Welcome to this week’s State of the Markets with Wayne Nelson and Seth Golden. Please click the following link to review the SOTM video. In this week’s episode we discuss October markets and nearly touching the former S&P 500 all-time high on Friday. Our dialogue this week aims to rationalize the numerous headlines while recognizing the impact on financial markets. Economic data has been strong for housing all year long while Markit and ISM manufacturing and services data has weakened. Amazon results have far reaching implications for the retail industry that have yet to be recognized in the equity market retail sector. Looking ahead, we find the coming week loaded with earnings releases, economic data and the FOMC rate announcement. Please review the supporting graphics and bullet points that accompany our State of the Markets video!

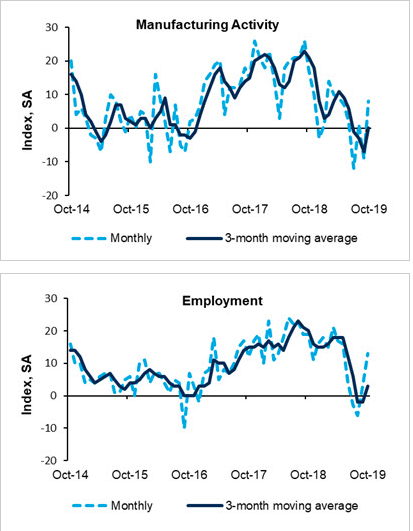

- Fifth District manufacturing activity strengthened in October, according to the most recent survey from the Federal Reserve Bank of Richmond. The composite index rose from −9 in September to 8 in October, as all three components — shipments, new orders, and employment — increased. Manufacturing firms also reported an increase in backlog of orders and improved local business conditions. Respondents were optimistic that conditions would continue to improve in the next six months.

- After last week’s reading was revised higher, this week’s reading on jobless claims saw a decline from 218K down to 212K compared to forecasts of 215K. With this reading, jobless claims remain at healthy levels and are well within the range of the past several months. Claims have now spent 241 consecutive weeks at or below 300K and 106 weeks at or below 250K. Both are record streaks.

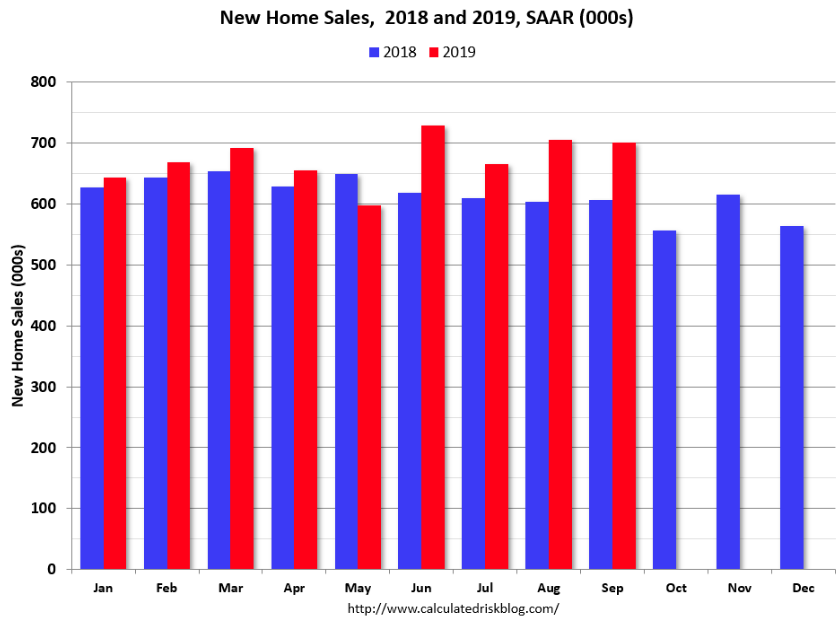

- Sales in September were up 15.5% year-over-year compared to September 2018.

- Year-to-date (through September), sales are up 7.2% compared to the same period in 2018.

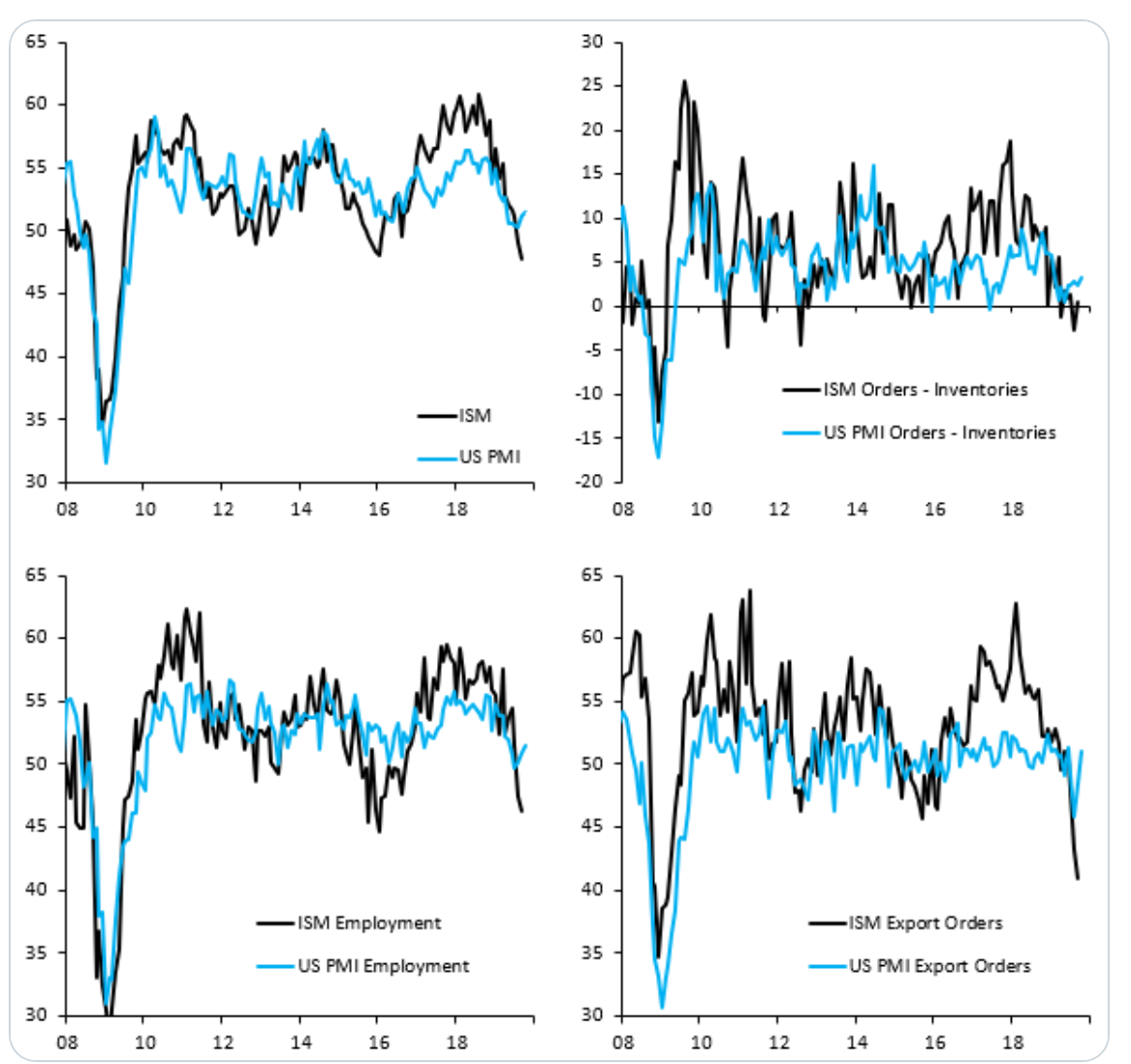

- Robin Brooks: “One of our consistent push-backs on recession fears is that weak manufacturing data are just the usual up and down in the sector, as an inventory overhang is worked down. That’s where today’s US manufacturing PMI points. Look at the rise in orders – inventories and export orders”

- “The Markit PMIs for October, reported this week, are consistent with growth slowing a little further in the fourth quarter, but also suggest that the downturn may be close to bottoming out.”

- Fed officials are likely to say this is the end of the “mid-cycle” adjustment that Chairman Jerome Powell alluded to in July, the bank predicts.

- In addition, the central bank could remove the language stating it will “act as appropriate to sustain the expansion” that has been in play since June.

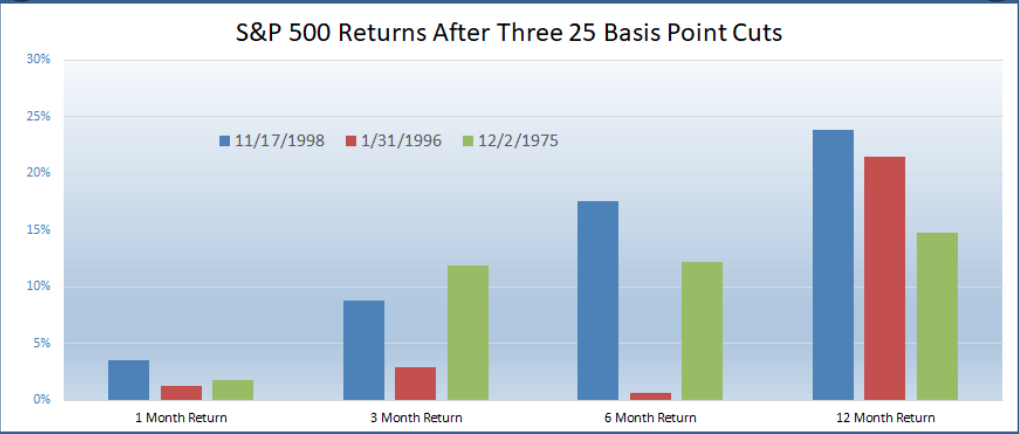

- The first Fed rate cut in ’01 and ’07 was 50 basis points. Almost like they knew there was more trouble under the surface.

- This cycle is looking like 3 consecutive 25 basis point cuts.

- The S&P 500 on a total return basis is set to close at an all-time high today. There are a lot of worries and concerns, but this it a bit of good news for those investors who didn’t panic over every 5% pullback we’ve seen the past decade.

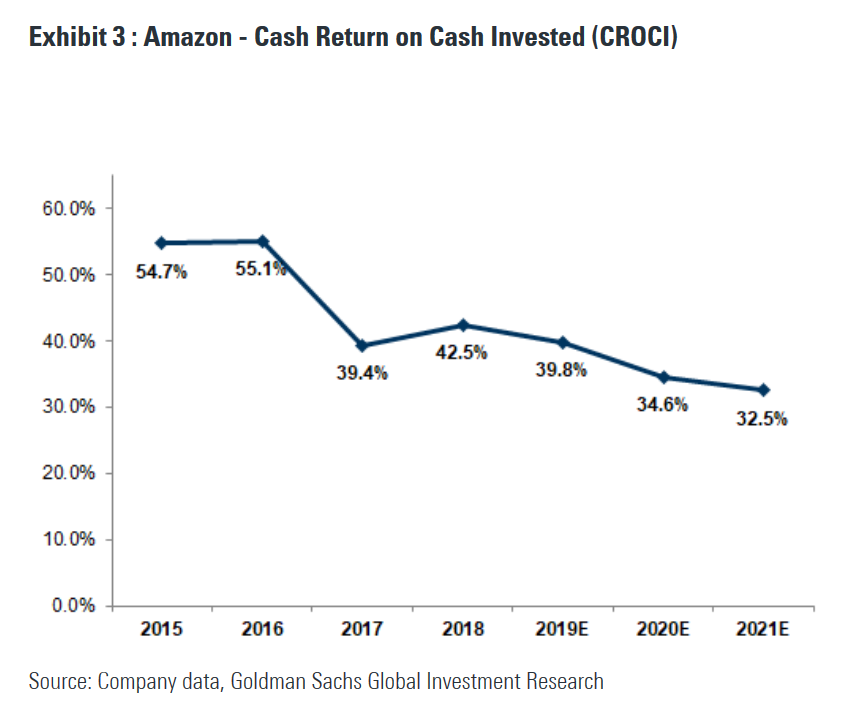

- Goldman Sachs: We revise our 2019-2021 revenue/adj. EBITDA estimates -1% / -5% per year

- Our price target (12-month) goes to $2,200 from $2,350

- we continue to believe AMZN represents one of the best risk/rewards in Internet and remain Buy-rated

- JPM: We’ll Take The Trade-Off of Lighter Profits for Higher Revenue—Amazon’s Earned It; We’re Buying the Pullback, PT $2,200

- Overall, we like AMZN’s strategy w/P1D as it raises the bar in e-commerce yet again & accelerates the top line, even at the expense of profitability.

- No company we cover has earned the right to invest more than AMZN, & we’d be buying the pullback in shares.

- Our $2,200 PT is based on 1.5x 2020E Retail GMV of $433B and 15x AWS EBITDA of $27B.

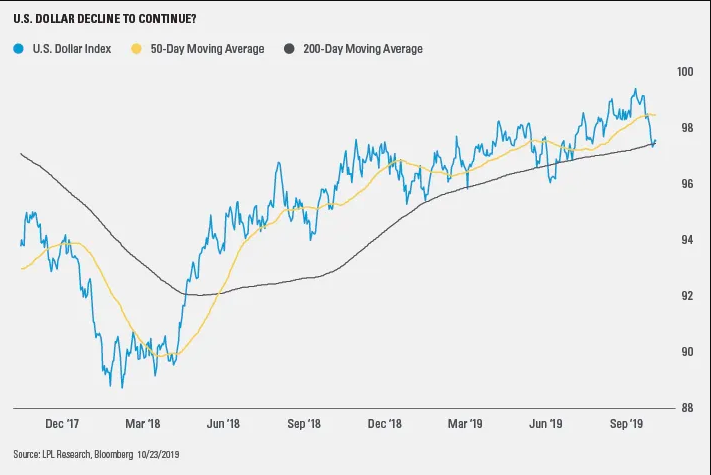

- We would view further dollar weakness as a reflection of better global growth and an improved global trade environment, clearly positive developments. But don’t expect a collapse. The greenback remains the world’s reserve currency and will likely remain so for decades to come. The U.S. economy remains the biggest and most productive in the world, making it a very attractive destination for international investment dollars.

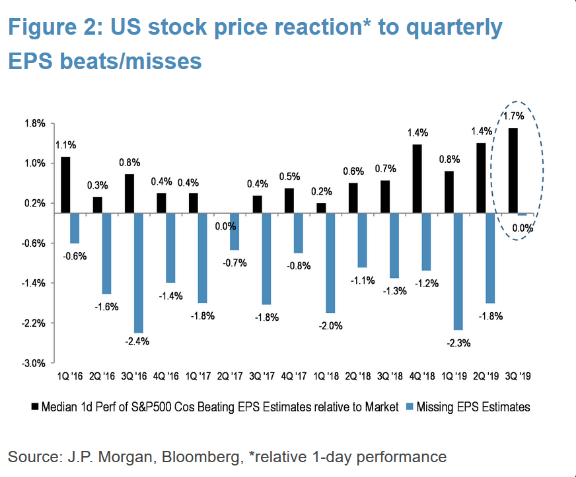

- Beat rates have been fine, but guidance has been a major problem the last few days as we’ve entered the heart of earnings season. 36 lowered guidance to just 17 raised over the last 2 days, more than 2 to 1 to the downside. Big negative shift from recent quarters.

- 1. US: 82% of S&P 500 companies beat EPS estimates. Out of the sample that has reported so far, EPS growth is running at +2% y/y, surprising positively by 5%.

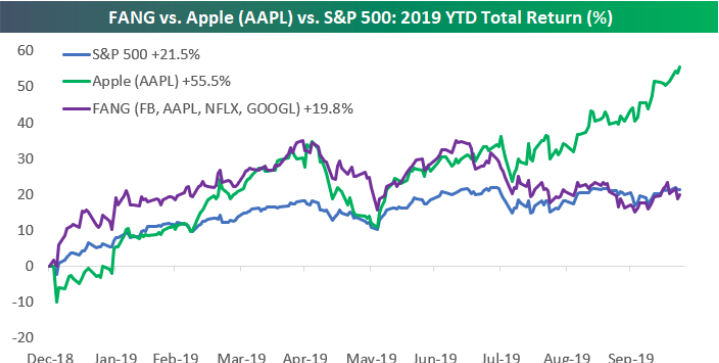

- Tech has had a terrible quarter as expected because of the cyclical slowdown and the trade war. Bad news is only 13% of these firms have reported. We still need to get through most of them. Biggest one is undoubtedly Apple which will report results on October 30th.

- Binky Chadha of DB: Following persistent downgrades (-10% over 12 months for the S&P 500), Q3 earnings are beating at a slightly above average historical rate.

- Muted reactions to misses but strong reactions to beats suggests the slowdown was well priced in.

- Forward estimates continue to fall, but remain high relative to expectations for macro growth. Global growth forecasts point to earnings growth in the low- to mid-single digits for next year, well below the double digit rates projected by the bottom up consensus

- S&P 500 Value Index just made a new all-time high.

- In the past, when it broke out to a new all-time high for the first time in 200+ days, the S&P 500 Value Index always went higher 6 months later.

- Growth vs. Value back below 200-day moving average for the first time since Jan 2019.