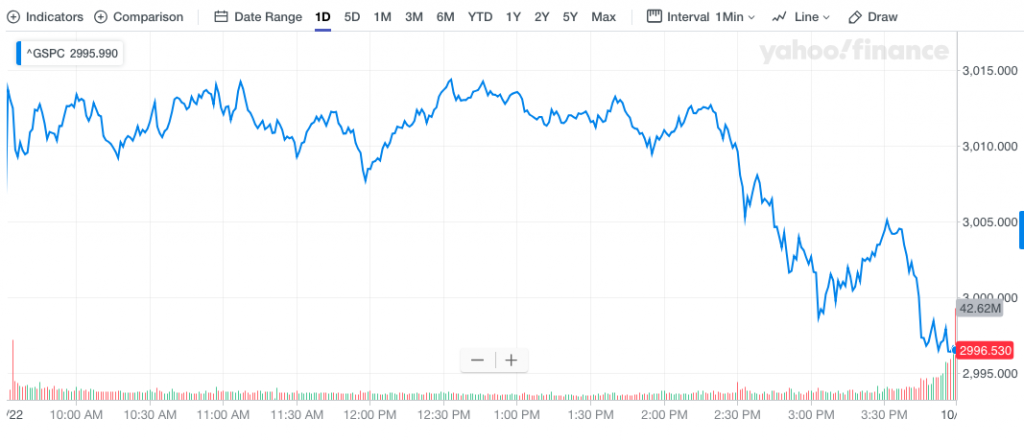

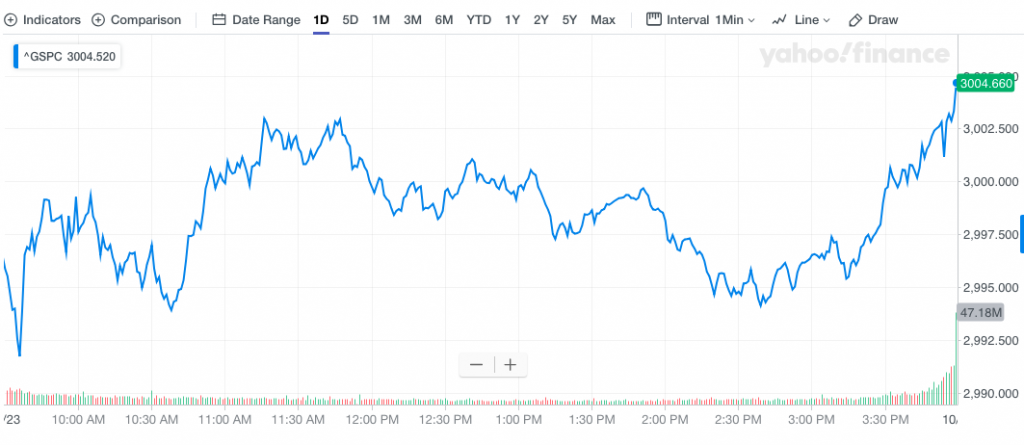

Chop, chop, chop…, no better way to describe the last 2 trading days on Wall street as the S&P 500 (SPX) finds itself with sputtering above the 3,000-level and during the peak of earnings season. Nonetheless, when we compare Wednesday’s SPX chart with that of the previous session, the market is still favoring the bulls. Tuesday, the S&P 500 fell into the closing bell…

…, but on Wednesday we witnessed a very different move into the closing bell and leading up to the release of Microsoft’s (MSFT) Q3 2019 earnings release.

With many of the mega-cap Dow Jones Industrial Average (DJIA), S&P 500 and Nasdaq (NDX) companies failing to achieve analysts estimates earlier in the morning Wednesday, the market seemed to shrug off the lesser quarterly reports in favor of the notion of potential troughs in the economic and earnings cycle. Caterpillar said it earned $2.66 per share in the third quarter, versus the Refinitiv consensus estimate of $2.88 per share. Revenue came in at $12.758 billion, while Wall Street expected revenue of $13.572 billion. The Company lowered its full-year earnings per share forecast to a range of $10.59 and $11.09, lower than the expected $11.70. The stock closed 1.2% higher, however, after falling more than 6% in the premarket.

Additionally, Boeing shares climbed 1% after the airplane maker said it will stick to its timeline for the return of the 737 Max. That was enough to offset earnings that badly missed analyst expectations. The company reported a profit of $1.45 per share. Analysts polled by Refinitiv expected a profit of $2.09.

Despite weak results from some of the mega-cap stocks, the third-quarter earnings season has largely topped analyst expectations. Of the S&P 500 companies that have reported through Wednesday morning, 81% have posted better-than-expected results, according to FactSet.

Following closely behind the earnings story, which we’ll get back to in a moment, was the surge in the price of crude oil during Wednesday’s trading activity. The EIA reported a draw of -1.699M barrels vs a 2.232M expected, and 9.281M the prior week. Crude has been getting battered lately due to fear of the less demand from the global slowdown and the China-US trade war.In addition, yesterday’s API Weekly Crude Oil Stock showed a rise of 4.45M barrels and OPEC said they would consider reducing production when they meet in December.

All the negative news for crude oil created the perfect storm for a good old-fashioned short squeeze yesterday. After testing the lows of 50.50 five times since the beginning of June, WTI broke a descending trending yesterday and closed above it just below horizontal resistance at 54.90.

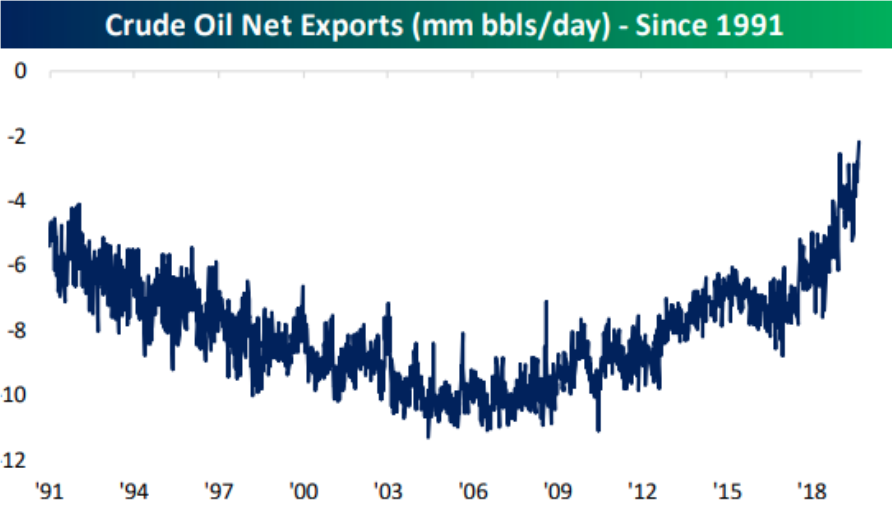

In addition to the surprising draw in crude oil inventories and short squeeze on Wednesday, the EIA report shined a spotlight on the U.S.’ growing energy independence. EIA data showed crude oil imports collapse to their lowest level since 1996. In addition to near-record exports, the deficit for crude is now the narrowest it has ever been in the history of the data going back to 1991. (Chart from Bespoke Investment Group)

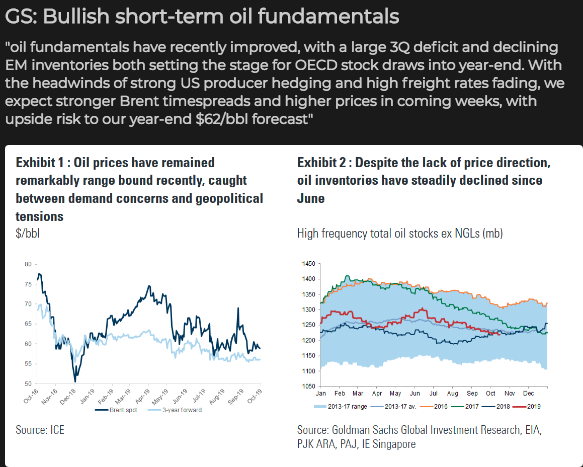

With the price of crude oil rising significantly Wednesday, investors shouldn’t be surprised if the price of “black gold” retraces a bit before finding its “sea legs” once again. Goldman Sachs latest notes confirm their near-term bullish sentiment for crude, but their outlook for 2020 is rather muted.

Despite apparent weakened demand in energy markets, the bank anticipated improving fundamentals would lead to higher prices over the coming months. The firm predicted some upside risk to its year-end forecast of $62 a barrel, as headwinds from U.S. producer hedging and higher recent freight rates fade. At $62, this would provide a tailwind for the energy sector stocks as the average price of crude oil from November-year end in 2018 was in the upper $40 range.

“Nevertheless, absent growth or geopolitical tensions escalating into meaningful shocks, we expect that Brent oil prices are likely to continue trading in 2020 around our $60 (a barrel) forecast,” Goldman Sachs said in a research note published Tuesday.

“The ongoing OPEC cuts and slowing shale activity will offset rising other non-OPEC supply and moderate demand growth next year.”

Reverting back to the equity markets conversation, as Thursday will mark a day of more key earnings reports, investors might consider continued choppiness in the markets. Some of this is a force factor of low market volumes.

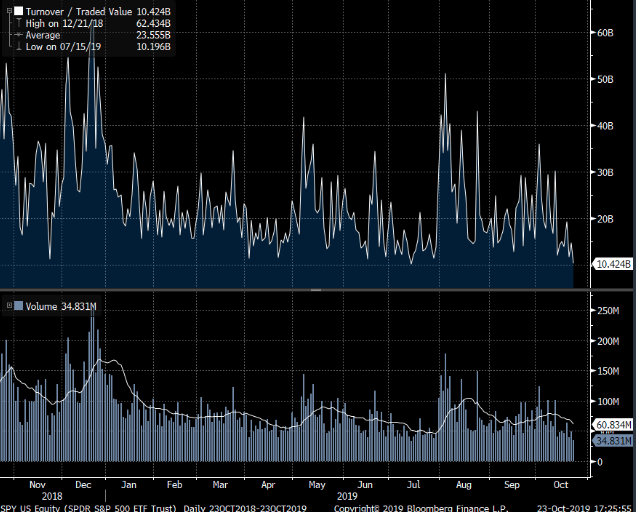

As shown in the chart above, Wednesday was the second-lowest dollar volume traded in the Spiders ETF (SPY) over the past year at $10.4B. The average daily volume is $23.6B. Low trading volumes are a market liquidity concern, especially with the market nearing its former highs and during earnings season. Earnings season tends to produce lesser share buyback activity performed by corporations, even if there is no truth to the so-called “black-out period”. Companies self impose restrictions surrounding buybacks during the period leading up to a quarterly release.

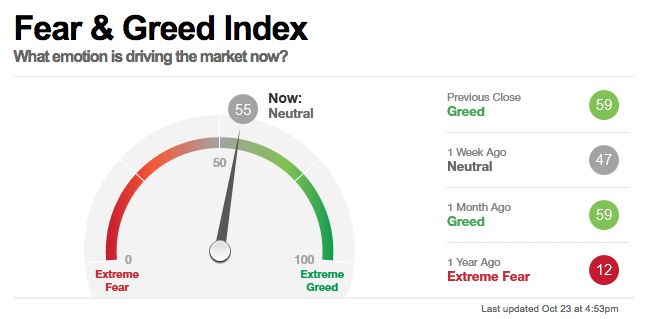

With the S&P 500 now closing above the 3,000-level for the 2nd time this week, investors aren’t finding sentiment or appetite for equities climbing. In fact, when we look at CNN’s Fear & Greed gauge, we see that investors are rather Neutral on risk assets presently.

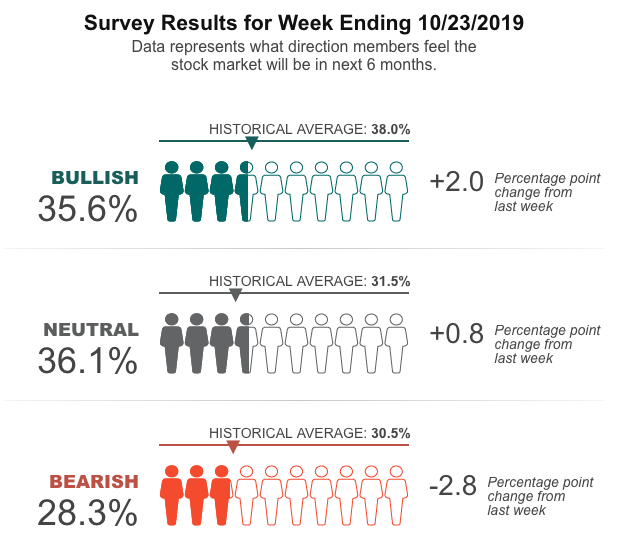

The CNN Fear & Greed index is mirroring exactly what we see in playing out in the market the last 2 trading days, choppy and uncertain directional moves in the market. Nonetheless, when we look at the AAII weekly investor sentiment survey, it has improved for the second consecutive week. Improved if your bullish on risk assets at least. The bearish sentiment took another small leg lower while bullish sentiment mirrored this move to the upside.

While bullish sentiment rose last week, it still resides below the historical average. Investor sentiment has remained rather subdued throughout 2019 and with economic policy uncertainty at peaks last seen in 2016. In no way, shape or form has the year-to-date market rally been one dominated by over exuberance and/or found for offensive positioning. In fact, our latest look at the growth vs. value technicals show that the Growth vs. Value chart is back below the 200-DMA for the first time since the beginning of 2019.

Another way to view the move into value and away from more risky sectors of the market is through the iShares S&P 500 Value ETF (IVE). The IVE has outpaced the broader market by a wide margin in recent weeks and as of yesterday it was on track to beat the broader market for the week, month and three-month period, with an outside shot of eclipsing year-to-date gains for its rival iShares Russell 1000 Growth ETF (IWF) should the trend extend.

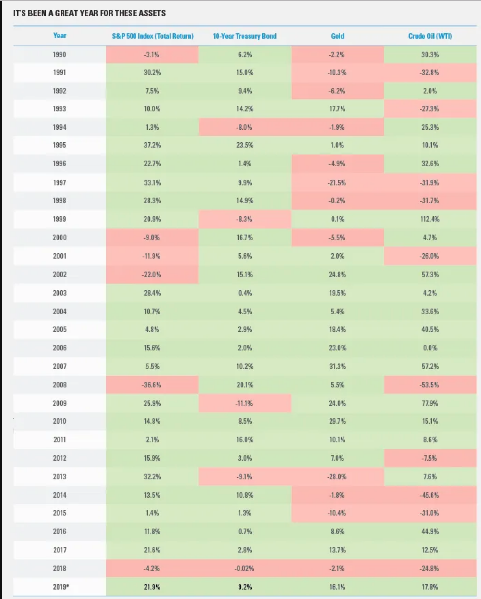

The rally in value for 2019 has come amid a strong advance in bonds, gold and equities, which are all expressing outsize year-to-date gains, usually coinciding with losses for gold. Indeed, 2019 is proving a complete reversal of asset class performance in 2018. Last year was the first year since 1969 in which both the S&P 500 (stocks) and bonds both finished the year with a negative return. Toss in the fact that gold and crude oil were both down last year, and it was one of the worst years ever for a diversified portfolio.

“As bad as last year was for investors, 2019 is a mirror image, with stocks, bonds, gold, and crude oil all potentially finishing the year up double digits for the first time in history,” explained LPL Senior Market Strategist Ryan Detrick.

As shown in the LPL Chart of the Day, it has been a great year for stocks, bonds, gold, and crude oil. With more than two months to go in 2019, but this year is shaping up to be one of the best years ever for these four important assets.

Everything being on the rise isn’t necessarily a bad thing, especially if the U.S. Dollar continues to weaken through year-end. Having said that, a mor bullish market environment would likely be signaled from a rotation out of value and back into growth. The headwind for this rotation, however, has largely been centered on FANG, which continues to find certain of the stocks with either slowing growth and subscriber performance (Netflix) and Federal probes/regulatory scrutiny (Facebook, Google and Amazon).

Neil Dwane, global strategist at Allianz Global Investors, who says investors are leaning more on that old favorite Microsoft Corp., as regulatory wagons circle around some popular names in the tech, internet and media space.

“I think the momentum behind Facebook and Alphabet is constrained by tax regulation in Europe and by the Justice Department investigations into their monopolies which will end up with them being broken up. And obviously Apple is constrained by the fact that its new business model is to undercut everyone from Disney to Netflix..and to cut their iPhone prices by 35%.

We’re now seeing tech is splitting into enterprise software names like Microsoft. I think the chip names, while buoyant, are very, very sensitive to the atmosphere around China and trade and the FAANGy names that have moved into media and consumer services have just got regulation written all over them. Therefore I think many investors are not inclined to chase those companies at the moment, in that environment.”

Nope! This is what we call focusing on the noise, as the earnings growth creates lasting opportunity. That opportunity of constrained value in the FANG names may prove fleeting near-term should the FANG stocks, set to begin reporting this week, prove to outperform analysts’ expectations.

More broadly speaking, and as we head into an extremely busy day for markets and investors, the market seems to be on solid footing and a steady march higher. Not so fast says Capital Wealth Planning’s Jeffrey Saut! The wealth manager is on watch for a near-term hiccup that produces a market pullback.

“My very short-term trading indicator did flash a sell signal. We just on occasion try to make these tactical trading calls, and the market looks a little tired here. The pullback is probably going to be contained to the 2,930 to 2,950 level.

“Secular bull markets tend to have three phases in them. I think we’re in the second phase. I think it began in February of 2016. It is always the longest and the strongest. You should be fairly fully invested here even if you’re going to get a small wiggle on the downside.”

Saut still believes there’s at least seven years left in the bull market. He expects low interest rates coupled with stronger quarterly earnings to push the S&P 500 to at least 3,400 next year.

U.S. equity futures are pointing to a higher open on Wall Street, but of course, that could be altered as earnings and economic data roll-out ahead of the opening bell. Investors are awaiting New home sales, Initial Jobless Claims, Durable goods and Markit PMI data this morning. Alongside the economic data deluge, here is a snapshot of key corporate earnings releases for Thursday:

While we’re all focused on earnings season and the onslaught of economic data, least we not forget about geopolitical headlines that have roiled markets all year-long. On Thursday investors might prove cautious ahead of another V. P. Pence speech on White House policy. Vice President Mike Pence will deliver a policy speech concerning China Thursday morning. The topic is expected to be broad, reflecting on the US.-China relationship over the past year and looking at the future of the relationship. Pence has often spoken quite hawkishly about China, but given the desperation for some sort of trade agreement that has become evident he might tone it down a little this time. We’ll see!