Bear with us…! Asian equity markets had the first opportunity to react to headlines from the United States whereby two of President Donald Trump’s confidants and one-time employees will be sentenced for crimes. While most major Asian markets finished higher overnight and European markets are flat to slightly higher in the early hours on Wednesday, U.S. equity futures are modestly lower ahead of the market’s open.

Former Trump campaign chairman Paul Manafort late Tuesday was found guilty on eight charges including tax fraud, and the president’s former lawyer Michael Cohen said he violated campaign-finance law at President Donald Trump’s direction. The news broke slowly around 2:30 p.m. EST on Tuesday and after the S&P 500 surpassed its former record high to set a new all-time high level. All three major indices finished higher on Tuesday, but well off their trading highs as the news surrounding the Manafort verdict and Cohen plea deal managed their way into the media headlines. For certain, the news cycle will impact the market if not volatility in the market on Wednesday, for better or for worse.

In terms of economic data on tap Wednesday, a July report on existing-home sales is slated to hit at 10 a.m. Eastern Time. Economists polled by MarketWatch forecasting a seasonally adjusted annual rate of 5.40 million homes. Additionally, the minutes from the Federal Reserve’s last meeting are slated to be released at 2 p.m. Eastern, and they will be combed over for insight into what the Fed sees as potential problem spots for the economy that may lay ahead.

Two themes are going to dominate trading today… possibly and as earning season winds down. Least we not forget the strong retail sector earnings that have been rolled out last week and to date with Kohl’s (KSS) beating Q2 2018 analysts’ estimates and raising its FY18 guidance on Tuesday. Before the opening bell on Wednesday, Target Corp. (TGT) will report its Q2 2018 results. But the two themes of the day will center on President Trump’s dealings with Michael Cohen and the “record setting bull market” rally.

Every single day and as the S&P 500 edged toward a record high, permabear market participants and economists have suggested the market crash is imminent and the bull market is extended in both value and lifespan. It’s a drumbeat of the permabears that beats loudly in social media and even within the offices of many prominent fund managers.

Ed Yardeni published a fantastic video detailing why the longevity of a bull market has no relevance on its potential to turn into a bear market.

- Records are made to be broken. Bull markets and economic expansions don’t die of old age; the same way humans don’t have a “die by age XYZ” date. Bull markets, like humans, don’t have an expiration date.

- This is the longest bull market in history (based on conventional measures) simply because this will soon be the longest economic expansion in history.

- Permabears stomp there feet about national debt, consumer debt and corporate debt, but debt doesn’t cause a bear market. At best, debt can amplify the effects of bear market, but causation it cannot provide.

- The economy is simply too strong to reverse course all of a sudden and subsequently reverse the trend in corporate earnings.

Look, we’re terribly sorry to have disappointed market pundits and permabears since the market corrected back in February, but logic and reason don’t typically disappoint. What does disappoint is fear mongering without a fundamental, logical and rational thesis for the market that is rooted in facts and possibly supported by history. Even historic precedence may be found with error from time to time and given the unique circumstances that admittedly have provided this bull market and economic expansion with a “second wind”. But just for the sake of argument let’s look at history and what might happen to the S&P 500 after achieving a new all-time high.

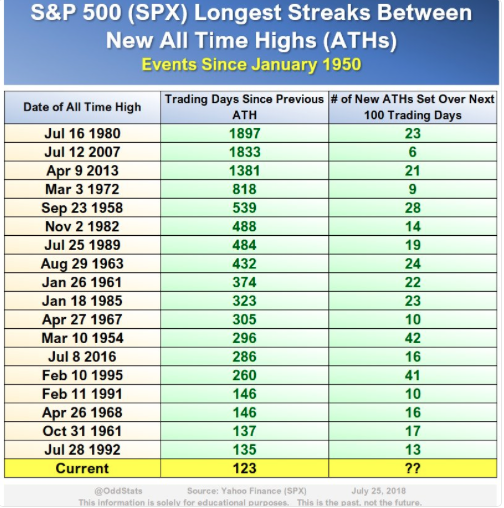

Firstly, no! Just because a new all-time high has just been achieved, this does not mean the market will suddenly make a U-turn and “crash”. This is purely nonsensical sentiment and forecasting. Here’s every time period between new ATHs longer than the current. You can see a new ATH after that much time off has been followed by many more in the next 100 days.

These are historical facts for which drawing and going forward may find the market still yet with room to run. Nonetheless and even with historical facts, permabears like David Stockman promote “imminent market crash” is upon us. Just a few days ago and as the media ramped up the rhetoric surrounding the record-breaking bull market, Stockman offered the following permabear sentiment.

These are historical facts for which drawing and going forward may find the market still yet with room to run. Nonetheless and even with historical facts, permabears like David Stockman promote “imminent market crash” is upon us. Just a few days ago and as the media ramped up the rhetoric surrounding the record-breaking bull market, Stockman offered the following permabear sentiment.

“This economy isn’t strong, and it can’t take the punishment that’s coming out of an unhinged White House and a Washington policy environment where they all have their heads in the sand,” Stockman said Thursday on CNBC’s “Futures Now.”

The reality of David Stockman’s forecasting and rants is that one day, one day he will be right. In fact, Stockman has predicted 50 of the last 1 stock market crashes, which basically means he predicts 99% of the market crashes that never come to be. Take a look at some of these by date over the last few years:

- 2010: David Stockman: I Invest In Anything Bernanke Can’t Destroy

- 2012: DAVID STOCKMAN: You’d Be A Fool To Hold Anything But Cash Now

- 2015: Stocks are a ‘disaster waiting to happen’: Stockman

- 2016: David Stockman warns both Trump and Clinton could lead to 25% sell-off

Year after year after year after year after year does Stockman promote and forecast the demise of the market. Eventually and as long as he maintains this forecast, he’ll look like a genius. More importantly, investors should better understand that his forecasts aren’t rooted in what drives markets over time, earnings! Since 2010 and Stockman’s “stay away from assets Bernanke manipulates” argument, the S&P 500 is 141% higher. Can you imagine being fearful of the market for some 8 years?

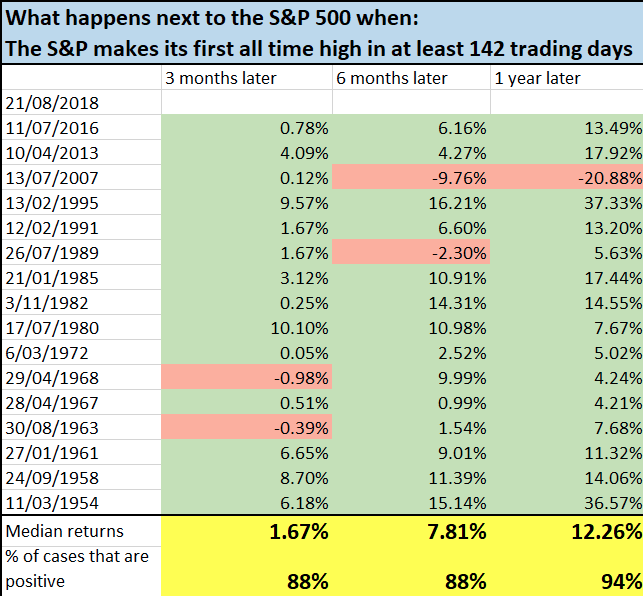

2018 is a year unlike 2017 or any other. The absolute chaos surrounding not just the White House, but the geo-political community of issues and agendas is unprecedented. While we look at history to provide some guidance, we must remain cognizant of the fact that unique conditions warrant unique perspective and an open mind. With that being said, and again, let’s look back at history for some semblance of what we can expect in terms of net returns from the S&P 500 after the benchmark achieves a new ATH after a period of 142 days.

It’s not a bad forecast for the S&P 500 returns going forward using history now is it? With the facts in hand, this does not exonerate the possibility of some level of intermittent market correction from fear driven geopolitical issues or other variables of consequence.

The problem with history is that it’s not always a proven, reliable guide. Having said that, many still rely on history without fear of consequences from unique and new factors in the economy or financial markets. Some well-regarded fund managers never change their investing and analytical styles. They see every economic cycle and market cycle through the same lens. Just ask Janus Henderson bond fund manager Bill Gross.

Unfortunately, Bill Gross isn’t likely going to take your calls. Bill Gross’s signature fund at Janus Henderson has shed more than 40% of its assets, in a humbling period of redemptions and wrong-way bets for the fixed-income “genius”. The losing stretch for the 74-year-old Gross comes amid bets on U.S. Treasurys and German bunds, among other assets, that haven’t quite panned out for the bond pro. Gross has wagered that the yield spread between 10-year Treasury notes and comparable German bunds would converge, but that has failed to pan out. Gross’s unsightly performance has elicited a less-than-ringing endorsement from his boss, Janus Henderson CEO Richard Weil, who last week told CNBC during an interview that the investment manager had been “wrong and wrong badly.”

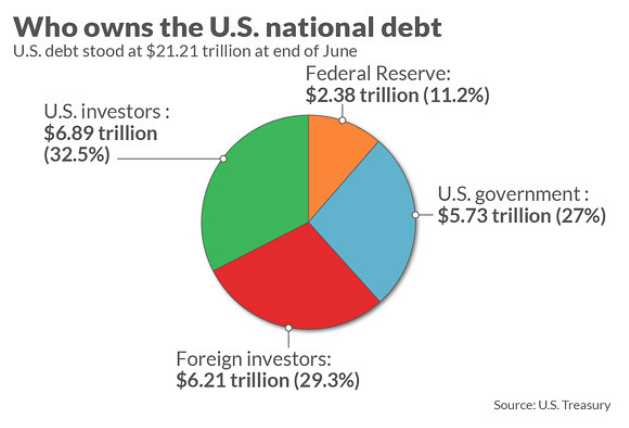

What this example from Bill Gross signifies is that relying on history doesn’t always pan out. U.S. treasury yield have risen, but have also seem to have hit a wall mid-year around the 3%, level. As the FOMC has been tightening and unwinding its balance sheet, the belief was that the selling pressure would be coupled with selling pressure from other entities, but the reality is that a 3% U.S. T-bill is still more attractive than sovereign debt offered by foreign countries. The Federal Reserve owned $2.38 trillion in debt, but it trimmed its holdings by $85 billion since June 2017. The Fed last year began to partly sell off its hoard of Treasurys. Russia has slashed its Treasury holdings to a mere $15 billion from a peak of $153 billion in mid-2013 amid worsening tensions with the United States. But it hasn’t been enough to keep debt investors away from U.S. Treasurys. Just who owns U.S. debt you might be asking. Well, it’s mostly owned by us, the U.S. citizen.

The bottom line with regards to the misanalysis and positioning by Bill Gross is that he failed to respect today’s global economic conditions and unique variables. In a manner of speaking, he bet against the U.S. to some degree. But enough about Gross and Stockman, let’s talk about U.S. corporate earnings through analysts’ expectations for Target’s Q2 2018 results.

FactSet expects earnings of $1.40 per share, up from $1.23 last year. Target missed earnings expectations that last two quarters, according to FactSet data. FactSet is guiding for revenue of $17.23 billion, up from $16.43 billion last year. FactSet is guiding for same-store sales growth of 4.1 percent. Shares of TGT are up sharply YTD, some 27% and up some 8% since last reporting Q1 2018 results.

“Wal-Mart’s results were also better than expected and the dollar growth was substantial, raising questions about balance of share versus consumer demand growth,” Credit Suisse wrote. “We think Target held its own. Wal-Mart’s strength (beyond season) seems to indicate a stronger consumer, perhaps even a stronger low-income consumer.”

Target shares have retraced gains in 4 of the last 5 reporting periods and on the day of reporting quarterly results. Having said that, the company and stock are set up nicely for a breakout, in kind with the breakout witnessed yesterday by T.J. Maxx (TJX). The company maintained its FY18 guidance after its Q1 2018 results and if Wal-Mart, Kohl’s (KSS) and Macy’s (M) Q2 reporting is any guide for Target, the company may be poised to report results ahead of analysts’ estimates and a boost to its FY18 guidance. Recall, it wasn’t until Q2 of 2017 that the company boosted its FY17 guidance.

It remains to be seen whether or not Target’s Q2 2018 results will support its share price performance of late and whether or not the market can look past political headlines. Again, if history is any guide, investors should remain optimistic!