Apple & Tesla Earnings on Deck

The June quarter is typically dubbed Apple’s (AAPL) most boring and uneventful quarter with most consumers awaiting the next product launch that coincides with the September quarter. The June quarter tends to be Apple’s smallest in terms of revenue and iPhone sales. Apple Inc. will report its most boring quarter of the year Tuesday after the closing bell.

Given the modest expectations for the quarter to be reported, investors are likely to be watching and listening for any commentary or indications about timing and pricing for the next iPhone release. Here is what Berstein analyst Toni Sacconaghi recently wrote about he upcoming quarterly release.

“FQ3…results are likely to mean little to investors barring a significant surprise to iPhone units, gross margins, or services trajectory. Investor focus has shifted to iPhone demand in FY19 with the next-generation iPhones.

“We note that historically, revenue guidance for FY Q4 has *not* been a helpful predictor of the strength of the forthcoming cycle, and FY Q4 gross margin guidance has only been helpful when Apple has guided meaningfully lower.”

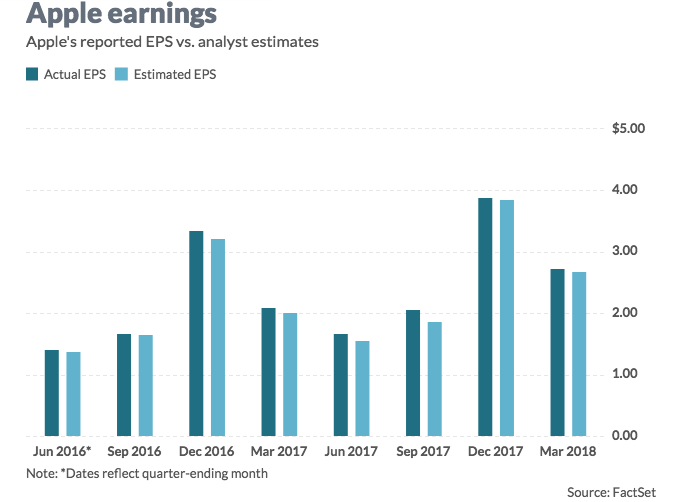

As noted in the chart above, Apple typically outperforms analysts’ earnings expectations. Analysts surveyed by FactSet expect the firm to report earnings per share of $2.16, up from $1.67 a year earlier. Apple’s management has forecast revenue of $51.5 billion to $53.5 billion for the June quarter, compared with $45.4 billion a year earlier. The FactSet consensus calls for $52.3 billion in quarterly revenue. In terms of iPhone sales, analysts surveyed by FactSet expect that Apple sold 42 million iPhones in the quarter and generated $29.2 billion in iPhone revenue. Analysts surveyed by FactSet expect the company’s iPhone ASPs to come in at $693 for the recently ended period. That would mark an increase from $606 a year earlier.

Apple’s services segment has been a star in recent quarters, as iPhone unit-sales numbers have fallen short of expectations. The refresh cycle for smartphone sales has elongated in recent years, making the services business that much more critical to Apple’s sales and earnings performance, not to mention cash generation performance. Morgan Stanley’s Katy Huberty discusses the growth in services in her most recent notes ahead of Apple’s quarterly release.

“Given iPhone results matter less late in a cycle and consensus expects flattish iPhone growth going forward as the market matures, we expect investors to focus increasingly on Services results as a sign of whether Apple’s installed-base monetization efforts can drive overall company growth despite declining services revenue.”

Huberty projects $9.6 billion in services revenue for the spring quarter, above the FactSet consensus estimate of $9.2 billion. She has an overweight rating on Apple’s stock and a $232 price target.

Moreover and with respect to earnings results that are highly anticipated for this coming week, Tesla (TSLA) earnings are slated to be released Aug 1, 2018. It’s no secret that TSLA’s share price performance and valuation are of constant consternation to the bears and naysayers. Finom Group’s chief market strategist Seth Golden suggests that the fundamentals for Tesla make the share price performance a phenomenal and historic break from any kind of fundamental analysis. Needless to say, Golden is a naysayer on TSLA (no positions held in Golden Capital Portfolio presently).

With all that being said, the share price of TSLA has been an outperformer for several years. However, the stock performance in 2018 has left new investors with a bad taste in their mouth, now down nearly 3% YTD. Analysts polled by FactSet expect Tesla to report a second-quarter adjusted loss of $2.78 a share, compared with an adjusted loss of $1.33 in the second quarter of 2017. Crowdsourcing platform Estimize, which gathers estimates from buy-side analysts, hedge-fund managers, company executives, academics and others, has a consensus loss of $2.68 a share.

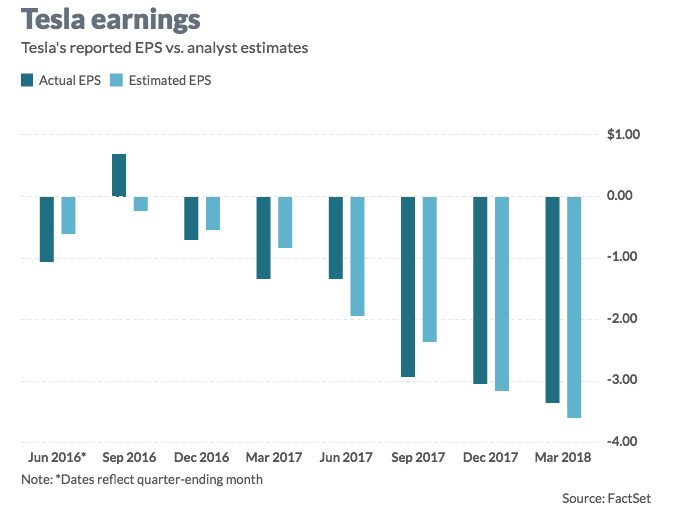

As shown in the bar chart above, TSLA has a rather mixed performance against analysts’ estimates over the years. Analysts surveyed by FactSet expect sales to rise to $3.99 billion in the quarter, from $2.79 billion in the year-ago period. Estimize is calling for sales of $3.91 billion.

Musk has proven to unnerve investors in recent quarterly reports and with his verbiage against analysts and even his own investors. He’s either a willful genius with the visionary endgame known only by his person or an emperor soon to be disrobed, further. Only time and results will tell. What we know to-date is that results are generally found to under deliver and over promise with the share price still rising year-after-year. With respect to the aforementioned, this is why Golden suggested the complete detachment of any fundamental analysis being projected by the share price performance and valuation of the company.

Tesla earlier this month reported it produced 53,339 vehicles in the second quarter. It said it expects to be making 6,000 Model 3s a week by late August.

It delivered 40,740 vehicles, of which 18,440 were Model 3, 10,930 were Model S, and 11,370 were Model X. Those Model 3 deliveries were short of consensus expectations, part of the reason analysts at Goldman Sachs earlier this month kept their sell rating on the stock and their bearish stance overall on Tesla.

In a research note earlier this month, the Goldman analysts noted that at 420,000, the net number of reservation holders has decreased from the roughly 455,000 Tesla disclosed around the July 2017 Model 3 unveiling. Tesla may not have actively sold the Model 3, but “enough media attention and announcements” about the Model have proliferated the customer base,” the Goldman analysts said.

“In that vein, an incremental push to increase demand likely resembles traditional auto OEMs (where incentives are layered on to vehicles to help stimulate purchases), and could be a headwind to margins.”

Steve Eisman, the hedge-fund manager and investor who garnered prominence on Wall Street for his bets against dicey mortgage products engineered by the world’s biggest banks offered the following with respect to Tesla’s CEO:

“Look, Elon Musk is a very, very smart man but there are a lot of smart people in this world, and being smart’s not enough you gotta execute and he’s got execution problems.”

Now Eisman is betting against Elon Musk’s Tesla Inc. because, as he put it during a Friday interview on Bloomberg TV, he doesn’t see value in the company and doesn’t believe they’re doing enough in autonomous driving.

“I don’t see the value in Tesla. “We’re short Tesla.”

While the longstanding short position in TSLA shares remains outsized at over 30% of the float short the stock, the share price has done very little over the last 18 months. The median analyst price target on the stock is $295 per share and with an average analyst rating of Hold according to Capital IQ.