Ahead of Apple’s (AAPL) earnings results and the FOMC rate announcement, troubling Brexit concerns mounted on Tuesday and found the Eurozone indices tumbling. The German (DAX) led the way lower, down more than 2% on the day. The Eurozone equity sentiment found its way into the U.S. equity markets, resulting in a sharp move lower for all 3 major indices. Shortly after the European close, however, U.S. stocks made an afternoon rally, but still finishing in the red.

The media blamed much of yesterday’s early market declines on President Donald Trumps comments about China’s stalling technique when it comes to trade. As U.S. Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin landed in Shanghai on Tuesday, Trump accused Beijing on Twitter of stalling, and warned of a worse outcome for China if it continued to do so.

As talks were just beginning on Tuesday, Trump said on Twitter that China appeared to be backing off on a pledge to buy U.S. farm goods, and he warned that if China stalled negotiations in the hope that he wouldn’t win re-election in the November 2020 U.S. presidential contest, the outcome will be worse for China.

“The problem with them waiting … is that if & when I win, the deal that they get will be much tougher than what we are negotiating now … or no deal at all.”

As it pertains to U.S./China trade talks, Goldman Sachs offers their best case as follws (odds: 10%):

- A joint communique is published with the two sides agreeing on specific language concerning the contours of the economic relationship. China commits to make changes to certain laws aimed at placating US demands (this issue of changing local laws seems to be the key sticking point). Trump permanently removes the threat of incremental tariffs ($300B/25%) and suggests some (or all) of the existing ones could be rescinded. China ramps US agricultural purchases and the US Commerce Department hands out large Huawei waivers.

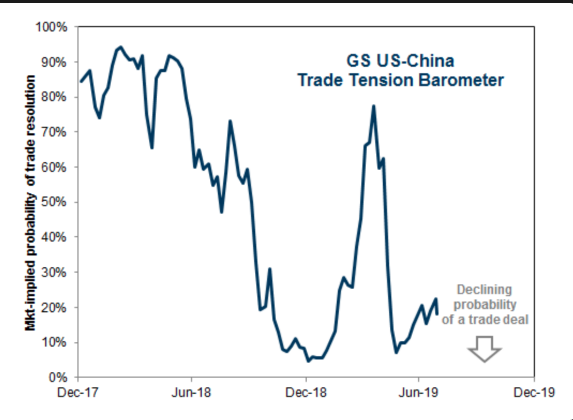

The good news, in this elongated trade dispute between the U.S. and China may be expectations. As Goldman Sachs denotes in the following chart, a deal is no longer seen as the likely outcome:

The reality is that the U.S. equity market futures were already in the red before President Donald Trump aired his discontent with the trade talks and tactics used by Chinese officials. As such, we point the finger at Boris Johnson and the continued Brexit saga.

Boris Johnson has said it is up to the EU to compromise to avoid a no-deal Brexit, after his demands for the backstop to be scrapped were met with a flat refusal from the Irish taoiseach, Leo Varadkar.

In comments that showed he is preparing to blame the EU if the UK ends up leaving without a deal, Johnson said he was not aiming for a no-deal Brexit but the situation was “very much up to our friends and partners across the Channel”.

“They know that three times the House of Commons has thrown out that backstop, there’s no way that we can get it through, we have to have that backstop out of the deal, we cannot go on with the withdrawal agreement as it currently is,” he said.

“If they understand that then I think we are going to be at the races. If they can’t compromise, if they really can’t do it, then clearly we have to get ready for a no-deal exit.”

He said it was “up to the EU, this is their call if they want us to do this” but “unless we are determined to do it they won’t take us seriously in the course of the negotiations”.

This is what tends to happen when the markets have rallied over an elongated period of time and suddenly show signs of weakness. The media looks for a story to assign blame and highlight causation. And with a 7-month long S&P 500 rally, which has boosted the benchmark index over 20% in 2019, the stories are easy to find and fingers are easily pointing to blame in what has been a widely despised rally.

Heading into the final trading day of July, we reflect on the S&P 500’s year-to-date performance as well as what may lay in store for investors in August. While June is typically the worst month of the year over the last 10 years, it proved to be one of the strongest this year. As such, it was only natural to believe that July would also prove contrarian to its historically strong performance. But that hasn’t come to pass. The S&P 500 is up some 2.5% in July and ahead of the FOMC rate announcement on Wednesday afternoon.

Only 7 times since WWII has the S&P 500 been up more than 20% at the end of July. August has been down 5 of those years and the last time it happened (1997), the S&P 500 was down 5.7% in August. It’s worth considering, especially if something goes awry with Wednesday’s FOMC event that culminates with Fed chairman Jerome Powell’s press conference.

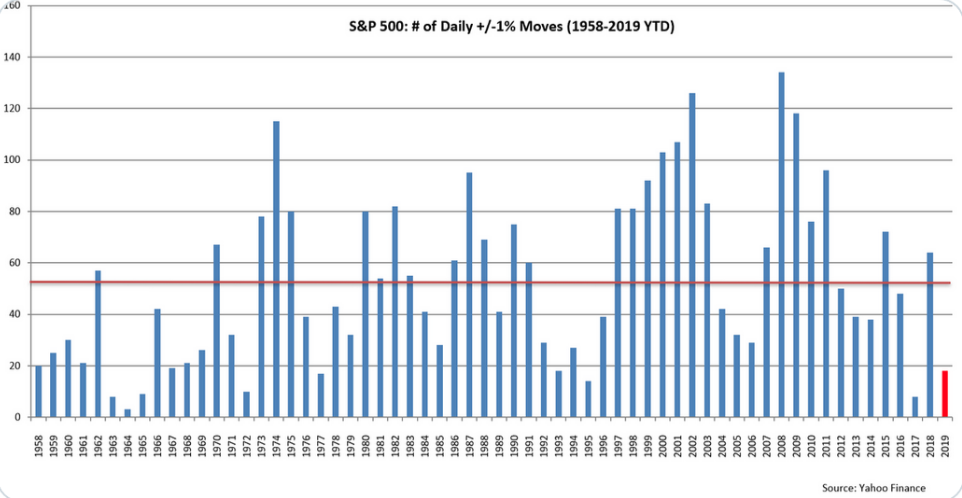

As investors await the FOMC on Wednesday afternoon, hedging activity has proliferated and the VIX has jumped nearly 18% in just the first two trading days of the week. Nonetheless, this hasn’t produced a 1% daily move in the S&P 500 with the VIX still residing under 16. In fact, the S&P 500 has not had a daily return of plus or minus +1% in over 7 weeks. That’s highly unusual, as the S&P has typically had one 1% day/week on average over the last 60 years.

It’s been two months since a fall of more than 2% and even the 2013-14 period, during which S&P 500 rose more than 50%, those years saw drops of 3% or more 11 times, or every other month on average.

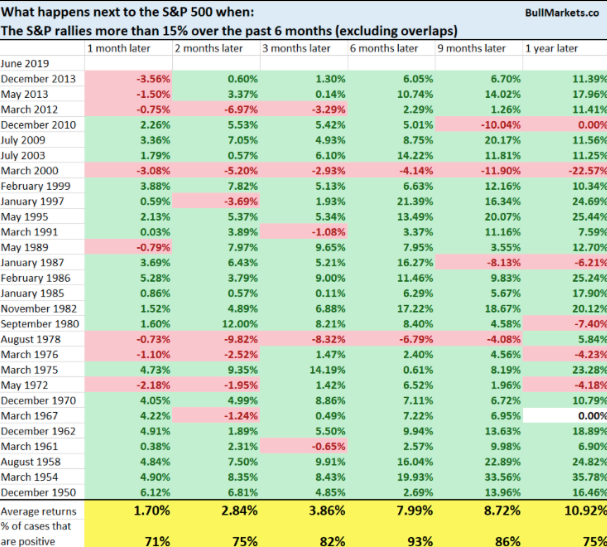

Moreover, since 1950, any 6 month rally that carries the S&P 500 at least 15% higher has been followed by further gains (of 8% on average) the next 6 months 93% of the time (from Troy Bombardia).

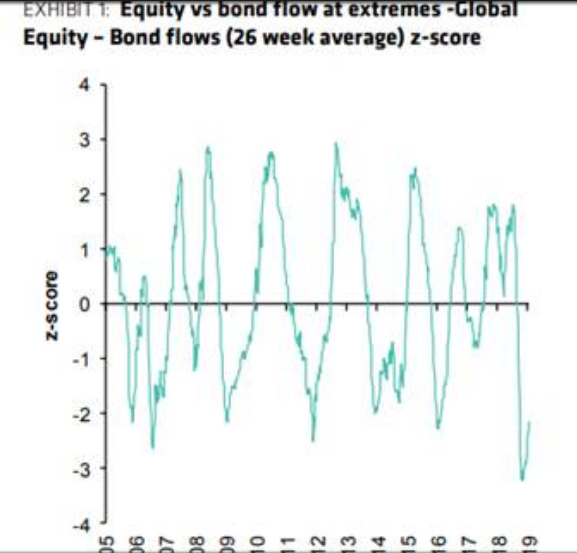

Undoubtedly, this has been one of the most unloved, unforeseen and underfunded rallies in U.S. equity market history. The market’s rally this year has found $150bn outflow from global equities. The U.S. accounts for the bulk of outflows. So far this year, a net outflow of -$93.1b (Lipper) has been accumulated in the United States and Bernsten Strategist believes there is potential for an inflow into equities in the coming months that would provide a cushion for the market.

While we could quite literally talks stats on the market all day, looking at various indicators, historic data and the like, the fundamental outlook for the market remains bullish. The reason for this is largely due to the strength of the U.S. economy that feeds through to earnings over time. While it can be said that the global and domestic economies are weakening YoY, most regions of the industrialized world remain in expansion territory.

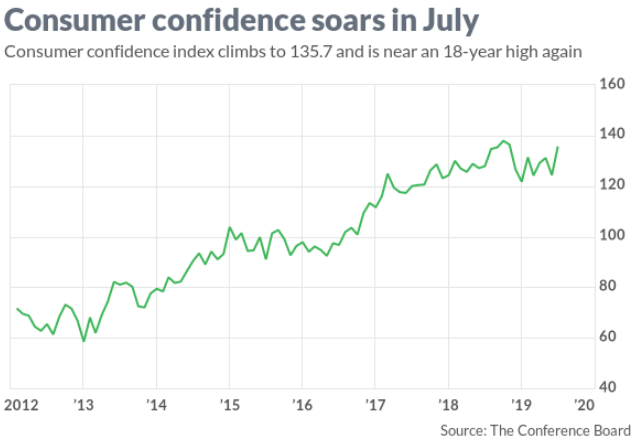

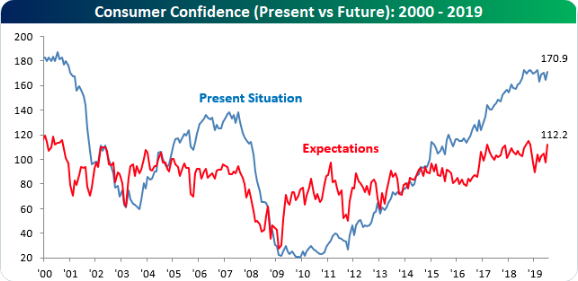

Certain of the economic data released on Tuesday identified better than expected economic conditions in the United States. The consumer confidence index jumped to 135.7 in July from a revised 124.3 in June, the Conference Board said Tuesday.

The present situation index, a measure of how consumers view the economy right now, rose to 170.9 from 164.3. Another index that looks out over the next six months also advanced. Both indexes are near the highest levels of the current economic expansion that began in mid-2009.

“Consumers are once again optimistic about current and prospective business and labor market conditions,” said Lynn Franco, director of economic indicators at board. “These high levels of confidence should continue to support robust spending in the near-term despite slower growth in GDP.”

As we’ve seen in the June retail sales data, the consumer continues to remain quite healthy, spurring consumer spending growth YoY and MoM. Consumer spending rose 0.3% last month, the government said Tuesday, matching the forecast of economists polled by MarketWatch.

Consumer spending habits have been supported by growing incomes. Personal income rose by 0.4% for the fourth month in a row and revised figures show the gains in the first quarter were even stronger than originally reported. The savings rate edged up to 8.1% from 8%, keeping them near a three-year high.

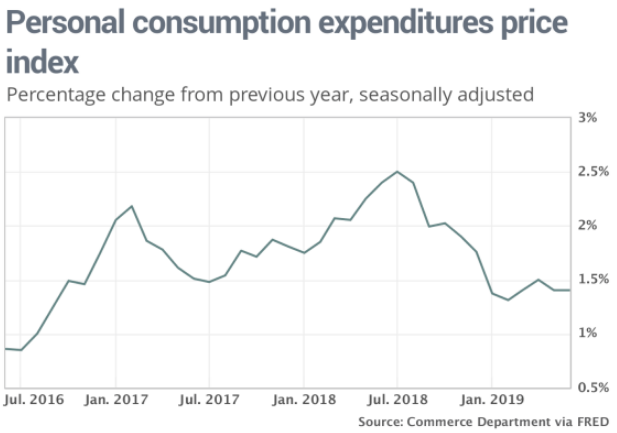

The PCE inflation gauge that’s closely watched by the Federal Reserve, meanwhile, rose a scant 0.1% in the month, leaving the increase over the past year unchanged at 1.4 percent. That’s well below the Fed’s 2% target.

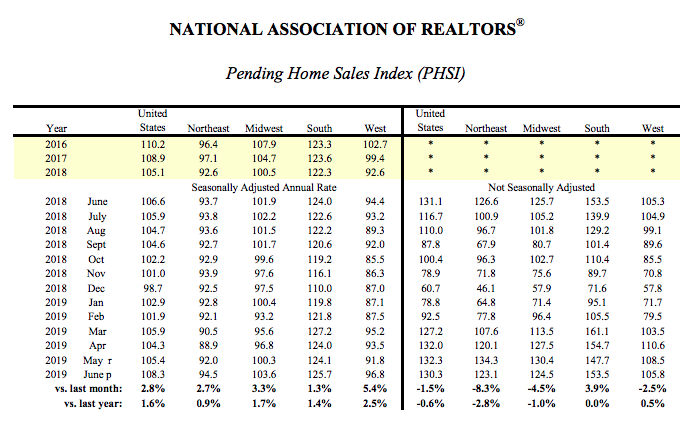

Alongside weaker inflation and an ebullient consumer spending environment, Pending home sales also put in a solid result in the month of June. The National Association of Realtors said pending home sales climbed 2.8%, with gains in each of the four major regions, including a 5.4% jump in the West. Compared to 12 months ago, sales rose 1.6%, the first year-over-year gain in 17 months.

In addition to the stronger than anticipated economic data with limited inflation potential proving the Fed’s easing cycle afoot, economic data out of Germany followed suit on Wednesday. While the German economy has been sputtering lower in 2019, its consumer has proven the likeness of the U.S. consumer and keeping the economy with modest growth.

German retail sales rose more than expected in June, posting their steepest monthly increase in more than 12 years, data showed on Wednesday, offering a rare beam of hope that household spending will prop up Europe’s largest economy.

The German economy has been relying on private consumption and construction for growth, a cycle supported by a solid labor market, record-low interest rates and rising wages. Nonetheless, economic output is expected to shrink in the second quarter.

retail sales were up by 3.5% on the month in real terms after a revised 1.7% drop the previous month, data from the Federal Statistics Office showed. This was the highest monthly increase since December 2006 and easily beat a Reuters forecast of 0.5 percent.

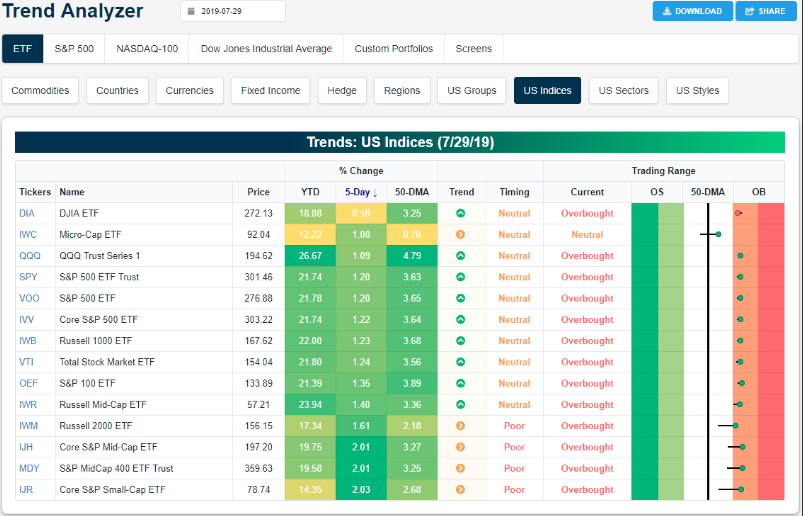

U.S. equity indices rallied into the closing bell and ahead of Apple’s earnings release on Tuesday, but still finished in the red for the trading day. Although the S&P 500 and Nasdaq (NDX) have expressed two negative days in a row, most of the index ETFs remain in overbought territory and above their respective 50-DMAs. (Table from Bespoke Investment Group)

After the closing bell on Tuesday, Apple reported results that beat analysts’ estimates. Here’s how the company did versus what analysts were expecting:

- EPS: $2.18 vs. $2.10 estimated by Refinitiv consensus estimates.

- Revenue: $53.8 billion vs.$53.39B estimated by Refinitiv consensus estimates.

- Q4 revenue guidance: $61 billion to $64 billion versus$60.98 billion estimate by Refinitiv consensus estimates.

- iPhone revenue: $25.99 billion vs. $26.31 billion estimated by FactSet.

- Services revenue: $11.46 billion vs. $11.61 billion estimated by FactSet.

Apple’s revenue was up 1% from the year-ago quarter. Earnings per share were down 7%.

“Great services quarter, unbelievable wearables quarter, significant progress on iPhone, and off-the-charts significant progress on China, compared to where we were the previous quarter,” said Tim.”

Apple said that it had spent over $17 billion on share buybacks of almost 88 million Apple shares, and had also paid out $3.6 billion in dividends and equivalents during the quarter.

“The highlight of this release and focus of investors in our opinion will be the robust September guidance for total revenue of between $61 billion and $64 billion vs. the Street’s $60.9 billion estimate,” Wedbush analyst Dan Ives said in a note.“

Here is what Goldman Sachs had to say about Apple’s results and commentary shortly after the release:

- We are increasing our FY20 revenue estimate by 0.6% to $268bn, but our EBIT declines by 2% due to higher opex as we reflect higher-than-expected FQ4 OpEx guidance in our estimates going forward

- Our 12-month price target moves up to $191 (from $187) as we roll forward our NTM multiple to include September ’19 through June ’20 quarters.

- We continue to see risk to consensus expectations for FQ1’20 to December and suspect that the short term risk on Services is to the downside but supporting data on this is unlikely to materialize until we start getting more clarity on iPhone sales in October/November.

- we believe Apple is exposed to trade newsflow volatility and that the stock is fully valued

- Reiterate Neutral.

Here is what J.P. Morgan Chase had to say about Apple’s earnings results and commentary after the release:

- We see further upside to investor expectations moving into 2020, led by a strong product cycle

- The ramp of a slew of new Services launching later this year is the key reasons to own the stock over the next 12 months in our view.

- We are raising our EPS forecasts to $13.25 (vs. $13.00 prior) for FY20E and $15.45 (vs. $15.30 prior) for FY21E, both materially above consensus expectations

- We are raising our Dec-19 price target to $243 vs. $239 prior, as we continue to see opportunities for further upside to investor expectations

With shares of Apple up roughly 4% in the premarket on Wednesday, equity futures look to open in the green and ahead of the FOMC rate announcement that is likely to dictate the outcome for the markets on Wednesday. According to Goldman Sachs the outcome for the markets depends on how the Fed guides investors regarding the future outlook for monetary policy.

“Good case (odds: 20%) – the Fed cuts the FF and IOER rates by 25bp and concludes the balance sheet run-off process (which is 6 weeks earlier than previously scheduled). The statement stays largely the same as before. Powell doesn’t use the word patient and signals at least one additional 25bp cut this year. His emphasis during the press conf. isn’t just on “insurance” but also disinflationary headwinds, a flat yield curve, and ongoing int’l pressures. Powell doesn’t shy away from balance sheet questions and says this very much remains a key component of the policy toolkit (and hints the balance sheet could be utilized even before the FF returns to zero). No one dissents.

Best case (odds: 10%) – everything in the “good case” except the Fed cuts rates 50bp.”

The likelihood of a cut of some magnitude is statistical very high, with the only key unknown remaining as to how the stock market might react to the 2 p.m. Eastern Time policy decision and the following Q&A hosted by Federal Open Market Committee Chairman Jerome Powell.

Jerome Powell has a losing record on Wall Street as it pertains to the market’s reaction to statements and his words. He has had two winning days out of the past 11 meetings, with the only positive gains for the market coming in January when policy makers paused a string of rate increases and last month when Powell & Co. set the stage for what is shaping up to be a likely rate cut in 24 hours,

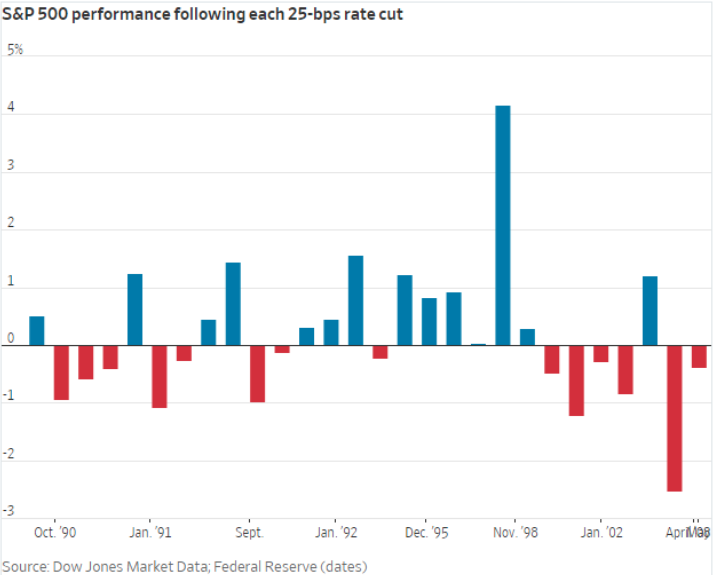

Markets tend to rally after rate cuts because those policy actions translate into lower borrowing costs for individuals and corporations and tend to support higher moves for stocks.

Since 1990, the S&P 500 has gained on average 0.16% on the day of a 25-basis-point cut. One-month later, the broad-market benchmark is 0.57% higher. Double that cut and the market is 0.34% higher on the of the decision day and 1.25% higher a month later. But what if the market starts to sell-off during and/or after the FOMC rate announcement on Wednesday?

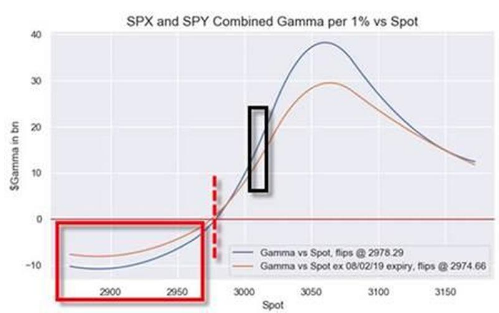

Charlie McElligott notes that dealers are generally positioned aggressively long and additionally ‘long gamma’ heading into the FOMC announcement. Given the potential for some serious volatility, here is what McElligott says investors should be watching if a chaotic unwinds begins.

“Our analysis shows that Dealers are currently “long Gamma” across combined SPX / SPY options, with $Gamma at 80th %Ile since 2013. However, we would see that position “flip” to “Short Gamma” down at 2978, or 2974 ex the 8/2/19 expiry.”

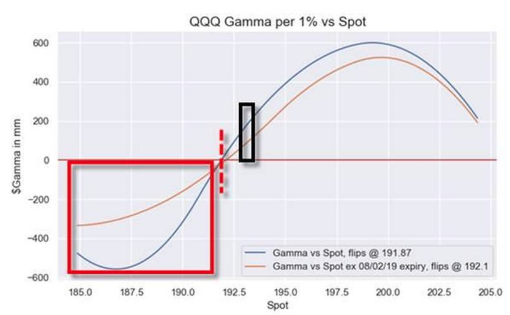

Also worth noting is the VERY long positioning in crowded Nasdaq. This leaves QQQ too nearing a flip from current Dealer “Long Gamma” positioning to the “Short Gamma” flip-zone at 191.87 / 192.10 (ex 8/2/19 expiry).

While ADP private sector payroll data is due out at 8:15 a.m. EST on Wednesday and may point to weakening or strengthening labor market conditions, investors will remain focused on the afternoon FOMC event. We expect fireworks that will move markets here in the U.S. as well as Asia, in the overnight session.