U.S. equities got off to a rough September trade in the morning hours on Tuesday and after a long Labor Day weekend. With European markets sharply lower, U.S. equities followed suit until European markets closed for the trading day and found U.S. markets recouping almost all their losses by the end of the trading session. At its lows of the trading day, the Dow Jones Industrial Average was down almost 160 points before closing down only 12 points on the day. But the selling pressure has renewed in the premarket trading hours on Wednesday and as U.S. equity futures are following Asian and European markets lower thus far. As trade talks are set to resume between the U.S. and Canada on Wednesday, we’ll see how U.S. equities perform as the trading day carries forward.

Volatility has been rising, slowly but surely and as the S&P 500 achieved its record high level in August. But even with that rise in volatility toward the end of August, the monthly S&P 500 moves were relatively subdued. In fact, this has been the calmest August since 1967, with all daily moves less than 0.8% from one market closing day to the next market closing day.

With that being said, the VIX did surge higher intraday in Tuesday’s trading session. The fear gauge ticked above 14% before locking onto the overall market buying activity in the afternoon hours and finished the day higher at 13.16 percent. With equity futures largely lower on Wednesday, the VIX is once again rising and nearing 14% in the early hours. The only question that remains, given the early morning market activity is whether or not the dip buyers will continue to reign supreme in September.

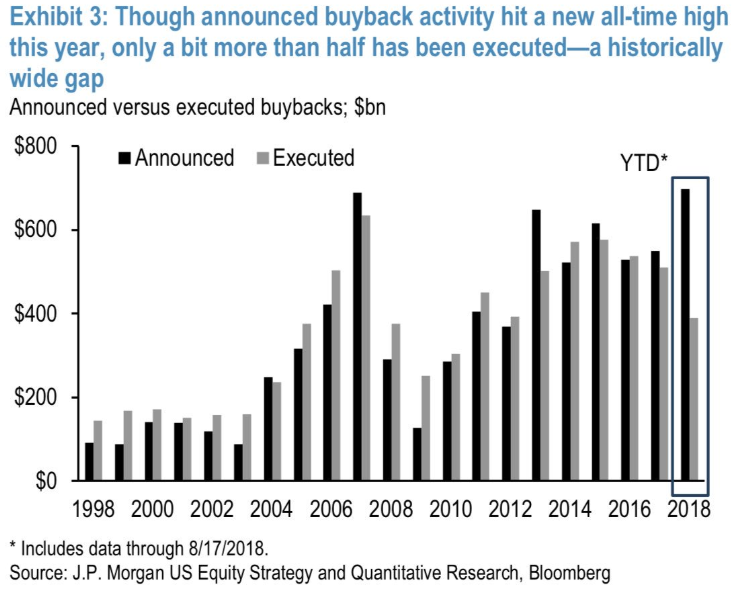

Stock buybacks continue to serve as a floor or backstop for equities and as another 2018 correction seems elusive. Total stock buybacks are expected to exceed $1 trillion this year. There’s an outsized gap presently between announced buybacks and what has actually been executed by corporations.

This suggests that corporate buybacks will rise on the next stock market pullback. It could be said that for this reason, stock market’s pullbacks in 2018 have become increasingly shallow during 2018.

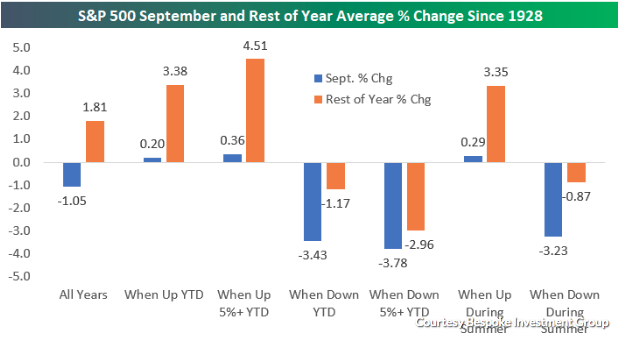

If September holds true to its historic form on average, the month will produce a negative return from the S&P 500. But Bespoke Investment Group takes exception to this sentiment as the firm reviews September’s market history performance. While the month averages negative returns overall, September tends to be positive in years where the market has been positive going into the month.

“While September has indeed been the worst month of the year for stocks, the negativity usually comes during years when the market is already struggling entering the month. That’s simply not the setup in place this year.”

According to Bespoke’s data, when the S&P has been in the red through August, September has seen an average decline of 3.43 percent. When the index has been down 5%+ YTD through August, September has averaged a decline of 3.78 percent.”

“But when the S&P is positive year-to-date through August, the benchmark index averages a gain of 0.2% in September, and then rises an additional 3.38% from September through the rest of the year. When the S&P gains at least 5% in the first eight months of the year, as in the case this year, “the average change in September has been positive again at +0.36%, and the rest-of-year gain is +4.51 percent.”

The deeper dive into the data by Bespoke is compelling, but it may be overlooking the many variables posing obstacles for equities in September 2018. Some of those headwinds are tied to global trade spats, the strengthening dollar resulting in emerging market currency strife and flights of capital around the world. Additionally, investors may already be struggling to gauge the impact of mid-term elections on the markets.

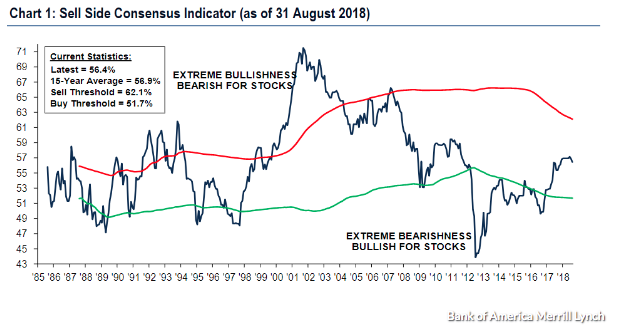

Although the headwinds for September are numerous, they have been so for much of 2018. In August, a closely watched contrarian indicator hit its lowest point in months.

“In August, the Sell Side Indicator — our gauge of Wall Street’s bullishness on stocks — dipped slightly for the second month in a row to 56.4 from 56.9,” said Savita Subramanian, equity and quant strategist at Bank of America Merrill Lynch, in a Tuesday note. “The indicator is currently at a nine-month low, a reversal from the rapid rise in sentiment from the middle of 2016 through the end of last year. Historically, when our indicator has been this low or lower, total returns over the subsequent 12 months have been positive 94% of the time, with median 12-month returns of plus 19%.”

The Sell Side Indicator is typically understood to be a contrarian indicator, suggesting the current reading is a bullish sign for equities in the near term. Subramanian projects a 12-month price return of more than 10% and a 12-month target of 3,202 for the S&P 500.

The Sell Side Indicator is typically understood to be a contrarian indicator, suggesting the current reading is a bullish sign for equities in the near term. Subramanian projects a 12-month price return of more than 10% and a 12-month target of 3,202 for the S&P 500.

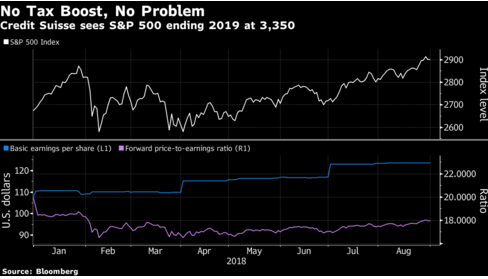

While September 2018 ‘s market performance remains in question, one firm is projecting onto 2019. Jonathan Golub, chief U.S. equity strategist at Credit Suisse, expects the S&P 500 Index to finish 2019 at 3,350, implying a gain of 11.7% from where he predicts the measure to end this year at 3,000. The 2018 call, if it comes true, would amount to a 12.2% advance.

“The next 16 months will be particularly tricky for investors, with the threat of yield curve inversion, potentially disruptive midterm elections, and continued Fed tightening. Despite these headline risks, we believe that solid economic/earnings per share growth and benign recessionary risks will be sufficient to propel the market higher.”

As U.S. corporate earnings growth remains in high-growth mode and with YOY S&P 500 earnings growing in the 20% range, the forward-looking valuation of 16.7% remains attractive. Golub expects profit growth moderation in 2019 to 7.7% from 21.5 percent while multiples expand, a rise that is normal throughout bull markets, according to the strategist.

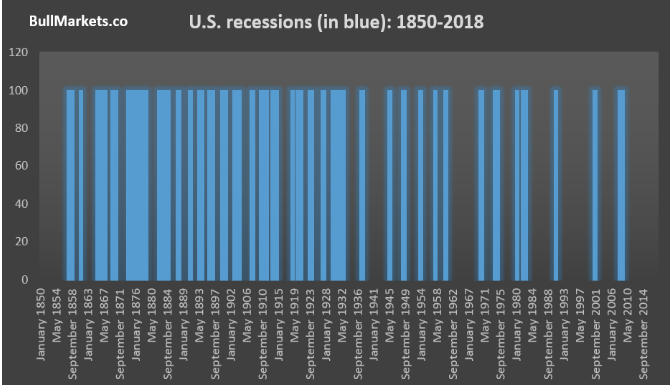

Again, September’s market performance remains in question, but a recession is not at-hand and the U.S. economy is outperforming the rest of the world. All Leading Economic Indicators remain with expansionary characteristics and supported by two key elements: A strong labor market and a strong consumer. Even as the bull market cycle remains elongated historically this is a factor of trend whereby economic expansion constantly elongates. More succinctly stated, “Economic expansions in the U.S. have become longer and longer over the past 150 years.” Economic expansions are constantly setting new records as indicated in the chart below:

Bull markets DO NOT DIE OF OLD AGE!