The markets were a rather tranquil place yesterday, which hasn’t likely been stated for much of 2018 and in more than 2 months. But indeed it was with all 3 major averages finishing with less than a .5% move on the day and the VIX below 16. The S&P 500 index advanced about 2.25 points, or about 0.1%, at 2,708.6. Energy shares led the gains, up 1.6%. Meanwhile, the Nasdaq Composite Index closed up 14.14 points, or 0.2%, at 7,295.24. The Dow was the laggard on the trading day, falling almost 40 points and weighed down by shares of IBM. The Dow ended the day off 0.2%, at 24,748.07.

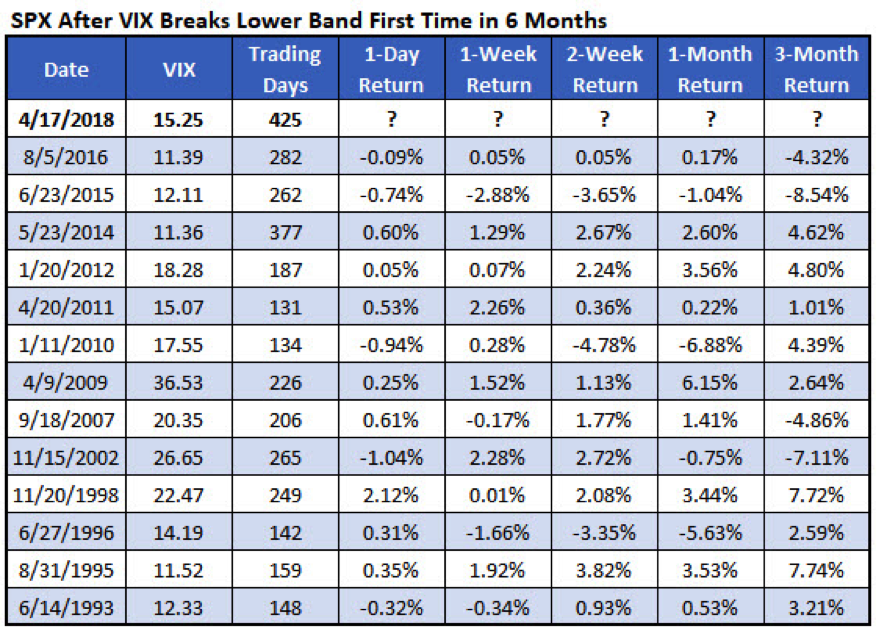

As bank earnings begin to wind down this week, another catalyst will be needed to maintain the recent rally in the major averages. Having said that investors welcome the recent stability in the market with a VIX currently below 16. A reading above 16 typical exacts daily 1% moves in the S&P 500, which has found itself commonplace in 2018 and has also exacted increasingly low market volumes/participation. Furthermore and according to Schaeffer’s Senior Quantitative Analyst Rocky White, the VIX also closed beneath its lower Bollinger Band (BB) for the first time since August 2016, or 425 trading days ago.

As shown in the chart above, the breaking below the lower BB recently, marks the longest streak above its lower BB ever, going back to 1990. What it may be foreshadowing remains to be seen, but greater perspective is definitively needed when drawing correlations to historic BB indications. Not all records are created equally, as they say. Just ask Barry Bonds, Mark McGwire and Sammy Sosa! Now let’s see what’s on tap for economic data today.

A reading on weekly jobless claims and an April, Philadelphia Federal Reserve’s business-conditions index are slated to hit at 8:30 a.m. Eastern Time. At 10 a.m. Eastern, a March report on leading indicators is scheduled for release. The labor market has been tightening over the last couple of years and that tightening has heightened in 2018, with raises rising at a faster rate than in previous years. Having said that, one aspect of the labor market that remains with job losses continues to be the retail sector. Such job losses for the sector are expected to continue in 2018 as the rate of retail store closures is also forecasted to grow when compared to 2017.

One such retail operator announcing store closures and bankruptcy, on the heels of Toys R Us bankruptcy is Bon-Ton Stores. The retailer will begin closing down its remaining stores and go out of business after a bankruptcy judge said she would approve the sale of the retailer’s assets. Judge Mary Walrath of the U.S. Bankruptcy Court in Wilmington, Del., Wednesday cleared the way for a sale to a group of bondholders and a pair of liquidators, which will begin closing more than 250 stores across 23 states. The store closures and bankruptcy are expected to result in a loss of about 24,000 jobs.

When it’s all said and done, there could be roughly 12,000 store closures in the U.S. in 2018, up from about 9,000 store closures in 2017, according to data from real-estate firm Cushman & Wakefield, cited by consulting firm BDO USA LLP in a recent report.

While Amazon takes much of the blame for the destruction in the physical retail operations of U.S. storefronts, the truth is that the evolving nature of technology spirited by the age of the Internet and shifting consumer demographics was inevitable. Some retail operators will evolve and some will be found too slow to adapt and fail to compete. Speaking of Amazon, Jeff Bezos letter to shareholders heralded much of Amazon’s success over the years. In the letter, Bezos stressed the importance of having high standards in running a business. By setting high standards, companies are able to live up to “ever-rising customer expectations,” he said. I’m going to guess that high standard didn’t extend to the company’s former attempt at a smart phone, which failed quickly and hasn’t been revisited since. The full letter here:

“How do you stay ahead of ever-rising customer expectations? There’s no single way to do it – it’s a combination of many things. But high standards (widely deployed and at all levels of detail) are certainly a big part of it.”

Bezos also disclosed that Prime now exceeds 100 million members worldwide.

“Amazon continues to have an ‘iron grip’ on the e-commerce market heading into the rest of 2018,” said Daniel Ives, GBH’s head of technology research, in a note late Wednesday.

The figure came in above Wall Street’s estimate of 80 million Prime members and GBH’s projection of 92 million.”

RBC analyst mark Mahaney also weighed in on the figures announced by Amazon. “By our estimate, Amazon already accounts for roughly 20% of U.S. online retail sales, but the company’s strong mobile positioning and infrastructure advantages facilitating next-day and Same-Day Delivery should allow Amazon to continue to take share,” said the RBC team.

In less flattering headlines concerning global government and debt, The International Monetary Fund issued a new warning. The IMF offered that governments worldwide should take action to try to reduce their indebtedness while the going is relatively good. The Washington D.C.-based institute said lawmakers should seek to build buffers and cut public debt levels in order to tackle “challenges that will unavoidably come in the future.” It may be that the IMF is simply “going on the record” for the sake of an unavoidable “I told ya so” moment in the future. Global debt has reached levels never seen in history and without the necessary levers to pay down debts in a manner that won’t adversely affect future generations right to social programs, social norms and financial structures around the globe.

While the warning seems innocuous enough the political will to fight indebtedness is lacking for most advanced economies of scale. Most advanced economies are willing to fuel economic growth in the near-term and with increasing debt as a measure of GDP. The hope is that stimulative measures will serve to boost economic growth, buy more time and eventually find a balance that would allow governments to pay down the debt burden without causing financial calamity.

Moreover and speaking with regard to the geopolitical climate, a calm has recently been found post the Syrian missile strikes over the weekend. Such calm may not last for very long warns Kristina Hooper, chief global markets strategist at Invesco during a CNBC’s “Futures Now” interview.

“What we know from experience is that most geopolitical risks don’t impact markets materially over the longer term, but there’s one exception to that rule, and it’s protectionism,”

While markets seem not to be concerned right now about any impending trade war, we have a lot to be worried about when it comes to that potential,” she said.

The level of alarm over a potential trade war has been dialed back since Chinese President Xi Jinping’s speech last week. Xi pledged to free up the Chinese economy to trade and foreign investment, both seen by some as a move to placate the U.S.

However, Hooper warns markets not to underestimate Xi’s “strategic prowess.”

There’s no compelling reason why China would grant material concessions and there could be another flare-up, she said.

U.S. equity futures are slightly lower ahead of the market open. The S&P 500 has recently proven to hold off setting a new low for the year and is now resting above the 50-DMA.

As of yesterday, The S&P 500 is down 0.5% YTD and is 5.7% below its record close set in January 2018.