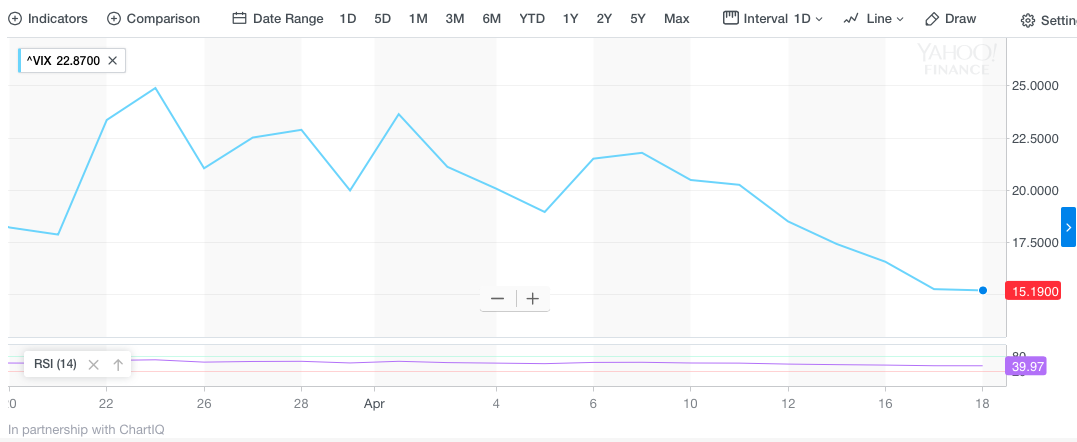

U.S. equities have been in rally mode and the VIX is providing confirmation. That doesn’t make any sense now does it? Seeing how the VIX is completely reactionary it should be an example of equities/major averages/dog wagging the VIX/tail. Nonetheless as the major averages have been responding favorably to the early innings of earnings season, unless you’re a reporting bank stock, the VIX has been expressing decay and or calm in the S&P 500. Stocks continued to rally yesterday, leaving the S&P around 5.8% off its all-time high.

Since recently touching above 25 in late March, the VIX had slowly been decaying. As reporting season got underway, however, the VIX went into full-scale retreat even as tensions escalated last week regarding Syria and a probable missile strike that did come to pass from the United States. Yesterday found the VIX falling that much further and ahead of this morning’s VIX Futures expiration whereby VIX-ETF/ETNs will find M1 contracts expiring and back month Futures rolling forward. In light of VIX Futures expiring and an S&P 500 climbing by more than 1% yesterday, the VIX fell below 15 at one point intraday and before closing at 15.17, a low reading not seen in over a month.

With all that being said, the question investors may be asking themselves, as markets seem to be stabilizing after great turbulence over the course of the previous two months, “Is the worst behind us”?

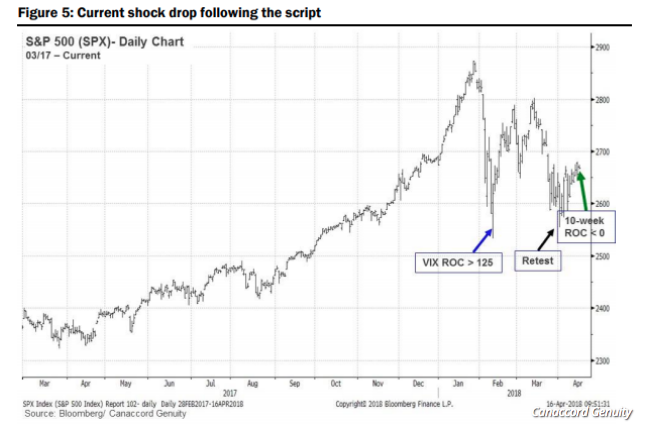

In order to answer that question, which is admittedly speculation or predictor in nature, we’ll take a look at two opposing viewpoints from well-respected analysts and financial institutions. First up is Canaccord Genuity analyst Tony Dwyer. The analyst has been one of the biggest bulls on the street with a year-end S&P 500 target above 3,000. Dwyer has characterized the stock market’s early February plunge as a phenomenon known as a “shock drop,” in which a correction is sharp enough to cause the 10-week rate of change in the Cboe Volatility Index or VIX, to spike to 125. The rate of change, or ROC, measures the percent change in price from one period to the next.

In a Monday note, Dwyer said he saw no reason to change “what worked so well in analyzing a human-nature-driven ‘shock drop.” He elaborates:

“We found that when the 10-week VIX ROC spiked to 125 or above, and then dropped below zero, (1) the VIX dropped even further, (2) the SPX low was in, and (3) the SPX made a new high a median 78 trading days later. (See chart below)”

Dwyer goes on to say that in the past shock drops of 1998, 2010 and 2011 stocks moved to a new high following a retest of the low. In all three cases, when the VIX rate-of-change dropped below zero, the low was in and new highs were less than four months later, he found. Dwyer was quick to acquiesce to the fact that this exercise or theory did not pan out in 2008, but offers a rationale as to why it didn’t work then.

“2008 was not applicable, as it came in the midst of the global financial crisis. And while the sample size is small, such extreme human nature reactions should be expected to be infrequent.”

Seth Golden of Finom Group has put forth factors surrounding human nature in VIX terms since 2015. In discussing human nature and the VIX, Golden often refers to the human condition of desensitization. In his theory, humans become desensitized to the exposure, in repetition, of like stimuli. In other words, the more that investors are presented with the same stimuli, the less reactionary or fearful of the stimuli they become. Desensitization serves to produce less fear over time, which shows up in the broader market and VIX.

Golden and Dwyer both fancy the probability of the S&P 500 achieving new highs in 2018. Dwyer offers that the fundamental backdrop of the economy remains strong.

“He said those core fundamental factors this time around include solid global growth, positive domestic activity driving earnings per share, a pickup in capital spending, real household median income “jumping” with strong employment, and a demographic-driven push to higher homeownership.”

As Dwyer and Canaccord Genuity have laid the more bullish case for equities before us, now we’ll explore a more bearish case from Morgan Stanley. If investors are expecting big returns going forward, Morgan Stanley’s most recent analysis proves contrarian.

“The feel good aspects of said policy appear at or nearly in the price of US markets, whereas the downsides are less accounted for,” the 31-page research paper said. “While there’s a fair amount of debate about how much this fiscal expansion extended the economic cycle, for markets our analysis suggests we’re closer to the end of the day than the beginning.”

“Our historical analysis suggests that there may be a benefit for markets from deficit-funded tax stimulus, but the boost in returns appears temporary and is not statistically significantly higher than periods without stimulus,” Morgan Stanley said. “Moreover, markets tend to underperform with policies similar in size to the Trump tax cuts.”

Morgan Stanley seems to be taking a longer-term view and one that finds deficit-funded policies out of favor in the not too distant future. Many economists actually support this notion, especially when it comes to the deficit-funded tax reform policy that still yet needs to prove simulative to overall growth. Economists are largely speculative surrounding growth prospects given the level of consumer and/or household debt that would likely find the benefits of lower taxes funding debt repayment. Such repayments would not prove stimulative to GDP, otherwise deflating the affects of lower taxes. But again, this is a principle argument put forth by economists that bears time to play out.

Taking Morgan Stanley’s research and analysis a step further, the firm discusses the possibility of a recession taking shape beyond 2018.

“The firm also is warning that the next recession could be deeper than many economists are now forecasting. Conditions could be further constrained should a push for austerity occur as the budget deficit begins to swell.”

There are a great many reasons this warning could turn out to be prudent planning as the U.S. national deficit reaches beyond 100%:GDP. Such deficit levels coming at times whereby the Federal Reserve has yet to clean its balance sheet and upon rising rates would likely find a cross current of problematic economic scenarios that prove difficult to manage through government policy.

After reviewing the differing sentiment from the two parties within this context, investors/readers are asked to recognize that the differing takes are more about sentiment as both Canaccord Genuity and Morgan Stanley predict further market gains in 2018. It’s the 2019-2020 forecast that remains blurred or marred by the policy impacts of the day. One variable that remains unclear for equities in 2018 and until further notice is the affect of the 10-year breaching a 3% yield. With reflationary/inflationary fears abound and a correction in equity prices taking place already in 2018, prior to such an occurrence in the 10-year treasury yield, what occurs if in fact 3% is breached has the ability to suppress equity prices going forward. It’s not to say upside potential for equities isn’t in tact, but how much upside may be impacted by rising rate concerns.

In a more neutral market stance, Wharton professor and market bull Jeremy Siegel finds stocks and bonds on a collision course in 2018 as rising rates stoke fear in equity investors.

“This market is going to struggle this year… as good earnings collide with what I think will be higher interest rates both by the Fed and in the Treasury market.

Siegel said “3.25% on the 10-year will give stocks a pause in 2018” and that the most investors could realistically hope for is a 10% rally in the market, compared with a 25% surge on the Dow last year.”

A feather in the cap for equity investors at present is the technical outlook for stocks. As of yesterday, the S&P 500 broke above and closed above the 2,695 resistance level as indicated in the chart below.

Admittedly, the recent rally above resistance levels comes on the heels of relatively low volume and narrowing leadership from tech stocks. Moreover, the financials haven’t shown themselves to participate in the rally just yet and after many bank stocks have recently reported strong quarterly results. This remains a concern and something to keep a watchful eye on as a sector (XLF).