Welcome to this week’s State of the Markets. Please click the following link to review the SOTM video . Our emphasis in this week’s SOTM video concerns the overextended bond market rally and potential consequences that could create additional equity market volatility, underlying economic data that continues to outline the strength of the consumer and trend-growth GDP pace and what investors need to consider now that the market has retraced some 6.5% in the last two weeks.

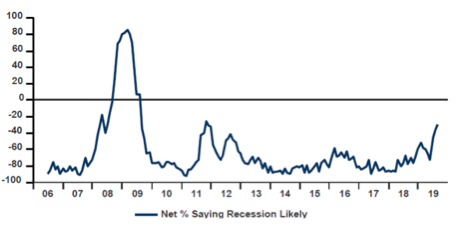

- 34% of FMS investors think a recession is likely in the next 12 months, the highest recession probability since Oct’11. Similar to BofAML U.S. economists that think there is close to a 1 in 3 chance of a recession in the next 12 months.

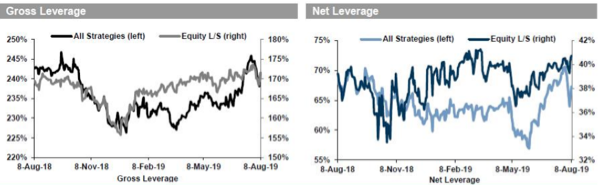

- The overall GS Prime Brokerage book was net sold for the first time in nine weeks

- Gross leverage of the overall book decreased -0.9 pts to 241.6% (77th percentile one-year) and net leverage decreased -1.4 pts to 67.3% (80th percentile).

- North America’s weight vs. the MSCI fell -1.9 pts to -1.2% underweight… Since GS began tracking the data (Oct ‘07), the GS PB Book has only been underweight North America three times: Feb ’08, Nov ’17, and this week.

- “Low unemployment, rising real wages, moderate energy prices, the surge in mortgage refinancing and the 7.3 million job openings firms are still desperate to fill — all suggest that consumers will continue to spend enough to contribute to GDP growth even as businesses retrench.”

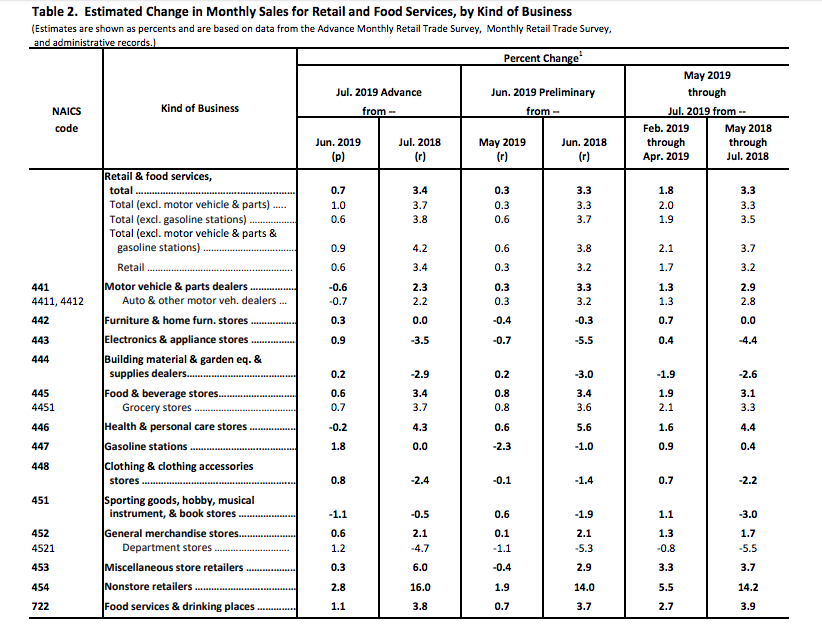

- July retail sales rose .7% MoM and 3.4% YoY. Dept. Store retail sales rose 1.2% MoM but fall 4.7% YoY. Nonstore retail sales continue to syphon sales from brick & mortar retailers, growing 2.8% MoM and 16% YoY.

- We suspect some growth was pulled into July at August’s expense. After all, Prime Day was a big driver of sales. Non-store retailing exploded 2.8% in July. Still, ex non-store retailers, core sales rose a respectable 0.4% and up 5.1% annualized over the last three months.

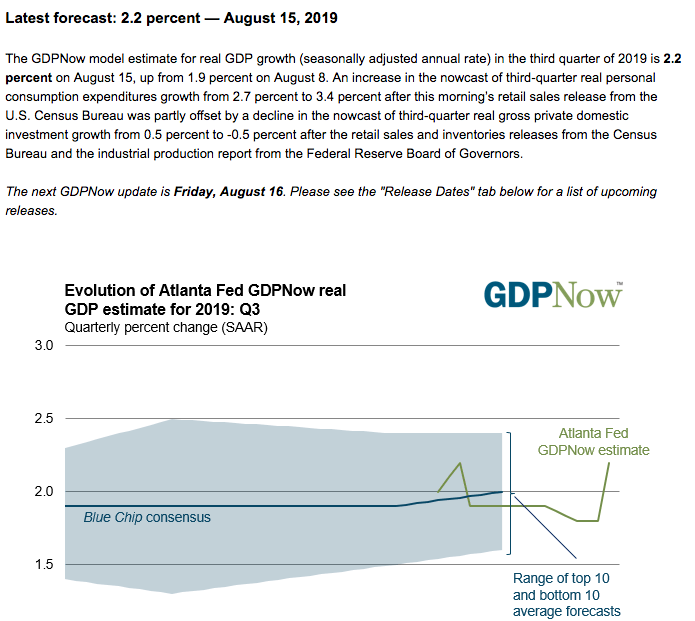

- Following today’s data deluge, Goldman boosted its Q3 GDP tracking estimate by two tenths to +2.1%

- Merrill: “The data boosted our 3Q GDP tracking estimate by 0.4pp to 2.1% qoq saar. 2Q was unchanged at 1.8%.”

- Very light economic calendar next week. FOMC and Housing industry related data highlight the week.

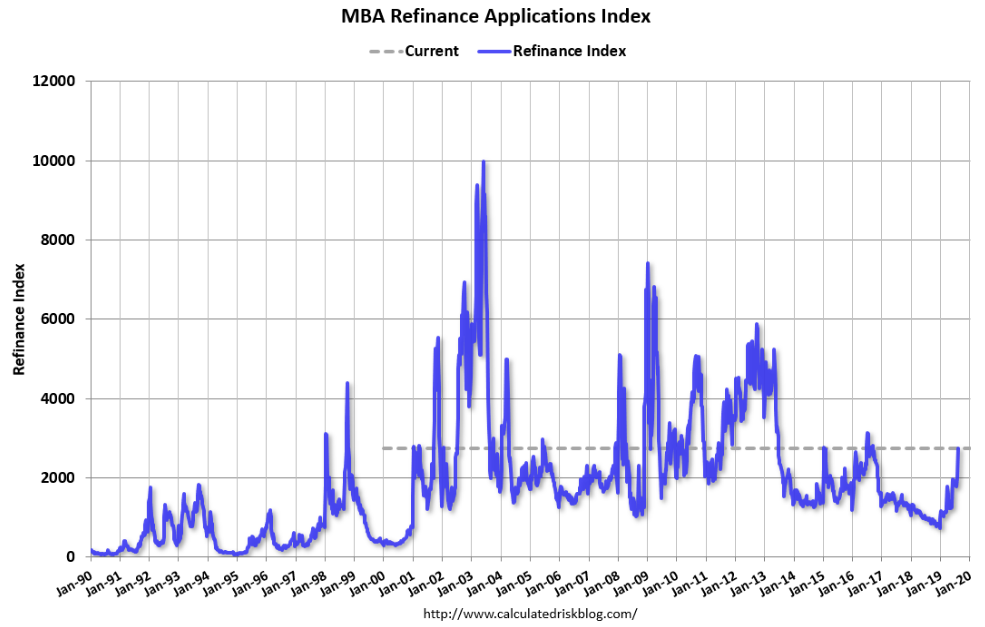

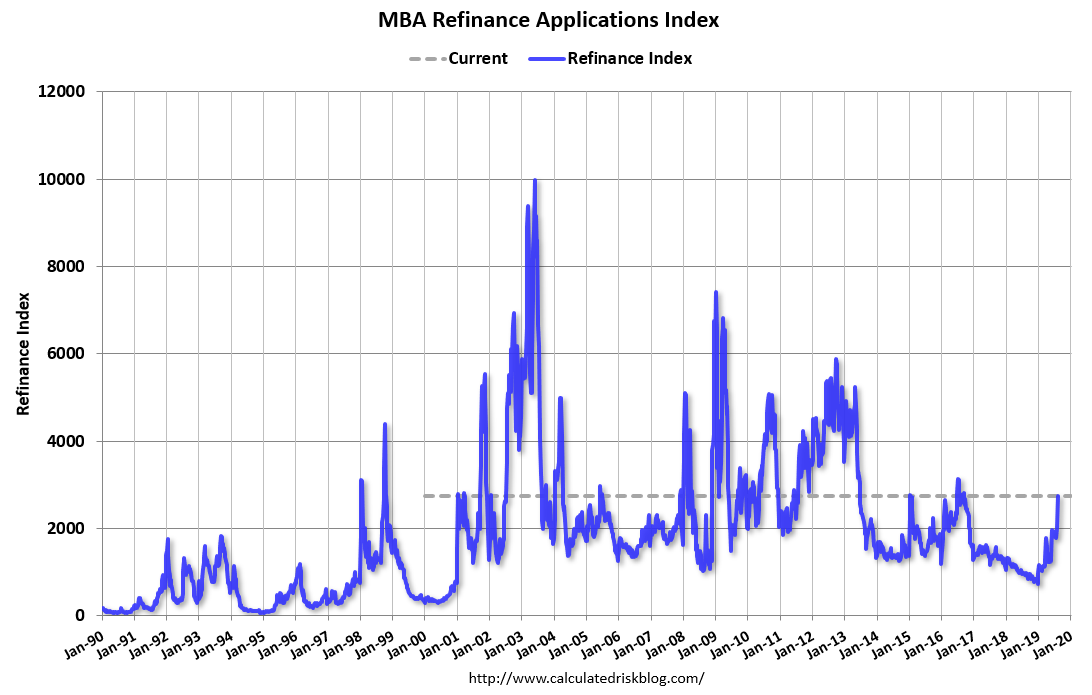

- 37% jump in refinance volume for the week, the highest level since July 2016. Refinance applications were nearly 196% higher than a year ago.

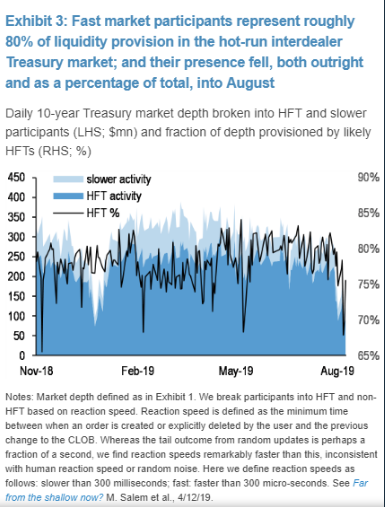

- Behind the wild swings in Treasurys? Diminishing liquidity, potentially caused by ultrafast traders pulling back this month, JPMorgan says.

{kind=link}