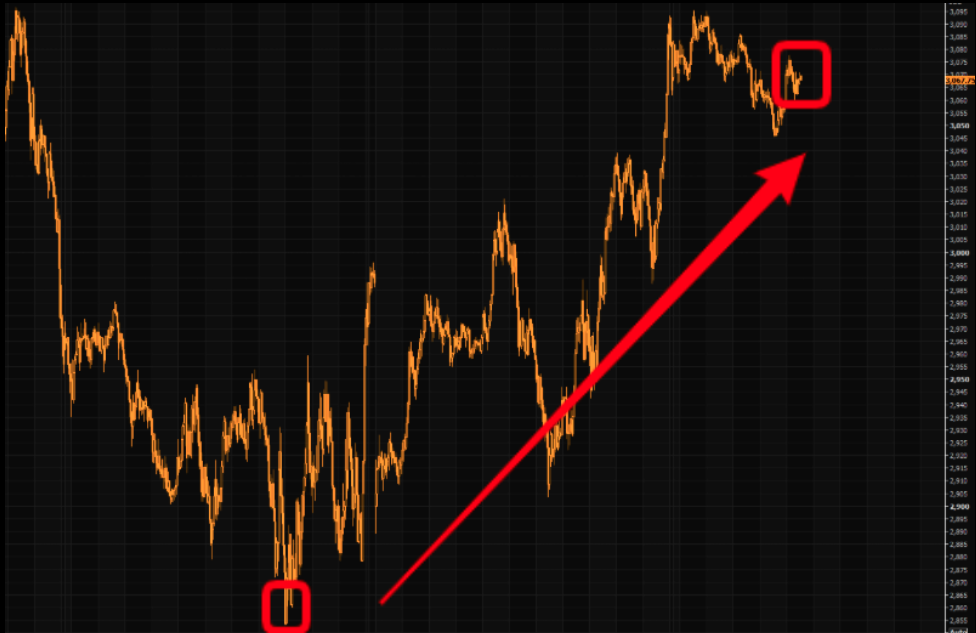

It’s never advisable to short the market when it’s known that central banks are likely to respond to perceived exogenous economic shocks. Friday’s S&P 500 lows are a perfect example of such inadvisable action, with the low of the trading session and seemingly trough in recent correction at 2,855 and a close roughly 100 points higher. Additionally, that Friday closing price was only found with increased buying activity on Monday. The S&P 500 chart below is also an example of why the average trader, absent guided professional coaching, shouldn’t trade index futures.

I couldn’t propose with any great certainty that the corrective phase in the market has been completed, but I can suggest that Monday’s close back above the 200-DMA is a positive sign for the continuation of the bull market in 2020. It seemed inconceivable that the S&P 500, having closed nearly 90 points below the 200-DMA last Friday would recapture the key moving average in just a single trading session, but that is what took place, with Monday’s high volume and strong market breadth.

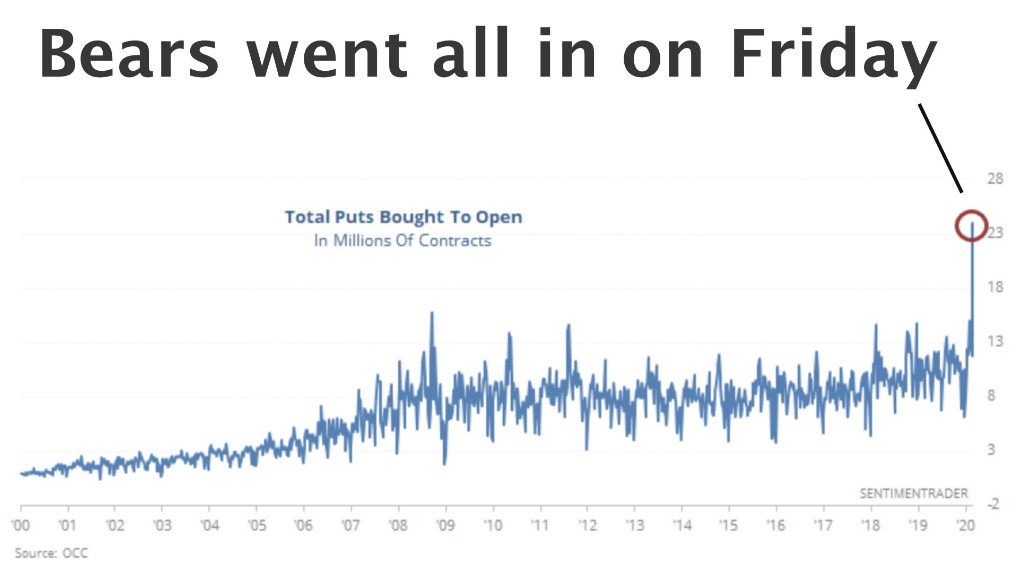

A goodly amount of technical and sentimental damage has taken place in the market over the last 8 trading sessions, with the S&P 500 slicing through it’s major moving averages. Some of the repair work is now being expressed, but remains sensitive to media headlines and overall sentiment. Possibly the most unfortunate aspect of the recent market correction of roughly 16% peak-to-trough, is the “retail chase”. As shown in the SentimenTrader chart depicted below, that is exactly what happened as headlines assumed the worst from COVID-19.

I’ll refer to my opening statement and add that it is always a better practice to buy the dip (improved valuations or risk/reward) than it is to short the market. With the S&P 500 up more than 4.5% on Monday, it caught a lot of folks by surprise, but not our members, as we largely understood a reflexive rebound rally was afoot. Before we get to some of what we outlined in our weekend Research Report for Contributor, Premium and MasterMind Options members, we wanted to see what might come next and after such a strong rebound in a single trading session.

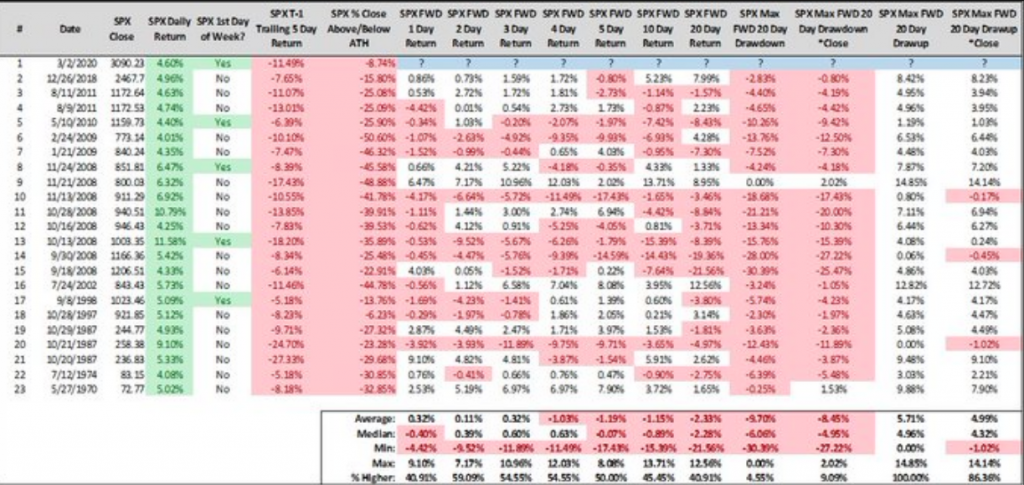

Here are all trading days where the S&P 500 gained 4% or more after having declined -5% or worse the prior 5 trading sessions. (Steve Deppe)

The study above looks forward 20 trading days and suggests that the reflexive rally we just witnessed as an incredibly strong probability of being unwound with additional losses to come. Hence, a lot of red on the screen folks. And now, let’s take a look at some of Finom Group’s notes within our weekend Research Report which indicated a bounce was afoot, for which we also offered trade alerts that might take advantage of such a bounce.

“The S&P 500 Bullish Percent was down ANOTHER 13.5% on Friday. The bad news is that we can all clearly see the strength in this bearish move this past week, right? The good news is a breadth thrust like this one also suggests sellers’ exhaustion, oversold conditions that may prove ripe for a near-term bounce. A tangential defining characteristic we can extrapolate from this chart is that liquidity is just awful in the market. If it weren’t, such a move would be terribly difficult to exact in a week let alone a single trading day. But let me define the liquidity issue as I have for Goldman Sachs’ (I consult for GS London since 2017) derivative team this past week and with the following chart and analysis.”

“S&P futures top-of-book depth stands at ~$8mm currently vs. ~$21mm as of Wednesday’s close this past week, but has worsened to ~24.6mm at week’s end. Relevance? Weakening liquidity can make incremental trades move markets more, pushing up volatility further. This move lower in liquidity will likely exacerbate any talks of “short gamma” in the market as well, as worse liquidity tends to increase the cost of liquidity (market impact of a given trade) and propel/trampoline price action. Overall, this has the potential to produce higher Volatility of Volatility (VVIX). And that is exactly what was produced by week’s end. Even though the VIX itself finished Friday near, if not at, the lows of the trading session, VVIX did not see the same kind of decline into the closing bell. Sorry if this sounds condescending as that is not the intent, but, please stop right here, review all that I’ve laid before you thus far and review it once more before we all move forward together and with the following bullet points:

First Summary

- Market sentiment and breadth have demonstrated a bearish breadth thrust.

- A bounce may come near-term, but is best used for the purpose of rebalancing and/or hedging. Heavy cash position already? One can nibble for small exposures and with a long-term outlook.

- You are not rowing this boat alone and most market participants have taken a drawdown to-date.

- Liquidity is poor and produces outsized market moves.

- Time is your friend, but it is best to build the amount of time one can capture in order to benefit from it.

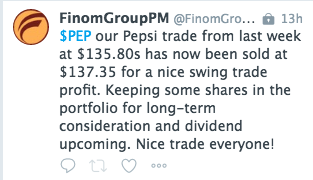

While we offered many more charts and analysis that identified a probable market bounce near-term, positioning ahead of the bounce proved prudent as we offered long trades on both TJX and PEP shares last week and profited from there strong moves on Monday.

It’s increasingly clear that COVID-19 is eliciting a growing response from central banks and governments. Responses to the spreading virus have already been initiated by governments in Europe, China, South Korea, Malaysia and Australia’s Reserve Bank overnight. The 25 bps cut may prove minuscule when compared to what investors are promoting the FOMC commits to in the coming weeks.

President Donald Trump once again called on the Federal Reserve to deliver some major policy easing measures, after the Australian central bank cut rates to record lows and noted the impact of the coronavirus outbreak. Within hours of the RBA cut initiated, the U.S. president responded on Twitter, saying the U.S. central bank’s chairman had “called it wrong from day one.”

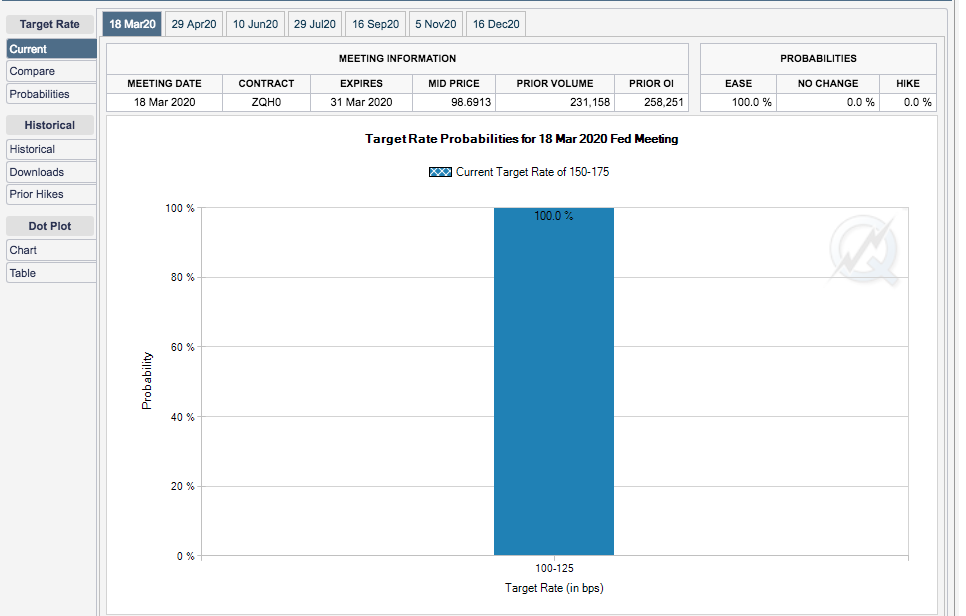

Presently, there is no probability that exists whereby the FOMC won’t cut rates. This statement is congruent with Fed Fund Futures which are not just baking in a 25 bps rate cut, but a 50 bps rate cut by the March 18, 2020 FOMC meeting. Historically, when Fed Fund Futures have a 60% probability for any action or pause, it has always been accurate, never found in error for predicting Fed action or inaction as the probability would outline.

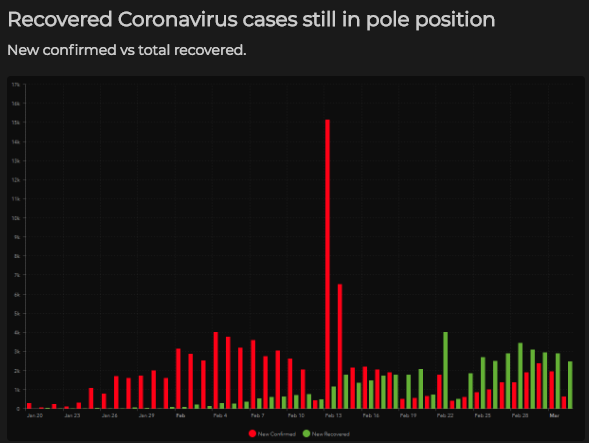

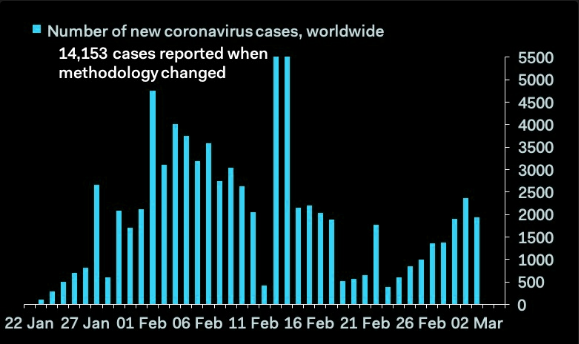

In reflecting on the “crisis” of the day, the Coronavirus, it is important to recognize that fear of the crisis and how it is being handled amongst regional governments is driving the economic and market sentiment, not the virus itself. The virus remains with a low mortality rate and a very high recovery rate. As shown in the chart below, the recovery rate continues to outpace the number of daily new cases as well.

The COVID-19 data is updated daily. Monday proved the first day whereby the number of new cases was also on the decline since the methodology for reporting changed. I’m of the belief that China has largely contained the outbreak and is in the recovery stage, post the initial spread and economic fallout from the virus.

Here is what Investco’s Kristina Hooper had to say about the potential recovery afoot in China and what has to happen in the near future.

“The situation in China in terms of contagion already appears to be improving, as new infection data is being driven by cases outside of China. Having said that, economic data is poor — especially the February Purchasing Managers’ Indexes (PMIs) just released this past weekend. China’s official manufacturing PMI dropped to 35.7 — from 50.0 in January — while the services PMI dropped to 29.6 from 54.1 in January.1 However, that is to be expected given the extreme measures taken by the Chinese government to lock down travel and commerce in order to stem the tide of infection.

I suspect the data for February will represent the bottom, and that March data will indicate improvement. If this is the case, it suggests the greatest impact on Chinese economic growth will be felt in the first quarter of 2020. In China, we expect a V-shaped economic recovery, with a sharp rebound quickly following the first-quarter fall.“

Hooper doesn’t just suggest that China is likely to have a V-shaped recovery, but the U.S. is likely to follow suit.

“At this juncture, here is what we anticipate in terms of the impact and the policy response:

- We believe it is more likely that the US experiences a V-shaped recovery given favorable economic conditions in the country.

- We do not currently expect the coronavirus to have a substantial impact on the global economy beyond 2020. While we are unsure of the timeline of this contagion, we believe it will be relatively short-term in nature.

- In terms of earnings, we of course expect an earnings recovery in Chinese equities first. It should take longer for an earnings recovery for other major stock markets given where they are in the contagion cycle.

- China has continued to provide significant stimulus, both monetary and fiscal, to help support its economy, and we expect most other major economies to provide an adequate policy response.

- However, developed countries will likely focus on monetary policy rather than fiscal stimulus. Federal Reserve (Fed) Chair Jay Powell issued a statement of reassurance on Friday: “The fundamentals of the US economy remain strong. However, the coronavirus poses evolving risks to economic activity. The Federal Reserve is closely monitoring developments and their implications for the economic outlook.” This indicates the Fed stands ready to act and provide monetary accommodation if needed.

- A specific risk is that a rise in infections will lead to people hunkering down more, resulting in cash flow issues for select companies, resulting in wider credit spreads. Policymakers may need to respond to provide emergency liquidity.

While we’ve witnessed panic among many other firms, Finom Group has remained “cautiously optimistic”. In fact, this is our advised outlook for members of Finom Group as we don’t subscribe to some of the massive revised outlooks from many institutions. One of the reasons is that when we pull together all of the data, anticipated central bank response to the current impact from the coronavirus and add our analytics, financial conditions thus far remain exceedingly easy compared to the starts of each of the past three recessions, as illustrated in the chart below. The picture does not seem to be suggesting that a recession is in the offing.

The Goldman Sachs Financial Conditions Index does not suggest that a recession is imminent

The base from which the economy is positioned going into the peak affects of coronavirus has been showing steady, fundamental macro-growth that had also been improving. On Monday, the latest economic data proved a mixed bag, but the affects on the data from the coronavirus were already presumed to play out in the data.

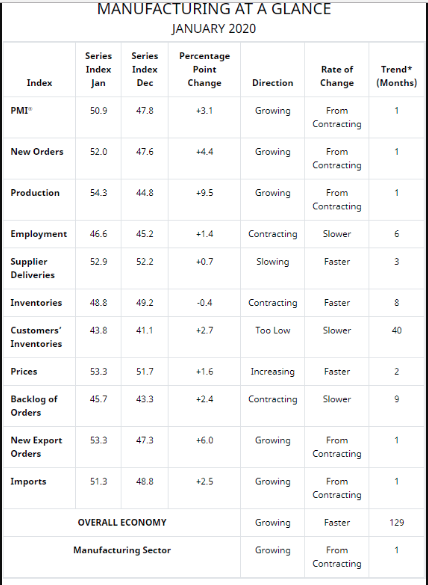

The Institute for Supply Management said its manufacturing index dipped to 50.1% last month from 50.9%. Economists had forecast the index to total 50.5 percent for the latest period tracked. Damage reports from the coronavirus are just starting to come in and the situation could get a lot worse before it gets better. Plant shutdowns and other disruptions in China are starting to jam global supply lines while travel has been sharply curtailed.

“Manufacturing production and order book trends deteriorated markedly in February as producers struggled against the double headwinds of falling export sales and supply chain delays, both in turn often linked to the coronavirus outbreak,” said Chris Williamson, chief business economist at IHS Markit, another forecasting firm who manufacturing index has gotten considerably weaker.

As I’ve mentioned in the past, the data for manufacturing weakness was largely to be expected and may continue into the month of March, depending on how quickly the coronavirus peaks in the U.S. and how quickly China’s commerce and manufacturing hubs fully engage once again. Below is a table of the subcomponents of the ISM Manufacturing index which are taking a direct hit from the manufacturing curtailment in China as well as the export capacity to the region.

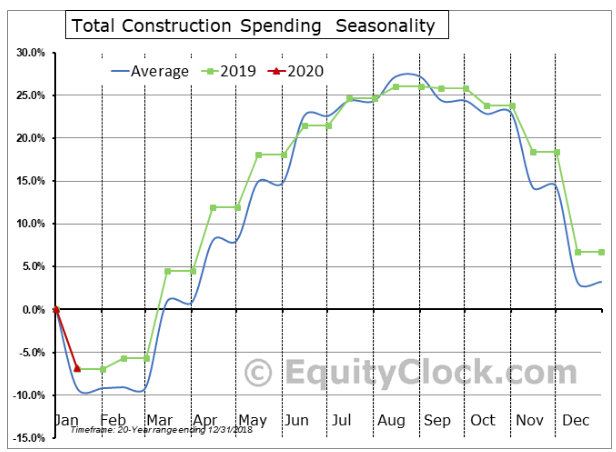

In other data, U.S. construction spending remains on-trend and moving in a more positive direction when compared to the slowdown in manufacturing. Spending on U.S. construction projects surged 1.8% in January at a annual rate of $1.37 trillion, the Commerce Department said Monday. Economists polled by MarketWatch had expected growth of 0.9 percent. Residential construction outlays climbed 2% in January, as lower interest rates have given a boost to home sales and home builders.

Warmer weather also helped. Investment in nonresidential projects rose 1.6% and spending on public construction projects rose 2.6%. In December, construction spending was revised up to show a 0.2% increase instead of a 0.2% decline as previously reported.

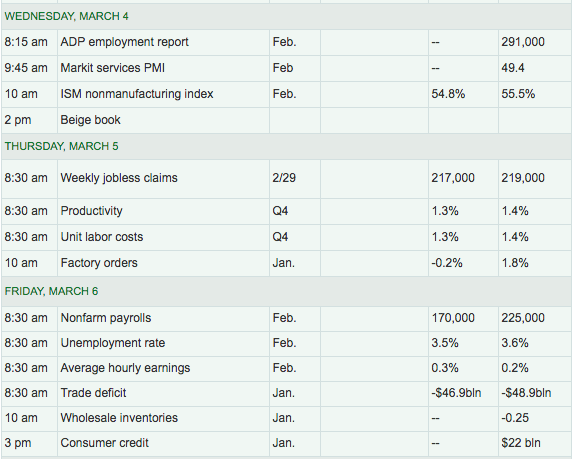

Tuesday’s economic data releases are void, with monthly auto sales and a crude inventory data report due out in the late afternoon. Like most risk assets, crude oil had a nice rebound on Monday, as Treasury prices fell and yields rose slightly on the day. Come Wednesday, investors will be anticipating reports that may also prove to show some negative impacts from the coronavirus spread by way of the ADP private sector payroll report and ISM non-manufacturing data.

The ADP report will, of course lead into Friday’s release of the BLS’ Nonfarm payroll report. Economist surveyed currently anticipate 170,000 jobs were created in the month of February. Revisions from previous months will also be a key focal point in the report come Friday’s release.

While Monday’s bounce back in risk assets seemed to quell investor anxiety and push aside fears and on quite high volume, we encourage investors to look forward.

Planning ahead for all possibilities allows for investors/traders to maintain disciplines and execute a pre-determined game plan. When a game plan demands flexibility, that investor/trader is also more likely to react to such demands with rationale and logic. By the time the COVID-19 issue is said and done, it will likely prove a “blip on the radar” on a long road higher in equity prices. Again, perspective is key and the data suggest COVID-19 is no better than a severe flu season would prove to be. We recently discovered the facts in an article by Dr. Tony Fauci, director of the National Institute of Allergy and Infectious Diseases, in The New England Journal of Medicine on Friday.

The article suggested there is a 1.4% mortality rate connected to the COVID-19. Again, the measures taken by regional governments to combat the outbreak has been the greatest driver of fear than the virus itself. Sometimes, that’s just the way it goes and why I believe a V-shaped economic and market recovery is still the optimal outlook. Don’t get me wrong, I’m not suggesting the bottom in the market is in, in fact that is not what history suggests, but over time we should see higher risk asset prices.

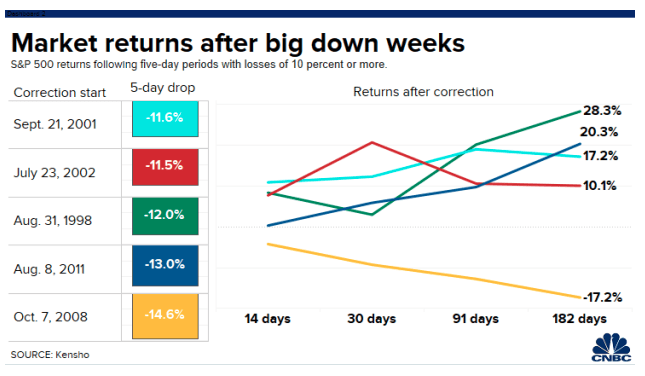

Analysis of prior market declines of 10% or more over five trading days since 1990 shows that equities tend to rebound in the weeks to follow, according to data provided by hedge fund tool Kensho.

In the wake of the 9/11 attacks, the S&P 500 gained 10.9% over two weeks after selling off, according to data provided by Kensho. Those gains ballooned to 12.3% one month after the sell-off and 19% after three months. The Kensho data excludes multiple declines of more than 10% for one month after the initial slide in an effort to isolate separate bouts of market turbulence.

Jefferies also recognized the likelihood of a market rebound after a swift selloff.

“The silver lining to intense sell-offs is that by the time it feels panicky, it’s generally closer to the rebound,” Ward McCarthy, chief financial economist at Jefferies, wrote Saturday.

“While there are many market prognosticators that will tell you why buying a dip might not work, and why every time is different, it is hard to argue with human nature and history.

While we found that the bounces tend to be swift and robust, more importantly, performance tends to be overwhelmingly positive over a [three-month] horizon.”

The market, very simply put, trends higher alongside earnings over time. This is common knowledge and recognized in every major index chat. As such, “buy the dip” is inevitable as a strategy and works every time, with varying degrees of participation and success. Nonetheless, not everyone is as optimistic as Jeffereies assumes to be. Goldman Sachs has gone on record several times, insisting that investors exercise caution and avoid buying the dip until greater certainty surrounding the macro-backdrop and the earnings outlook materializes.

“While ‘buy the dip’ has been a successful strategy since the Global Financial Crisis, with equity drawdowns often reversing quickly, it might be more risky this time,” Christian Mueller-Glissmann, equity strategist at Goldman Sachs, said in a note. “With global growth still weak, the shock from the coronavirus outbreak lingering and less scope for monetary and fiscal easing, the risk of a more prolonged drawdown remains.”

Citi’s chief U.S. equity strategist, Tobias Levkovich, echoed that sentiment, saying he’d like to see even more panic before stepping up.

The earnings growth outlook remains in question and remains the biggest question for valuations and the benchmark S&P 500 going forward. Last week Thursday, Goldman Sachs’ analysts outlined that they believed there would be no earnings growth for fiscal 2020, due in large part from the coronavirus shock. Howard Silverblatt, analyst at S&P Dow Jones Indices, noted that first-quarter profit estimates have declined 5.0% since the end of December, and more declines are expected, as approximately 100 companies have warned.

Based on IBES data from Refinitiv, the 2020 consensus profit forecast from analysts is still well above zero. As of Friday, analysts were expecting earnings growth of 7.6% for 2020, down from an estimate of 9.7% at the start of the year, while for the first quarter, analysts expect a 2.7% gain in earnings versus a year ago, down from 6.3% on Jan. 1, according to Refinitiv’s data.

While first-quarter estimates have further to fall as more companies give negative guidance, zero earnings growth for the full year is unlikely, said Nick Raich, chief executive of The Earnings Scout, an independent research firm, anticipating some rebound in corporate results once the spread of the virus slows and demand picks back up.

It remains to be seen what the actual earnings results for the year prove to be, but I also think it safe to offer the following and as I tweeted out recently:

This demands some additional context. That context was offered to our members in our weekend Research Report and as reiterated in the following:

“I’m sure that my forecast appears more favorable than most Wall Street analysts are modeling. But I desire for readers to consider what I previously mentioned with regards to the 30-year fixed rate mortgage, which is only going to fall further as all yields have fallen dramatically WoW, and with the 10-year Treasury yield at an all-time record low level.“

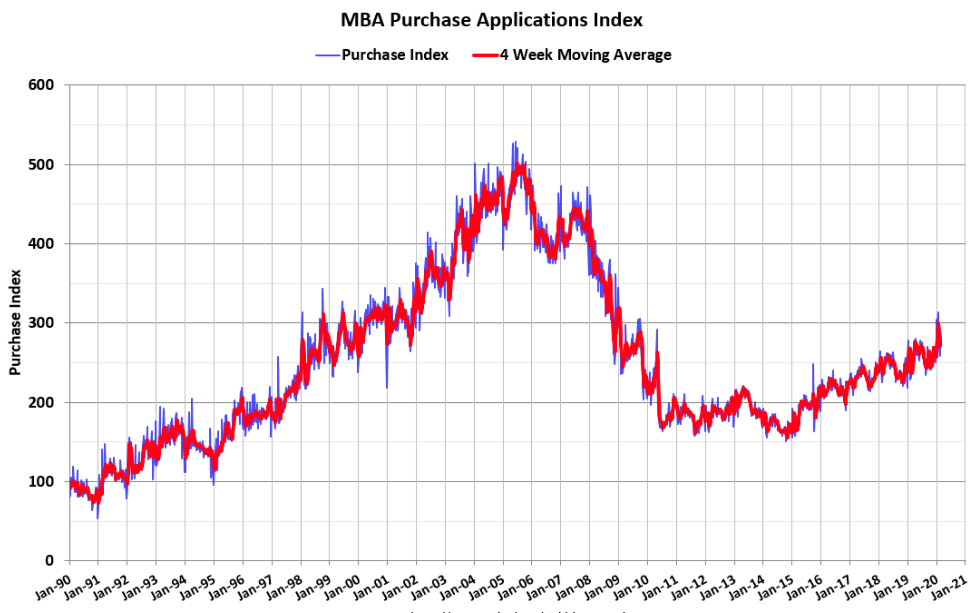

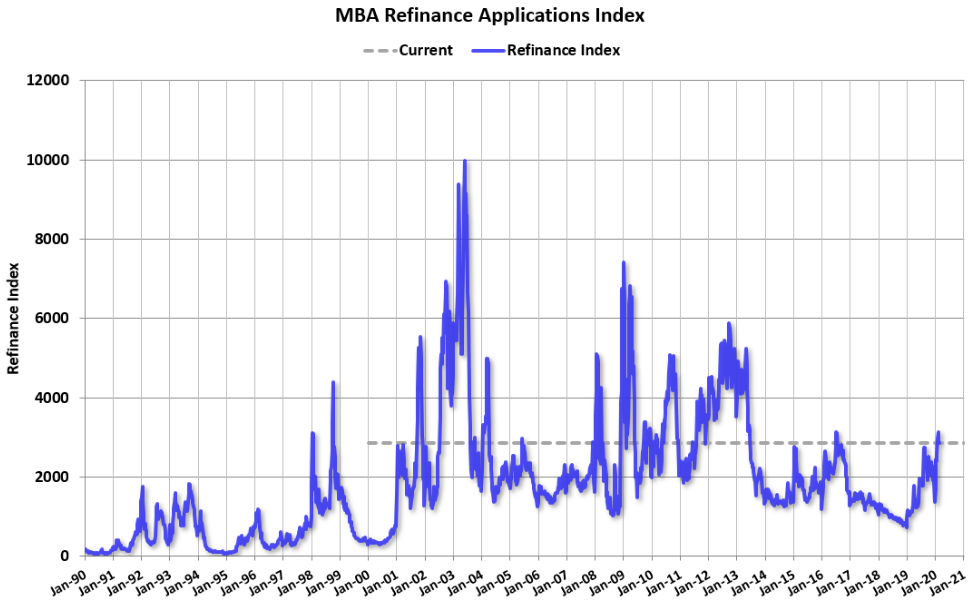

“In reviewing the chart of the 10-year yield (TNX) above, it’s not just that the yield is at all-time lows ahead of any material and/or realized COVID-19 impact on the economy, it’s the massive rate-of-change (ROC). The top chart shows the ROC for the 10-year yield. Not only is this the lowest yield for the 10-year note in history, it’s also the fastest YoY decline in percentage terms. This correlates perfectly with the decline in mortgage rates and rise in mortgage Purchase applications, which are at cyclical highs, as well as rise in Refinance applications since mid-2019. (Charts from Bill McBride)

“It will also likely continue to facilitate refinance activity, providing a safety net of loan demand and loan origination fees for banks as households look at refinancing as a means of boosting monthly disposable income. Recall my former comments on the negative feedback loop of consumers and their exposure to headlines and Google Trend searches? Now juxtapose that with this outlined positive feedback loop to better understand why I am offering a lesser COVID-19 impact on the economy near-term when compared to my contemporaries. I remain, as stated previously, cautiously optimistic and with the offered analytics, rationale and logic. I am always open to being wrong and a more severe outbreak from COVID-19 in the United States can certainly find fault with my outlook.”

Don’t be surprised and under the premise of NO EARNINGS GROWTH and NO RECESSION if the S&P 500 P/E expands to new cycle highs in 2020 folks. Investing is about return on capital over time, the sentiment surrounding accommodative monetary policy and a stable economic outlook. Assuming all three are found beyond the current issues of the day that should prove fleeting, history suggests multiple expansion. As such, my tweet proves relevant and may also be what Tony Dwyer of Canaccord Genuity recently highlighted in notes to clients:

I hope I’ve given investors and traders enough to chew on or mull over with regards to recent price action in risk assets. Near-term, a great deal of market direction will depend on how quickly China’s economy resumes normalizing and the U.S. COVID-19 cases are discovered while seasonal weather increasingly proves to halt the spread of the virus. We’re already seeing the former desired outcome improving, as China’s commerce and manufacturing slowly come back.

And in case you haven’t noticed by now, the market is no where near as expensive as it was 2 weeks ago. Stick to your game plan, review your process and maintain flexibility in a fast moving market environment!