Equity markets were sent reeling, once again, Monday as trade war concerns and their impact on global growth moved to the forefront once again. What spurred the latest fears was the following headline:

Google’s (GOOGL) move to stop licensing its Android mobile operating system to Huawei could deal a huge blow to the Chinese tech giant’s ambitions to become the top player in smartphones globally. The U.S. tech conglomerate has suspended business activity with Huawei that involves the transfer of hardware, software and key technical services. Google made the move in order to comply with Washington’s decision to put Huawei on the so-called Entity List, meaning American firms need to get a license to sell products to the Chinese firm.

Late Friday of last week, however, the U.S. Commerce Dept. was taking steps to ease the restrictions placed on Huawei. A little too late as global equities fell sharply on Monday, but U.S. equities finished off of their lows. The tech-heavy Nasdaq (NDX) was hit the hardest on Monday, falling nearly 1.5% while the Dow Jones Industrial Average (DJIA) and S&P 500 (SPX) finished down .3% and .67% respectively. With companies that supply Huawei with infrastructure, internal components and switches proving to reside within the Nasdaq, the index has been under pressure, as the Vaneck Vectors Semiconductor ETF (SMH) fell some 4% Monday alone.

But if you’re just waking up Tuesday morning to the markets, the fears surrounding the Huawei ban seem to have subsided, if not only for the moment.

“The U.S. government on Monday temporarily eased some trade restrictions imposed last week on China’s Huawei, a move that sought to minimize disruption for the telecom company’s customers around the world. The U.S. Commerce Department will allow Huawei Technologies to purchase American-made goods in order to maintain existing networks and provide software updates to existing Huawei handsets. The company is still prohibited from buying American parts and components to manufacture new products without license approvals that likely will be denied.

The escalating of trade tensions between China and the U.S. has certainly spilled over and into the corporate sector, damaging sentiment for the tech sector and individual companies. But who stands to gain from the apparent blow to Huawei may be the optimal question to be asking in light of the recent developments.

”The biggest winner in the long run will be US IT companies, but in the short term, tension between two countries raises opportunity for Korea,” Daniel Yoo, head of global strategy and research at Kiwoom Securities.

In the smartphone segment, where Huawei was among the few companies seeing annual growth in shipments at a time of slowing sales, South Korea’s Samsung Electronics would be a beneficiary, Yoo said. Data from Canalys showed Samsung’s annual growth in worldwide smartphone shipments declining 10% in the first quarter of 2019, while Huawei surged 50.2%. In the same period, American technology giant Apple’s smartphone growth slid 23.2%.”

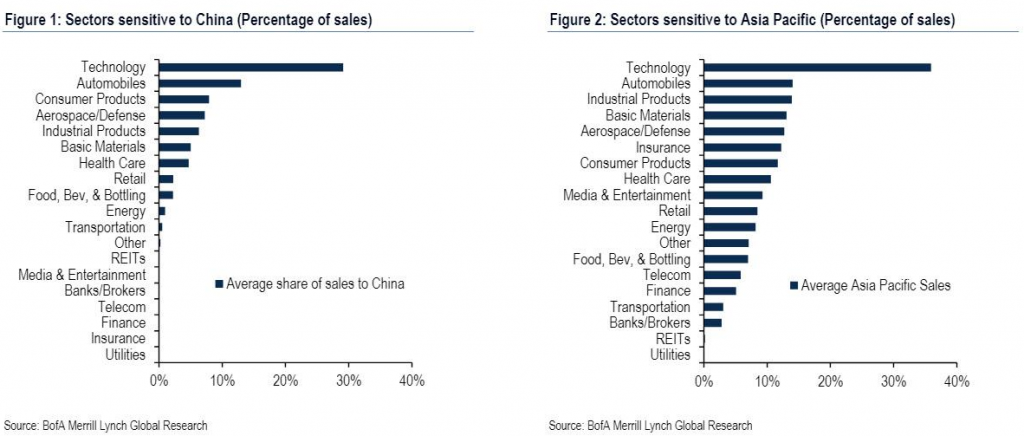

Naturally, if we choose to look at who stands to benefit the most from any fallout from Huawei’s restrictions, we aim to look into what companies could be adversely affected. What BofAML found is that based on the latest full year 2017 earnings results available, U.S. sectors most sensitive to China as judged by share of sales include Technology, naturally, as well as Autos and Consumer Products.

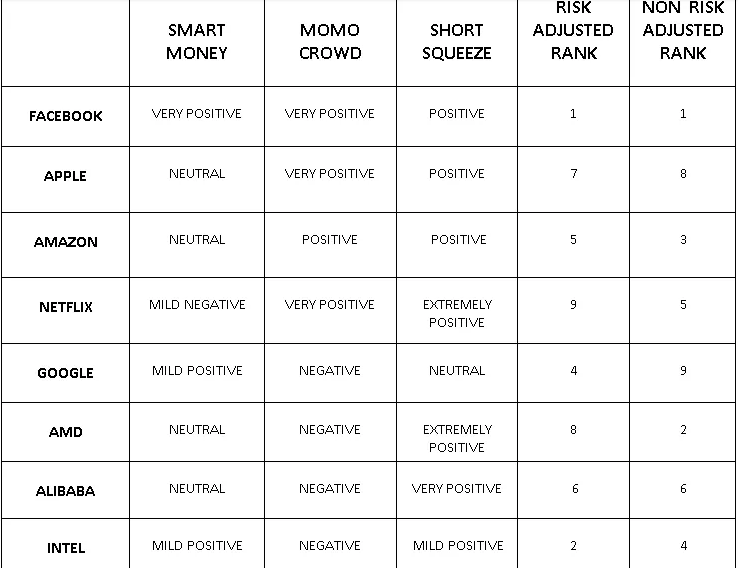

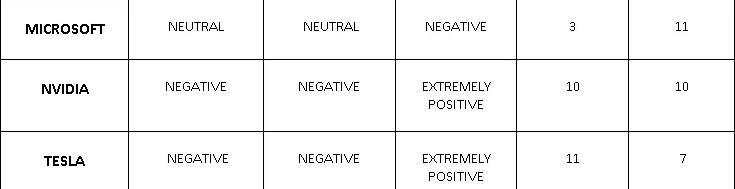

In addition to the BofAML offering we would want to take a look at fund flows. Naturally, with the tech sector coming under pressure we would expect to see flows out of the sector. The mega-cap tech stocks are seeing the worst of the fund flows as shown in the table below from the Aurora Report.

- Intel will lose some business from Huawei but the loss is not significant. Perhaps this is the reason that smart money flows in Intel stock are mildly positive. Furthermore, Intel stock is very oversold, provides a good dividend and the valuation is cheap. Of course, the momo crowd does not care about these things; momo crowd money flows are negative in Intel stock.

- In a surprise, the momo crowd money flows have just switched from positive to negative in AMD stock.

- China poses significant risk for Apple stock, though momo crowd money flows are very positive.

- Amazon does not drive material revenue from China. Momo crowd money flows are positive in Amazon stock. Smart money flows are neutral. Perhaps because of concern that if the market falls, Amazon stock may be hit hard.

- Momo crowd money flows are very positive in Netflix stock but smart money flows are mildly negative.

- Smart money flows in Alibaba stock are neutral. The reason may be that Alibaba is likely to continue growing irrespective of the trade war.

- Smart money and momo crowd money flows are negative in Nvidia stock and Tesla stock.

- Smart money and momo crowd money flows are neutral in Microsoft

Possibly the greatest threat to the global economy would come from the White House Administration, should it choose to apply the last traunch of tariffs on China imports at the 25% rate. This traunch would directly impact consumer goods such as clothing and accessories for which has caught the attention of retailers and athletic apparel vendors. More recently, footwear retailers sent a letter to President Donald Trump, asking him to remove shoes from a proposed list of tariffs on China imports.

The letter, dated May 20, was posted on the website of the Footwear Distributors and Retailers of America (FDRA), and signed by nearly 200 companies, including Nike Inc. (NKE) Under Armour Inc. (UA) Foot Locker Inc. (FL) and Reebok.

The footwear makers said that as an industry that “faces a $3 billion duty bill every year, we can assure you that any increase in the cost of importing shoes has a direct impact on the American footwear consumer.” If prices rise at the border due to transportation costs, labor rate increases, or additional duties, the consumer will end up paying more for the product, the companies said.

The FDRA estimates Trump’s proposed tariffs on China will add $7 billion in extra costs for consumers, on top of the billions Americans pay due to the tariff on footwear imports that was enacted in 1930. Those extra duties fall hard on working class Americans and families, it said.

“Adding a 25% tax increase on top of these tariffs would mean some working American families could pay a nearly 100% duty on their shoes. This is unfathomable. It is time to bring this trade war to an end.”

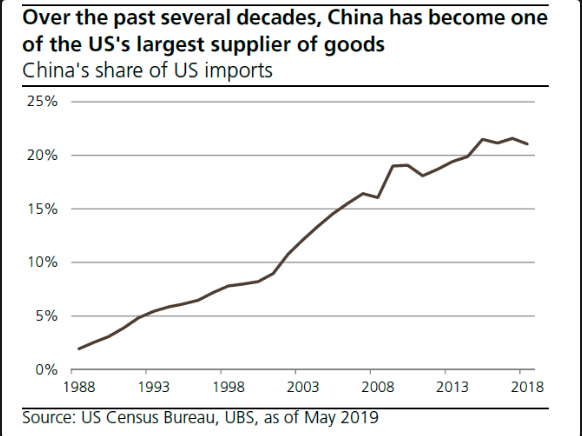

Regardless of what you might think or hear about the U.S. economy becoming less reliant on goods produced and exported from China, the reality is that the U.S. remains heavily reliant on such production and trade partnerships with the nation state.

The ongoing trade feud that has recently escalated between the U.S. and China has rang several alarms amongst the analyst community, possibly none as loudly as that from Morgan Stanley’s chief economist and global head of economics Chetan Ahya.

“If talks stall, no deal is agreed upon and the U.S. imposes 25% tariffs on the remaining $300 billion of imports from China, we see the global economy heading towards recession.”

If no trade resolution is reached between the world’s two largest countries, the central bankers would adjust their monetary policy to provide support for the deteriorating economy, said Morgan Stanley.

The economist predicted the Federal Reserve would cut rates back to zero by spring 2020. China would again upsize its fiscal stimulus to 3.5% of GDP.

“But, a reactive policy response and the usual lags of policy transmission would mean that we might not be able to avert the tightening of financial conditions and a full-blown global recession.

The impact on global growth is non-linear – the risks are firmly skewed to the downside and the window for resolution is narrowing.”

While the outcome from a an all out trade war seems dire and we would think most would draw the same conclusions, Morgan Stanley’s team also contemplates the potential offsets to the trade war with respect to fiscal stimulus plans that could be put forth.

“After months of market jitters, rallies and global growth concerns, fiscal stimulus could provide a boost that puts the economy on the road again. Weakness in financial markets has generally led central banks to adopt a more dovish attitude, most notably reflected in the recent US rate hike pause. However, we believe that fiscal stimulus programmes, many of which include large infrastructure spending initiatives, could be key to reducing the risk of recession in the near term. We expect further fiscal stimulus announcements from China, the US and the Eurozone, meaning that by the second half of 2019, we could see a cyclical upswing in infrastructure investment, which would go into 2020.”

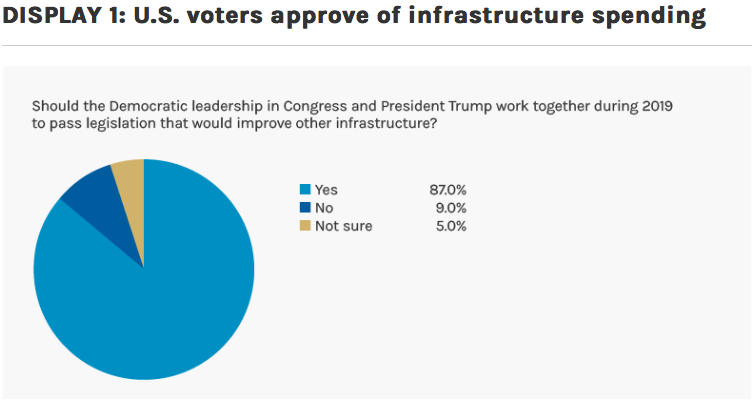

With a divided Congress, the U.S. is in a political stalemate. But one of the areas where a bipartisan agreement seems possible is infrastructure spending. Due to decades of neglect, U.S. infrastructure is in desperate need of an upgrade, garnering a D+ rating from the American Society of Civil Engineers in 2017.3 Infrastructure spending would likely create jobs and improve the economy. It could also reduce transportation costs and increase safety, leading to higher profitability for businesses, which would then have the wherewithal to boost investment.

The most promising means of paying for an infrastructure package would be raising the gasoline tax—which has not been raised since the Clinton administration—by 25 cents per gallon over five years.

In the Eurozone as a whole, fiscal stimulus for 2019 is nowhere near that of China or the U.S., but it is nevertheless expansionary. With ageing infrastructure across the Continent, European governments look like they will adopt stimulus programmes of approximately $47 billion cumulatively.

Oddly enough, with all the noise surrounding global trade investors are actually adding risk by removing hedges. Yes, despite all the aforementioned and the possible binary outcome from the ongoing trade feud, investors have been removing their hedges as gauged through the activity in and around the Volatility complex. At least this is the analysis from Nomura’s strategist Masanari Takada. Keep in mind that the VIX itself derives its value through S&P 500 OTM options activity that largely reflects hedging activity or the lack thereof.

“Investors look to have locked in profits on their long VIX calls (premised on a rise in the VIX). This rollback of downside hedges may have indirectly supported the US equity rebound,” wrote the Nomura quantitative strategist. “As a result, US equity exposure at hedge funds overall has turned upward again.”

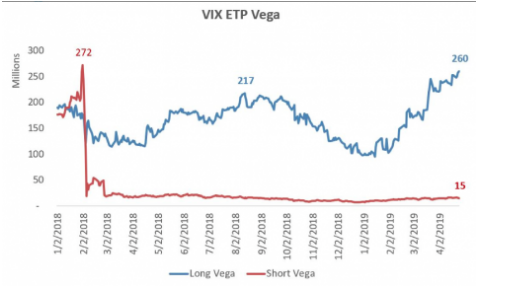

While we definitely agree that monies have been withdrawn from the VIX complex of derivatives, we are highly doubtful that any significant portion of that withdraw was a profit extrapolation given the intense long-VOL positioning in VIX-ETPs that commenced in late January 2019. Here is a look at the Long Vega VIX-ETP positioning as of just 2 weeks ago, as outlined in Finom Group’s Research Report.

“In rationalizing the Volatility market positioning, we are forced to conclude that there is a sizable headwind for long-VOL positions juxtaposed with a sizable tailwind for short-VOL positions. Additionally, we can also assume that some of the record level noncommercial short VIX Futures positioning has come, of late, from long-VOL trades being hedged with short-VOL positions.”

With respect to Takada’s rationalizing of the withdraw of hedging activity, we can also confirm this via the latest fund flows update from J.P. Morgan Chase’s quant team as follows:

“Since May 5, when President Donald Trump issued a tweet signaling a reignition of Sino-American trade tensions, investors pulled over $300 million from unlevered long VIX products, and over $450 million from levered products, including the ProShares Ultra VIX Short-Term Futures ETF (UVXY). Unwinding of this exposure has kept in check the increase in the VIX and prevented the type of VIX increase we saw in February and October last year.”

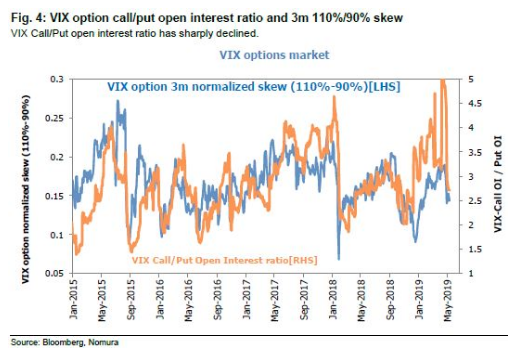

In addition to the latest withdraw of funds from VIX-ETPs, Takada also discussed the call-to-put ratio for VIX options, that is, the percentage of people betting on a rise versus a fall in volatility. He suggested that this has since returned to lows not seen for months. That could mean that indexes may have seen the worst of their springtime woes as hedge funds take on more stock exposure.

“The majority of hedge funds, cautious of the risk of a correction in the US market, seem to have intentionally held down their exposure to US stocks in April. But they also seem to have cleared away their downside hedge positions. Of course, this also means hedge funds have left themselves defenseless in the event of another sharp drop in US stocks.

Still, “it would appear that the majority of hedge funds do not expect another sharp rise in volatility, and that they have concluded that the correction has run its course.”

Ahead of the opening bell on Wall Street, investors are witnessing some relief from the selling pressure that produced a 3-straight weekly loss in the Dow and a .5% decline in the S&P 500 last week. Equity futures are on the rise as Home Depot (HD) reports a better than expected bottom line result for the Q1 2019 period. Here’s how the company did, compared to what Wall Street expected, according to Refinitiv consensus estimates:

- Earnings per share: $2.27, vs. $2.18 expected

- Revenue: $26.381 billion, vs. $26.378 expected

Sales at stores open at least 12 months rose 2.5% on a global basis and were up 3.0% in the United States. Home Depot said customer transactions were up 3.8% during the quarter, while the average shopper’s ticket increased 2.0%, and sales per square foot were up 5.6%. The company reaffirmed its guidance for fiscal 2019.

Retailers remain in focus this week with J.C. Penney (JCP) and T.J. Maxx (TJX) set to report ahead of the opening bell. On Wednesday, Target Corp. (TGT) will also report its Q1 2019 results ahead of the opening bell and on the heels of an upgrade from Underweight to Equalweight from Morgan Stanley on Monday.

And with retailers in focus, the retail complex continues to see the deterioration of physical storefronts across the nation. The latest in the trend of store closings and liquidations comes from the Dress Barn.

Ascena Retail Group said Monday it’s winding down its Dressbarn business and plans to shut all 650 or so of the women’s clothing stores in order to focus on its more profitable brands. Ascena, which also owns apparel chains Ann Taylor and Loft, said the decision wasn’t an easy one. But the “Dressbarn chain has not been operating at an acceptable level of profitability in today’s retail environment,” Dressbarn CFO Steven Taylor said in a press release.