October has been a brutal month for the stock market, but if Wednesday (Halloween) mirrors the positive action from Tuesday’s trading, it could erase some of the significant damage done to investor sentiment. On Tuesday, the Dow (DJIA) rose 431.72 points, or 1.8%, to 24,874.64; the S&P 500 (SPX) index gained 41.38 points, or 1.6%, to 2,682.63; and the Nasdaq Composite Index (NDX) climbed 111.36 points, or 1.6%, to 7,161.65. The rally on Wall Street strengthened throughout the day as most FANG stocks turned around in the afternoon trade. Amazon (AMZN) was the only FANG stock that still finished in the red on Tuesday. Although Tuesday saw equities come back into favor, investors are not out of the woods just yet as technical damage to the major averages lingers without a clear trend reversal sustained. Having said that, U.S. equity futures are once again higher on Wednesday.

“We are seeing an oversold technical rally before we head even lower,” Sam Stovall, chief investment strategist at CFRA, predicted. “Most traders I talk to are still waiting for the capitulation to shake off before they call a bottom.”

“Once again, the month of October has been living up to its frightful reputation for wreaking havoc on stock prices: 1929 and 1987 are prime examples, and we can now safely say that 2018 will also go down in history as an illustration of October’s ability to scare investors. Unfortunately, I don’t foresee this volatility easing too much over the next few weeks,” Kristina Hooper, chief global market strategist at Invesco, said in a note to clients.

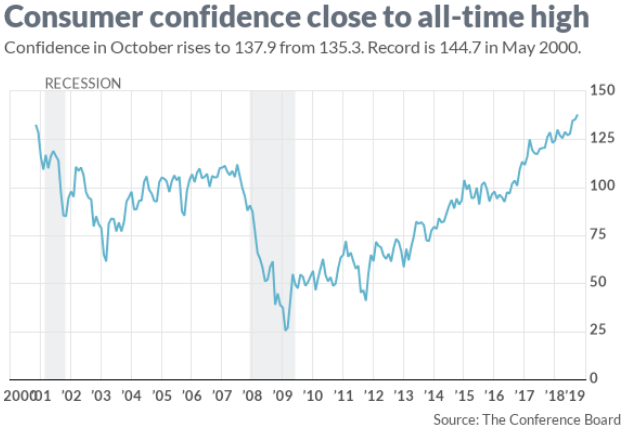

Earnings season continues to express better than anticipated results, but the economic data centering on the consumer spurred the rally on Wall Street yesterday. The U.S. economy is consumer-centric, with some 70+% of economic activity initiated by the consumer. So when consumer confidence is near record level highs, it suggests a strong economy that delivers strong corporate earnings growth.

The consumer confidence index rose to 137.9 this month from a revised 135.3 in September, the Conference Board said Tuesday. The present situation index, a measure of how Americans view the economy right now, climbed to 172.8 from 169.4. That’s also an 18-year peak. One of the driving forces behind consumer confidence is a strong labor market. Some 45.9% of Americans said jobs are “plentiful”, the highest percentage in nearly 20 years. Just 13.2% said jobs are hard to find and/or achieve.

“Consumers do not foresee the economy losing steam anytime soon,” said Lynn Franco, Director of Economic Indicators at The Conference Board. “Rather, they expect the strong pace of growth to carry over into early 2019.”

Although the housing and auto markets have both slowed, consumer confidence surveys showed the consumer is prepared to spend in these industries. More people also said they plan to buy a home or new car even with interest rates rising. The future expectations index, what Americans think the economy will look like six months from now, edged up to 114.6 from 112.5. Once again, it’s at an 18-year high.

While Tuesday’s significant rally in equities seemingly erased all that ails investor sentiment and appetite for stocks, we can’t forget that one day does not change the reality that seemingly caused the market correction. Rising rates, trade wars and fears of a slowing global economy remain ever-present and in the headlines. While the U.S. economy is proving to buck the global, slowing economic trend, rising rates remain a focus. Former FOMC chair Janet Yellen sat center-stage on Tuesday, discussing rate hikes, national deficit and more.

“If I had a magic wand, I would raise taxes and cut retirement spending,” Yellen told CNBC’s Steve Liesman at the Charles Schwab Impact conference in Washington, D.C., who characterized the U.S. debt path as “unsustainable.”

Yellen also discussed her concerns regarding global trade and the escalation of trade wars. The former Fed chair said she worries about the “role of the U.S. economy”, as the two countries (China/U.S.) slap tariffs on each other’s goods. Yellen’s comments come shortly after an interview with Fox News late on Monday whereby President Donald Trump said he believed there could be an agreement with China on trade. But he also warned Beijing that his administration had billions of dollars’ worth of new tariffs on standby if it became clear a deal would not be possible.

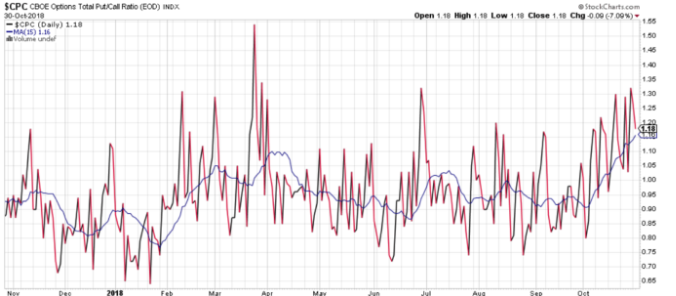

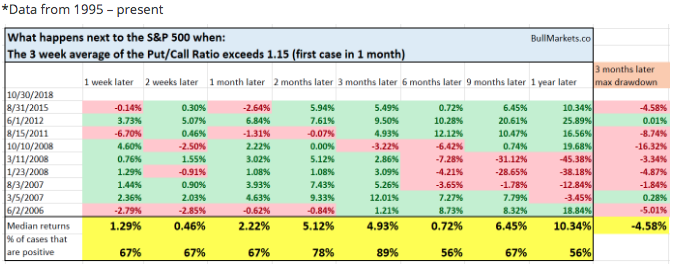

Leading into the market’s rally on Tuesday and as noted within, investor sentiment has been decisively poor. The Total Put/Call Ratio’s 15-day moving average (3 weeks) is now at 16.

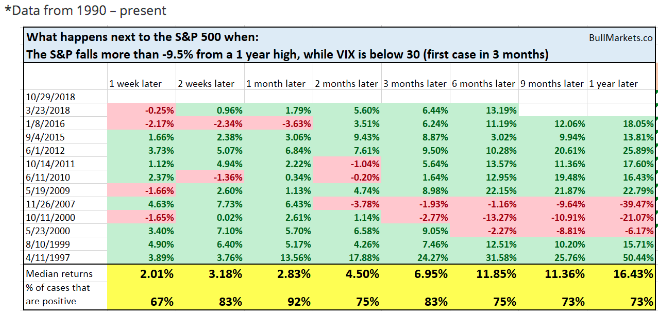

While history may not necessarily prove a guide this time around, the historical data suggests this has been a strong setup for a rally over the next 2-3 months for the equity markets. (See table below provided by Troy Bombardia)

It has remained a source of consistent consternation during the October stock market correction as to the VIX’s response to the selling pressure. During the correction, the VIX seemed to peak at roughly 28%, it has since reached that level once again, but failed to achieve the 30% or above level, as it did during the February market correction.

While a level above 20% signals elevated fear in the market place, the orderly nature and/or slow bleeding of the market has seemingly aided in maintaining the VIX at or below 25% during the market pullback. What we can extrapolate from the VIX during this market drawdown is that the majority of investors were either well prepared for the drawdown or acted in advance of it, by placing hedges as we saw in September. Recall, during the month of September and as the SPX was hitting record-level highs, the VIX was also rising; this is the expression of hedging activity that persisted during September.

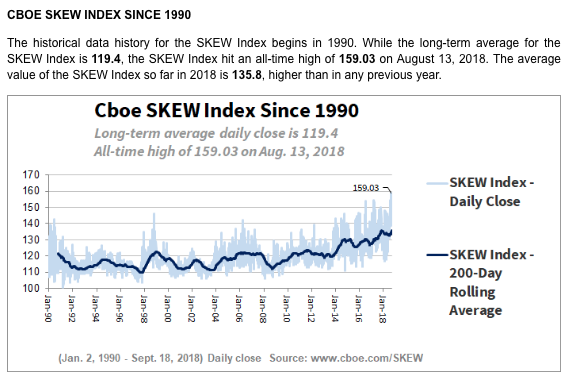

Two factors/index that showed possible stresses for the market were brewing during the month of September were Volatility Dispersion near record-lows and the SKEW Index at record highs. Recall that in September, the SKEW Index hit an all-time high. For the first time ever, on Tuesday, September 18, the CBOE SKEW Index closed above 150 for four straight trading days. The value of SKEW increases with the market’s anticipated tail risk of S&P 500 returns. If there were no tail-risk expectations, SKEW would be equal to 100. (Cboe’s FAQ on the SKEW Index) Back in September, CBOE offered the following commentary on the elevated SKEW Index:

“A recent headline in Bloomberg stated a “Surge in Black-Swan Hedging Casts Shadow Over U.S. Stock Rally,” and noted the Cboe SKEW Index near all-time high underscores hedging demand. The story suggested, ”Elevated levels could also reflect lack of demand for calls” ….‘This has everything to do with trade risk in my view,’ said Dennis DeBusschere, the head of portfolio strategy at Evercore ISI.”

The warning signs for the market ahead, back in September, were largely there for investors to consider. Finom Group was alerting subscribers to the potential market headwinds in it’s weekly research reports. Having already expressed a 10% correction in the major averages, here is what happened to the S&P 500 when it fell more than -9.5% from a 1 year high, while VIX was below 30 (first case in 3 months).

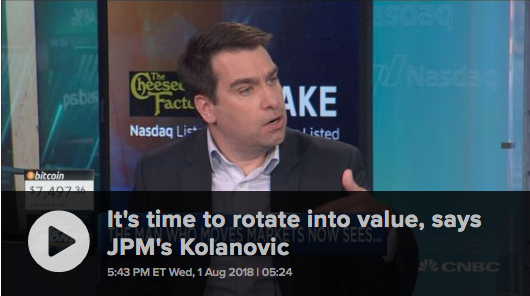

As October gives way to November, typically a strong month for equities, J. P. Morgan’s head of quant trading and strategy suggests an equity market “squeeze” may be afoot.

“With investors positioned defensively, and leverage rapidly coming out of system, there is an elevated risk of market reversion into year-end. Investors should keep this risk in mind – namely that an October ‘rolling bear market’ turns into a ‘rolling squeeze higher’ into year-end.”

Possible drivers of the “short squeeze” include asset managers who have to rebalance and increase equity exposure, a likely surge in buyback activity that could hit $200 billion through the end of the year, and a drop in volatility. “Active managers whose performance has languished this year also may need to window-dress heading into year’s end, which could result in more stock buying.”

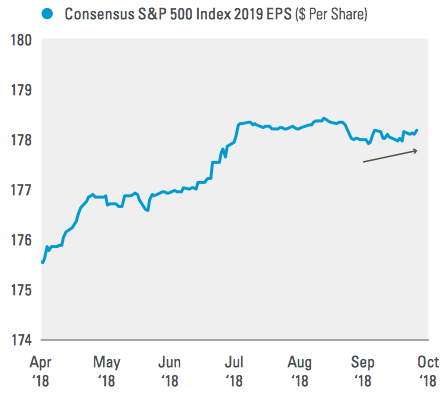

Also in a recent CNBC interview, Richard Bernstein, an Institutional Investor hall of famer stated that we are nowhere near a bear market, despite the poor market sentiment that has persisted throughout October. Bernstein points to corporate earnings strength for his continued optimism in the bull market that he sees lasting well into 2019. The following chart serves to underscore Bernstien’s belief that corporate earnings will continue to drive the bull market higher in 2019.

Despite all the anxiety surrounding corporate profits or peak earnings, consensus now expects a 25.2% increase in S&P 500 earnings per share in the third quarter, above the 24.9% pace in the second quarter (Thomson Reuters data). Estimates for the next four quarters have also been faring better, falling only 0.2% since earnings season began, despite many companies citing tariff costs. Estimates for 2019 have actually inched higher during the month of October, which is surprising given the market reaction to some of the earnings shortfalls over the past couple of weeks. In other words, Bernstein is following exactly what the market follows over time, earnings. Fits and starts in the market are a natural part of any bull market cycle; October’s swoon is nothing new, even healthy in many respects.

With Facebook’s (FB) quarterly results having now been released and all of FANG in the rear view window, the market can focus on Apple’s (AAPL) results come Thursday. Amazon, Alphabet and Netflix may all find dead-cat bounces near-term and provide the market with some much needed, market cap weighted support. But “make no never mind about it”, so to speak, the market is not out of the proverbial woods.

During times of market strife, which may not yet be over, investors can find difficulties with focusing on the bigger picture, the long-term market potential. Despite stock markets getting crushed in October, strategists say not only are sell-offs like this normal, they create opportunities for savvy investors.

“Warren Buffett’s not panicking,” Michael Farr, president and CEO of Washington, DC-based wealth management firm Farr, Miller & Washington told CNBC. “It’s a bucket of cold water but take a deep breath and know these things happen — let it work itself out.”

With that being said, let’s all hope to find some further strength in the economic data of the day. On the data front, ADP employment figures for October are scheduled to be released at around 8:15 a.m. ET. Investors are likely to keep an eye out for third-quarter employment cost index data at 8:30 a.m., before Chicago PMI data for October is released later in the session. As always, Finom Group will trade what the market delivers and hope you join us by subscribing to our valued trade alerts. Oh, and have a safe and happy Halloween to all!