“Markets are intrinsically constructed to go higher, not lower and investors largely position and participate for such outcomes. Hence, if there are quant probabilities informing of a greater than 70% downside probability, these still have a higher failure rate than quants informing of a greater than 70% positive outcome. In other words, always leave more room for negative quants to fail than positive quant failures. Markets are designed to go higher, which is the basis for investing.”

– SETH GOLDEN, CHIEF MARKET STRATEGIST AT FINOMGROUP.COM

(CONTRIBUTOR/PREMIUM MEMBERS ONLY)

MID-WEEK SUMMARY

WEDNESDAY, SEPTEMBER 24TH, 2025

WELCOME TO MARKET MANIA!

WHERE GROWTH SCARES AREN’T ALWAYS RECESSIONS, AND EVERY DIP DARES INVESTORS TO BLINK FIRST.

The final week of September finds the market suspended between historic momentum, technical fatigue, and an oncoming wave of FISCAL policy uncertainty—a narrative echoed and dissected in this weekend’s comprehensive Finom Group Research Report. With just five trading days left in the month, the S&P 500 finds itself viciously attempting to cling on to a rare September gain of over 3%, threatening to break seasonal expectations for the second year in a row, something that hasn’t happened since 2017, 2018, 2019 era. Will the market be able to outperform expectations as the most bearish week of September makes its surprise appearance near 6,700? Read on…

A resurgent bull market continues to outpace even the highest Wall Street expectations—S&P 500 earnings growth estimates have been steadily revised higher, and strategists have repeatedly upgraded their year-end targets, often after being caught off guard by relentless gains off the April lows. Even so, this melt-up is showing classic late-stage symptoms as Year 3 of the new bull comes to an end… (can we get 3 years of double digit gains for the S&P500)? Overextended technicals, the lowest Put/Call ratios since May, and mounting evidence of exhaustion in leading Tech plays as Big Tech and AI stocks go through multi-session reversals is confusing traders and investors on/off among Wall Street, with references to the tulip 🌷/dot-com bubble growing louder and louder.

Fueling market confidence is the solid foundation of corporate profit margins, sustained 3-month EPS upward revisions, and a “no-landing” labor and relentless consumption backdrop. Recent economic data show jobless claims stabilizing and retail sales still growing at a healthy clip, with no imminent sign of recession across the “Big Four” economic indicators. But, as detailed in this week’s quant breakdown, the probability of a near-term consolidation or pullback has never been higher all year, helped along by stretched momentum, a string of technical “overbought” signals, and a looming U.S. government shutdown standoff between Congress.

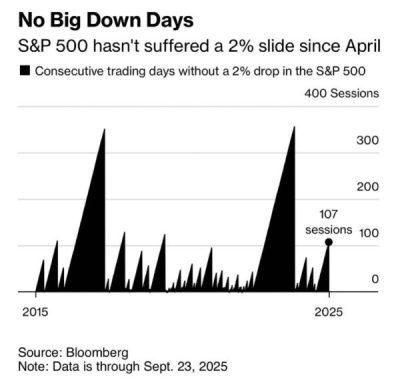

The S&P 500 is marching into rarefied air: not only has it gone over 100 sessions without a 2% drop (the longest stretch since July 2024), it is also attempting to rack up a five-month winning streak—a pattern that, historically, begets 70% probability of higher returns over the subsequent 1-3 months. Yet every quant from Wayne Whaley to SubuTrade is flashing yellow: when price stays above its 50-DMA for over 100 days, and RSI holds in overbought territory, the odds for a near-term correction multiply and/or compound.

Pullback soon?

The S&P 500’s RSI has stayed above 45, for 102 straight days — one of the longest streaks in history.

In the past 60 years, the S&P was lower EVERY time 2 weeks later pic.twitter.com/wCwKUz7FmK

— Subu Trade (@SubuTrade) September 18, 2025

Still, the resilience of the April 2025 breadth thrusts—Zweig and DeGraaf included—continues to serve as the market’s backbone. Not just a footnote, these breadth super-signals remain a fundamental reason dips have been shallow and new highs relentless. The lesson? Negative quants have a much higher failure rate in secular bull trends, as the market is structurally built to climb and reprice on optimism, not pessimism. The repetition of this market fact should be absorbed by savvy investors/traders!

The fact markets express technical bear markets and not just recessionary bear markets allows the macro-tourists to lay claim to the old adage "markets have priced 9 of the last 4 recessions." The problem with this type of attack on forward discounting markets and the accuracy of… pic.twitter.com/p9VflmuK2K

— Seth Golden (@SethCL) August 5, 2025

In this phase, “buy the dip” isn’t just a meme—it’s a quant-backed playbook. Every pullback, even a long-overdue -3% flush, is an opportunity for disciplined allocators—not a reason to run for the exits. Small-caps, though having flashed some “catch-up” outperformance, remain a tactical trade and not a core overweight in the GCP. Leadership still skews toward Quality Growth, Tech, and the consumer, with recent rate cuts likely to benefit cyclicals, housing, and discretionary as the fourth quarter approaches.

Do you want more rate cuts or fewer?

When the economy has been strong enough to need only 1 or 2 cuts after a pause, Cyclicals have outperformed. When 4 or more were needed, defensives have led and bear markets were found, if not recession as well.$SPX $SPY $ES_F $QQQ $NYA… pic.twitter.com/YlRmJN3D8l

— Seth Golden (@SethCL) September 24, 2025

Fed Chair Powell continues to signal caution—even as two rate cuts are still on the table for year-end, the path is muddied by a divided Committee and sticky inflation. The bond market’s muted reaction so far is a tell: equity investors continue to look through noise, but any surprise in PCE inflation or a drawn-out budget fight could be the spark for that much-needed consolidation phase if these cuts do indeed become recessionary and not just adjustment cuts.

The facts are: fundamentals remain strong, profit growth has surprised, and technicals are stretched—but the market rarely gives back much without a true catalyst. Surely a lot can go wrong and you could argue that the perfect storm has arrived… If and when we get that correction, the discipline will be in recognizing opportunity, not fear.

As our proprietary research report highlights: flexibility is vital, seasonality (scheduled fund flows) can mislead when considered/sequenced incorrectly, or given exogeny/endogeny… but nevertheless the weight of evidence still favors higher highs into year-end rally—with the caveat that shakeouts are overdue and should be viewed as invitations to allocate for the long game. Keep moving forward, keep questioning price, and let process—not prediction—guide the way.

KEEP RECENCY BIAS IN CHECK. IN THIS CYCLE, COMFORT IS A COST—AND DISCOMFORT, WHEN MANAGED RATIONALLY, IS WHERE OUTPERFORMANCE IS FOUND.

CUT THROUGH THE NOISE, AVOID THE HERD, AND GET READY FOR ANOTHER WILD WEEK IN MARKET MANIA.

CHART(S) OF THE WEEK

🏆 TODAY’S CHART OF THE WEEK WAS SHARED BY SETH GOLDEN AND LEUTHOLD GROUP (@SETHCL & @LEUTHOLDGROUP):

Warning flag⚠️

Margin Debt has begun to rise at faster rate than $SPX. In Aug, its Y/Y growth rate was 33% compared to a “mere” 14% for SPX.

Tops of 2000, 2007 and 2021 were all preceded by similar attempts to magnify SPX gains that were already far above average.$ES_F $SPY… pic.twitter.com/3R100r9Yvg

— Seth Golden (@SethCL) September 23, 2025

🏆 Chart of the Week: Margin Debt as a Warning Flag

This week’s featured chart, shared by Seth Golden from Leuthold Group, delivers a clear and timely message as the market wrestles with historically extended valuations, persistent breadth, and a wall of macro crosscurrents.

The graph overlays the S&P 500’s price (black line), 12-month percent change in margin debt (blue line), and the difference between margin debt growth and S&P 500 growth (bottom panel) from 1998 to present. The warning: August saw margin debt growth accelerate to a 33% year-over-year rate, outstripping the S&P’s 14% rise. This is not just a random curiosity; it’s a pattern that has foreshadowed pain in past cycles. Notably, the “red zone” in the lower panel (where margin debt growth far exceeds price growth) has COINCIDENTALLY preceded the major tops of 2000, 2007, and 2021—each marking the kind of risk climate in which exuberance and leverage outpace fundamentals and caution. It is important to note, margin debt does not cause recessions and/or steep bear markets… but if you look closely your bias can feed you the information you want to exstrapolate from the data, one way or another!

With the S&P 500 entering late September up more than 3% month-to-date—threatening to overturn the long-standing “September curse”—it’s easy to forget the risk building under the hood. Today’s market thrives on resilience and breadth, with shallow dips bought aggressively, but a sudden surge in margin debt offers a cautionary note about complacency. As investor leverage begins to magnify returns—even as technical and sentiment indicators scream “overbought”—the risk of an abrupt shakeout rises.

This is a classic late-cycle signal:

• Attempts to magnify late-stage gains, especially in an already extended market, historically lead to adverse outcomes.

• Exogenous events, policy risks, or an unexpected liquidity crunch have more fuel to turn corrections into disorderly unwinds when leverage is surging.

Takeaways for Investors

• Risk isn’t always about trend or headline—sometimes, it’s about how aggressively investors are playing catch-up.

• Margin surges are rarely the timing tool, but they mark a change in market structure—a shift from healthy participation to speculative churn.

• The lesson: monitor leverage, breadth, and liquidity with even greater attention as the cycle matures, and recognize the difference between RATIONAL EXUBERANCE and “FAIRLY HIGHLY VALUED PRICES”, per Jerome Powell. 😉

As we close one of the strongest September runs in recent history, heed the lesson: conviction is the foundation, but vigilance is the shield. Process and humility, not leverage, will define the winners in this later-stage, non-recessionary bull.

BONUS:

Now up roughly 85% off the bear market low.

📢Not all bull markets should be considered equal

Bulls that DO NOT start from recession, DO NOT gain as much as those that do start from recession. In the 4 other times a bull launched w/o preceding recession, its gains were solid, 48% – 80%, never spectacular.$SPX $SPY… pic.twitter.com/YL5UTivDtm

— Seth Golden (@SethCL) August 26, 2025

In case you wondered why stocks are at new highs. pic.twitter.com/AFY8QHJiBa

— Ryan Detrick, CMT (@RyanDetrick) September 23, 2025

At 88.2%, Forward positive 1 Quarter revenue is the 3rd highest in history.

"This is not an over exuberant stock market, it's a Blisteringly strong fundamental corporate landscape."

Imagine if the market actually did have the same Dotcom multiple…$SPX $ES_F $SPY $QQQ $IWM… pic.twitter.com/p9kZwWeA8W

— Seth Golden (@SethCL) September 23, 2025

QUOTE(S) OF THE WEEK

“There are no get-rich-quick schemes. That's just someone else getting rich off you.” – @naval pic.twitter.com/IJw5Bq5bL6

— Brian Feroldi (@BrianFeroldi) September 21, 2025

Over exuberance is the denying of normalcy and logic in-favor of the unicorn 🦄 and euphoria. You’ll know yesteryear.

~Seth Marcus

— Seth Golden (@SethCL) August 15, 2025

Repeating this Druck quote every morning to myself like some zen mantra so I don’t do something stupid pic.twitter.com/b19QGPiNss

— BuccoCapital Bloke (@buccocapital) September 20, 2025

"when you sell your great companies and add to the losers its like watering the weeds, and cutting the flowers."https://t.co/Cz4RvdtTLg

— Finom Group AYNI Luis Solórzano (@aynirealtor) September 21, 2025

— Peter Mallouk (@PeterMallouk) September 20, 2025

— Psyche Wizard (@PsycheWizard) September 18, 2025

TOP 10 TWEETS OF THE WEEK

The Energy sector is breaking above resistance today to its highest level since the tariff-tantrum in April. $XLE pic.twitter.com/jzz7QQEznA

— Bespoke (@bespokeinvest) September 24, 2025

15-year chart of the Russell 2K: pic.twitter.com/2hTg7M7cIp

— Bespoke (@bespokeinvest) September 19, 2025

The secular bull market in US stocks is now 12 years old

Shiller PE Ratio approaching TMT peak in 2000

Current market giving late 1998 vibes and rate cuts will likely give us a bubble in 2026. The trick will be to exit before everything turns into pumpkin and mice. $NDX pic.twitter.com/oDi6G8GI70

— Puru Saxena (@saxena_puru) September 24, 2025

Lot of talk how valuations are 'high'.

Here's another reminder there is virtually no correlation between P/E multiples and what the S&P 500 does the next year (R-squared of -0.01). pic.twitter.com/CKCvUAsJP3

— Ryan Detrick, CMT (@RyanDetrick) September 24, 2025

“I’ve been a cheerleader for the resilience of the economy, and even I’ve been surprised that earnings — profit margins — haven’t really flinched in the face of Trump’s tariffs.” – @yardeni

"Since the 1920s, there have been four Roaring decades, i.e., with the S&P 500 rising over 200%. We may be in a fifth now, to be followed by a sixth during the 2030s."@yardeni pic.twitter.com/ylzYQKgncO

— Daily Chartbook (@dailychartbook) September 24, 2025

2018:

Tax reform followed by tariffs, followed by rate hikes, followed by rising yields, rising crude, rising Dollar

2025:

Tax reform followed by tariffs, followed by rate cuts, followed by falling yields, falling crude, falling Dollar

Just because 2 lines appear to be going… pic.twitter.com/FnXmffLKuy

— Seth Golden (@SethCL) September 24, 2025

There was a large divergence between ARKF (lower high) and the S&P 500 (higher high) in late 2021 before the 2022 bear market. No such divergence is present today. SPY VOO pic.twitter.com/dcLst4836o

— Chris Ciovacco (@CiovaccoCapital) September 23, 2025

“Selling fear to another person is terrible, it’s a terrible thing.”

~ Warren Buffett

Rich Dad and keep you from becoming a Rich Dad!

When you're in the business of selling fear, you're in a terrible business and that business should be shut down.

Marko Kolanovic is looking for someone to play Chutes & Ladders or Connect 4 with; you two should talk? $SPX $SPY… pic.twitter.com/fIvU6eD8Pc

— Seth Golden (@SethCL) September 22, 2025

28 ATHs in 2025

8 new ATHs for the S&P 500 in September

Most in September since 9 in 2017 pic.twitter.com/4lXVzKcjcb

— Ryan Detrick, CMT (@RyanDetrick) September 23, 2025

This is wrong, ABSOLUTELY wrong

1. Heavy Truck sales account for ~.005% of GDP

2. Heavy Truck sales have been as much as -21% Y/Y

without a recession

3. Heavy Truck sales have been +5%, down -10%, -15%,

-20%, 30%

4. In other words, it doesn't indicate anythingSo… https://t.co/rwqgWZslLr pic.twitter.com/u4ape6uk9w

— Seth Golden (@SethCL) September 23, 2025

For those that hate TA on $VIX….

Will we see spot vol close above the 100-day MA for the first since May after five prior failed attempts? pic.twitter.com/pwk0Comknd— Andrew Thrasher, CMT (@AndrewThrasher) September 24, 2025

In relation to the @WSJ story about the size of MF assets, aka "cash on the sidelines," I again make this point. The S&P 500's market cap is $60T+! We have to scale things because "number go up." Viewed this way, the $7T+ in money markets isn't very impressive.@carlquintanilla… pic.twitter.com/q0Duqcvz9T

— Dan Greenhaus (@DanGreenhaus) September 22, 2025

📢NO SUCH THING as Money Market Funds signaling cash on the sidelines for equities.

ONLY 1 environment where cash is drawn-down from MMFs and allocated to equities, steep Bear mkt combined w/Recession i.e. 2009/2020 (green).

It makes MMFs an absolutely friggin' perfect timing… pic.twitter.com/nYZEWetJbt

— Seth Golden (@SethCL) September 23, 2025

$SPX wrapped up the first 9 trading days of Sept with 4 all time highs and a +1.92% gain, despite seasonal weakness. Historically, when Sept starts with ≥1 ATH and positive first 9 days, the rest of the month was positive 64.7% of the time, avg. +0.32%. #SP500 #Investing pic.twitter.com/53G28Rp8A4

— Bluekurtic Market Insights (@Bluekurtic) September 13, 2025

This week brings both September quad witching and the #FOMC meeting, two volatility drivers. Since 2000, the S&P 500 has been positive only 28% of the time in the 5 days after September quad witching, with an average decline of -1%. pic.twitter.com/a4GpIw86FC

— Bluekurtic Market Insights (@Bluekurtic) September 15, 2025

JOIN THE FINOM GROUP FAMILY – CLICK HERE TO UPGRADE NOW!

Master the markets with Seth Golden and our “Finominals” community! For just $24.99/month, unlock weekly 5000+ word macro research reports packed with charts and actionable insights. Go Premium at $79.99/month for daily Telegram Traders Corner, myth-busting Zoom sessions, and live 1%+ scalp/swing trading with Seth. Don’t let market noise win—join our Contributor or Premium Membership to build confidence and achieve your financial goals.

[Click here for a free Morning Market Setup sample from September 23rd 2025!]

FINOM GROUP – RECENT REPORTS

SEPTEMBER 21, 2025

At 6,600+ There Are Too Many Wallflowers At The Stock Market Dance

SEPTEMBER 14, 2025

September’s Op/EX And The Worst Week Of The Year Await Investors

SEPTEMBER 7, 2025

AUGUST 31, 2025

April to-date Markets Float Like A Butterfly; Here Comes The September Bee Sting?

AUGUST 17, 2025

Reflation Concerns Prove Short-Lived

YOU’RE ALL CAUGHT UP NOW. THANKS FOR READING!

If you have any questions, feel free to message Seth Golden or contact us support@finomgroup.com

Comment below or tag us on X (@FinXWeekly) with your thoughts—your feedback drives our innovation.