Markets went on another wild ride on Tuesday with the S&P 500 (SPX) opening higher and trading higher in the first half hour of the day by as much as 20 points. The benchmark index nearly touched 2,900 before tumbling, giving back all of its gains and falling some 38 points from the intraday high to low.

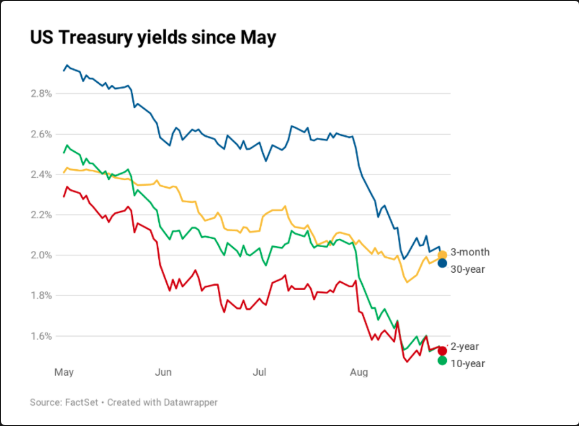

From the lows of the day there was a significant rally that brought the index back into positive territory, while bond yields rallied a bit, but then that all reversed in the final half hour of trading. Bond yields attempted a rally but it failed in the final 30 minutes and as bond yields went, so did equities, stumbling into the closing bell on Wall Street. In fact, since May its been nothing but a downhill slope for bond yields.

The tight correlation between between stocks falling alongside bond yields has been in place throughout May, something CNBC’s Jim Cramer discussed in terms of the uncertainty it breeds amongst investors earlier in August.

“As long as Treasury yields keep plummeting, investors will remain unsure of themselves. At least today, they finally found some stocks to buy along with bonds. It’s just that they’re the wrong stocks, the recession stocks, not the kind of leaders we want to get behind. The stock market will continue to be volatile until the bond market finds some stability.”

We would tend to agree with Cramer as the S&P 500 has fallen by 250+bps on 3 separate trading sessions this month, the first time this has occurred in a single month since September 2011 (-259bps on 8/23, -293bps on 8/14 and -298bps on 8/5). These 3 drops have offset 6 separate gains of at least 100bps, leaving the index currently sitting at -373bps month to date.

While the bond market continues to worry investors and is now found with the deepest 2s/10s inversion since 2007, there continues to be at least one advantage, one that we discussed at Finom Group in our recent article as follows:

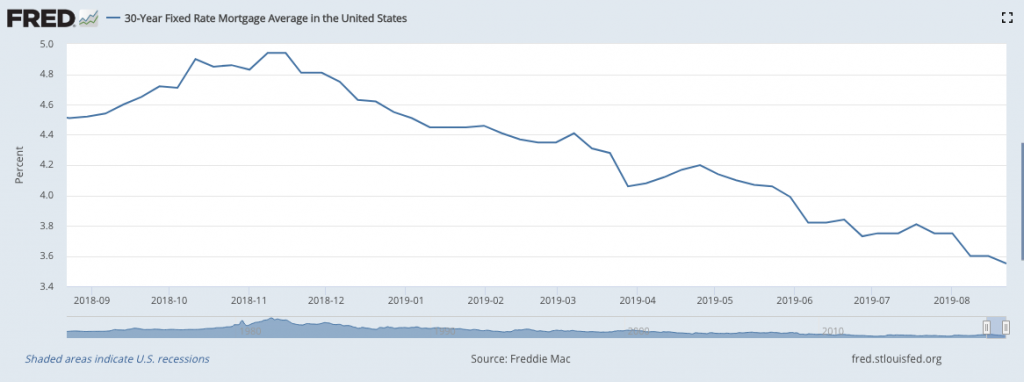

- Mortgage application filings have also recently hit cyclical highs as interest rates have fallen precipitously since November of 2018.

- The decline in the 30-year fixed rate mortgage over the last 10 months has lent itself to triple-digit gains in mortgage refinance applications in recent months. This has also served to offset some of the potential impact from tariffs on certain consumer goods. Data offered by various research firms suggest that the average mortgage holder is able to lower their mortgage payment by $87 per $100k mortgage.

There is nothing slated in the way of government economic data on to be released Wednesday, investors will receive the latest weekly mortgage application data. We expect, as the 30-yr. Fixed Rate Mortgage continues to fall to near its lowest levels since 2011, both refinance and home purchase applications to be higher on a YoY basis and higher for refinances on a WoW basis as well.

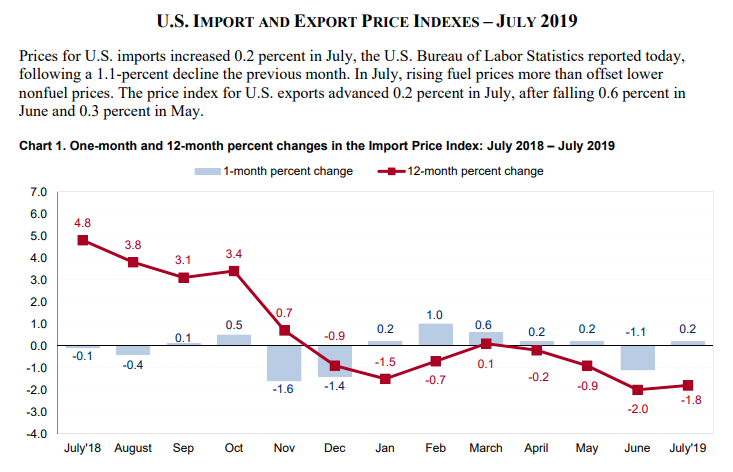

Tariff impact continues to gain the vast majority of attention given the lagging capital expenditures and business investment recently reviewed in the Durable Goods data, but it does go widely overlooked and ignored as to just how much lowered rates is likely to offset such tariff price increases, should they come to pass. Remember, for all the tariff hype we’ve yet to see prices rise on a 12-month basis as reviewed through the latest BLS Import & Export Price Index.

Again the main concern isn’t prices or even the consumer that continues to remain resilient in the face of a 13 month trade feud, but with respect to business investment. In other words, the economy isn’t faltering, it’s slowing, but not faltering as the consumer makes up some 70% of GDP. So as consumers pad their balance sheet monthly through, additional refinancing and lower gasoline prices YoY, the economy is little worse for wares, but the stock market may be a different story. And why? Lower rates play up well with the economy and consumers but the banking/financial sector doesn’t find favor with rates this low as we can see in the following chart of the Banking sector ETF (KBE).

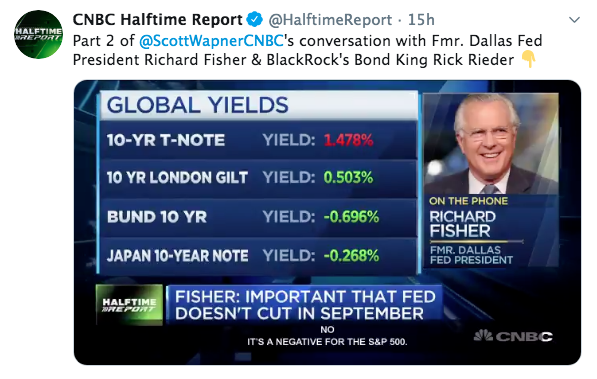

Along the same exact lines of discussion, former Dallas Fed President Richard Fisher argues that the world is in a negative interest rate environment. He believes this is what is driving a flight to safety and yield into U.S. bonds, not necessarily for fears of a recession. Facts are facts, just look at 10-year yields around the world compared to the United States; it’s a no-brainer.

- 10-Year Government Bond Yields… Switzerland: -0.99% Germany: -0.70% Denmark: -0.66% Netherlands: -0.56% Austria: -0.44% Finland: -0.43% France: -0.41% Slovakia: -0.38% Belgium: -0.36% Sweden: -0.33% Japan: -0.27% Slovenia: -0.22% Ireland: -0.07% USA: 1.49%

“Lower rates are largely going to offset the tariffs, it’s a positive for the consumer, the economy, but not the stock market.”

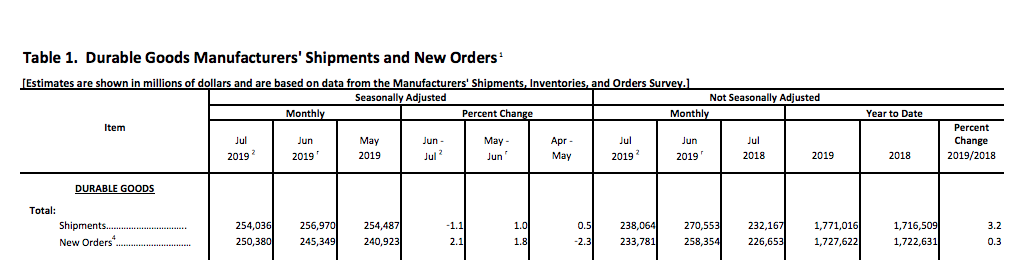

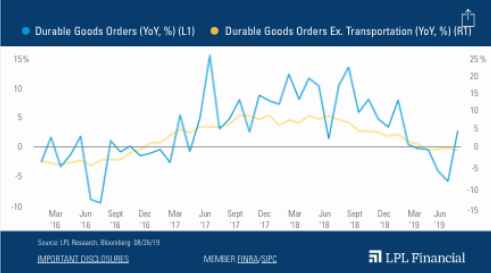

And while the MoM Durable Goods orders released Monday proved strong, it’s still the business investment/new orders that identify the angst amongst the business community and lack of clarity from tariffs going forward.

The overarching concern identified in CAPEX and or Durable Goods data is the slowdown and nearly flat reading YoY. Business investment remains weak while consumption remains healthy, but how long can that last. This the question recently posed by LPL Financial, as they recognize the strength of the consumer juxtaposed with weakening business investment and Durable Goods orders.

“On a year-over-year basis, as shown in the LPL Chart of the Day,Slowing Durable Goods Amid Trade Tensions, durable goods orders excluding transportation have been flat over the past year and growth has been slowing since June 2018—covering the bulk of the trade dispute. Year-over-year growth in orders for non-defense capital goods (excluding aircraft) has also grounded to a halt, averaging just 0.3% over the last three months.”

“Productivity-enhancing capital expenditures are critical for elongating this economic expansion,” said LPL Research Chief Investment Strategist John Lynch. “Capital investment has softened because of the trade dispute with China, which puts more of a burden on the U.S. consumer to continue to drive economic growth. That can continue for only so long.

Trade tensions continue to weigh on capital investment and overall economic growth, which is one reason we reduced our 2019 gross domestic product (GDP) growth forecast to 2% (down from a range of 2.25–2.5%). Yesterday’s report told us that business investment is unlikely to contribute to third quarter GDP, which is only expected to grow at a 1.8% annualized rate (Bloomberg consensus).”

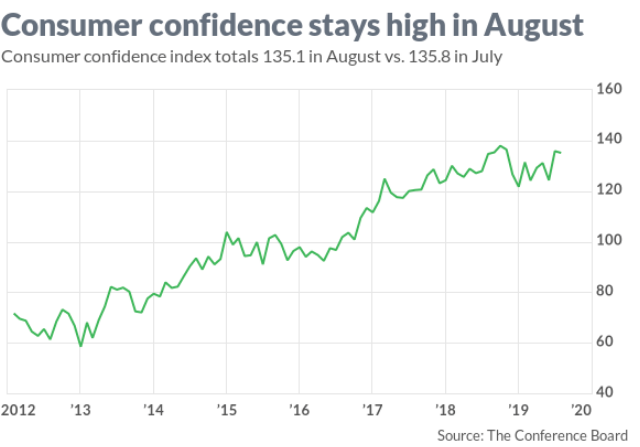

As an investor and analyst for over 20 years now, I can honestly say I’ve never seen conditions presented as they are today in the market. All we continue to see are charts of elevated recession risks, talk of the yield curve inverting which precedes a recession and various sectors of the market teetering on breaking down. Nonetheless, the consumer has shrugged it all off and for the better part of the last year. In fact, the latest Consumer Confidence reading suggests investors would rather the financial media “shut it’s pie hole”. (So to speak of course)

The Consumer Confidence Index fell slightly to 135.1 in August from a revised 135.8 in July, the Conference Board said Tuesday. The index remains close to an 19-year high, however. Economists polled by MarketWatch had predicted the index would fall to 127.8 in the wake of an escalating U.S. trade war with China that slammed stocks earlier in the month and sent interest rates plunging.

The present situation index, a measure of how consumers view the economy right now, rose to 177.2 from 170.9. Another index that looks out over the next six months, however, appeared to reflect somewhat more worry. The so-called expectations index slipped to 107 from 112.4.

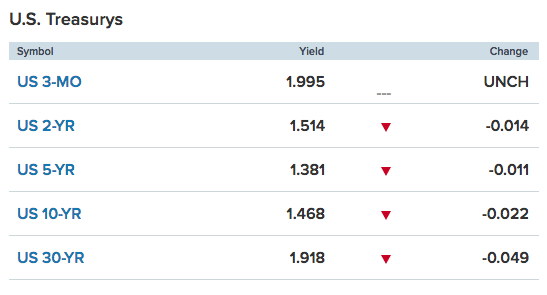

U.S. equity futures are pointed to a slightly lower open on Wall Street Wednesday, as yields are once again coming under pressure.

With the yield curve (2s/10s) further inverted on Wednesday morning, Jim Cramer suggests the yield curve linkage for a recession is “wrong”. Like other economists and Fed governors, Cramer believes the signal is different than in past economic cycles.

“Until we get some tangible signs that the economy’s picking up, you’re going to have to get used to the screams of this needy bear cub of a market. But I have to urge you to stay the course because … I do think the linkage will be exposed as faulty and stocks will remain the best investments.”

Cramer isn’t convinced that the yield curve inversion, where the 2-year bond pays out more than that of the 10-year bond, which has preceded each recession of the past 50 years, is flagging this time that a severe economic slowdown is in the works. His reasoning is based on the fact that U.S. bonds are yielding more than foreign bonds, which is drawing overseas demand for American bonds.

“All that foreign … buying has created an inverted yield curve, where short-term rates are higher than long-term ones.”

He went on to argue that lower interest rates should help consumers borrow money more cheaply. Lenders tend to use the 10-year yield as a benchmark for car loans and mortgage rates.

“I think this will be a huge boon, especially to housing.”

The problem doesn’t lay with the facts at-hand but the how pervasive sentiment can be and how that sentiment can become a self-fulfilling prophecy of sorts. Fear, uncertainty and general loathing amongst the business community, if it should grow further, can eventually determine the economic outcome. And we’re not just seeing this fear with business investment and capital outlays, but also with insider transactions as recently reported by TrimTabs.

Corporate insiders have sold an average of $600 million of stock per day in August, according to TrimTabs Investment Research, which tracks stock market liquidity. August is on track to be the fifth month of the year in which insider selling tops $10 billion. The only other times that has happened was 2006 and 2007, the period before the last bear market in stocks, TrimTabs said.

“It signals a lack of confidence,” said Winston Chua, an analyst at TrimTabs. “When insiders sell, it’s a sign they believe valuations are high and it’s a good time to be outside the market.”

Salesforce (CRM), Slack (WORK), Chipotle (CMG), Visa (V)and Home Depot (HD) all sold shares, according to OpenInsider, a site that tracks insider stock sales.

Not for nothing, but the noted examples of insider selling are probably bad examples offered. I mean, HD hit an all-time high, would you be selling as an insider? V is up some 35% YTD, woudln’t you be selling as an insider? CMG also recently hit an all-time high and Slack is an IPO with expected insider selling after going public and with a greater constituency of investors. The only stock on that list you could argue against would be CRM.

Nicholas Colas, co-founder of DataTrek Research, noted insider selling is not always a helpful indicator at a high level. Rather than reflecting a lack of confidence, he said, the selling may simply be the result of insiders bracing for leaner compensation.

“Most managers get paid on earnings growth. If they anticipate bonuses will be slower, they will sell stock to make up the gap,” Colas said. “It’s one more sign that managements know this will be a tough year for growing earnings.”

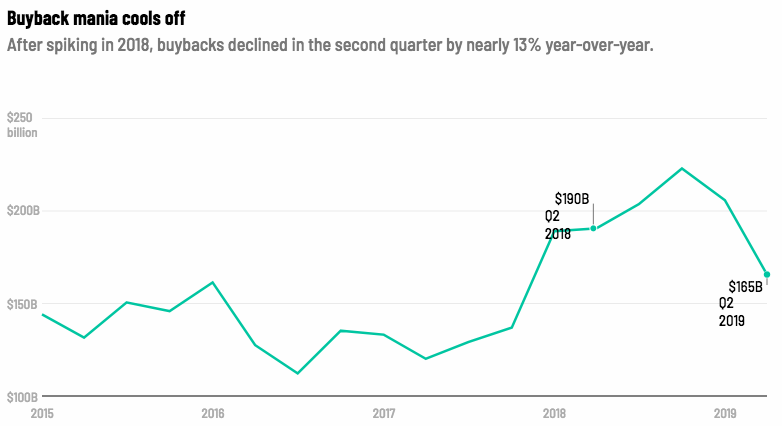

On the whole, the market doesn’t desire any sellers and while we can make excuses for these insider sales; a sale is a sale nonetheless. Coupled with consistent equity market outflows YoY, these represent headwinds for the market as a whole. And if this wasn’t bad enough, buybacks also slowed in the Q2 2019 period.

Don’t get me wrong, buybacks are still at extremely high levels, but less is less.

“A lot of these companies have seen their stock price go up a lot. Treasurers are thinking, ‘Maybe I save some ammo in case anything crazy happens,'” said Ian Winer, advisory board member at Drexel Hamilton.

In the 3rd quarter we’ve seen some acceleration of share repurchases from the Q2 period, especially in recent weeks. Bank of America Merrill Lynch published a research report just last week suggesting that buybacks continue to rise. Repurchases executed at Bank of America accelerated last week to three-month highs. Buybacks are up 14% from the same period of last year, the firm said.

Last week, the GS Desk saw flows increase +20% vs the 2018 ADTV and +15% vs the 2019 ADTV on the market-draw downs. The desk saw corporates step in on the Friday ~300bp sell-off, as their flows posted +30% that day.

Headwinds and tailwinds, the market is made up of both and presently the market is aiming to decide how it desires to end the month of August, with a bang or with a whimper. As it has been the trend in recent weeks, I’ll be continuing to monitor bond yields and oil prices. We’ve been laser focused on the fact that while many are only focused on what the bond market may or may not be signaling, despite inventory builds through August, crude oil has resisted falling further. The $53 level has held up nicely!

With the EIA inventory report due out today at 10:30 a.m. EST, we’ll be keeping an eye on crude and discussing black gold in the Finom Group Trading Room. Subscribe to Finom Group and receive our weekly Research Report, join our live Trading Room and receive our real-time daily/weekly trade alerts. See two of our latest trade alerts completed on Tuesday below: