U.S. equity markets rebounded from their Friday’s losses in a big way, led by the Nasdaq (NDX) that was higher by just over 1% on the trading day. With Google and the U.S. Commerce Dept. loosening restrictions on China’s Huawei, the market looked forward to the next trade headline with a more positive outlook. That outlook may have also been predicated on the resumption of U.S./China trade talks that have been held up recently by China, but appear to resume imminently.

China’s ambassador to the U.S. said Tuesday that Beijing was still open to resuming trade negotiations, and blamed the U.S. for changing its mind too much. In an interview with Fox News, Cui Tiankai said: “China remains ready to continue our talks with our American colleagues to reach a conclusion. Our door is still open.”

Monday found the S&P 500 (SPX) recapturing and closing above the 50-DMA, a key level of resistance. With that being said, it remains to be seen if the key level will hold with FOMC meeting minutes being released on Wednesday. Amid rising tensions and the uncertainty surrounding the impact of the global trade wars, investors will look to the FOMC meeting minutes. The minutes could show if the escalating tensions reverberate into potential changes to monetary policy. At present, we are not of the opinion that global trade issues will shift the tenor of verbiage and discussion within the voting FOMC members.

Eric Rosengren, president of the Boston Fed, said mixed economic signals and a festering trade dispute with China means “the Fed can afford to wait and see” before it takes any action. While the lowest unemployment rate in 50 years indicates the Fed should raise interest rates, Rosengren said, the low rate of inflation normally would result in the central bank cutting rates.

The Fed still expects inflation to reach or exceed its long-run target of 2%, Rosengren, but “given that inflation has under run the target over the last several years, it is wise to admit to some uncertainty about this part of the forecast.” Rosengren’s comments mirror that of fellow Fed President Brainard’s from the previous week and with regards to low inflation.

Fed Presidents from regional central banks such as Boston, Richmond, and Minneapolis have expressed concern regarding the economic impact of the trade wars. The markets continue to steadily price in a possible rate cut later this year in part, due to the trade war issue, but likely more so because of the Fed pausing its rate hikes. Historically, a pause in rate hikes finds a rate cut as the next action taken by the FOMC. At present, the probability of a rate cut by December 2019 has risen to nearly a 70% probability.

Ahead of today’s release of the FOMC meeting minutes, St. Louis Federal Reserve President James Bullard expressed optimism that the United States and China will reach a deal to end their trade war, despite recent negotiating setbacks.

“My base case continues to be that we’ll get an agreement on trade,” Bullard, a voting member on the central bank’s policymaking Federal Open Market Committee this year, said Wednesday in an address at the Foreign Correspondents’ Club in Hong Kong.

He cautioned that there is a risk of tariffs lingering, which could eventually be something the Fed would need to address.

“I would say If we’re going to see major trade barriers stay in place, they would have to at least be in place for six months before you’d start really worrying about it from a monetary policy perspective. It’s natural in a negotiating framework that you would see a lot of maneuvering right before an agreement is reached and I’m hopeful that that’s what we’re observing right now.”

As we mentioned in our latest weekly Research Report, Finom Group isn’t expecting any grand deal between the U.S. and China, but rather a deal that allows both parties to part amicably and with limited damage to their respective economies and reputation. With the 2nd traunch of tariffs now implemented, this has become a U.S. bargaining chip that could be remove, but leaves the initial tariffs in place and viewed as innocuous by both parties. This could have been the strategy all along for the U.S. should it have failed to capture a deal with the initial traunch of tariffs and, as a means of ensuring tariffs remained a key ingredient to offset any lack of deal verification in process over time. If the means of validating the terms of a deal are limited, the tariffs are still there at some level. Having said all of that, any deal or trade truce is likely to find investors more ebullient on the market and prepared to deploy capital. CNBC’s Jim Cramer is of this opinion and as he outlined on Tuesday during the infamous Mad Money show.

“Today’s rally was a reminder that if we do get any breakthrough in the trade talks whatsoever, you’re going to get an epic rebound” the “Mad Money” host said. “Today may smack more of fantasy than of fact, but now you know what the market would feel like if President [Donald] Trump and the Chinese Communist Party can find a way to bury the hatchet. “

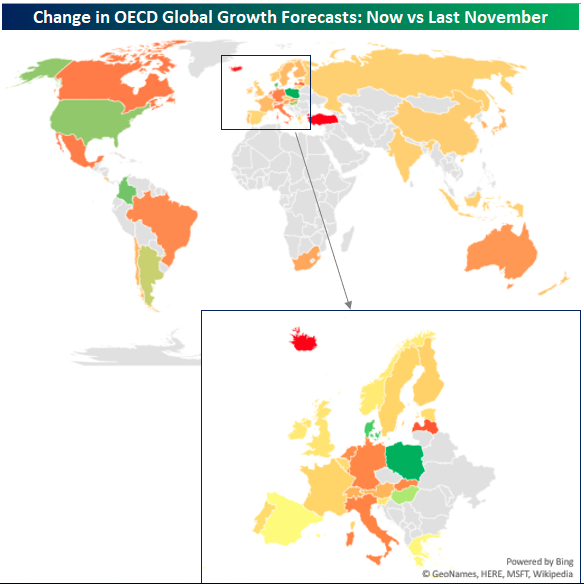

With trade tensions carried forward into the Q2 2019 period, a global economic growth rebound that had been forecasted for the back half of the year has come into question by the OECD. The latest revisions to global growth forecasts for countries in the OECD (Organization for Economic Co-Operation and Development) reflect those concerns.

For the OECD as a whole, 2019 global GDP growth forecasts were cut from 2.12% in November to 1.78% now, marking a 36 basis point (bps) haircut. The map below shows the change in growth forecasts for each OECD country from November to now. Looking at the chart, there isn’t a whole lot of green. Besides the gray shading which indicates non-member OECD countries, most countries are colored in a shade of red to yellow. Of the 45 countries shown, only six saw upgrades to their GDP growth forecasts, and none of the increases were all that significant, as no country saw its growth forecast raised by more than 30 bps. On the downside, however, three countries (Turkey, Iceland, and Latvia) saw their growth forecasts slashed by more than a full percentage point, while another eleven saw growth estimates cut by more than half a percentage point! While no country saw an especially large increase in its growth forecasts, the US, which is by far the largest economy in the world, saw an upgrade to its growth forecast from 2.71% up to 2.82%. China, meanwhile, saw a cut in its GDP growth forecast from 6.2% down to 6.1%, a level of growth that most other global economies would kill for.

In Europe, growth forecasts were cut by a pretty sizable chunk, falling from 1.77% down to 1.22%. Again, countries in the region that saw the largest downgrade to growth forecasts were Iceland, Latvia, Luxembourg, Italy, and Germany. To the downside, Poland, Denmark, and Hungary were the only three countries that saw increases to global growth estimates.

“Everybody is betting today… on a deal between China and the U.S. but the problem is that on the face of it the tensions are getting greater and, second, the problem – the spillover effect of this tension – is becoming more and more evident,” he told CNBC’s Joumanna Bercetche at the start of the OECD’s Spring Forum in Paris.”

As we pivot from the geopolitical and global growth story to the underlying affected earnings, we have recently taken note of the mixed reporting season from the retail sector. J.C. Penney (JCP), Kohl’s (KSS) and Nordstrom’s reported results on Tuesday and all three disappointed investors and all three stocks were hit pretty hard. The department store category of the overall retail sector have seen persistent headwinds to their business over the last decade.

Department store operators haven’t figured out how to increase foot traffic, when more and more customers (especially millenials) are opting to buy things online from places such as Amazon, Rent the Runway and Stitch Fix, Wayfair or are heading directly to brands such as Nike and Kate Spade, skipping a trip to the mega mall or strip malls.

America’s department stores are still struggling, even with efforts to trim their massive real-estate footprints, refreshing bricks-and-mortar stores with modern fixtures and adding more delivery options. For the most part, however, right sizing stores has done little to nothing in the way of offsetting the shift away from physical retail sales declines.

Off-price chains such as TJ Maxx and Ross Stores have been stealing market share from department stores, as have Wal-Mart and Target. These retailers are viewed as being more successful because their stores aren’t found in shopping malls and they promise good value for customers shopping on a budget. Additionally, the hypermarket format ensures that customers can visit such locations to purchase their everyday essentials such as groceries. The traditional department stores simply don’t offer this priority shopping experience that is “needs based”.

Kohl’s missed earnings expectations for its fiscal first quarter and, like Nordstrom, slashed its outlook for the full year. The retailer’s tie-up with Amazon, where it’s been accepting Amazon returns at certain locations, hasn’t yet moved the needle on Kohl’s sales. But that returns program is going nationwide this summer, and Kohl’s said it expects to meaningfully boost foot traffic and hopefully sales. Hope may be the only thing investors have to cling to with the share price falling dramatically on Tuesday. The reality may very well be that the tie-up with Amazon was an act of desperation that actually adds cost to the Kohl’s business operation and through the cumbersome reverse logistics process that accompanies customer returns.

Kohl’s reported adjusted earnings of 61 cents a share on sales of $4.09 billion. Analysts were calling for earnings per share of 68 cents on revenue of $3.94 billion, based on Refinitiv data. Sales at Kohl’s stores open for at least 12 months fell 3.4%, while analysts were calling for a drop of just 0.2 percent.

Kohl’s said it now expects adjusted earnings per share to fall within a range of $5.15 to $5.45, compared with an earlier estimate of $5.80 to $6.15. Analysts had been calling for earnings of $6.04 per share.

CEO Michelle Gass said the year “started off slower than we’d like. Kohl’s home-goods business underwhelmed, as a cooler, wetter start to spring hurt sales of spring goods. But she called these “temporary” issues.”

J.C. Penney also missed Wall Street’s earnings and same-store sales estimates. The company attributed a drop in sales to its decision in February to halt selling appliances in stores. CEO Jill Soltau said the company is “working to reestablish the fundamentals of retail.” But she didn’t offer many details during a call with analysts about how exactly it plans to do that.

Soltau has been building out Penney’s executive leadership bench, though, and Tuesday the company announced it’s hired Shawn Gensch from grocery chain Sprouts Farmers Market to be chief customer officer and executive vice president. Penney is still looking to hire a head of e-commerce.

Penney reported a net loss of 46 cents per share on total revenues of $2.56 billion. Analysts were calling for a net loss of 38 cents a share on sales of $2.56 billion. A year ago, Penney had total revenues of $2.67 billion. Penney’s same-store sales dropped 5.5%, worse than an expected drop of 4.2%.

“Looking ahead, our main concern is not that CEO Jill Soltau will fail to take action nor that she will make the right decisions, but that the company will run out of time and capital to make the necessary changes,” GlobalData Retail Managing Director Neil Saunders said. “J.C. Penney is a very weak operator in one of the toughest sectors of a highly competitive retail market in an era of more subdued demand from highly fickle consumers.”

Target is set to report first-quarter earnings before the bell Wednesday. Here’s what analysts are expecting, based on Refinitiv data:

- Earnings per share, adjusted: $1.43

- Revenues: $17.52 billion

- Same-store sales: up 4.2%

Morgan Stanley earlier this month upgraded shares of Target, calling it a “survivor” in retail. The firm said it believed Target was beyond its “peak margin pain,” as it’s been making investments in its stores, website and supply chain, which have eaten into profits in the near term.

“Now, there are signs Target’s shipping related deleverage is narrowing, particularly as it invests in fulfillment options .. which promote higher traffic and reduce costs,” Morgan Stanley said.

The expectations are moderately high for Target in the Q1 period and with many balls in the air for the retailer to focus on, not to mention the potential threat of increased tariffs on Chinese imports. Although tariffs haven’t necessarily hit the consumer goods level to date, should the remaining $300bn in tariffs move into place, retail profits could be wiped out for the year.

Target’s CEO Brian Cornell took the helm of the Target ship back in 2014. Over that time, the stock has literally gone nowhere and is slightly lower than when he was positioned. Cornell’s first order of business back in 2014 was to discontinue the Target Canada venture and close all newly supplanted Canadian operations. To the extent that the company has been able to grow sales since then, the company has seen limited earnings growth power as gross margins from an increasing focus on the growing grocery category has come at a high cost of goods sold. (Golden Capital Portfolio holds shares of TGT since 2017).

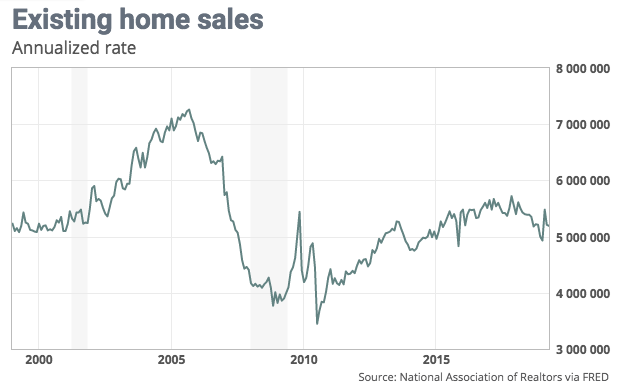

The economic calendar is rather light for Wednesday and with the focus remaining on the FOMC meeting minutes to be released at 2:00 p.m. EST. On Tuesday, however, Existing Home sales disappointed.

Existing-home sales ran at a seasonally adjusted annual 5.19 million rate in April, the National Association of Realtors said Tuesday. That was 0.4% lower than March and 4.4% lower than a year ago. With respect to the disappointing existing home sales data, there are a few variables to keep in mind. The key for housing and the overall economy is new home sales, single family housing starts and overall residential investment. Overall, this is still a somewhat reasonable level for existing home sales.

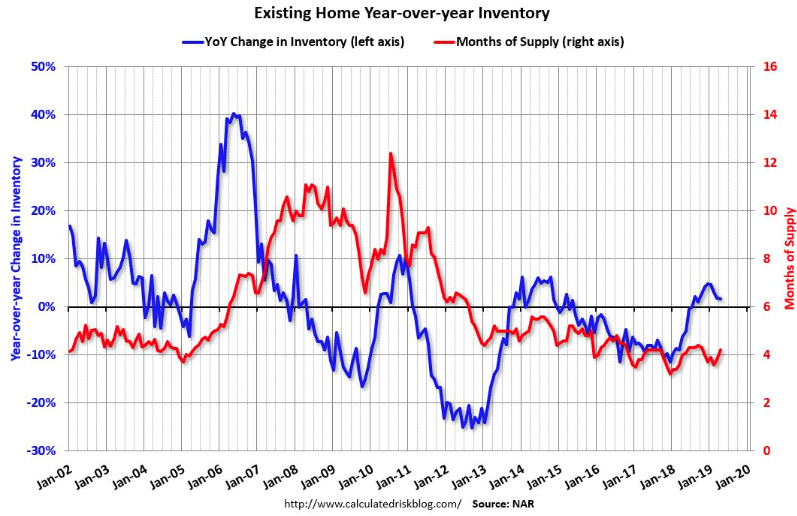

Inventory is still low, and was only up 1.7% year-over-year (YoY) in April. This was the ninth consecutive month with a YoY increase in inventory, although the YoY increase was smaller in April than in the 6 previous months.

Year-to-date sales are down about 4.9% compared to the same period in 2018. On an annual basis, that would put sales around 5.1 million in 2019. Sales slumped at the end of 2018 and in January 2019 due to higher mortgage rates, the stock market selloff, and fears of an economic slowdown.

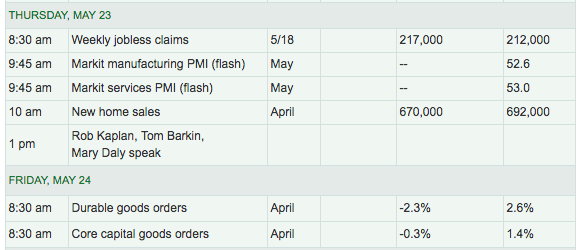

For the remainder of the week, the two key points of economic data will be New Home sales and durable goods orders.

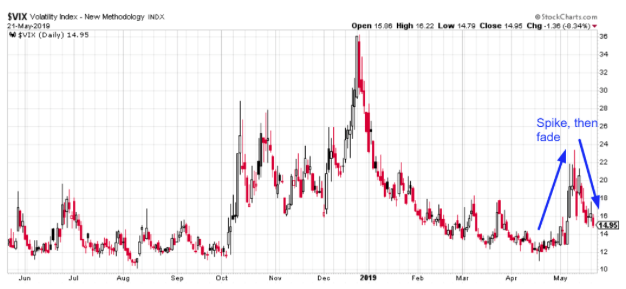

Equity futures are roughly flat ahead of the opening bell and with the VIX having fallen sharply again on Tuesday. Wednesday marks the beginning of another VIX Futures cycle. It seemed as though market participants were in a rush to do one thing on Tuesday and ahead of the VIX May Futures expiration.

Clearly investors were dumping these products all day and into the closing bell, based on the chart above. The VIX itself rose above 20 last week and has since dropped back below 15 rather quickly.

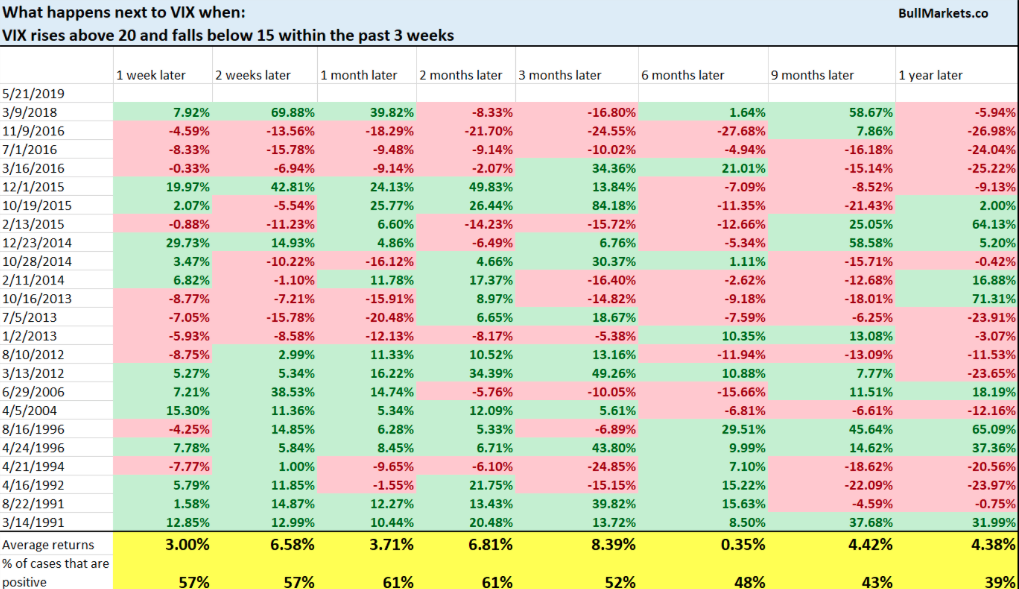

What does this mean going forward? In a recent study by Troy Bombardia he aimed to look at that very question.

According to the table provided, suggests that forward returns over the next 1 week – 2 month for the VIX are slightly more bullish than normal, which demonstrates that many > 50% of VIX spikes tend to come in pairs. This is because many stock market pullbacks and corrections occur in 2 down-waves. While the S&P 500 may make a lower low on the 2nd down-wave, VIX won’t always make a higher high.