Global and domestic markets went on a roller coaster ride from Sunday night through Monday’s U.S. trading session. Headlines coming from the G-7 summit stated that the U.S. received multiple calls from China concerning trade. President Donald Trump said Monday that China is ready to come back to the negotiating table and the two countries will start talking very seriously.

“China called last night our top trade people and said ‘let’s get back to the table’ so we will be getting back to the table and I think they want to do something. They have been hurt very badly but they understand this is the right thing to do and I have great respect for it. This is a very positive development for the world.”

I think we are going to have a deal. They have supply chains that are unbelievably intricate and people are all leaving and they are going to other countries, including the United States by the way, we are going to get a lot of them too.”

And while China denies such calls took place, CNBC’s Jim Cramer warns investors about believing China over the U.S. President.

“I’m aghast we trust the People’s Republic of China more than we trust the White House. The predominance of coverage this morning is that the president is lying. I’m not willing to say that he’s lying. We can doubt him, but in the end we’re doubting a guy that didn’t want the market to crash.”

“Chinese government officials “haven’t necessarily been square and honest. People need to take Trump “seriously.”

Forget about whether or not the President is painting the most accurate picture of communications between the U.S. and China regarding trade. The more overarching theme is that the President is showing and expressing his concern for a falling stock market. After last Friday’s roughly 2.5% drop in the major averages and Sunday night’s equity futures stumble, it’s clear that the President was concerned that the markets would continue to falter under the weight of his heavy trade rhetoric/tweets and actions ensued to reverse such market declines.

Recall from Finom Group’s weekly Research Report where we offered the following: “With that being said, markets dictate policy and eventually the market will arise to the occasion once again. That may already be why the President’s tone on trade is seemingly more conciliatory than it was during Friday’s tweet storm.”

The Trump “put” is real and the markets evoked that put by demanding a change in trade rhetoric/policy. What’s left to see is whether or not the enacted Trump “put” is maintained and aids in delaying future tariff implementations. Nobody desires to see the September 1st threatened tariffs become realized, especially with global GDP faltering and now Germany’s economy showing a contraction, largely due to the global trade issues.

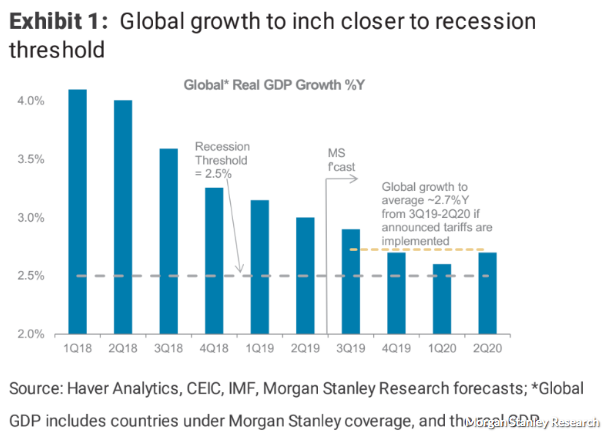

Chetan Ahya, chief economist at Morgan Stanley has been raising the warning flags over trade issues and a weakening global economy for the last couple of months. He recently suggested a “Lehman moment” is awaiting equity markets.

“We view risks of further escalation as meaningful. If the U.S. raises tariffs on all imports from China to 25% and China makes a matching response, with those measures staying in place for four to six months, we believe that the global economy will be in recession in six to nine months.”

Ahya estimated that global growth would decline to an annual rate of 2.6% in the first quarter of 2020, just a hair above the 2.5% threshold that, by Morgan Stanley’s definition, marks a global recession. A further increase of barriers that raises tariffs to 25% would likely be enough to sink global growth below 2.5%, he wrote.

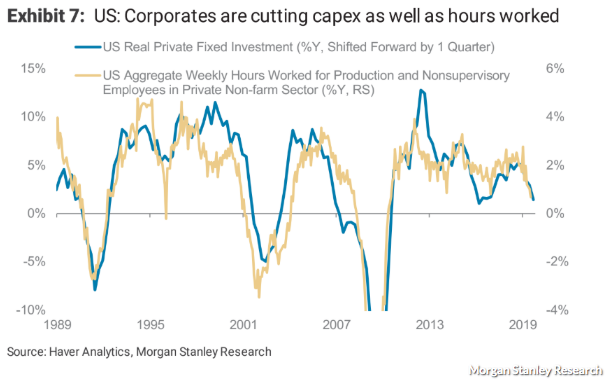

“We have been highlighting that there are signs of cracks appearing in the U.S. labor market. Just as in the rest of the world, the slowdown is spreading from the manufacturing and trade-related sectors to overall business investment and finally to the labor market.

Ahya cites slowing momentum in the labor market, with jobs growth decelerating to a six-month average of 141,000 from a peak of 234,000 in January, while growth in aggregate hours worked in the private sector has slowed from 2.8% in January to 0.7% in July.

“Hours worked is a leading indicator that has proven reliable in anticipating turning points in the business cycle. When input costs are rising . . . businesses will first slow hiring, then reduce the hours of the existing workforce before finally turning to layoffs.”

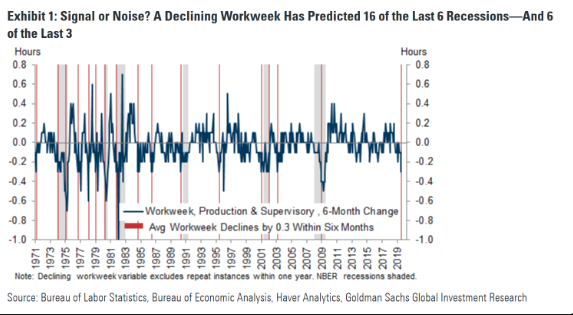

Finom Group doesn’t deny the data presented by Ahya in his latest Sunday evening notes to clients. Having said that, with regards to hours worked being a leading indicator, something suggesting a recession is afoot, well…

Hours worked, we’ve found is something like the yield curve (2s/10s) inverting. The yield curve inverting has predicted 9 of the last 6 recessions, basically suggesting that just because the yield curve inverts, doesn’t necessarily mean a recession takes place. It’s a condition of economic strength or weakness that demands other economic inputs to falter accordingly, which would contribute to a recession. As shown in the Goldman Sachs’ chart below of declining Workweeks, it identifies that a declining Workweek has “predicted 16 of the last 6 recessions and 6 of the last 3.

Basically, this argues that in no way is Workweek declining hours a leading indicator, but just another contributing factor of what may produce a recession. We’re not suggesting things can’t get worse or even that they wouldn’t get worse if additional tariffs are implemented, just factually representing the difference between what Ahya is offering and the historical data. What we do know is that tariffs are slowing the global and domestic economy and we can further see the toll it has taken on business sentiment and investment.

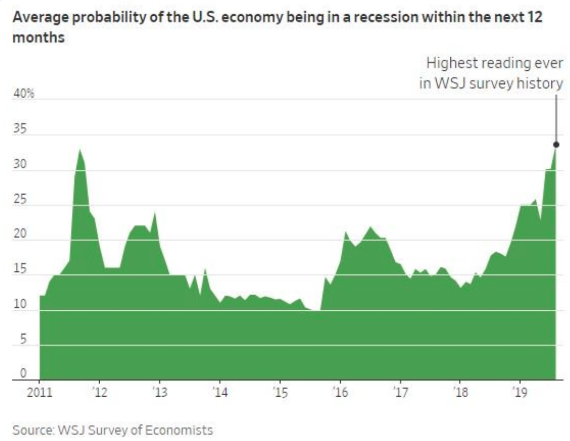

Recession risks are rising, that’s part and parcel for what tariffs can do to the economy over time, as business confidence deteriorates and eventually seeps into the broader economy. Nonetheless, one way or the other a recession is inevitable, but the depth of such a recession is unlikely to mirror that which was expressed during the Great Financial Crisis. So while Chetan Ahya is warning investors to be prepared for the eventuality, Morgan Stanley’s Chief Investment Officer Lisa Shalett is suggesting the severity of the eventual recession is likely to be rather soft.

- Are you forecasting a 2020/21 recession? No, although the odds of a U.S. recession in the next year or two are rising. Remember the definition of a recession is at least two consecutive quarters of economic contraction—it may not be that deep or prolonged. My concern is based on global economic slowing, as well as weakness in U.S. industrial and leading economic indicators. The behavior of the Treasury market, where an “inverted yield curve” (when long-term rates fall below short-term rates) is a reliable indicator of recession, also has me on high alert. Meanwhile, trade uncertainty isn’t helping.

- But isn’t the U.S. economy strong now? Yes. Unemployment is near 50-year lows and wages are growing nicely. Recent retail sales reports have been better than expected. But job growth has been slowing, and corporate earnings are declining. National Income and Product Accounts, a government measure of all corporate earnings (public, private, large and small companies), shows average U.S. corporate profits have fallen 10% since the third quarter of 2018. A contraction in that measure suggests the labor market is likely to weaken.

- Won’t Fed rate cuts help? I’m not so sure. Markets have already factored in a lot of the expected benefits of future Fed rate cuts. Currently, futures markets have priced in cuts to the short-term federal funds rate over the next six months totaling two-thirds of a percentage point. Also, the yields of 10-year and 30-year Treasuries, which reflect key borrowing rates for businesses and consumers, are already very low. It may be that the Fed is the wrong medicine for what ails.

- Should I sell my stocks? No. I expect volatility to remain elevated and think that we may see a 5%-10% correction in stock prices in the next few months. Since the expected market dislocation is modest, I don’t think abandoning stocks is the right move and don’t suggest trying to time the market. Instead, stay allocated to stocks, but shift toward actively managed, value-style funds that seek stocks with high quality cash flows and dividends. With those income sources, you effectively get paid to stay invested in equities and wait for the economic smoke to clear.

In keeping with the concerns raised by Morgan Stanley’s team, J.P. Morgan’s team has offered a similar sentiment as depicted in the following tweet.

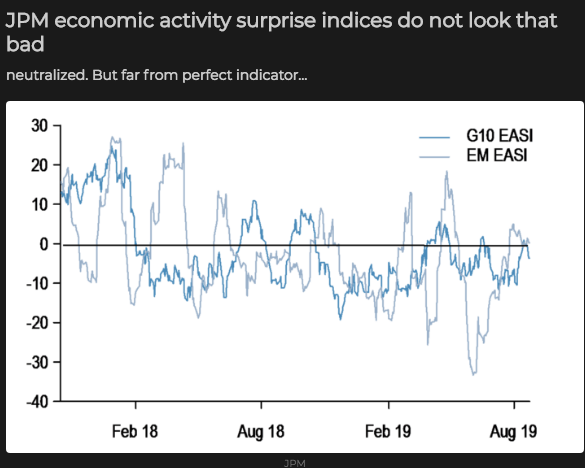

With all the recession risks seemingly rising and felt amongst the analyst community, the U.S. economic data has proven relatively ebullient. Where certain aspects of the economy are faltering, namely manufacturing, the majority of economic data is proving out trend-growth GDP. While J.P. Morgan acknowledges that risk of recession are rising, it’s proprietary Economic Activity Surprise Index isn’t showing meaningful stress.

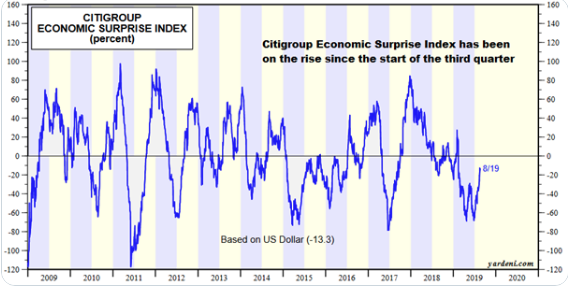

The Citigroup Economic Surprise Index is showing a similar expression of the economic data over the last month or so, bouncing off the recent and more concerning lows.

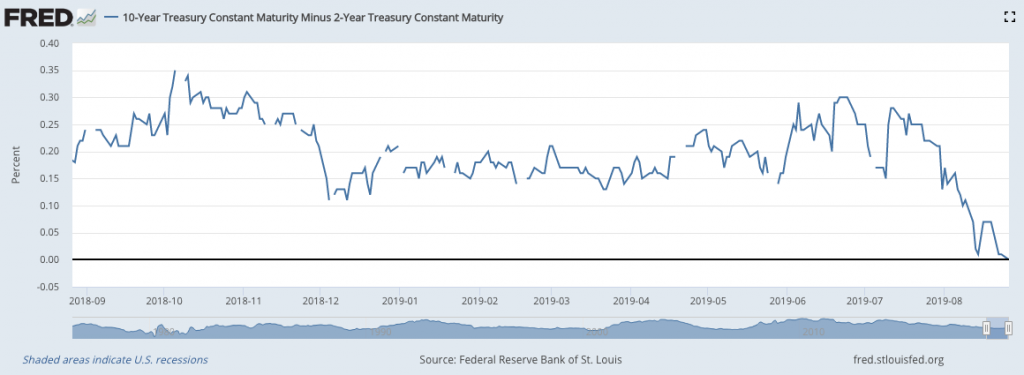

But even with the stronger than anticipated economic data, the backdrop of slowing, trend-growth GDP with more tariffs possibly going forward has given rise to recession fears. And the yield curve inversion isn’t helping alleviate those fears, naturally. As of Monday, the yield curve inverted yet again, albeit by just about 1 basis point.

The yield curve remains below the Fed Fund Rate (FFR), but the 2s/10s inversion is only slight. Remember, it’s not that the yield curve inverts, it’s how long and to what degree it inverts. But taken altogether, tariffs, declining private business investment and a yield curve inversion, investors continue to play up the recession risks.

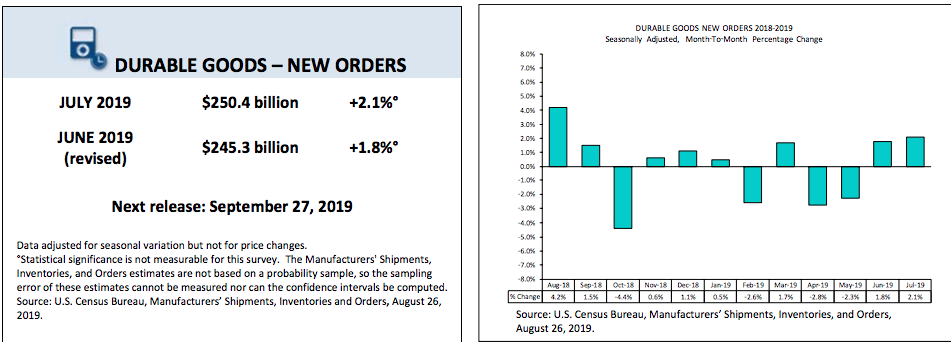

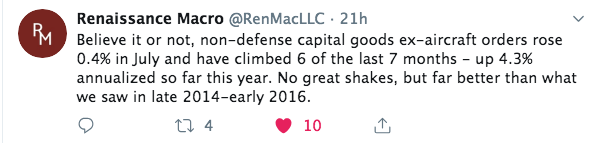

Speaking of economic data, U.S. Durable Goods orders surprised market participants on Monday by beating economists’ estimates for a 2nd consecutive month.

Orders for durable goods rose 2.1% in July, the Commerce Department said Monday. It is the second straight monthly gain. Economists expected a 0.9% gain. Unfortunately, the prior month’s reading was revised lower from 2% to 1.8 percent.

The gain in orders was led by transportation, a 47.8% surge in aircraft and parts that is mainly Boeing (BA) orders. Excluding that sector, orders fell 0.4%, the biggest drop since March.

A key metric, orders for non-defense capital goods, rose 0.4% in July, but a gain in the prior month was revised down to a 0.9% gain from the prior estimate of 1.5% rise. Orders in this sector are now down 0.3% from a year ago. Shipments of non-defense capital goods fell 0.7% in July, largest drop since Oct. 2016.

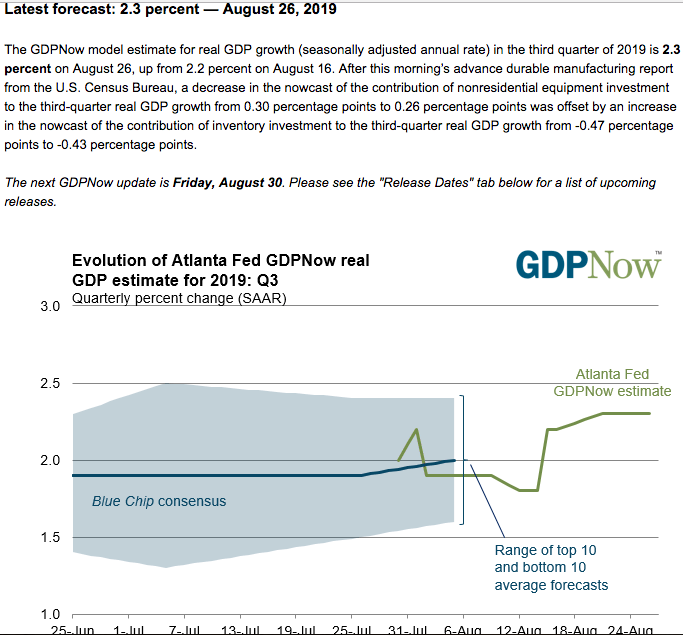

The release of the July Durable Goods report came with corresponding revisions to both Q2 and Q3 GDP forecasts amongst regional Federal Reserve banks and financial institutions. Don’t forget that despite the light economic data calendar over the coming two days, on Thursday investors will get a 2nd look at Q2 GDP. Nonetheless, after the Durable Goods data, the Atlanta Fed saw fit to raise their Q3 GDPNowcast model from 2.2% to 2.3 percent.

- GOLDMAN SACHS: Our Q3 GDP tracking estimate declined by one tenth to +2.0% (qoq ar) last week following a sharp decline in new home sales. Ahead of Thursday’s second release of Q2 GDP, we lowered our past-quarter Q2 GDP tracking estimate by a tenth to +1.8%.”

- Merrill on GDP: “Today’s data and our new trade outlook cut 2Q and 3Q GDP tracking estimates by 0.1pp to 1.7% qoq saar and 2.0% respectively.”

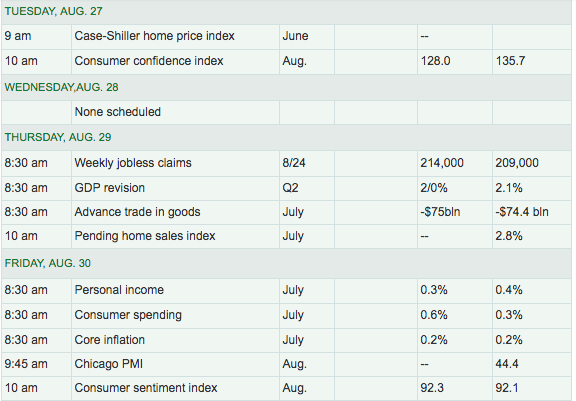

For Tuesday, market participants will be focused on Consumer Confidence data, which is expected to falter a bit from recent high levels. A decent amount of economic data is back-week loaded. The MarketWatch table outlines the cadence of the economic data releases, inclusive of Pending Home sales data, to be released on Thursday and alongside Initial Jobless claims. Recently, New Home sales hit a cyclical high.

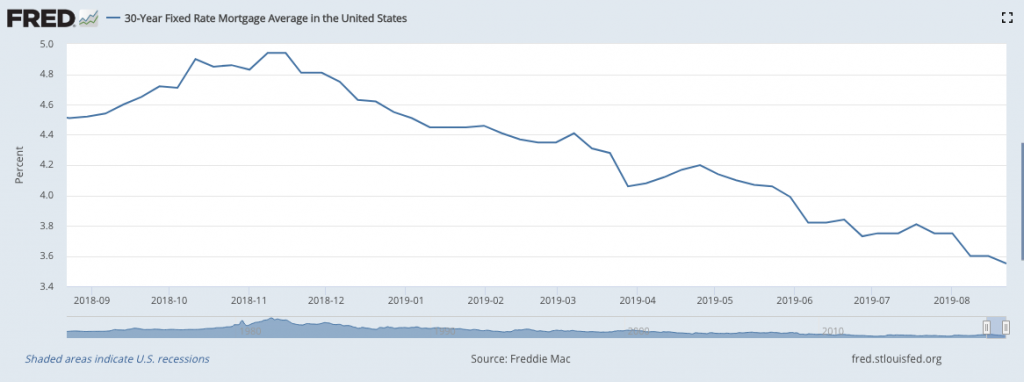

Although not depicted in the table above, mortgage application data will also be released on Wednesday. Mortgage application filings have also recently hit cyclical highs as interest rates have fallen precipitously since November of 2018.

The decline in the 30-year fixed rate mortgage over the last 10 months has lent itself to triple-digit gains in mortgage refinance applications in recent months. This has also served to offset some of the potential impact from tariffs on certain consumer goods. Data offered by various research firms suggest that the average mortgage holder is able to lower their mortgage payment by $87 per $100k mortgage. It doesn’t get much attention in the media, with respect to offsetting tariffs though. With rates continuing lower over the last several months, here is what Goldman Sachs and Merrill Lynch had to say about the lag time between lower rates and the housing sector’s performance.

From Merrill Lynch: Housing: something for everyone What comes next?

[W]e are making some tweaks to the housing forecast. Housing starts are likely to edge down this year to 1.24mn but recover next year. Existing home sales should also come in lower this year at 5.30 million and hold around this pace in 2020. The story for new home sales is a bit better with 650k this year and 660k next. In other words, further sideways motion for housing activity, leaving it a benign factor for the overall economy.

From Goldman Sachs: Can Lower Rates Still Boost Housing?

[O]ur estimate of the lag time between changes in interest rates and housing activity suggests the bulk of the boost is yet to come. … we update our outlook for the growth boost from housing via both the homebuilding channel and the impact of refinancing, mortgage equity withdrawal, and housing wealth effects on consumer spending. Our model points to a healthy rebound to a 4% growth pace of residential investment in 2019H2 and an increase in the total contribution from housing to GDP growth from -0.05pp in H1 to +0.15pp in H2.

Ahead of the Consumer Confidence data this morning, equity futures are pointing to a slight continuation of the Monday rally, even as the German economy officially showed a contraction in Q2 2019.

Coming into the trading week, the S&P has been stuck in a trading range throughout August and has fallen 4 straight weeks. That’s the bad news. The good news, however, may be that trade talks are ongoing and there have been very, very few occasions whereby the S&P 500 has fallen 5 weeks in a row during the current bull market.

Since this bull market started 10 years ago, only once has it been down 5 straight weeks (6 weeks in a row in 2011). In addition to the less likely probability of achieving another down week, Put/call ratios have spiked to levels that have been close to market bottoms.

Even with these, technical indicators at-hand, there may be some downside left for the market’s to explore near-term. Having said that, tweets and trade headlines don’t care about technicals, as recently proven… again. Nonetheless, Canaccord Genuity’s chief equity strategist Tony Dwyer offered the following in recent notes to clients:

“Sometimes it is better to react to market conditions rather than try to anticipate the next move. We believe the market has been in tactical no-man’s land following the early August 6% swoon because the market was no longer overbought but had yet to reach oversold enough levels to generate the next intermediate-term leg higher toward our 2020 S&P 500 (SPX) target of 3350.

We are in the 3rd near recession of this cycle, and that a much easier Fed, drop in market rates, and cautious investors sentiment sets the stage for both a market and econ recovery heading into 2020.”