Wall Street was looking dicey prior to the market’s open yesterday until the White House validated its trading approach with China. Oddly, the details surrounding the Trump administration’s approach were released on Tuesday, but with no positive market reaction like that in the pre-market hours Wednesday. The following details were released Tuesday afternoon and as we wrote in the article titled When China Sneezes… Global Equity Markets Follow? :

“There may be some relief for China in the interim and as they ready for potential tariff implementation imposed by the U.S. on July 6th. President Donald Trump suggested Tuesday that he will ease off his demands for tough new restrictions on Chinese investment in technology industries and will rely instead a 1988 law being updated by Congress that authorizes the government to review foreign investments for national security problems.

“We have the greatest technology in the world, people come and steal it,” he said in response to questions from reporters at the White House. “We have to protect that and that can be done through CFIUS,” referring to an interagency group, the Committee on Foreign Investment in the U.S., which screens foreign investments to see whether they endanger national security.”

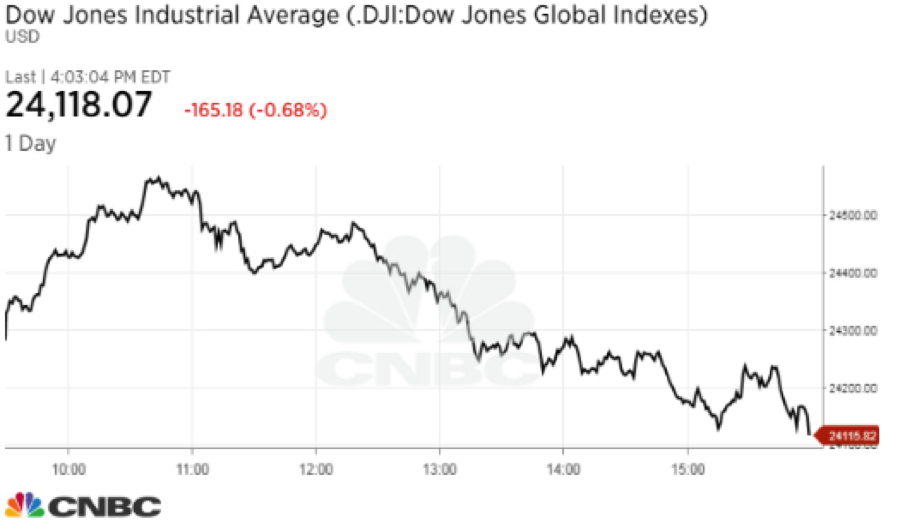

But when those very same details on the Trump administration’s approach on trade and investments with China was further announced before the equity markets opened yesterday, futures did a complete 180 and headed sharply higher. Once the market opened, the Dow climbed dramatically and was up roughly 285 points at its peak….before giving it all up and finishing lower by roughly 165 points on the day.

The S&P 500 pulled back 0.9% to 2,699.63 as tech fell 1.5 percent. The Financials Sector Spiders (XLF) fell for a record 13th straight trading session. The retreat by XLF highlights the broader decline in financials, which have been pressured by a number of geopolitical headwinds, including hostilities around trade, but has accelerated as the yield curve comes into focus. Yields have been expected to rise with the Fed raising rates, but this hasn’t been the case to some degree or rates haven’t lifted enough on the long end of the curve. At present, yields on benchmark Treasuries, specifically the 10-year note which remains historically low, this is a negative for banks that borrow on a short-term basis and lend on a longer-term basis. The spreads between the 2-10yr. yields have been tightening for some time now and threaten to invert. Currently, the spread between the 10-year Treasury yield and the 2-year Treasury stands near 31 basis points or 0.31 percentage point, the narrowest since 2017.

“The metric of the moment is the yield curve,” wrote Mike Mayo, bank analyst at Wells Fargo, in a June 19 note. “Investor concerns about the shape of the yield curve are warranted if the curve becomes inverted (short-term rates higher than long-term), which is often seen as a harbinger of a recession and the onset of a credit cycle.”

While the XLF and individual big banks have seen significant share price erosion throughout June, there may be some help on the horizon. Banks are set to receive approval to deploy capital to investors on Thursday as a part of the second leg of its banking “stress tests”.

So what happened in yesterday’s trade, one might be asking themselves? Simply put, the surge in the early part of the trading day was nothing more than short covering on what appeared to be good news on trade relations. But without any true buyers coming into the market once the short covering was complete, the market regained its trend lower. Another factor weighing on markets yesterday was the rebalancing efforts by fund managers at the end of the quarter. Many fund managers seek to lock in their gains and sell their losers at quarter end. This process is otherwise referred to as “window dressing“. Moreover, at present there simply isn’t a strong catalyst for buyers to step into the market at present. Although earnings and the economy remain strong and growing, the fears surrounding global trade are overpowering corporate fundamentals.

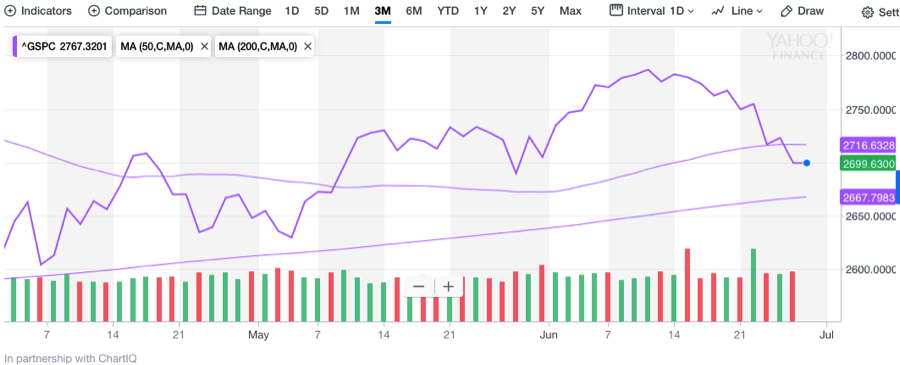

The technicals found the broader S&P 500 faltering in yesterday’s trade. The S&P 500, which managed to stay above its 50-DMA earlier in the week, dove below the key support level and closed below 2,700 yesterday.

Having said that, the index is now only 32 points away from touching its 200-DMA ahead of earnings season. While the near-term outlook for the S&P 500, and for the XLF, looks bearish it may prove to be a great buying opportunity should fears surrounding global trade ease alongside a strong earnings season.

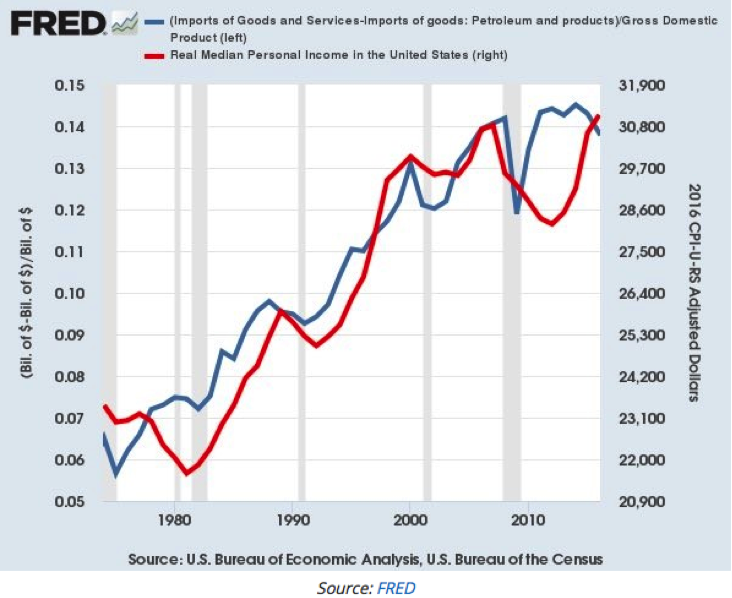

The bottom line is that trade is good and presently there is a rather sizable impediment confronting trade via the White House. Trade is never 100% fair or free, but that doesn’t mean it doesn’t work and work well. Like trading equities, sometimes you simply take what the market is bearing. Trade allows for specialization, which provides producers with efficiency gains. These gains are passed on to the consumer, which increases purchasing power. The American consumer has a multitude of inexpensive options for many goods because of global trade. The FRED chart below compares the real median personal income to the imports of goods and services minus the imports of oil products divided by GDP.

As shown in the FRED chart, as globalization has grown for several decades, the consumer has substantially benefited. The chart is an inarguable portrayal of why the world has traveled down the path of globalization. Global trade is good!

Yesterday’s economic data was rather benign as orders for durable goods fell 0.6% in May following a revised 1% decline in April, driven by a drop in new orders for trucks and cars. The trade deficit in goods narrowed 3.7% to $64.8 billion in May, which was below the $69.2 billion estimate of economists polled by MarketWatch. Separately, U.S. pending-home sales declined 0.5% to a reading of 105.9 in May. Today, investors will get another look at Q1 GDP, which is expected to remain unchanged at 2.2 percent.

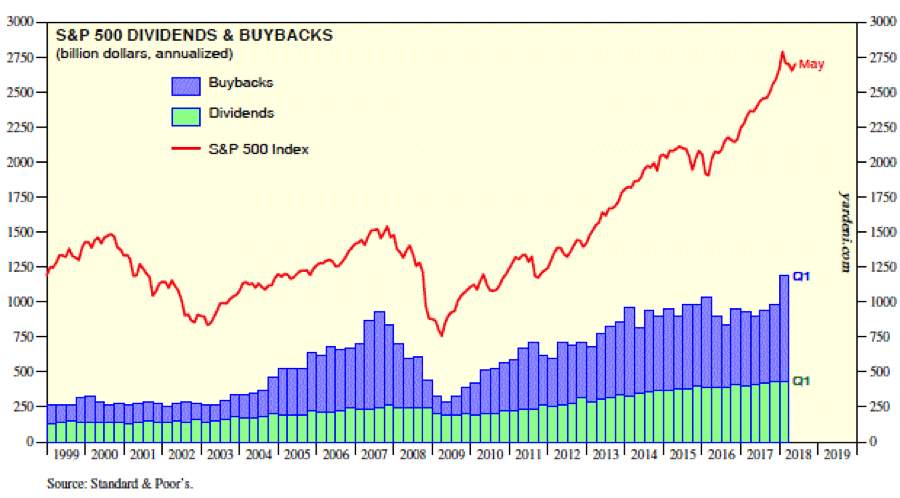

The market looks ugly without a doubt and there is growing fears around trade and the orderly process of window dressing. Having said that, fear could be to the benefit of those investors with a long-term outlook and willingness to wade through turbulent waters. Finom Group’s chief market strategist Seth Golden believes that the end result of the trade rhetoric and negotiations will prove innocuous to the U.S. economy, although certain tariffs are expected to be imposed in favor of others. Golden also believes one of the better buying opportunities in the market right now lay within the financials. For investors seeking diversity within the financial sector, the XLF may very well be the instrument to choose. Moreover, Golden also believes that while the technicals for the S&P 500 and Dow appear dangerous, that may prove to be a buy signal in hindsight and with corporate buybacks set to accelerate. Ed Yardeni of Yardeni Research believes this to be the case as well. Yardeni expects corporate buybacks to continue at a solid pace throughout the rest of 2018. Buybacks recently set a record in Q1 2018.

“S&P 500 buybacks are back. Actually, they never left the current bull market despite recurring chatter that the buyback binge was over. Since 2014, they’ve fluctuated around an annualized rate of roughly $550 billion. They jumped during Q1-2018 to an annualized $756 billion. That’s a record high, exceeding the previous record high of $688 billion during Q3-2007.”

These buybacks, according to Seth Golden, serve to provide a floor for the stock market. For each time during 2018 that the market has found steep declines, buybacks have been enacted that prove to support the market. Moreover, there’s not a whole lot of time to sell more equities given what is expected to be a strong earnings season. As such, while there may prove to be some enduring, short-term market selling pressure, it may also be the buying opportunity investors have been awaiting since the market rebound in late April.

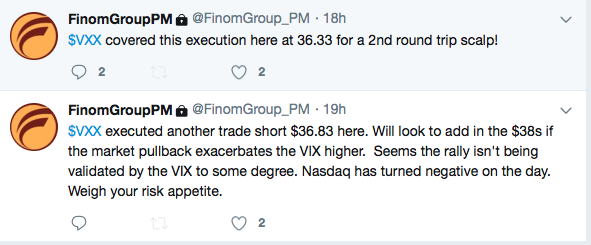

Regardless of how the market performs near term, Finom Group continues to trade what the market offers and yesterday, given the volatility in the market, Finom Group was able to trade that volatility.

The screen shots provided were from two separate trade alerts executed on VXX yesterday, Finom Group’s suggested VIX-ETP to highlight and engage with in 2018. Finom Group has an above 90% success rate on its trade alerts to subscribers in 2018 and will publicly disclose its latest, longer-term trade idea publicly in the coming weeks. This particular trade was delivered to subscribers 2 weeks ago and has since climbed into “the green”. Some investors might recall Finom Group’s chief market strategist take a longer-term position in Chipotle Mexican Grill last year in the $290 range.

In 2018, that investment delivered a substantial return on capital. With that said, U.S. futures are higher by nearly 100 points in the 7:00 a.m. EST hour, but European markets are largely in the red and with the DAX near its lows of the early trading hours. Good luck out there and come trade with us at finomgroup.com.