In Finom Group’s weekly Research Report, our summation was that the bull market should carry forward, absent any exogenous shocks to the economy and or market. Here is what we offered to our Premium Members this weekend:

“One can certainly suggest that we should have expected more good things from the market this past trading week and after both the S&P 500 Cumulative A/D line and the NYSE A/D line broke out to record highs. Having said that, in order to take advantage of the confirming move during the trading week, cash would have come in handy. And that was what August was really about for active portfolio managers and traders, raising cash for when the market internals/indicators offered a more bullish perspective.”

“Presently, those market internals/indicators suggest…drumroll… the S&P 500 should trend higher in the coming week. As shown below, the S&P 500 Breadth Momentum Oscillator has turned sharply higher after bouncing off of support for the 2nd time this year alone.“

The market internals and technicals have proven too strong to deny, but have also found an additional benefit from sentimental concessions regarding the protracted trade feud between the U.S. and China. While China’s recent announcement to exempt certain U.S. imports from tariffs scheduled to go into place in October, Wednesday night the U.S. also lent a conciliatory measure to the negotiations. Markets in Asia rose on U.S. President Donald Trump’s tweet that he will delay increasing tariffs on $250 billion of Chinese goods from Oct. 1 to Oct. 15 as “a gesture of good will.”

It was back in early August that the trade feud seemed to be “heading off the rails” when more tariffs were announced. Things were escalating fast between the two regions and equity markets were roiled. But this was likely necessary before the situation was to improve. You’ve probably heard the colloquialism, “It has to get worse before it gets better”. This was the theory I had when offering the following tweet on August 5th.

While there does seem to be a more amicable negotiation taking place between China and the U.S., we wouldn’t necessarily take it for granted or at face value. The White House Administration is known for its surprise announcements.

Equities finished nicely higher across the board on Wednesday, with the Russell 2000 (RUT) once again leading the way. As discussed on Tuesday, sector rotation is driving the majority of market activity. One of the biggest movers over the last 4 trading days and since the onset of September trading has been the XRT and the IWM sector and index ETFs. The rally in both of these ETFs has been confounding to many investors and will not last, but shows how value has come back into fashion and may continue, but to a lesser degree as growth will once again come into vogue soon enough.

In speaking of the value trade, J.P. Morgan’s chief quant strategist Marko Kolanovic suggests the value trade can last for some time and benefit the entire market. Kolanovic says investors have become entirely too pessimistic with regards to equities due to the trade war. He believes value will benefit from short covering primarily, should there be some positives that come out of the October U.S./Chine meetings in Washington D.C. Kolanovic highlights that equity exposure and sentiment are at levels comparable to 2008.

“Most of the S&P 500 gains came from defensive sectors, stocks that investors tend to buy as a proxy for long duration bonds, and so-called ‘secular growth’ technology stocks. These stocks, incorrectly in our view, are deemed to be impermeable to economic woes. As institutional and individual investors pulled money out of the US market, US corporates continued buying their own shares, supporting large cap stock prices. Even with the support of buybacks and historically low bond yields, the market is nearly flat from January 2018. This performance ranks poorly, i.e., below the 20th percentile, over the past 30 years. The picture is obviously much bleaker when looking at decimated cyclical segments such as manufacturing, oil and gas, steel, agriculture, and SMid cap companies, which are most negatively impacted by the current administration’s policies.

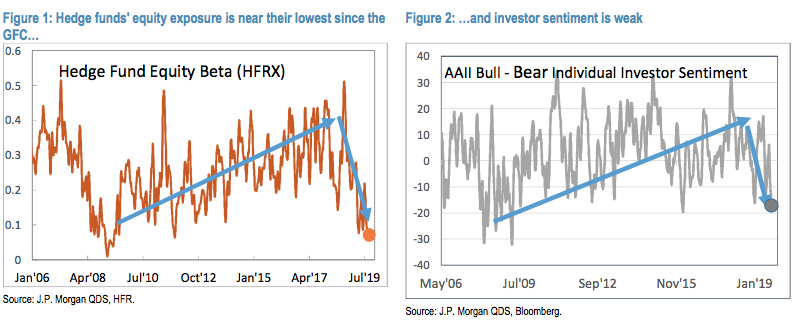

Market and Volatility Commentary: Near-term outlook, How long will Value/Low Vol rotation last, SMid commodity equities. As we discussed above, positioning of equity investors is near historical lows. Specifically, global hedge funds’ equity beta is in its 2nd percentile, and equity long- short hedge funds in its 1st percentile. The exposure of systematic investors is also low, with CTAs’ equity beta in its ~20nd percentile, and volatility targeting exposure in its ~25th percentile. Volatility has started declining from the August spike and dealers’ index option convexity is now long (further suppressing realized volatility). We expect equity inflows on account of declining volatility, and strong buyback activity over the next ~3 weeks (before the Q3 blackout).

We first note that while net equity positioning is near lows, gross exposure of hedge funds is very high (for instance, PM’s Prime Brokerage portfolio shows gross leverage in its 99th percentile since Jan’18). Given record high gross and near record low net exposure, the most likely way to increase exposure is by closing shorts. This is the type of move that we saw yesterday and we think it has a lot of room to continue. Closing shorts would push value, cyclicals, high volatility, and small caps to outperform the broad index. Momentum and defensives would lag. In fact, we think that yesterday’s move was only started by discretionary PMs, and will continue with equity quants (that typically operate at lower frequency, e.g. month-end) and fundamental investors.

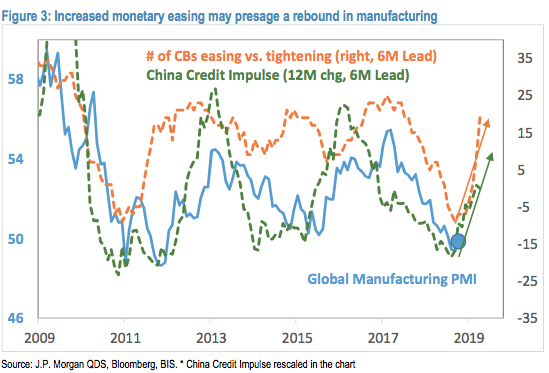

Can we see a more sustained value and broader market rally beyond the October trade talks? We think that is quite possible given the recent increase of monetary and fiscal stimulus globally that typically acts with a delay. Figure 3 above shows central bank easing as well as China credit impulse and global manufacturing PMI. While manufacturing lags both, we see that in the coming months one could expect manufacturing activity to pick up given the increased monetary stimulus, providing support for the market and value stocks. We think October negotiations will be the key for future performance of equity markets and more broadly the global economy. However, there is reason for being cautiously optimistic about progress being made on these negotiations. Recent voter polls indicate that 65% of US voters would blame US administration trade policies and Trump directly for market volatility, and 57% would blame Trump if the US were to enter recession. These results were confirmed with another poll yesterday indicating similar results. A recession going into election would be politically devastating, and with the time window to the election closing, it would be reasonable to expect some progress on trade. This could give enough time for monetary and fiscal measures to turn around economic activity (e.g., as indicated by Figure 3).”

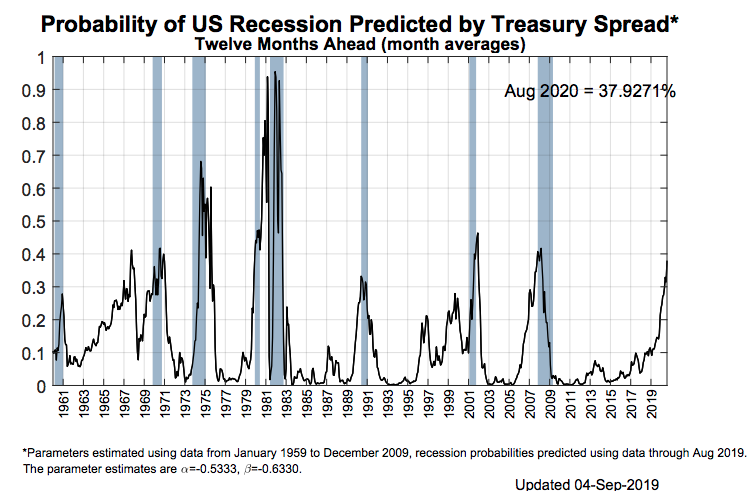

The trade feud between the U.S. and China has been found to deteriorate not only global growth, but risk appetite, which is highlighted within the J.P. Morgan notes above. The pervasiveness of the trade feud has led to recessionary fears, which have grown throughout 2019 and as recently updated by the New York Federal Reserve Bank recently.

Even with all the uncertainty over the economy and thrown about in the equity markets, Credit Suisse’s recession index hasn’t budged much at all.

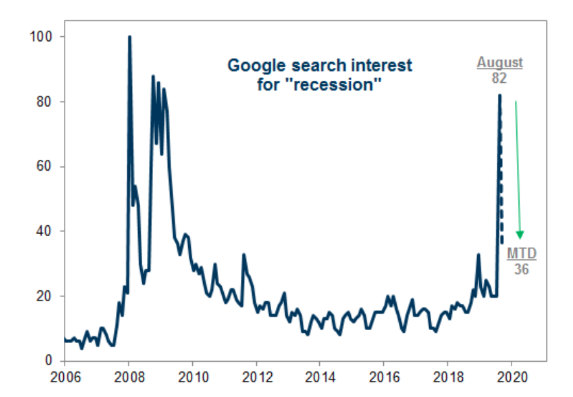

Another sign of good news is that searches for the term recession have declined recently. Goldman Sachs found that it had escalated to levels not seen since the Great Financial Crisis of 2008, but has since relaxed in the month of September.

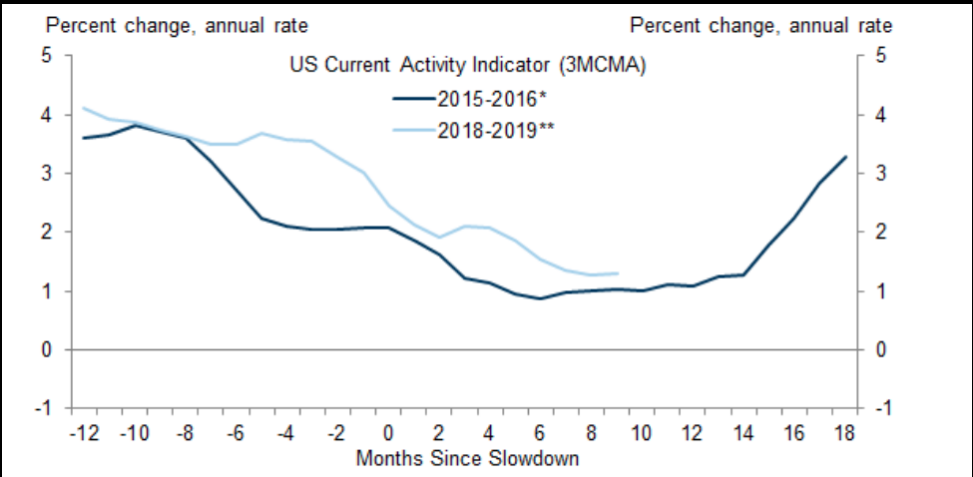

The current economic period, whereby global PMIs have contracted and China’s economy is feared to be slowing more than expected reminds many investors of the 2015-2016 period. It was during this period last that the U.S. economy did indeed slow and expressed a corporate earnings recession. While an earnings recession has not happened to date, based on GAAP measures at least, the analogue still looms large amongst the investor community. Goldman Sachs recent analysis indicates as such and is noted in the following chart:

The path forward for the global economy and risk trade remains aligned with the trade feud. At present, investors are simply positioning for where they see the trade feud going. And with regards to the sector rotation and value trade, here is what Morgan Stanley has to offer so far as the catalyst for the momo-trade unwind and sector rotation:

- There was no single hard catalyst – the proximate causes were modest improvements in macro data (ADP, ISM Non-Manufacturing, Citi Economic Surprise Index > 0), optimism over October US-China talks, and an increase in interest rates (10-year up 10bps from last Tuesday through last Friday’s close, and another 18 bps since then).

- But it was really heightened risk aversion that caused the moves – investors were becoming increasingly nervous about P/L after underperformance from crowded areas like Growth Software in August and the underperformance of shorts in the week following Labor Day. A lot of investors trying to protect P/L and de-risk at the same time led to gaps that then accelerated and fed on themselves.

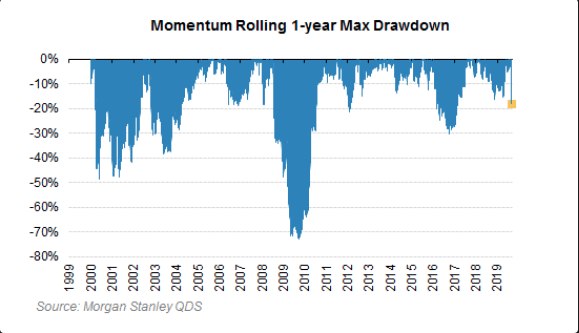

- This selloff has lasted only 26% of the typical duration of a selloff, but has already moved 75% of the way to the median in terms of price. Keep in mind that there is a fat left tail though, and momentum declines can be much worse than the median (historical max drawdowns larger than -30%).

- If contained to a positioning unwind the pressure should abate in a week or two.

- But to be clear the risks skew towards more derisking relative to historical unwinds, not less. The level of crowding remains high, portfolios are fragile right now, and should there be a fundamental shock this unwind could persist for multiple months.

In the face of a protracted trade war, with escalated tariff implementation in 2019, the equity markets have remained quite resilient. Earnings are growing, albeit extremely modestly and it is likely that FW12M earnings estimates will be revised lower in the coming months. But should a trade truce of sorts that is found for exercisability, the markets may find a good deal of multiple expansion and as sentiment improves.

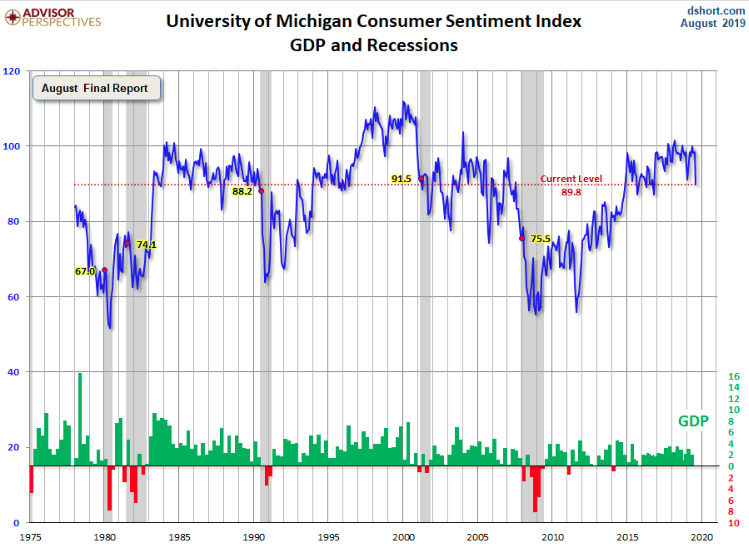

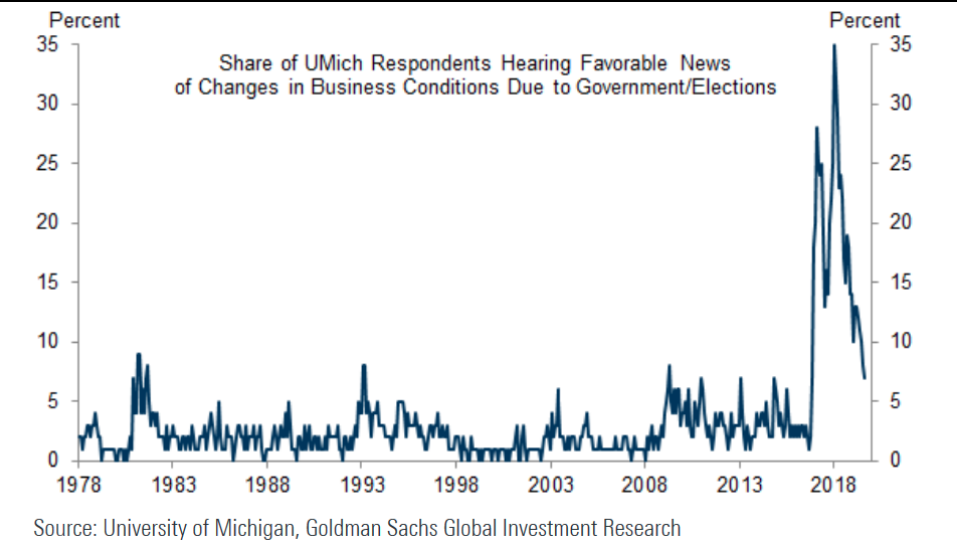

The U.S. economy has also been resilient through the trade feud, but that has been called into question more recently with the latest University of Michigan Consumer Sentiment reading. The Consumer Sentiment Index posted its largest monthly decline in August 2019 (-8.6 points) since December 2012 (-9.8 points). The 2012 plunge reflected widespread fears of being pushed off the “fiscal cliff” due to rising taxes and falling government spending. The recent decline is due to negative references to tariffs, which were spontaneously mentioned by one-in-three consumers. Unlike concerns about the fiscal cliff, which were promptly resolved, Trump’s tariff policies have been subject to repeated reversals amid threats of higher future tariffs.

With consumer sentiment faltering over trade issues, investors and consumers will pay increasing attention to the trade headlines and the data when it is released on Friday, alongside the monthly retail sales data. Consumer spending is some 70% of the U.S. economy, as they go the economy seemingly follows. With all the headlines considering the probability of a recession and when it would take place, consumers have been found lacking for favorable headlines on business conditions.

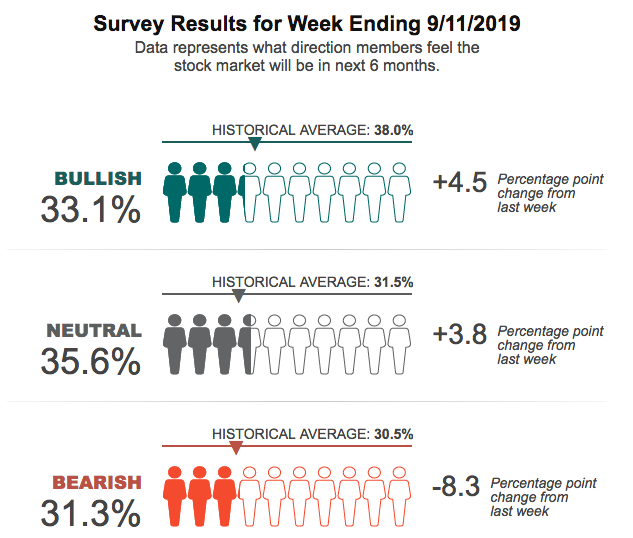

As noted earlier, investor sentiment is not too far behind that of the consumer, but has been found for bearish sentiment for an extended period of time. The recent AAII survey indicates a slight improvement over the prior reporting period, but the bullish sentiment remains below the historical average as the two-week long rally in the S&P 500 has found improving confidence.

For the remainder of the week, it would prove difficult to forecast the equity market’s performance, that will lean on central bank commentary and rate cut announcements from the European Central Bank on Thursday.

“We still think that Mr Draghi will muster a sufficient majority in the Governing Council to push through a package that will include rate cuts as well as a restart of the asset purchase program,” Dirk Schumacher, an ECB watcher with Natixis, said in a note to clients.

The meeting comes as some ECB hawks in recent weeks have been trying to downplay the chances of a huge stimulus package.

“There is, judging from (the) latest comments coming out of the Governing Council, no clear consensus within the Governing Council regarding the size and scope of potential easing measures.”

“Potential surprises could include an expansion of the QE (quantitative easing)-eligible universe to new asset classes (senior bank debt or equities), or more radical changes to QE parameters (removing capital keys),” said Frederik Ducrozet, who watches the ECB at Pictet in Geneva.

In detail the ECB is expected to do the following:

- Cut its deposit rate.

- Re-launch monthly net asset purchases.

- Strengthen its forward guidance by extending the horizon to keep rates at present or lower levels beyond the first half of 2020.

- Introduce a tiering system for bank deposits.

- Raise the self-imposed issuer limit for purchases of government bonds from 33% to 40%, or even 50%.

If that is what we get, it will probably be the most comprehensive package ever by the ECB and a sign that the central bank has changed under the new Chief Economist Philip Lane.

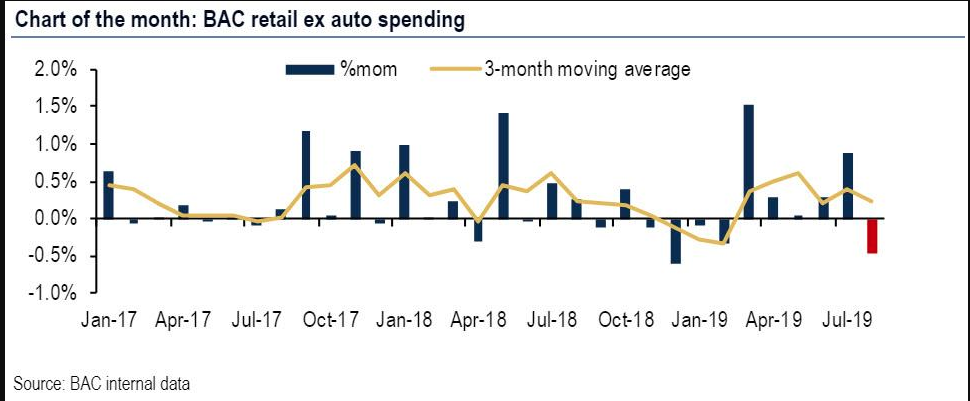

Thursday’s market activity is very likely to be determined by what the ECB announces and forecasts for the Euro zone economy. But Friday’s U.S. market action will likely be a reaction to the monthly retail sales data. Some are already out in force, suggesting a sharp reversal in retail sales from a strong report in July. Bank of America credit and debit card data, which shows that after a strong month of spending in July, consumers aggressively tightened the strings of their wallets in August.

Specifically, BAC found that retail sales ex-autos fell 0.5% month-over-month, which reversed the 0.9% gain in July, and was not only the first monthly contraction since February this year, but was also the biggest monthly drop in 2019.

- Based on the aggregated BAC credit and debit card data, retail sales ex-autos fell 0.5% month-over-month (mom) seasonally adjusted (sa). This reversed the 0.9% mom gain in July. As always, there were a number of “special factors” which we decipher in this note.

- Amazon Prime Day and other retailers’ summer promotions in mid-July provided a significant boost to spending, as we showed last month. In our view, these promotions effectively pulled forward demand into July and out of August.

- Outside of the promotion distortions, we also think spending was dampened by weakening sentiment.

- According to BofA, Amazon Prime Day and other retailers’ summer promotions in mid-July provided a significant boost to spending, in effect pulling forward consumer demand from the future, into July and out of August. Focusing specifically on discretionary spending categories likely impacted by the promotions, the bank’s economists found that it increased 1.7% mom in July but tumbled 1.4% in August.

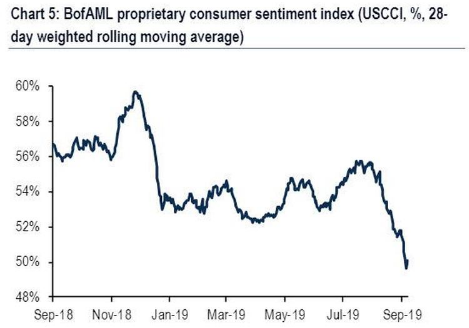

- Also, BofA’s own proprietary “Word from Main Street” index showed that the BofAML US consumer confidence indicator (USCCI) dropped in recent weeks, tumbling to the lowest level in years. It briefly dipped below the 50% breakeven level before rebounding, signifying that respondents, on balance, are more pessimistic. BofA suspects that the drop in sentiment left consumers a bit more hesitant to spend this month.

This wouldn’t be the first time BofAML credit card and sentiment data has painted a negative light on their retail sales forecast. The firm called for a decline in April retail sales, which on first reporting was accurate, but with monthly revisions was not. April retail sales were revised from a negative .2% print to positive in the following monthly data release. The BofAML data is skewed due to credit card profile tracking. Nonetheless, the size of the reversal forecasted is notable and also identified in current economists’ expectations. Most economists only expect a modest .1% growth in August retail sales, largely due to the Amazon Prime affect and lower MoM gasoline prices. If the major issue in the report is in fact gasoline price related, investors are likely to look beyond a weak report. Additionally, a weak report may also be found favorable for investors cementing rate cut expectations by the FOMC next week.