We’ve reached the end of the week and what a week it has been. A couple of overextended streaks came to an end during the trading week, including a Dow and Financials Select Spiders ETF (XLF) losing streak. In our daily market dispatch yesterday morning, we discussed the potential for XLF going forward.

“While the XLF and individual big banks have seen significant share price erosion throughout June, there may be some help on the horizon. Banks are set to receive approval to deploy capital to investors on Thursday as a part of the second leg of its banking “stress tests”.

“Golden also believes one of the better buying opportunities in the market right now lay within the financials. For investors seeking diversity within the financial sector, the XLF may very well be the instrument to choose. Moreover, Golden also believes that while the technicals for the S&P 500 and Dow appear dangerous, that may prove to be a buy signal in hindsight and with corporate buybacks set to accelerate.”

Both the S&P 500 and XLF rose yesterday with the XLF ending a 13-day losing streak. With regards to the Fed’s stress test results and determinations, 35 banks were included in this year’s stress test and 18 of the biggest and most complex institutions had to go through both qualitative and quantitative parts of the exam. Of those, 15 firms were cleared by the Fed and will be allowed to proceed with their planned payouts, which could include hikes in dividends and buybacks.

As shown in the chart above, the XLF has traded below its 200-DMA recently, which tends to be a net negative near-term. But with the supportive conclusions of the stress test results and upcoming earnings-reporting season, such variables could turn the tide for the financial sector and XLF. Already, post the stress test results, the banks have responded with payout announcements as follows:

J.P. Morgan Chase & Co. said it will increase its quarterly dividend to 80 cents a share from 56 cents a share and buy back up to $20.7 billion in stock. American Express Co. will hike its quarterly dividend 11% to 39 cents a share and buy back up to $3.4 billion in shares. Citigroup Inc. said it will increase its quarterly dividend to 45 cents a share from 32 cents a share and buy back up to $17.6 billion in shares. Wells Fargo & Co. said it will increase its quarterly dividend to 43 cents from 39 cents a share and buy back up to $24.5 billion in stock. Bank of America Corp. said it will increase its quarterly dividend by 25% to 15 cents a share and buy back up to $20.6 billion in shares. Fifth Third Bancorp increased its quarterly dividend to 22 cents a share from 18 cents a share, and said it would buy back up to $1.65 billion in shares. Regions Financial Corp is hiking its quarterly dividend to 14 cents a share and buy back up to $2.03 billion in shares. Huntington Bancshares Inc. will hike its quarterly dividend 25% to 14 cents a share and announced up to $1.07 billion in buybacks. Capital One Financial Corp. will keep its quarterly dividend at 40 cents a share and buy back up to $1.2 billion in shares. KeyCorp hiked its quarterly dividend 42% to 17 cents a share and announced up to $1.23 billion in buybacks. State Street Corp. will raise its quarterly dividend to 47 cents from 42 cents a share and buy back up to $1.2 billion in stock. PNC Financial Services Group Inc. said it will hike its quarterly dividend by 27% to 95 cents a share and buy back up to $2 billion in stock.

With positive stress tests results now in the rear view mirror and with a turbulent week for the equity markets, we’ve come to the end of the trading week that is looking for a 2-day rally on Wall Street. Overnight, Asian markets were sharply higher and this has also poured over to the early hours of European trading. U.S. equity futures are responding positively to both global equities and the good news surrounding the financial sector. Thus far this week, the Dow is off 1.4%, the S&P has lost 1.6%, and the Nasdaq has lost 2.5 percent. For the second quarter, the Dow is up 0.5%, the S&P has gained 2.9%, and the Nasdaq is up 6.2 percent. For 2018, the Dow has lost 2%, the S&P has gained 1.6%, and the Nasdaq has surged 8.7 percent.

For Finom Group, it’s time to focus on a perspective/point we had offered a few weeks ago in an article titled Is a Recession Imminent? Market Colloquialisms Defined! The article’s main point was to contest the notion of the colloquialism “this time is different”. Within the article we defined the origin of that colloquialism and why it causes disdain when put forth or uttered.

“The reality is most market conditions and behaviors are ever different despite the disdain cast upon those who utter the words “this time is different”. This is because markets evolve, grow and adapt over time.”

What we determined in the article is that this time is different, but more importantly is that the markets are forced to differentiate from the past as they evolve. Now let’s explore why we revisit this perspective.

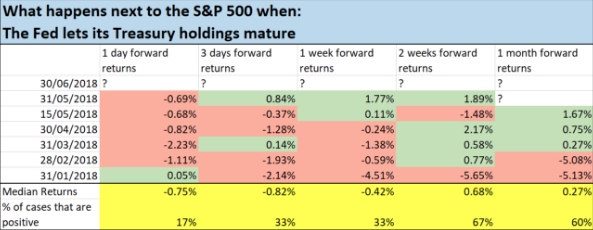

We know, accept and understand there has never been Quantitative Easing to the degree the Federal Reserve enacted, post the financial crisis. As such, we also know that there has never been the equivalent quantitative tapering and unwinding of the Fed’s balance sheet currently in process. It’s a very unique experience the markets are contending with and muddling through. This time is different and inarguably so. With that said, here is how the markets have responded on the day that the Fed reduces its balance sheet.

Pretty interesting, right? As we can see, the day the Fed tapers its balance sheet the stock market goes down the majority of the time. It doesn’t have a lasting affect either, as the market tends to snap back within a couple of weeks. The reason for this is that the Fed is tapering ever so slowly and in a manner so that it proves inconsequential to the market and economy. So while all those analysts are issuing warnings to the market and suggesting returns will decline as the Fed tightens and tapers, there’s still no real validation in the markets for such warnings.

So why are we highlighting the Fed tapering and market reaction now? Well, the next taper is scheduled for Saturday, June 30, which will impact the stock market on Monday, July 2. Maybe we should rather say that is the first opportunity the market will have to respond to the tapering. We don’t know how the market will respond; all we have is the most recent historic depiction of how the market has responded thus far. The trending response has not been positive initially, that we know.

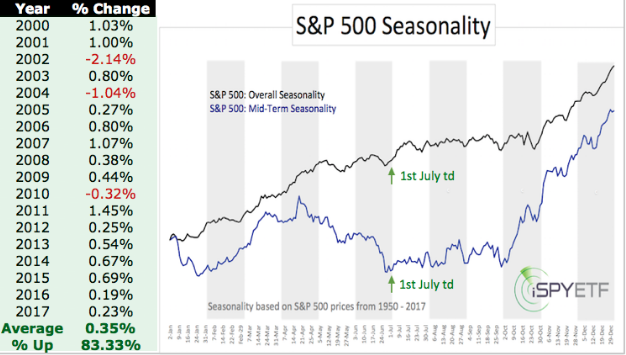

Ok, so here’s the contesting point regarding the tapering schedule that results in a 75% lose rate for the stock market the day of tapering correlated to the July 2nd date. It’s really a binary dynamic, which has no historic precedence. The most bullish S&P 500 trading day of the year, since the new century is (drum roll please)…. that’s right, July 2.

- When: First trading day of July (in 2018, that’s July 2)

- Average return: 0.35%

- Win rate: 83.33%

The win rate for the Dow Jones Industrial Average is 77.77%. The win rate for the Nasdaq is 72.22 percent. So you see the problem with forecasting today’s market and the foreseeable future when we take into consideration the new dynamics of the market, right? What will be the market’s reaction on July 2nd when the affects of tapering collide with historic seasonality of this particular trading day? Modern history tells us July 2nd is the more positive trading day of the year, but Fed tapering day tells us that markets tend to fall that day. Seasonality never had to contend with Fed tapering in the past and as such, “this time is different”.

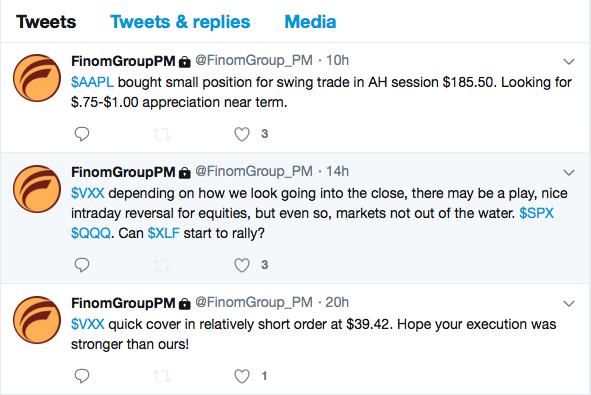

Regardless of how the markets perform come July 2nd, Finom Group will continue to trade what the market delivers. During yesterday’s trading session, we took advantage of the market volatility by doing what we believe we do best, short VIX-Exchange Trade Products, namely shares of VXX.

As shown through our private Twitter feed for subscribers, we scalped short VXX intraday for a quick profit. Additionally, and with the markets taking a turn for the positive and ending the day nicely higher, the stress test results and bank buyback disseminations were found favorable to us. We took a position in shares of AAPL during the after hours trading session with the belief that Friday’s market would follow Thursday’s trading sentiment, for the most part. We’ll be looking to take the profit on the long AAPL trade in the premarket on Friday morning.

It’s been a long and topsy-turvy week for investors and it would be a net positive to witness equities strongly higher to end the week. Next week will likely be another newsworthy week for which investors have a looming deadline to consider, the July 6th tariff implementation on China deadline. See table below:

| U.S. | China | $50 billion of goods | 25% | To take effect July 6 on $34 billion worth. Second set of $16 billion pending further review. |

| China | U.S. | $34 billion of U.S. goods | 25% | To take effect July 6 |

| U.S. | China | Additional $200 billion of goods | 10% | Threatened |

| U.S. | European Union | Automobiles | 20% | Threatened |