steepened.

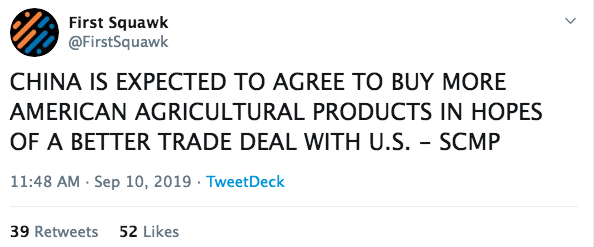

The headlines on trade have generally been such that have bred more optimism on trade lately than they had in late July and August. This has served to bring stability to yields and boost risk asset prices. Most recently, China has offered the probability of purchasing small amounts of U.S. agricultural goods.

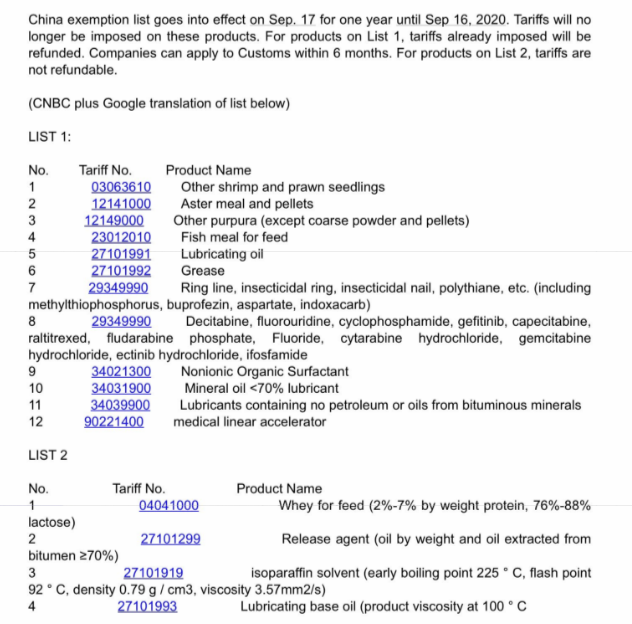

Overnight China’s Ministry of Finance announced plans to exempt 16 types of U.S. products from additional tariffs on Wednesday, including food for livestock, cancer drugs and lubricants.

The exemption, which is scheduled to go into effect from September 17, will be valid for a year through to September 16, 2020.

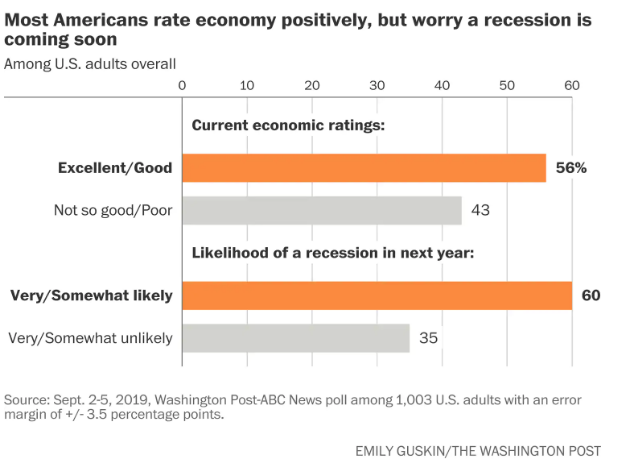

Regardless of the renewed optimism and conciliatory rhetoric on trade of late, fears of a looming recession remain present and at the forefront of investors and even consumer minds. President Trump is ending a tumultuous summer with his approval rating slipping back from a July high as Americans express widespread concern about the trade war with China and a majority of voters (6 of 10) now expect a recession within the next year, according to a new Washington Post-ABC News poll.

Despite what polled respondents suggest the fear for the future economy might be, Goldman Sachs David Kostin doesn’t see a recession over the next 6 months at least. Kostin’s response to the decline in the ISM manufacturing index, which last week fell below 50 points for the first time in three years is one of opportunity for investors. While some may raise concern about the drop, Kostin called the index “an inconsistent predictor of US recessions.” But Kostin noted that, when a recession didn’t occur following the ISM dropping below 50, aerospace and defense stocks outpaced the growth of the S&P 500 in the six months after. The S&P 500 has historically gained 22% in the six months following an ISM contraction that doesn’t lead to a recession. And aerospace/defense stocks do even better, gaining an additional 2.5% during the same period, Goldman found.

The market has a couple of anxious trading days left in the week with a benign Producer Price Index (PPI) reading due out Wednesday. The rest of the week, however, will be presaged with a bit of nervousness as Thursday investors will anticipate the ECB rate cut announcement and reaction to Mario Draghi’s Q&A session. Friday, investors will also be anticipating the strength or weakness of the U.S. consumer, as determined by the August retail sales and Consumer Sentiment data.

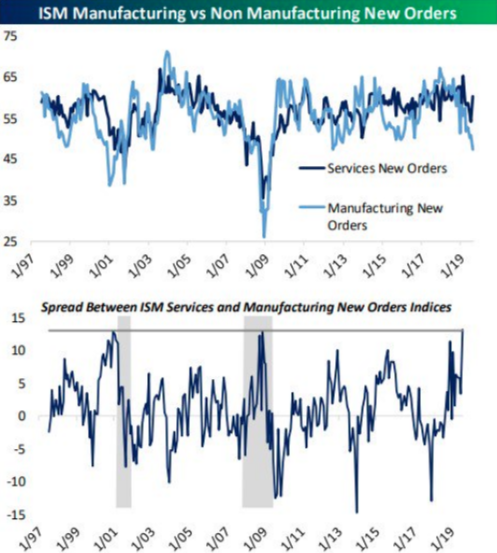

The U.S. consumer has held up the economy rather well in 2019, while the manufacturing sector moving into contraction territory. The divergence between the service sector and manufacturing sector has been much more prevalent in 2019.

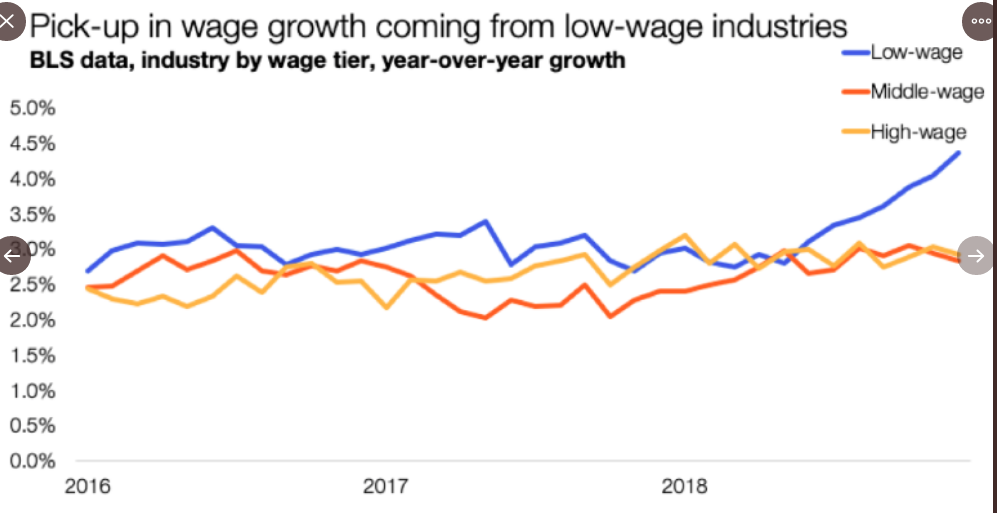

Jobs growth has slowed YoY, but the unemployment rate has held at record low levels and wages are rising at 3.2% annually. What’s more, in recent months the fasting growing wage demographic is finally coming from the lower pay wage demographic.

Consumer confidence remains near record highs and consumer spending has remained strong throughout 2019. But with manufacturing now in contraction territory, investors will pay more attention to the consumer and retail consumption to ensure the broader economy doesn’t move to below trend-growth GDP.

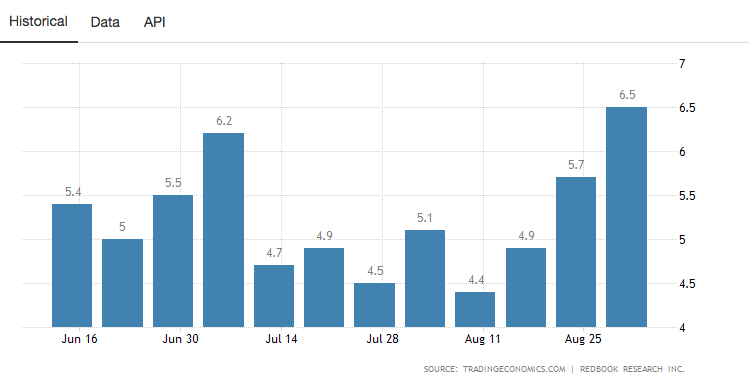

It’s a mixed bag of expectations ahead of the August monthly retail sales report. Some early reads suggest a slowdown MoM, but still growth on a YoY basis. Johnson’s Redbook retail sales showed strong momentum through the back-to-school shopping season, which carried forward into September.

Redbook Index in the United States increased by 6.40 percent in the week ending September 7 of 2019 over the same week in the previous year. Redbook Index in the United States averaged 2.60 percent from 2005 until 2019, reaching an all time high of 9.30 percent in December of 2018 and a record low of -5.80 percent in July of 2009. Redbook isn’t always a good read on what the Census Bureau tracks for monthly retail sales.

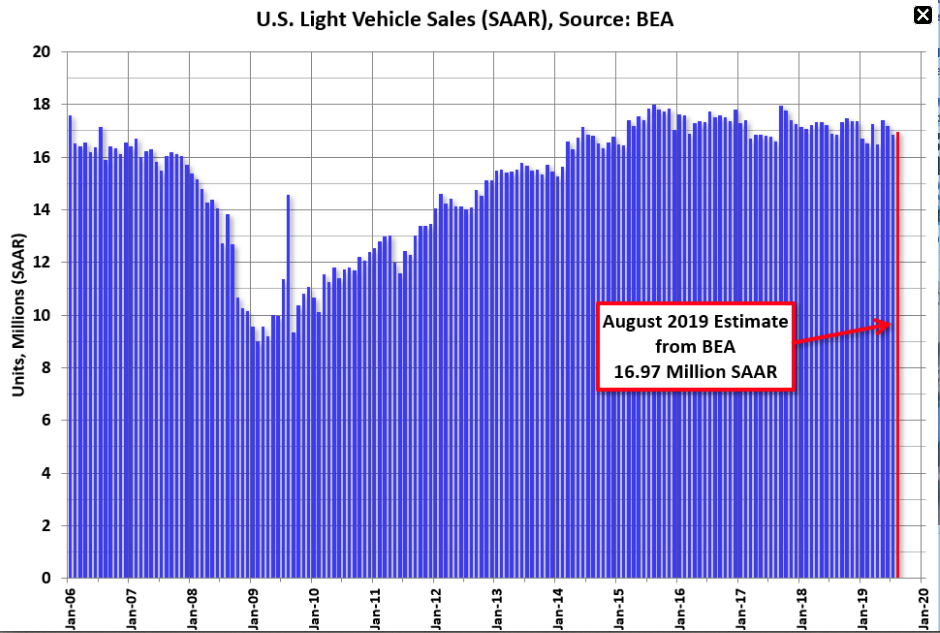

Additionally, light vehicle car sales continue to show strength as reported just last week.

The BEA estimated sales of 16.97 million SAAR in August 2019 (Seasonally Adjusted Annual Rate), up 0.7% from the July sales rate, and up 0.7% from August 2018. But while light vehicle sales were higher for the month of August, gasoline prices were down sharply through August, which will likely weigh on total August retail sales. At present, economists polled by MarketWatch forecast a modest .1% MoM increase in retail sales for August.

Speaking of the price of gasoline, the Organization of the Petroleum Exporting Countries (OPEC) in its monthly report, lowered its forecast of world oil demand in 2019 to growth of 1.02 million barrels a day, citing weaker-than-expected data in the first half from various global demand centers and slower economic growth projections for the remainder of the year. It also lowered its 2020 world oil demand view, seeing growth of 1.08 million barrels a day. OPEC also increased its assessment of non-OPEC oil supply growth, to 1.99 million barrels, mostly on the U.S. but also Brazil, China, the U.K., Australia and Canada.

Reverting back to our considerations for Friday’s monthly retail sales data, Morgan Stanley is of the opinion that a disappointment is in store for investors. Coming off a rather strong July retail sales print, the firm believes some one-off issues were pulled forward from August, namely Amazon Prime Day, and that will play poorly in the upcoming retail sales report.

We’d be remised if we didn’t recognize that many if not all of Morgan Stanley’s bearish sentiment has failed to materialize in the equity markets for 2019, thus far. As such, investors might consider when one of the Morgan Stanley bearish thesis may come to fruition. With this in mind, even Morgan Stanley’s own analysts are beginning to doubt their 2019 thesis for the markets.

Andrew Sheets, chief cross-asset strategist at Morgan Stanley, who says the global economy may be poised for an upside surprise and investors aren’t ready for it. In a note to clients that published over the weekend, Sheets explores the possibility that his bank’s “below-consensus” view on global growth could be wrong, and better days may be ahead if trade tensions thaw further, China offers more stimulus and global manufacturing woes start to bottom out.

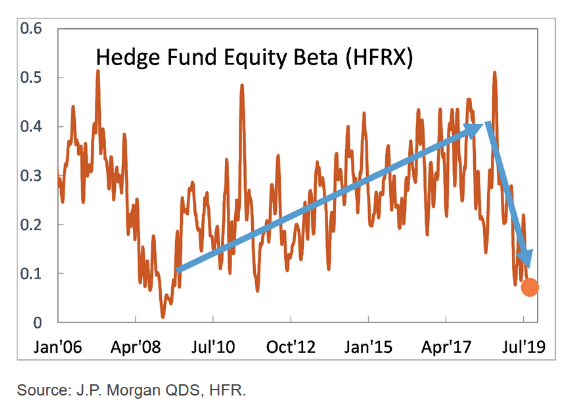

Market and economic growth expectations are more uncertain than they have been in recent memory. This is likely the reason we see consistent equity market outflows and bond inflows while hedge fund equity exposure remains very low/light. (See char and notes from JPM)

- positioning of equity investors is near historical lows

- global hedge funds’ equity beta is in its 2nd percentile

- equity long-short hedge funds in its 1st percentile

- The exposure of systematic investors is also low, with CTAs’ equity beta in its ~20nd percentile

- volatility targeting exposure in its ~25th percentile.

- dealers’ index option convexity is now long (further suppressing realized volatility).

- We expect strong buyback activity over the next ~3 weeks (before the Q3 blackout).

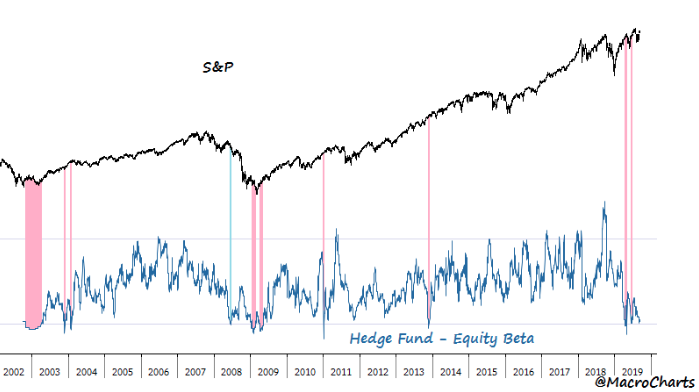

Barely any buying response all year even as stocks continued to march higher. Looking back in history, in most cases fund managers eventually had to chase. (See chart below from like low-level positioning, pink)

The weekly expected move for the S&P 500 this week is just $38 and we’ve gone basically nowhere during this period of sector rotation that has not a definitive life expectancy. If contemplating capital allocation for the long-term, the near-term gyrations are of little relevance. Having said that, some pretty strong fundamental performers have become quite cheap of late. If the only thing that has changed is the share price, a greater bargain today than in past weeks and months… well “alrighty” then! It may be an opportunity is at-hand. Don’t temp us with a better valuation!