It appears to be another rocky open on Wall Street with all 3 major indices set to open sharply lower. In Wednesday’s trading session, the Dow and S&P 500 both fell with the Nasdaq outperforming, as the tech-heavy index found favor among investors on the heels of Apple’s (AAPL) better than expected quarterly results. That sentiment is seemingly fading quickly as trade war rhetoric runs rampant and the Federal Reserve is set to raise rates once again in September. The Fed maintained rates at current levels in their announcement yesterday.

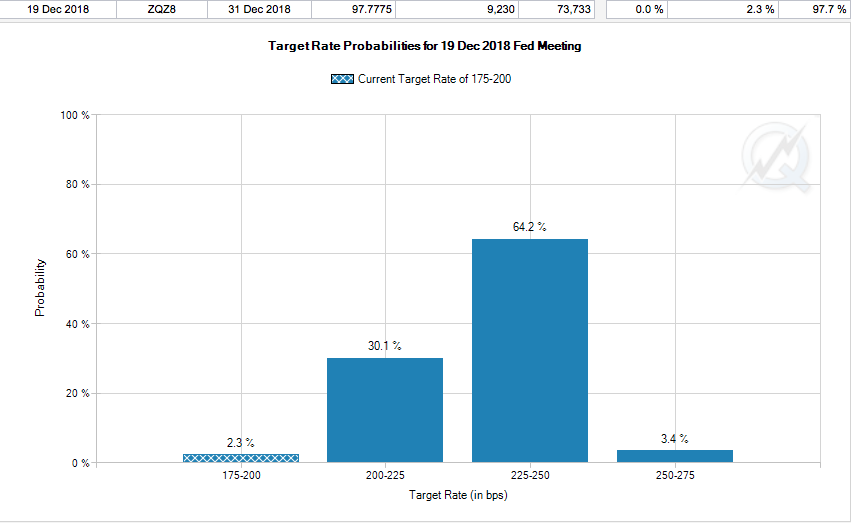

In a widely expected move, the central bank’s policymaking FOMC voted unanimously to keep the target range for its benchmark rate at 1.75% to 2 percent. The committee is widely expected to approve an increase at the September meeting. The statement said the labor market has “continued to strengthen,” language consistent with the June and “economic activity has been rising at a strong rate,” a more bullish view than the June characterization of “solid” growth. The committee also noted that its policy stance remains “accommodative” and said inflation continues to progress near the Fed’s 2% goal. For the balance of the 2018, the Fed is expected to raise rates by a .25 bps in September and December. A December rate hike is highly debated given the geopolitical concerns and what seems to be a decoupling of U.S. economic growth from that of global economic growth due, in part, to increased trade war escalations. At present, the CME’s FedWatch Tool gives a December rate hike a 64% probability as depicted in the graphic below.

Speaking more specifically to the trade war rhetoric being ratcheted higher, Asian markets fell sharply overnight, especially with respect to Chinese equity markets.

“The White House, seeking to ratchet up pressure on Beijing and prod China into further negotiations, said it would consider more than doubling its proposed tariffs on $200 billion of Chinese goods to 25 percent.

The move Wednesday came as talks between Beijing and Washington have stalled, and Washington is looking for additional leverage. In a Monday White House meeting, Trump dismissed a proposed 10% China tariff as weak, said people familiar with the discussions, and had them bump up the levy to 25 percent.

Senior administration officials said they would ask for industry comments on a 10% tariff and a 25% tariff. A final decision on the rate isn’t expected until September at the earliest.”

As an investor, the key consideration continues to be “will they or won’t they”; will the White House take the rhetoric and fully employ the tariff measures should China not come back to the negotiating table? Also, should China come back to the negotiating table, but not offer incremental concessions on trade to the U.S. is the White House prepared to implement tariff measures and accept any potential economic fallout. In the view of Finom Group, we’re forced to accept the viewpoint that there is better than even odds that some level of increased tariffs is to be implemented in September. The measure of U.S. economic impact from such increased tariffs is speculative, at best, given the level of economic growth presently expressed, which also seems to be accelerating.

Given the uncertainty over the aforementioned tariff implementation and adverse affects from such implementation on the economy, earnings continue to guide investors longer-term. Corporate earnings have continued to accelerate from Q1 to Q2 2018.

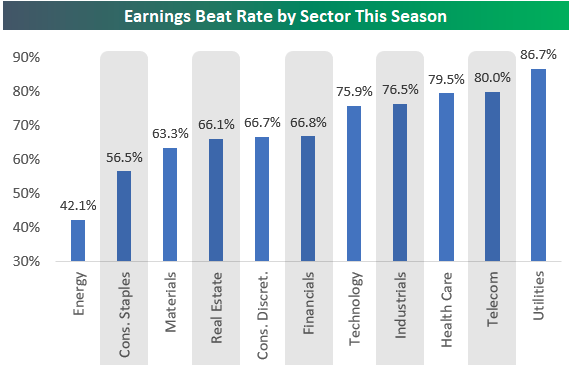

The beat rate for quarterly reports remains strong quarter-over-quarter. Tech stocks are beating at a very high rate of 75.9%, but even with such strength some of these results are finding stocks being sold-off due to perceived stretched valuations. Below is a chart that identifies the beat rate by sector, as developed by Bespoke Investment Group.

Even with elevated expectations, 78.2% of the S&P 500 index reported 18Q1 earnings above estimates and 18Q2 is looking even better, with 81.0% of S&P 500 companies beating. If this holds, it will be the highest percentage of earnings beats on record (going back to 1994 Q1). Higher than expected earnings have facilitated the S&P 500’s 18Q2 YOY earnings growth rate to 23.3%, which is the highest second quarter on record since 10Q2’s 38.8 percent.

Although earnings have been stellar year-to-date, the S&P 500 has remain range bound since the correction period in February. Having said that, the uptrend since that period has found the broad-based index back above 2,800 and within arms reach of its all-time high set in January.

The table above represents what happens to the S&P 500 when it comes within 1% of its all-time highs for the first time in 120 days. When the S&P 500 is near all-time highs, it is pretty much GUARANTEED to go up in the next 3+ months (see study). While the table appears promising longer-term, former market cycles may not be fairly compared to the current market cycle that has a plethora of different variables to consider.

While the S&P 500 has recently recaptured the 2,800 level and maintained the level for 2 weeks now, Thursday’s trading session may find the index giving up that level for the moment. Market pundits continue to castigate the strength in the market amidst its rise since the February bottom. Morgan Stanley is one such institution that believes the market will tumble in a worse fashion than during the February correction.

“With Amazon’s strong quarter out of the way, and a very strong 2Q GDP number on the tape, investors were finally faced with the proverbial question of ’what do I have to look forward to now?’ The selling started slowly, built steadily, and left the biggest winners of the year down the most. The bottom line for us is that we think the selling has just begun and this correction will be biggest since the one we experienced in February.

We must admit, the market sent some misleading signals over the last few weeks by limiting the damage to the broad indices when Netflix and Facebook missed. We believe this simply led to an even greater false sense of security in the market,” wrote the team of Morgan Stanley analysts, led by Michael Wilson, the firm’s chief U.S. equity strategist.

While it is possible tech and consumer discretionary stocks won’t experience the derating witnessed in other cyclical sectors, we think it is unlikely and are only emboldened by the misses from Facebook and Netflix and the price action last week.

We recognize that money can also move from these sectors to others thereby leaving the S&P 500 around current levels rather than falling 10% as we expect.”

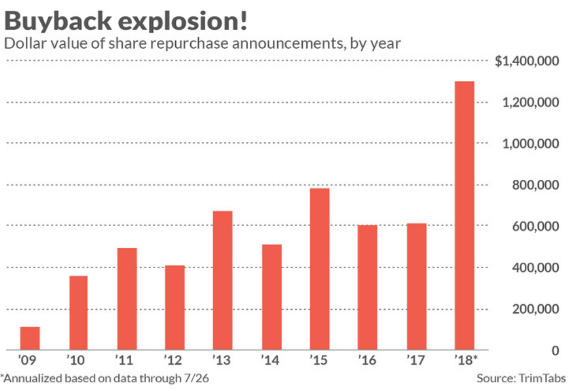

It’s a pretty nice “OUT” they are giving themselves with the last statement, the notion of sector rotation possibly not bringing their forecast to fruition. Another factor that could prove problematic for the Morgan Stanley proposed 10% correction in equities is that of corporate buybacks. Moreover, those corporate buybacks appear to be supporting the broader market and accelerating quarter-over-quarter.

As shown in the chart above, corporate buybacks totaled $240 billion in Q1 and $430 billion in Q2. It’s every clear that quarterly buybacks nearly doubled from Q1 to Q2 2018, likely boosting the major index averages and placing a floor beneath the major averages. Again, the level of buybacks would be a headwind for not only Morgan Stanley’s forecast, but for any general bear market thesis.

While corporate earnings and corporate buybacks are seemingly keeping a floor underneath the stock market, it has proven a difficult task for the S&P 500 to make a new all-time high in 2018. The choppy market environment has ben perpetuated by geopolitical tensions on trade that has pervaded itself in investor sentiment. Many investors have been unwilling to chase the market higher, but unwilling to pass-up market dips. The level of uncertainty has risen year-over-year and resulted in an elevation in volatility residing in the marketplace and as expressed in the VIX.

As the market seems keenly focused on trade today and ahead of the Nonfarm Payroll report due out Friday, trade negotiations are still ongoing with NAFTA partners. U.S. trade czar Robert Lighthizer and Mexican Economy Secretary Ildefonso Guajardo will meet again on Thursday, in Washington, to discuss NAFTA, according to media reports.

On Monday, U.S. Commerce Secretary Wilbur Ross said he thought there was a good chance American negotiators were on a “pretty rapid track” when it comes to NAFTA talks with Mexico, noting that Washington has fewer issues with Canada in the talks.

“Mexico is, intellectually, the more complicated of the two; so if we can solve that, we should be able to fill in with Canada,” Ross said during an appearance at the U.S. Chamber of Commerce’s Indo-Pacific Business Forum.”

Given the heightened level of attention on global trade at the moment, any good news from today’s bilateral meetings may find buyers coming into the market later in the trading session. This, of course remains to be seen. Additionally, we urge investors and traders to consider that while trade rhetoric is the them for which the market is retrenching today, other issues remain elevated with regards to investor consideration and sentiment. We denote some of these considerations or headwinds for the market as follows:

- Rising rates

- Flattening yield curve

- Peak earnings cycle

- Rising levels of corporate and household debt

- Longevity of market correction before achieving new all-time high

- Strengthening USD

- General reflation/inflation

While all the aforementioned headwinds are to be considered and as we’ve mentioned on many occasions, none have ever proven to overpower market direction, which is more firmly correlated to corporate earnings trajectory. With or without good news in the market today, Finom Group continues to deliver actionable trades daily and weekly to subscribers.

The screen shot above depicts just a couple of our latest, completed and profitable trade alerts on the week. To date, Finom Group has a greater than 90% hit rate on its actionable trade alerts. Subscribe today and access all of our weekly research reports and trade alerts!