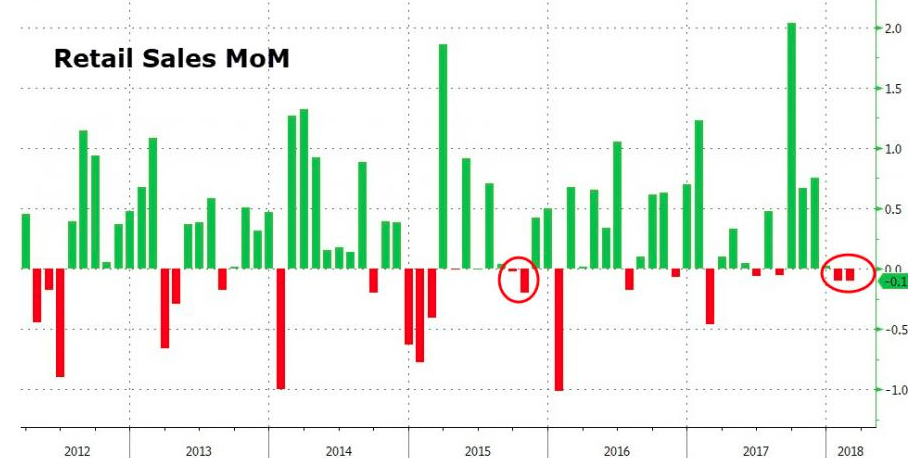

As reported yesterday by the Commerce Department, February retail sales fell month-over-month and for a 3rd consecutive month. It’s important to discern the decline was MoM and not year-over-year as total retail sales continue to grow in the United States.

The Commerce Department reported that retail sales slipped 0.1% last month with economists forecasting growth of .4% for the month. January data was revised to show retail sales declining 0.1% instead of falling 0.3%, as previously reported. It was the first time since April 2012 that retail sales have declined for three straight months, signaling a potential slowdown from the U.S. consumer. On the bright side, however, total retail sales grew by 4% in the month of February on a YOY basis. Below is a breakdown of February retail sales by category on a MoM and YOY basis:

With tax reform in full swing and a strong labor force in place, consumer spending could pick back up in the coming months. Consumer spending makes up the greatest portion of U.S. economic growth, which is expected to grow some 2% in 2018. The last look at Q4 2017 GDP is due out later this month. Revisions to December data on construction spending, factory orders and wholesale inventories have suggested the fourth-quarter growth estimate could be raised from 2.5% to a 3.0% rate of growth.

In other economic data released yesterday, U.S. producer prices increased slightly more than expected in February. The Department of Labor said on that PPI rose 0.2% last month; economists polled by Reuters had expected PPI gaining 0.1 percent. Core PPI, which excludes food, energy and trade service prices, rose 0.4% in the month of February.

Outside reversals have been par for the course and in both directions for the major indices this year. Combined with the prior day’s losses, the Dow’s decline yesterday’s of 1% on the found the major index giving up most all of its gains from last Friday. The S&P 500 and Nasdaq were down to a lesser degree, but find investors selling rallies more frequently than in previous months. But the market fundamentals do remain solid given the backdrop of strong corporate earnings growth and an economy that doesn’t seem to be overheating based on the flow of economic data reported. Over 70% of companies that reported Q4 2017 earnings beat analysts’ estimates and with 77% beating sales estimates, the most since 2008. Sales growth is organic, real economic growth that corporations can’t manage to manipulate to the degree they can do so with earnings and through various measured activity such as share repurchases and cost cutting.

“According to FactSet, the S&P 500 is changing hands at 17 times projected earnings for the next 12 months. That’s above the five-year average of 16x and the 10-year average of 14.3x, but it’s far from exorbitant considering earnings growth and still-low interest rates.”

Even with strong earnings and relatively tame inflation in view, as the 10-year Treasury yield is hovering just above 2.8% presently, there will always be market pundits calling for a market top. Dennis Gartman of the Gartman letter has warned that a market top is here, a multi-year market top at that. Gartman offered the following to his clients recently:

“Long-time clients know that we do not write WATERSHED reports often and indeed we’ve not written one in many years… in fact we cannot remember when we put forth the last one but it was several years ago certainly” but today is one of those days when “we put our reputation hard upon the line… and we are doing so today, calling for a major, multi-year top on the equity markets following the recent volatility and following the reversals to the downside that took place yesterday in the Dow Industrials; the NASDAQ; the S&P and the Russell 2000.”

The issue with Gartman’s call on the equity market is that this is not the first market top call he’s made over the last couple of years and he admits as such in the following that was also disseminated to clients:

“We know that we have vacillated in our regard for equities of late, moving from bullish to bearish to bullish to bearish with too great regularity, but such is the demeanor of markets as they make important peaks: they make us appear foolish and ill advised, wearing out our margins and more importantly wearing out our psyches. But with the multiple “reversals” to the downside note above and with the volumes swelling each time as the markets fell and with the failures in so many instances well below the previous peaks, the stage finally is set for continued, manifest and perhaps material weakness going forward. Eventually, even “Old Turkey” is proven wrong.

It would appear as though the market exuberance expressed just last Friday has run into another brick wall surrounding increased rhetoric on trade tariffs and the firing of Secretary of State Rex Tillerson this week. With Larry Kudlow taking the place of outgoing top economic advisor to the President, Gary Cohn, investors may be awaiting to see if the President’s tough talk on trade can be aligned by Kudlow. Until such a time, markets remain on edge and with great intraday swings expressing greater market volatility.

Today’s economic data includes weekly jobless claims, Philly Fed, Empire State and Home Builders index. Next week is a much busier economic data week that is headlined on Wednesday by the Fed’s rate hike decision and the supporting press conference by Fed Chair Jerome Powell. Thursday’s broader market direction and end of day result will likely carry through the Friday trading session. At present, equity markets have yet to find the stability they desire and force upon traders the need to act quickly and look for opportunities in this market environment.