“Let uncertainty reflect in your position size.

The sooner you get used to drawdowns. The better you will be able to suffer the drawdowns in the future.

No better way to produce better disciplines than by taking big drawdowns.

This is the type of stuff you won’t find on social media. It’s the AVOIDANCE of drawdown that gets attention.

The best hedge doesn’t cost you anything and that’s the cash you have on the sidelines. Doesn’t cost you anything emotionally and all you have to do is follow the scheduled fund flows and put the money to work when the market is pulling back.“

– Seth Golden, Chief Market Strategist at FinomGroup.com (Contributor/Premium Members Only)

Mid-week Summary

Wednesday, August 13th, 2025

Welcome to Market Mania!

Where every headline is a twist, and the only constant is surprise.

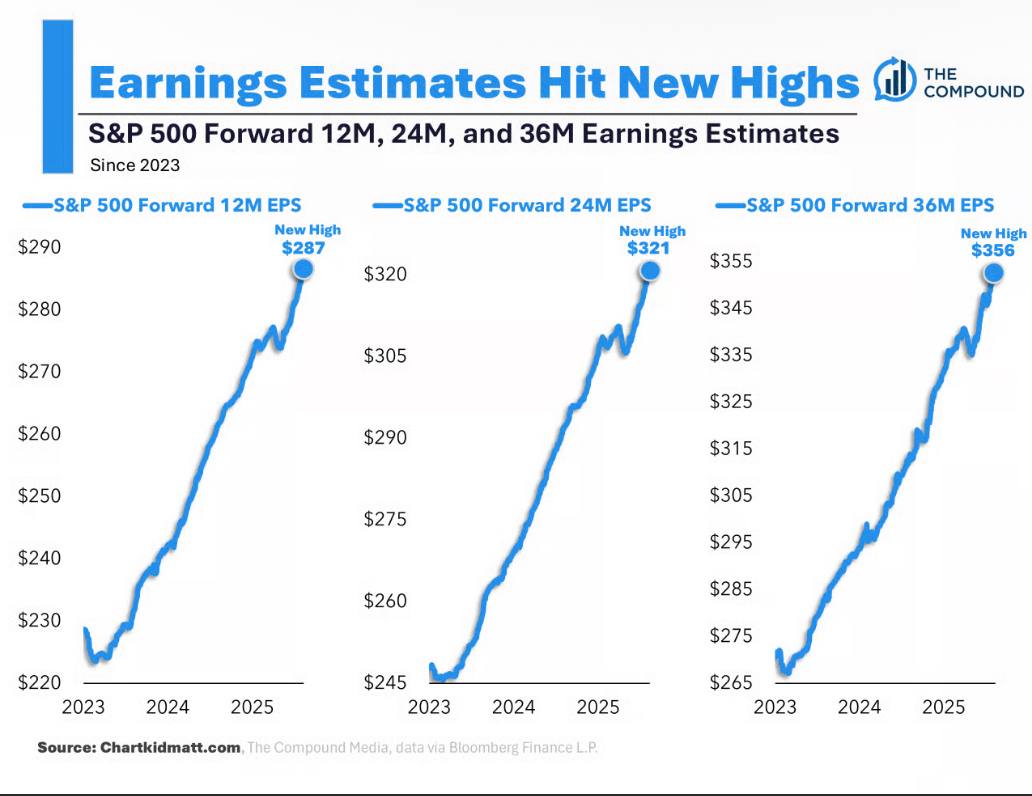

As we stand in mid-August, the market continues to defy the usual bearish narratives. Core inflation’s modest uptick year-over-year barely excited the bears 🐻, as the “permabulls” continue to shrug off shallow pullbacks and embrace significant, back to back years of double-digit earnings growth. Below is a wonderful chart from @mattcerminaro that wonderfully delineates these nuances. Breadth remains robust, embodied most recently by the Global Bull Market Advance/Decline Line hitting another all-time high just yesterday, while the widely anticipated recession still refuses to appear despite relentless warnings from financial media. A striking but underappreciated reality, underscored by veteran strategist Jim Paulsen, is that in the post-war era, excluding the 3 months where the FED cut in 2024, the Fed has “retained a tightening force” throughout this entire bull run—an extraordinary anomaly in market history.

Many are still bracing for the “eventual recession,” pampering their “eventual-ysis,” but it’s easy to forget that Powell has presided over FOUR bear markets in the past seven years alone, and three in the past four(ish) years for Trump. Additionally, there’s never been 3 BEAR 🐻 markets in 5-year period, neva’ eva’! In fact, this unusual backdrop—with atypical market rhythms and multiple sharp drawdowns behind us—makes “aggressive discipline” and SAVVY investing more essential than ever.

Today's CPI report kept a September rate hike in play. Historically, the $SPX has rallied when the Fed has cut rates after a long pause (>6 months).

Aligning a September 17 cut to 2025 gives an average 2H gain of 14%. Not a forecast, but interesting historical perspective. 3/3 pic.twitter.com/T48pC1zUWR— Ed Clissold (@edclissold) August 12, 2025

Equities continued to plow ahead last week, recovering from the brief growth scare a week earlier following the lackluster jobs report. The S&P 500 index continues on its V-shaped recovery track and remains in the running for the fastest and strongest recovery ever following a… pic.twitter.com/TOJFHNqKLy

— Jurrien Timmer (@TimmerFidelity) August 12, 2025

Recent analysis by Jurrien Timmer adds a crucial dimension to this view. His “Anatomy of a 20% Drawdown” chart reveals that the initial magnitude of recovery following a drawdown often signals if the gains will extend or deteriorate over the subsequent 12 months. Given our current Quant data and the market’s ignorance of August scheduled fund flows (so far), the evidence suggests we are likely on the path of the former, with sustained strength underway. This reinforces the idea that it is not simply whether the Fed cuts rates at all-time highs that matters, but the pace, length, sequencing, and broader data backdrop that truly dictate outcomes. When rate cuts serve as preemptive support amid resilient earnings, improving breadth, and manageable inflation, they often coincide with extended rallies—barring unforeseen shocks or policy missteps. Conversely, cuts triggered by a deteriorating economy frequently align with deeper selloffs.

The Fed remains on pause, but the Fed Funds Futures market continues to price in nearly a 95% probability of a September cut, reflecting shifting sentiment around inflation and slowing growth. Meanwhile, political noise, renewed tariff headlines, and the approaching Jackson Hole symposium add layers of unpredictability. However, the bigger narrative remains the market’s resilience: leadership endures, volatility measures like VXX are at new lows, and earnings beats continue to surprise to the upside. For investors, the mandate is clear—stay focused on process, stay flexible, and never underestimate the power of broad market participation driving the trend forward.

S&P 500 EARNINGS

Post-GFC, S&P earnings have grown faster than inflation all but 5.9% of the time (5y ROC).

Since 2013, earnings have been > inflation 100% of the time.

With S&P 500 ROIC > 20%, these companies will continue to absorb cost increases and maintain pricing power. pic.twitter.com/jIc2cb4Zvt

— Warren Pies (@WarrenPies) August 10, 2025

In a complementary perspective, Warren Pies highlights inflation and earnings dynamics that add nuance in this late-cycle environment. While seasonal summer buying has buoyed markets, Pies cautions against mistaking temporary strength for a durable rally unsupported by fundamentals. He voices skepticism around the persistent vigor in small-cap stocks and flags lingering concerns about the labor market and broader growth that may not yet be fully priced in. Importantly, Pies stresses the complex interplay between inflation trajectories and earnings performance—both key drivers of market sentiment and Fed policy. Though inflation has softened and earnings outpace inflation in many sectors, he advises care in interpreting any single data point as definitive, recognizing market patterns can shift quickly as new data and economic policies evolve. But does the labor market matter more?

Rather than anchoring to simplistic narratives of late-cycle tiredness or premature exuberance, Pies counsels disciplined vigilance, watching closely how inflation data, earnings results, labor market signals, and policy moves weave together. This holistic and data-dependent approach aligns well with the fabric of 2025’s ever-shifting market story.

In Short: Why the Bull Still Has Room to Run

The August pullback so far has been shallow, perfectly in line with the probability-weighted setups flagged in late July. Every dip below key quant “baseline” levels like 6,358 on the S&P 500 has quickly attracted buyers, reinforcing that the dominant trend is still higher. Breadth thrust signals from April–May remain firmly in play, historical quants show a near-perfect track record for higher highs into year-end, and even volatility spikes have failed to take more than 2–3% off the index before recovery.

Technically, leadership in Technology and Semiconductors is still intact, though showing some narrowing breadth, a natural sign of a later-stage bull market. This phase rewards broad ETF exposure over concentrated stock picking. Multiple semiconductor “buy” signals, including the rare 4‑month win streak trigger, suggest durable strength into 2026, even if the sector sees an autumn breather.

On the macro side, the economy is softening at the margins, ISM data points to sluggish new orders and stubborn prices paid, but corporate earnings tell a different story: double-digit growth, record margins, and no sign of an imminent contraction.

Bottom line: sentiment may swing with each data print, but the market’s message remains unambiguous, pullbacks are opportunities, not warnings. With strong breadth signals, historically bullish seasonal triggers, and policy potentially shifting toward support, the path of least resistance still points higher into Q4. The smartest move now is to stay process-driven, keep cash working, and let the data, not the headlines, dictate your actions.

This is August’s Market Mania—unconventional, resilient, and a vivid reminder that the most compelling market stories unfold when the world expects the worst.

Stick to the plan.

I've used the attached playbook for recognizing "What Inning is the Market" trend.

Based on the playbook I would suggest rally is in Middle 5th Inning with roughly half of the trend in the books. $SPX $QQQ $SPY $NDX $NYA #investing #trading pic.twitter.com/hx8hxJgB9m

— Seth Golden (@SethCL) July 1, 2025

Down is good. Up is simply better. 💯

Stay tuned as we cut through the noise, break down this week’s big earnings, and spotlight the signals that matter across ever-shifting markets.

TLDR: The script keeps changing, but our approach doesn’t. Smart analysis, sharp process, better outcomes.🤝

Here’s what’s catching the eye of the sharpest minds in the market today!

Chart(s) of the Week

🏆 Today’s Chart of the Week was shared by Seth Golden (@SethCL):

Current bull mkt began Oct 12, 2022.

There have been 5 NON-recessionary bull markets since 1957.

Current bull mkt is trailing the greatest NON-recessionary bull mkt by only +1.2%. I would not hold opinion this ends without surpassing. Markets have mandates!$SPX $ES_F $SPY… pic.twitter.com/6sPLROufaY

— Seth Golden (@SethCL) August 11, 2025

Seth Golden’s tweet points out that the current bull market — which began October 12, 2022 — is just shy of surpassing the greatest non-recessionary bull market gain since 1957. As of August 11, 2025, it stands at +78.6% over 33 months, trailing the 1962–1966 non‑recessionary run (+79.8% over 43 months) by only 1.2%. The fact that it has approached this historical benchmark without a recession in the rearview is meaningful, especially when you examine the history Seth included in his tweet.

Since 1957, there have been 13 bull markets in the S&P 500:

• 8 of them followed a recession

• 5 did not

The two key differentiators Seth’s table from @LeutholdGroup makes clear are:

1. Duration – Non-recessionary bull markets average roughly 33 months, versus about 61 months for those following recessions. Our current bull at 33 months sits right on that average lifespan for a non-recessionary run.

2. Magnitude of Gains – Bulls that follow recessions tend to be far more powerful, producing nearly double the cumulative returns of non-recessionary bulls. That’s because recessions usually reset valuations and earnings expectations more deeply, allowing for a longer, steeper recovery.

If this cycle remains a non-recessionary bull, purely on historical rhythm, we are approaching a zone where gains and duration are “average” — meaning, from a statistical perspective, the easy part of the run may be behind us unless fresh catalysts emerge.

What This Means in Today’s Context

• Macro backdrop: Uniquely, this entire bull run has occurred with the Fed holding rates steady — not easing — something strategist Jim Paulsen rightly flags as historically rare. Now, with nearly a 95% probability of a September rate cut priced in (per CME FedWatch), the market could soon see its first monetary tailwind of this cycle.

• Breadth and earnings: Breadth remains robust (Global Bull Market A/D at all-time highs) and corporate earnings growth remains in the double digits. These conditions typically align with sustained uptrends, particularly when paired with a Fed pivot.

• Risk positioning: Historically, cutting rates at all-time highs is not inherently bearish. The real differentiators are the reason for the cut (preemptive vs reactive) and the sequencing of macro data. If this cut is an “insurance” move into a still-healthy earnings and growth backdrop, it could extend the bull market beyond “average” non-recessionary norms.

Seth Golden’s data shows that by the traditional metrics of duration and magnitude, the current bull market is mature for a non-recessionary cycle. However, history also shows that the addition of new macro supports — like an initial Fed cut, improving liquidity, and powerful breadth thrusts — could stretch and even reclassify a cycle’s trajectory. If those catalysts land, the current run could transition from a textbook non-recessionary phase toward something bigger, more akin to a 2009/COVID-like recession expansion in length and gains.

So while statistics argue we’re “late” for a non-recessionary bull, macro dynamics suggest this movie may still have another act. The key is in the catalysts — and right now, several of them are aligning.

BONUS:

Selling is easy, buying is not. Ask yourself why and therein may lie your answer.

Came into 2025 with:

22X Forward P/E… too high

30% cap-weight for Tech… too high

Highest household equity exposure… too high

Buffett Indicator sell signal… too soon

24-month long Burry sell signal… too soon

Longest yield-curve inversion since ‘80s… too long

Longest… pic.twitter.com/m6CLWUe7ll— Seth Golden (@SethCL) July 30, 2025

Scared yet? Okay good, now do it scared!

Some of the worst market crashes happen after the peak of investor sentiment (Bull vs. Bear spread)$SPX $ES_F $SPY $QQQ $NYA $RUT $DIA $VIX pic.twitter.com/W6FshlMZeN

— Seth Golden (@SethCL) August 11, 2025

JULY CPI

-Supercore +.48% MOM driven by medical care (highest MOM gain since 22).

-Yet, overall report shows little tariff effect (modest increases in furnishings, etc.)Bottom Line: The Fed's excuse to pause (tariffs) is losing its power. Sept cut odds go up to 96% (from 87%) pic.twitter.com/B7Q3YPfVzF

— Warren Pies (@WarrenPies) August 12, 2025

Quote(s) of The Week

People think good decision-making is about being right…It’s not. It’s about lowering the cost of being wrong & changing your mind. When the cost of mistakes is high, we’re paralyzed with fear. When the cost of mistakes is low, we can move fast and adapt. Make mistakes cheap,…

— Linda Raschke (@LindaRaschke) August 10, 2025

“Much will be required of the person entrusted with much,

and still more will be demanded of the person entrusted with more.” – Luke 12:48

Al que se le ha dado mucho

Se le va a exigir mucho

(From todays Gospel)

— Finom Group AYNI Luis Solórzano (@aynirealtor) August 11, 2025

Risk not!

Reward never! pic.twitter.com/bfuJvqLHZx— Seth Golden (@SethCL) March 29, 2025

Any amount of intelligence can be overridden by: ego, insecurity, immorality, bad incentives, or impatience, usually in that order.

— Morgan Housel (@morganhousel) August 12, 2025

BONUS:

How many of these have you heard? You 🫵 decide!

Phrases often heard near market tops:

1. "This time it's different"

2. "Valuations don't matter"

3. "Everyone's getting rich"

4. "New paradigm"

5. "Everyone's an expert"

6. "It's backed by fundamentals"

7. "The smart money is all in"

8. "This is generational wealth"

9. "Buy the…— The Great Martis (@great_martis) August 10, 2025

Some quotes from 1929, before the devastating crash.

Sound familiar?

You decide 🫵

1. Charles E. Mitchell, president of National City Bank, September 1929:⁰“The industrial condition of the United States is absolutely sound, and nothing can arrest the upward movement.”…

— The Great Martis (@great_martis) August 9, 2025

“Everybody in the world is a long-term investor until the market goes down.” Peter Spencer Lynch

— Adithia Kusno ☦️🐂🚀💎🙌🎯 (@AdithiaKusno) August 11, 2025

Top 10 Tweets of The Week

Math is still a thing, right?

Always be in stocks and/or sectors with ever-decreasing supply and ever-increasing demand

Always be🍎 iSmart$SPX $SOXX $XLK $AAPL $SPY $SMH $MSFT https://t.co/ubzxUg3URU pic.twitter.com/SCaiw6kKI5

— Seth Golden (@SethCL) August 12, 2025

Few interesting datapoints I thought I’d share, without context of course!

The three most correlated six-month periods with the last six months for $SPY are the six months ending on 2/27/24, 6/30/03, and 4/29/19. Here's how those three periods traded over the next six months: pic.twitter.com/43DwaFtgm4

— Bespoke (@bespokeinvest) August 12, 2025

The trillionaire club, led by Huang, Nadella, Cook, Pichai, Jassy, Zuck, Tan, and Musk, was once again 'the market' last week. pic.twitter.com/1rs4ss7fVQ

— Bespoke (@bespokeinvest) August 12, 2025

The cumulative A/D line of the trillionaires club hit a new high last week. pic.twitter.com/c5ni6KAT5Q

— Bespoke (@bespokeinvest) August 12, 2025

Elon Musk is the richest person in the world according to Forbes. Here’s the list of Forbes “world’s richest” by year since 1987: pic.twitter.com/mmnO4Fodo2

— Bespoke (@bespokeinvest) August 9, 2025

Scheduled fund flows are just that – scheduled. They’re gonna flow, its just a matter of when and to what degree.

"Seasonal tendencies are just that – tendencies. They hold true most cycles, but they can be overwhelmed by outsized forces, such as a pandemic or financial crisis. The question feels especially relevant for 2025, given financial markets have been so news driven" – NDR pic.twitter.com/TDMEVI5y82

— Andrew Thrasher, CMT (@AndrewThrasher) August 11, 2025

Just That!

NASDAQ Hot Julys & Later Buys. Every NASDAQ “Hot July” since 1971, except 1980 was followed by a retreat that averaged 5.8% from July’s close to a subsequent low in the second half of the year. Expecting pullback over next 2-3 months. https://t.co/5DlTNGlfp1 pic.twitter.com/uyjn9FuQx8

— Jeffrey A. Hirsch (@AlmanacTrader) August 1, 2025

What if… every time is different?

The Nasdaq 100 just did something it's never done before. Not in a good way.

For the 1st time since inception, NDX closed at a record high with less than 48% of its members trading above their 50-day moving average. Over the past 40 years, an average of 76% of members were above… pic.twitter.com/UsBNGGcDIC

— SentimenTrader (@sentimentrader) August 12, 2025

If valuations not a timing tool, why are you timing the tool, fool!

Amongst the most overvalued markets ever, on par with 1929.

Does not mean it can't get more overvalued.

Though, some people say the market has good foundations!?!

———————

Free eBook "1-Year US Stock Market Outlook” with over 70 charts. Download 👇… pic.twitter.com/8ftnxFxeGG— BraVoCycles Newsletter (@BraVoCycles) August 12, 2025

Investors will focus on CPI, then PPI. Not vice versa. (-;

Tomorrow is CPI day; the consensus is +2.8% YoY, up from 2.7% last month. I have no strong opinion on this specific print.

However, in trying to gauge inflation around Christmastime or spring 2026, I want to show you this chart. On Friday we get Empire Manufacturing. Prices… pic.twitter.com/M5fS1G6kAY

— Jeff Weniger (@JeffWeniger) August 11, 2025

BUT someone told me I should be dumping stocks when VXX is at all-time lows?

my $VIX $SPX model fired an equity "buy" signal last week (August 4th), while i was out of the office… volatility (lower panel) spiked on the 1/10 oscillator and then settles… it was the first one since April… pic.twitter.com/Hn9QsqlqDk

— David Cox, CMT, CFA (@DavidCoxRJ) August 10, 2025

BUT tell me more about how this reminds you of the dotcom bubble!

The AI story has been strong ever since ChatGPT was released back in late 2022 💪

Now that story is showing up in the macroeconomic data as well. In a big way …

New blog on the positives and negatives 👇@CarsonResearch @RyanDetrick https://t.co/Lwlyfl5PCm pic.twitter.com/gOoCilynrW

— Sonu Varghese (@sonusvarghese) August 10, 2025

Autumn is coming so make sure you are ready for the FALL, surely climate change hasn’t been a thing this year either?

Goldman's latest (still very early) analysis of tariff effects thru June 2025:

-Foreign exporters absorbed 14% of US tariffs

-US companies ate 64%

-US consumers ate 22%

-Protected US companies also raised prices

-Consumers will see bigger price increases (70%) thru the Fall pic.twitter.com/0S0fVnEvQp— Scott Lincicome (@scottlincicome) August 10, 2025

How was that shining moment, Marko? Miss the feeling? Doesn’t sound too SAVVY to me.

Not just seasonality, but an increase in volatility (last 2 days) typically leads to outflows. This bounce should be faded.

— Marko Kolanovic (@markoinny) August 4, 2025

Disruption is here. Are you still stock picking or just sticking to index/sector ETFs, Keep It Simple Stupid! 💋

BBG: BoA's AI at risk basket (companies some strategists expect will see falloffs in demand as AI applications become more widely adopted) has underperformed the S&P 500 Index by about 22 percentage points since mid-May after previously more or less keeping pace with the market… pic.twitter.com/iB7TwLPuv6

— Neil Sethi (@neilksethi) August 10, 2025

We live, AND we learn. Right?

It's true that throughout history, we have never experienced a time with zero foreclosures. https://t.co/jKve7tEMuO pic.twitter.com/m5l9gYzNlT

— Logan Mohtashami (@LoganMohtashami) August 10, 2025

Breadth still suck? Yes it can always get worse!

What a day for the average stock.

Small-caps $IWM up nearly 3%.

NYSE advance/decline ratio almost 6/1…one of the strongest readings since the April lows. pic.twitter.com/IJyWPovn89

— Mosaic Asset (@MosaicAssetCo) August 12, 2025

The higher we go, the more bearish they will get. Sad, true, and simply wrong!

A lot of tactically #bearish commentary heading into this week's #trading . Mother Market loves to confound, and today was no exception. On Tuesday alone, $SPX's +1.13% rally nearly covered the upside it has traveled on average in the 4 trading sessions following the 12 previous… https://t.co/TRcZ6RoiWn

— The Range (@TheRangeDaily) August 13, 2025

Join the Finom Group Family – CLICK HERE to Upgrade Now!

Master the markets with Seth Golden and our “Finominals” community! For just $24.99/month, unlock weekly 5000+ word macro research reports packed with charts and actionable insights. Go Premium at $79.99/month for daily Telegram Traders Corner, myth-busting Zoom sessions, and live 1%+ scalp/swing trading with Seth. Don’t let market noise win—join our Contributor or Premium Membership to build confidence and achieve your financial goals.

[Click here for a free Morning Market Setup sample from August 11th 2025!]

Finom Group – Recent Reports

August 10, 2025

August 3, 2025

July 27, 2025

July 20, 2025

July 13, 2025

You’re all caught up now. Thanks for reading!

If you have any questions, feel free to message Seth Golden or contact us support@finomgroup.com

Comment below or tag us on X (@FinXWeekly) with your thoughts—your feedback drives our innovation.