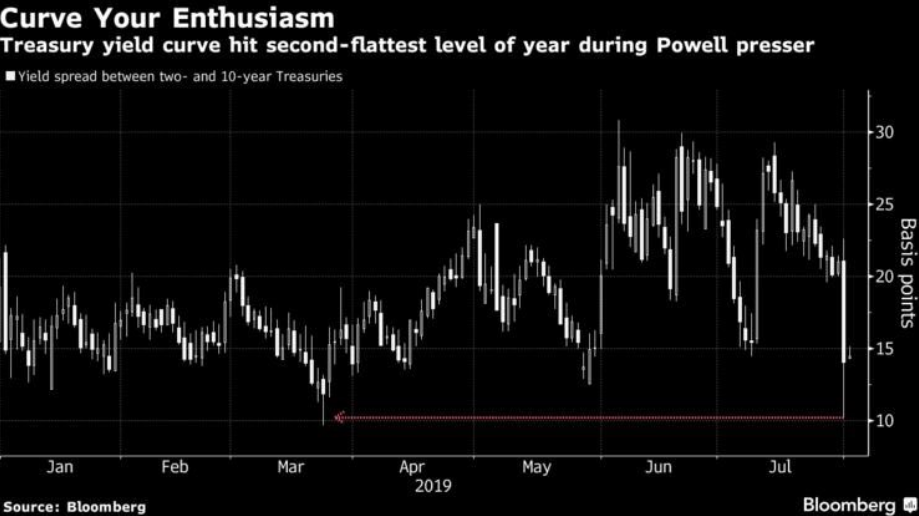

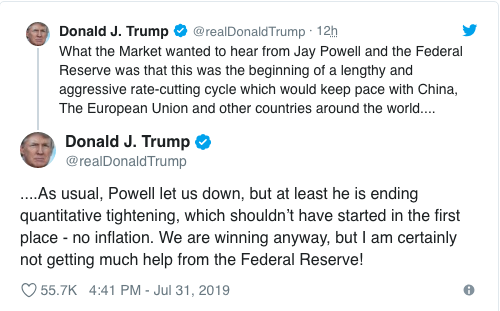

You wanted a rate cut, well you got it! And with that 25 bps rate cut you got an even stronger U.S. Dollar (DXY), pushing upwards of $98.80 and a flattening at the long-end of the bond yield curve (2s/10s = 15 bps spread).

So what did Jerome Powell say that the markets adversely responded to with a precipitous fall in equities? Firstly, recall that chairman Powell has a dubious record with regards to market performance on FOMC announcement days. The market, now, has only risen on FOMC days 2 out of 11 times under the leadership of chairman Powell. Here’s what he offered that led headlines as the DXY rose, yield curve flattened and equities plunged in the 2-4:00 p.m. EST hours on Wednesday.

“We’re thinking of it essentially as a midcycle adjustment to policy,” he said. Powell added that Fed officials “think it will serve all of those goals.”

Looking at the history of the Fed, Powell cautioned against assuming that this week’s cut is the beginning of the cycles that happened in the past.

“That refers back to other times when the FOMC has cut rates in the middle of a cycle and I’m contrasting it there with the beginning of a lengthy cutting cycle. That is not what we’re seeing now, that’s not our perspective now.

What you’ve seen over the course of the year as we’ve moved to a more accommodative policy, the economy has performed about as expected with the gradually increasing support. Increasing policy support has kept the economy on track and kept the outlook favorable.”

“Midcycle adjustment!” That’s what investors found hawkish, perceiving from the verbiage that the Fed may have issued a “one and done” rate easing statement. Markets overreact quite frequently to “Fed speak” and it is unlikely that midcycle adjustment means one and done.

“I think by that it means he doesn’t necessarily mean more cuts are coming, maybe not necessarily one off but not indicative of more aggressive cuts,” said Ben Jeffery, a fixed income strategist at BMO.“

Toward the latter portion of the press conference, Jerome Powell was offered the opportunity to clarify his comments and quell a certain level of fear in the markets by stating the following:

“Let me be clear: What I said was it’s not the beginning of a long series of rate cuts,” Powell said. “I didn’t say it’s just one or anything like that. When you think about rate-cutting cycles, they go on for a long time and the committee’s not seeing that. Not seeing us in that place. You would do that if you saw real economic weakness and you thought that the federal funds rate needed to be cut a lot. That’s not what we’re seeing.”

It’s not the first time Powell would find his verbiage objected to by investors and the markets and it likely won’t be the last. Powell, a highly intelligent man in many regards and agreed upon by many in the economists community, still has suffered from the shortcomings in messaging. His failures in messaging may be as simple as an internal belief that he’s saying what the markets want to hear, when the reality is to the contrary. Given the circumstances, this is not a messaging paradigm issue that can be remedied and as such the markets will simply need to adjust to the Fed and not the other way around.

When it was all said and done, it seemed as though the FOMC meeting event proved a failure. Finom Group looked upon the market’s reaction as a breeding ground of opportunity as the markets deeply desired a breather. Divergences overbought conditions abound and leading up to the FOMC meeting, a market drawdown was the most likely outcome regardless of what Fed chairman Powell was to say or not say. Additionally, while investors were panicked, to some degree on Wednesday, market breadth actually held up well; of course that’s not what you get from media headlines on a Fed day though. Nobody looks underneath the surface to talk about market breadth while the Dow, Nasdaq and S&P 500 are all falling greater than 1% on the day. What investors should have paid attention to was that small caps were outperforming going into and through the FOMC meeting.

The stock market’s breadth remained positive on Wednesday, helped by strength in small-cap stocks. The number of advancing stock outnumbered decliners 1,540 to 1,333 on the NYSE and 1,610 to 1,331 on the Nasdaq exchange. Where breadth data showed some weakness was in the larger, more active stocks, as volume of advancing stocks represented just 45.2% of total volume on the Big Board and 36.7% of total volume on the Nasdaq.

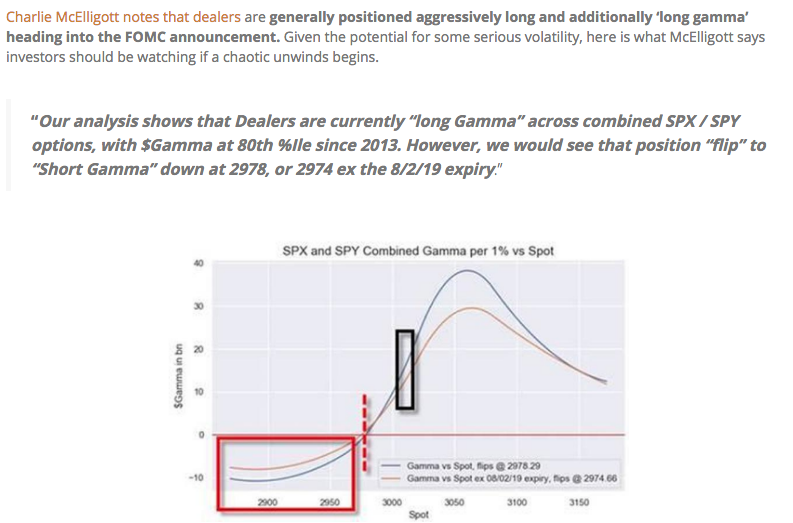

Alongside the positive breadth indicator on Wednesday, we also remind our Finom Group readers of what was offered by Nomura’s strategist Charles McElligott just yesterday, some key levels to watch for in the S&P 500.

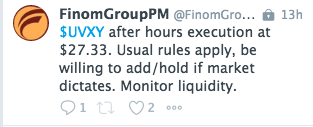

The S&P 500 defended, successfully, that 2,978- 2,974 level and managed to close above it at 2,980. Combining the positive breadth and closing above key gamma exposure/pivot levels, Finom Group offered the following trade idea after the closing bell (after hours trading).

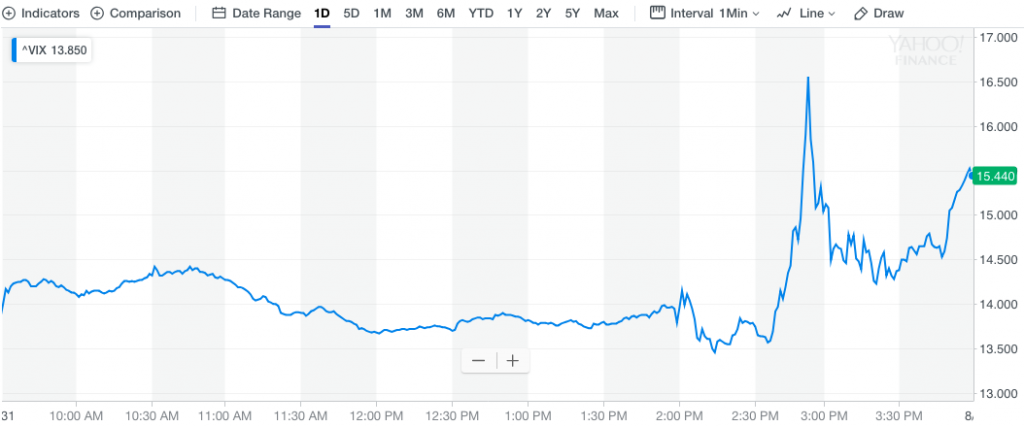

With the markets reeling from Powell’s missteps in messaging on Wednesday, volatility certainly took another leg higher. The VIX had already climbed some 18% in the first two trading days of the week, leading into the FOMC meeting and once Powell began speaking…

While many were expressing disappointment in the FOMC/Powell Wednesday, including President Donald Trump, Finom Group is of the opinion that another rate cut will be found in 2019. We anticipate at least one more rate cut, depending on the efficacy of the already issued easing. The Fed’s price stability mandate/inflation remains under pressure and is unlikely to see meaningful relief without asset price inflation and improved economic growth. Wage inflation has not proven enough to stimulate broader inflation in the economy to-date, despite the many economists’ belief it would.

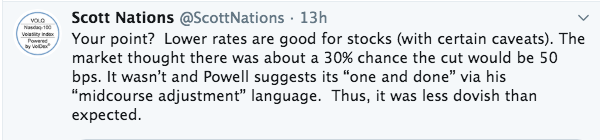

“At the end of the day”, we see opportunity in the rate cut for equity investors over time. Scott Nations, President of Nations Indexes Nations.com, creator of VolDex (ticker VOLI), CNBC Contributor and author of “History of US in Five Crashes”, represents our perceptions of rate cuts in the following tweet on Wednesday:

Lower rates/yields support equity/riskier assets. It’s just that simple although investors, for whatever reason, desire to make issues of investing principles more complicated than they actually need to be. Josh Brown, CEO of Ritholtz Wealth Management, told investors to “relax,” referencing a moment over two decades ago that reminded him of this one. Here’s what Brown offered on Wednesday on CNBC’s Closing Bell:

“Dow Jones Industrial Average] triggered down 400 and change? I looked at the stocks that had big beats on earnings last week, and I wanted to see if those gaps would hold, and they did. The big companies that had a lot of good results, you didn’t see selling there. So, it was an index thing, it wasn’t an investor thing. … It’s algorithm. That’s OK. We’ve come to expect that. That’s 90% of trading now. … 100% [I would be a buyer on weakness], because [Powell]‘s saying two things: he’s saying it’s midcycle, it could be one-and-done, but then maybe it’s not. That’s what he should say. I’m not a fan of the press conference anyway. I think it’s unnecessary. He says one remark that he didn’t say last time and then we pin him down to that until the next meeting. So, I wish they weren’t doing it. In my day, we had a briefcase with papers falling out of it and we loved it. It was good enough. So, in this case, he’s saying both things, and that’s what he should do. … If you’re going to be data dependent, we don’t have data in October yet, so why should he telegraph what he will do? He’s saying what he could do. Perfectly rational. And the one last thing I want to point out: there’s precedent for this. We’ve talked about it on this show in recent weeks. In 1995, they had to give back what they took away in ’94. [Former Fed Chairman Alan] Greenspan shocked the bond market in ‘94. The S&P [500] did a quick 18% swan-dive, totally unprepared for this overnight hike. And then, in mid-’95, right around a period like this in the summer, they had to give it back. And you know what? We had four more years of economic expansion, four-and-a-half more years of a bull market for stocks. And so why does he have to tell you what he’s going to do in December? Let’s see what’s going on. Maybe the missiles are in the air in trade terms, or maybe we’ve resolved it. Why do we have to have the answer today? Everyone needs to relax. Buy your favorite name. ”

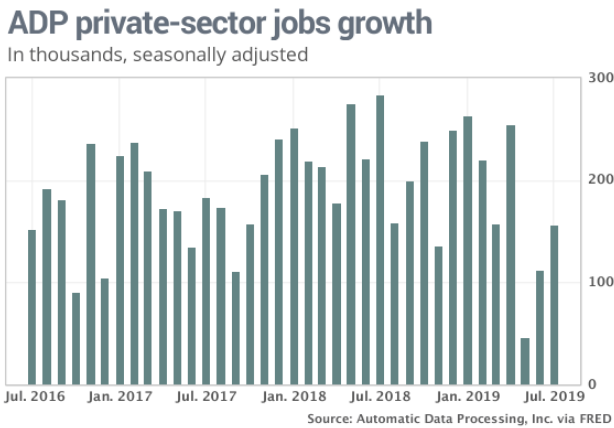

And now it is Thursday and the markets have already achieved the weekly expected move in the S&P 500. The weekly expected move this week was/is $38/points. The remainder of the week is now wide open for risk premium as two key points of economic data will be delivered on Thursday and Friday. Wednesday’s ADP private sector payroll report proved to beat economists’ estimates slightly.

The nation’s businesses created 156,000 private-sector jobs in July, payroll processor ADP said Wednesday. Some 112,000 private-sector jobs were added in June, according to revised figures. ADP originally put the increase at a seasonally adjusted 102,000.

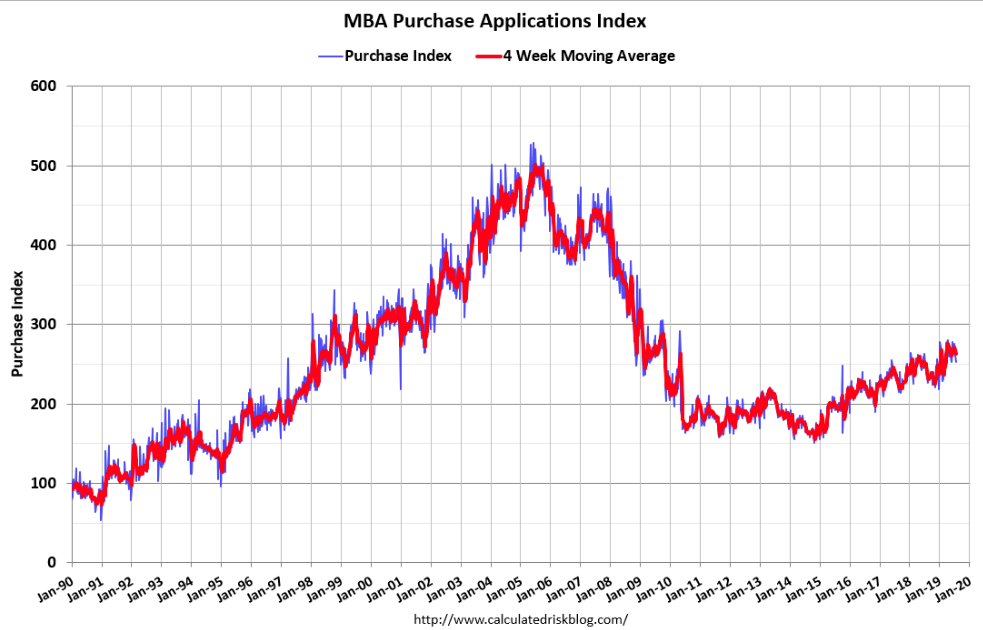

In addition to a better than expected ADP result for the month of June, mortgage application data proved to grow YoY and remain at cyclical highs.

- Overall volume for mortgage applications fell 1.4% last week from the previous week, according to the Mortgage Bankers Association.

- Volume was still 35% higher than a year ago, when interest rates were significantly higher.

- Mortgage applications to purchase a home fell 3% for the week but were 6% higher than one year ago.

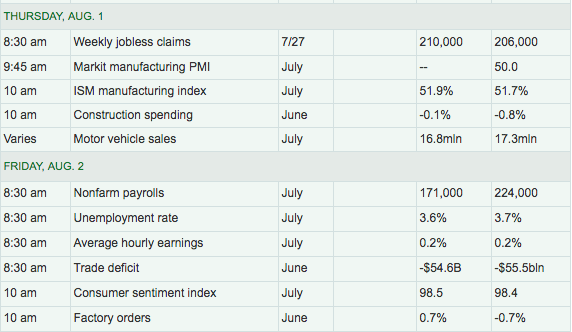

After Wednesday release of the dour Richmond Fed manufacturing survey, investors will be keenly tuned into the July ISM manufacturing index when it is released at 10:00 a.m. EST. Economists are forecasting a slight uptick in the sentiment-driven survey, which remains to be seen. In addition to the latest ISM reading, motor vehicle sales and Initial Jobless Claims will be released Thursday and ahead of Friday’s all-important Nonfarm Payroll data.

With U.S. economic data now moving to the forefront, investors are also digesting better than forecasted results from China’s factory activity. China’s factories showed signs of recovery in July though it continued to contract, a private gauge indicated. The Caixin China manufacturing purchasing managers index rose to 49.9 in July, compared with 49.4 in June, Caixin Media Co. and research firm Markit said Thursday.

The output and new order subindexes returned to expansion territory in July. The new export subindex rose slightly but remained in contraction territory. The subindex for employment fell further into negative territory, suggesting that China’s labor market showed no signs of improvement.

“China’s manufacturing economy showed signs of recovery in July,” Zhengsheng Zhong, an economist at CEBM Group, said in a statement accompanying Thursday’s release.

Mr. Zhong said policies such as tax and fee reductions, designed to underpin the economy, started to show effect.

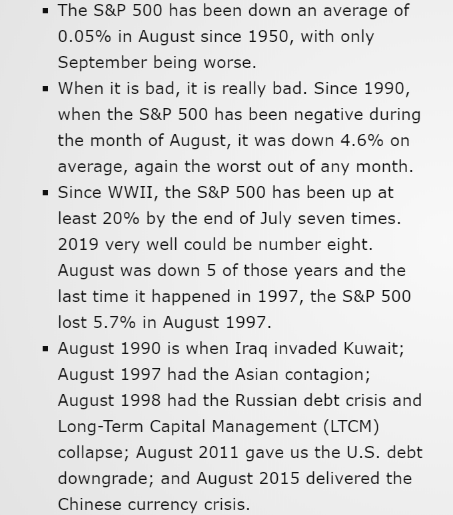

European markets are responding favorably to the FOMC easing, in early trade Thursday, which is also finding U.S. equity futures higher. Having said that, here are some key points to consider given the month of August and as offered by LPL Financial’s Ryan Detrick:

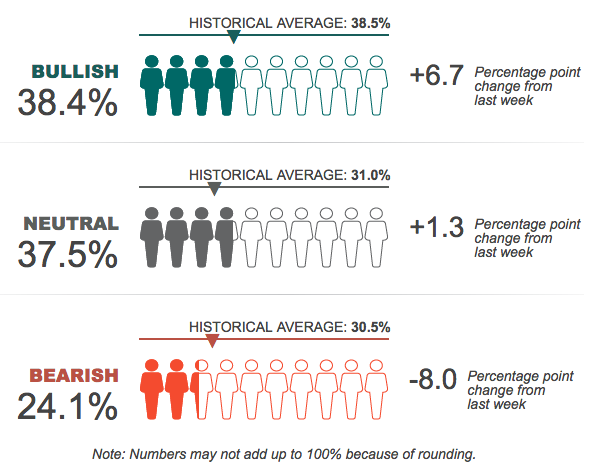

August can certainly be a rough month for risk assets and the equity markets will likely need bond market confirmation of positive sentiment belief in the easing cycle just commenced. With that being offered, equity market sentiment according to the latest AAII survey suggests bullish sentiment continues to improve, but remains below the historic average.

As we conclude today’s daily market dispatch we have a couple of final points to offer regarding the FOMC easing and end to the balance sheet run-off (ending earlier than forecasted).

- The Fed stated that despite what is occurring outside the U.S., resulting in slower global growth, the U.S. economic outlook remained unchanged. There was no deterioration in the economic outlook whatsoever.

- Lower rates serve as a measure of economic stimulus and support riskier asset price appreciation and favor multiple expansion.

In congruence with Finom Group’s emphasized bulletpoints, Yousef Abbasi, director of U.S. institutional equities and global market strategist at INTL FCStone, said the decision to cut rates “could give you more volatility in the coming days, but as we settle into August you’ll see equities start to perk again.”

“My assumption is that we could start to see a buy-the-dip mentality, created by the easy money move and the need to chase returns.

Mike Loewengart, vice president of investment strategy at E-trade also exampled the positive sentiment for risk assets based on the Fed’s easing in the following statement issued note to clients:

“The biggest surprise here is what’s not being said. There is nothing in the statement about growth cooling here at home. Despite the market’s short-term disappointment with the magnitude of the easing action, investors should consider low rates the new normal for the considerable future.”