Welcome to this week’s State of the Markets. Please click the following link to review the SOTM video. In this week’s episode we discuss the domestic political strifes that are overflowing into the equity markets. While the economic data is supportive of trend-growth and stable earnings, the market has been whipsawed all week long from headlines related to global trade and the announced impeachment inquiry. Our dialogue this week aims to rationalize the numerous headlines while recognizing the impact on financial markets.

- The White House is weighing some curbs on U.S. investments in China, a source familiar with the matter told CNBC. This discussion includes possibly blocking all U.S. financial investments in Chinese companies, the source said.

- It’s in the preliminary stages and nothing has been decided, the source said. There’s also no time frame for their implementation, the source added.

- Restricting financial investments in Chinese entities would be meant to protect U.S. investors from excessive risk due to lack of regulatory supervision, the source said.

- The deliberations come as the U.S. looks for additional levers of influence in trade talks, which resume on Oct. 10 in Washington. Both countries slapped tariffs on billions of dollars worth of each other’s goods.

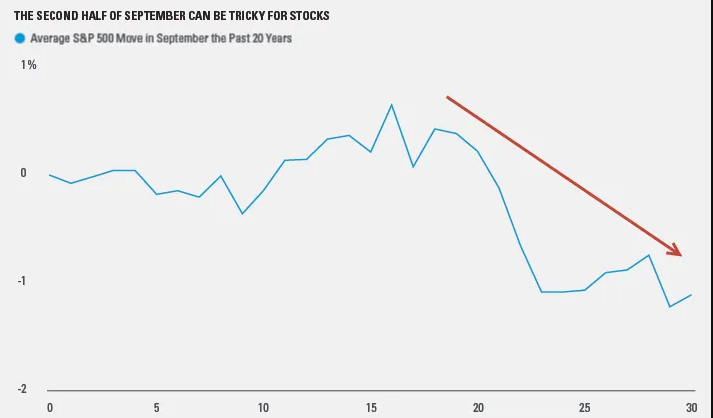

- “According to historical calendars, we may need to be on high guard for the second half of September, suggests LPL Financial and with regards to the following seasonal chart.

- Bespoke Investment Group uses a Seasonality Tool, suggesting a similar outcome as LPL Financial for week (9/20-9/27). Their Seasonality Tool suggests that the final week of September has been one of the worst times of the year for the S&P 500 over the last 10 years:

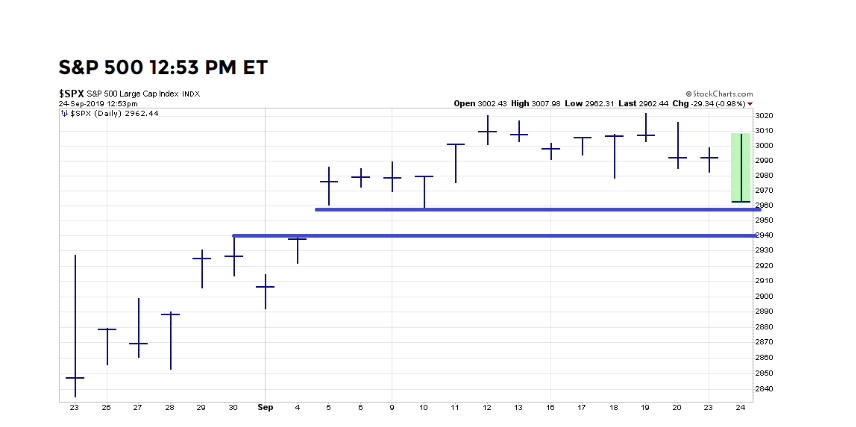

- This is more a colloquialism than truism, but the vast majority of gaps do indeed get filled. In the chart above, we see the current gap to be filled lay between 2,957 and 2,940.

- Seasonality, impeachment inquiry and U.N. General Assembly headlines are all just market noise that may impact the market trajectory near-term, but earnings guide the market long-term.

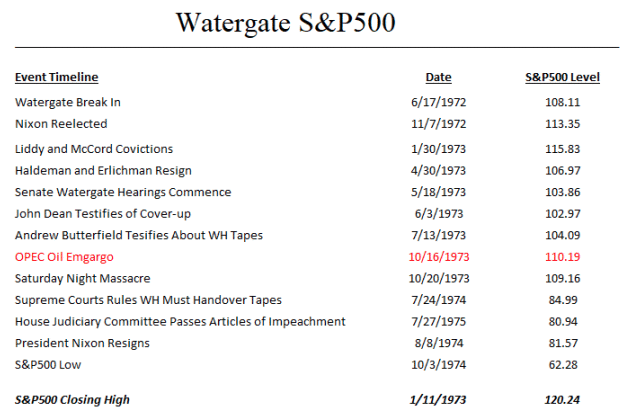

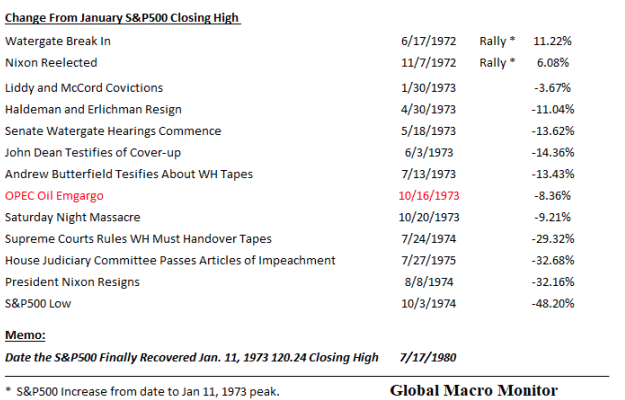

- Market has only 2 impeachment examples for which to draw performance expectations. The market fell sharply in 1973-1974 during the Nixon impeachment hearings mainly due to the oil embargo.

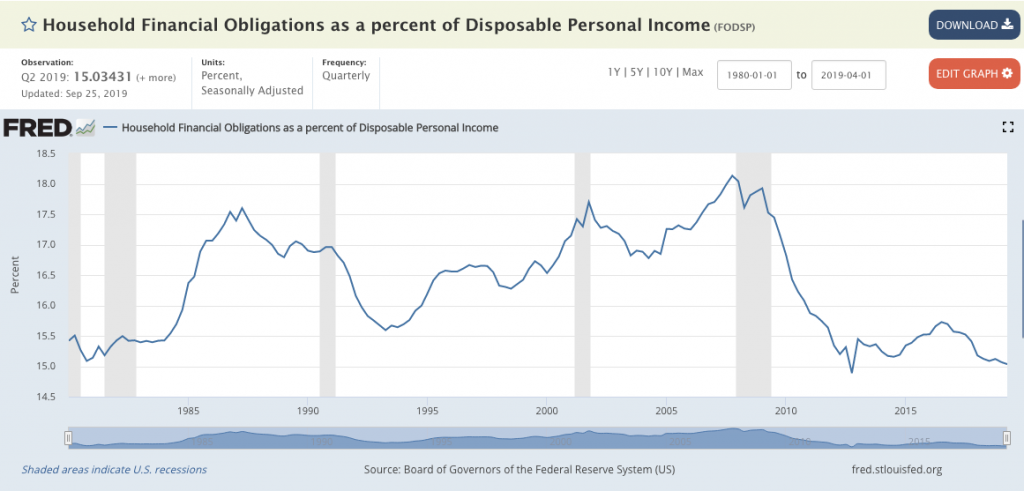

- The U.S. household balance sheet remains at its best levels since the 1970s with higher wages, and disposable income.

- The higher savings rate identifies a difference from previous recessions.

- Throughout history, the Personal Savings Rate is usually falling. The current expansion cycle is unique in that the personal savings rate has largely risen since the beginning of the economic expansion in 2009.

- Most people are not familiar with recession causation and trading during a recession and through a recession.

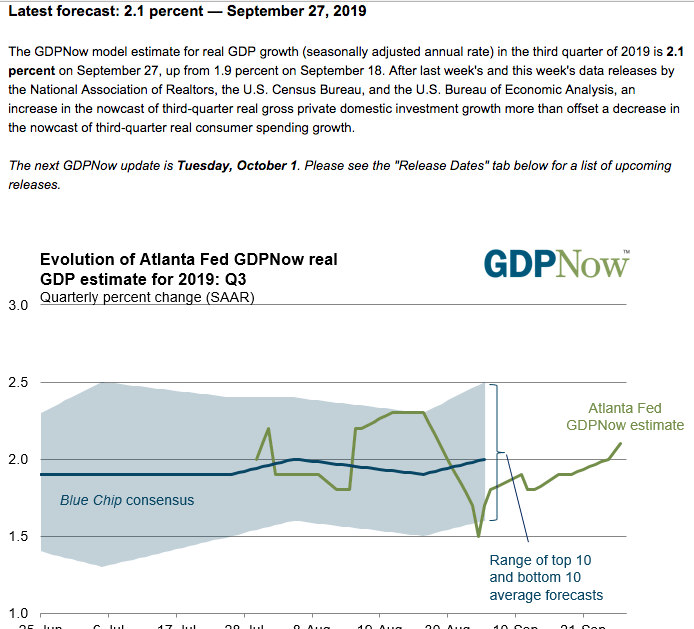

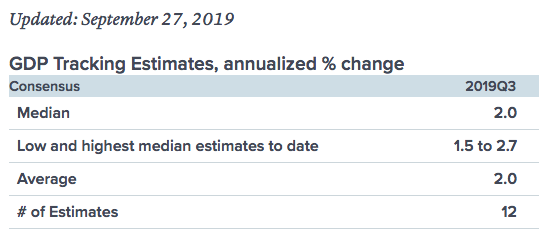

- From Merrill Lynch: The data sliced 0.3pp from 3Q GDP tracking, bringing us down to 1.9% qoq saar. [Sept 27 estimate] emphasis added

- From the NY Fed Nowcasting Report: The New York Fed Staff Nowcast stands at 2.1% for 2019:Q3 and 1.8% for 2019:Q4. [Sept 27 estimate].

- Impeachment may not take place in the Senate, even if Congress passes.

- Impeachment headlines likely to persist through October.

- White House Administration officials such as Attorney General Barr are likely going to be called to testify before congress.

- The White House Administration is likely going to attempt to distract the public from focusing on impeachment inquiry headlines.

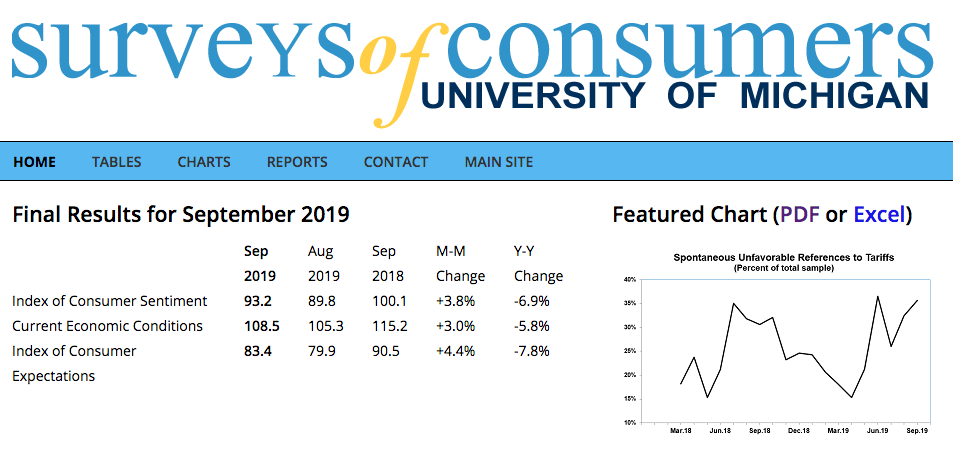

- University of Michigan Consumer sentiment rose during the latest period.

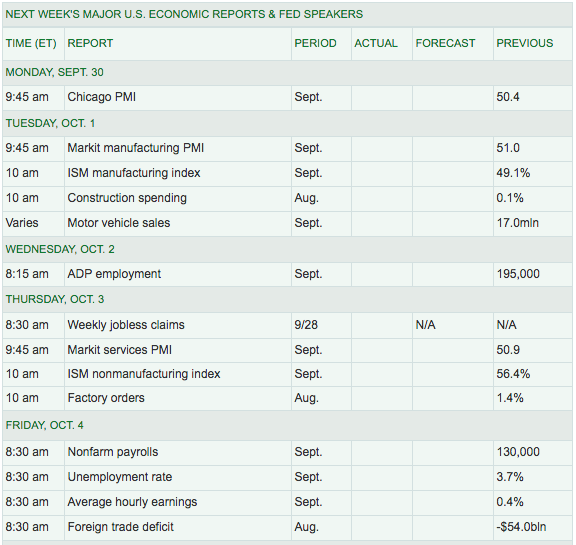

- Next week’s economic data will be critical to the markets.

- ISM manufacturing data is due out next Tuesday and to end the week investors will be delivered the monthly Nonfarm Payroll data.

“All year, markets have remained surprisingly resilient in the face of troubling developments, both domestically and internationally. Most recently, we’ve seen volatility in oil prices, policy disagreements within the Federal Open Market Committee (FOMC), the rate-setting arm of the Federal Reserve, and liquidity problems in very short-term fixed income markets. These developments come on top of ongoing uncertainty created by U.S.-China trade tensions and other geopolitical risks.

The S&P 500 has quickly bounced back from each news-driven decline and is up 19% year-to-date, near record highs reached earlier this year. While some investors see this resilience as cause for bullishness, I remain cautious. Important questions loom. Below are three new areas of concern that may well lead to more volatility.

- Oil market disruption: Attacks on Saudi Arabia’s oil fields led to concerns about supply risk and caused a large one-day spike in the price of oil, which then retreated, as investors were reassured that a long-term shock to oil prices was unlikely. Is it really that simple? I think Middle East tensions are intensifying and related oil market dynamics are complicated. Further oil market disruption is a possibility.

- Lack of unity on Fed: The FOMC voted to cut rates again at its mid-September meeting, as expected. But there was an unusual lack of consensus. Three members dissented. This is one reason that volatility in interest rates has spiked. Since September 1st, the benchmark 10-year Treasury yield has rapidly climbed from 1.4% to 1.9%, and then retreated to 1.75%. Those are big swings for bonds.

- Upheaval in money markets: The very short-end of the bond market has been even more turbulent recently. An overnight lending rate spiked and the Fed had to step in to restore liquidity to the so-called repo market. While this was a technical problem more than a problem in the banking industry, it does make me wonder why the Fed didn’t anticipate this event and what it will do if it can’t control short-term interest rates in the future.

While at the index level, U.S. markets may seem calm lately, a lot of turmoil lies just below the surface. The good news is that diversification is working: When Treasury prices fell, stocks rose, sheltering investors who own both asset classes.

Investors should strive to be highly diversified by asset class, geography and sector, favoring active management and high quality, income-producing securities that are more likely to hold up if complacency fades. The fact that the stock market is shrugging off the latest round of macro risks this late in the business cycle makes me cautious, not bullish.”