Coming into the trading week, Finom Group was of the opinion that last week’s 3%+ drop in the S&P 500 (SPX) was not without more selling pressure near-term. The geopolitical discourse/tensions have become increasingly tenuous due to the escalated trade feud between the U.S. and China and to a lesser extent, skirmishes arising in the Middle East. Here is what we offered in our weekly Research Report, this past Sunday, to subscribers:

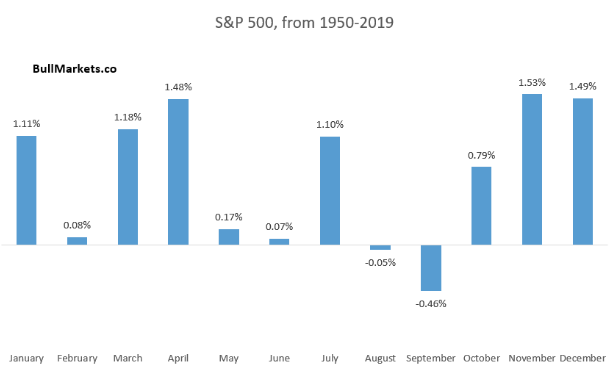

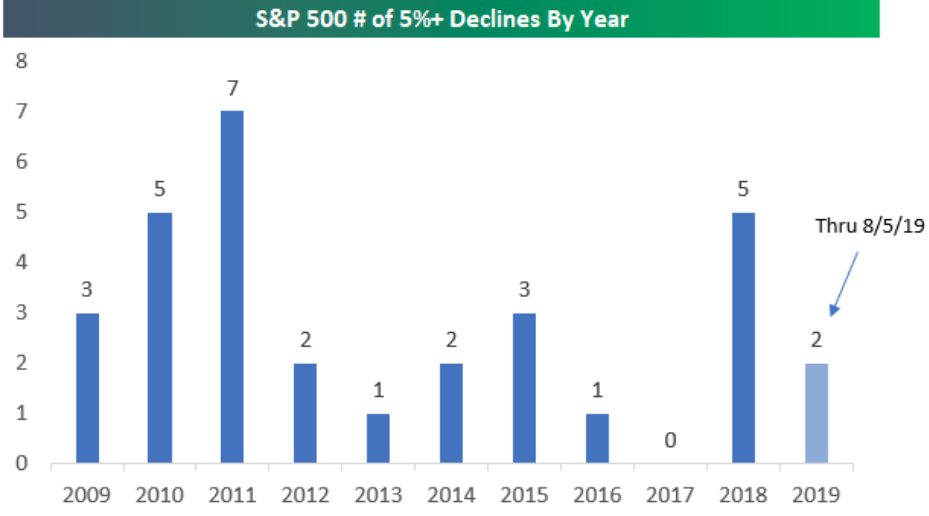

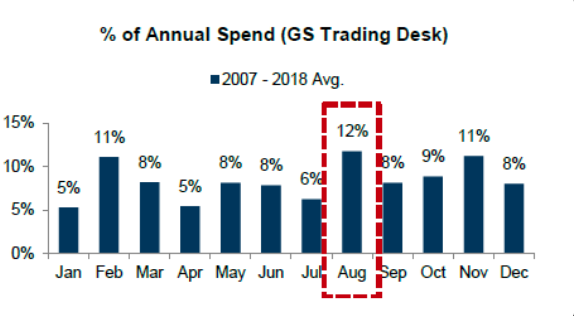

“Finom Group’s conviction of a short-term correction to rebalance portfolios remains high.We believe that correction will occur over the next 2 months to reverse the overbought conditions from the last 45 days.A 3 to 7% correction in August – September is likely and increasingly probable given all that has been stated within our Research Report.” Remember, this is par for the course folks and seasonality looms large as shown in the chart below:

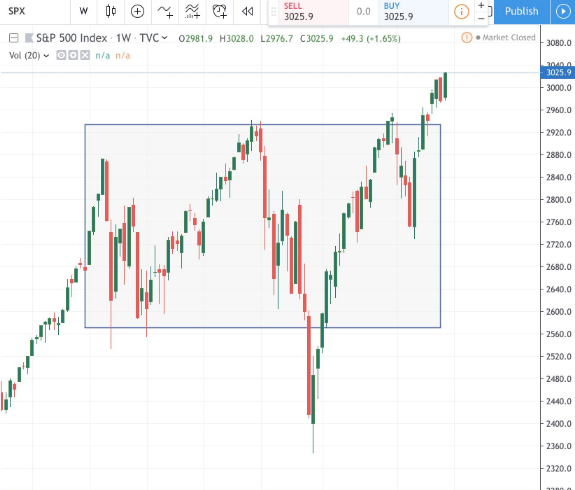

At the risk of highlighting Monday’s near 3%, single day drop in the S&P 500, the benchmark index has now fallen more than 6% from it’s record July highs. But even so, the S&P 500 has not seen the biggest distribution off its highs as some of the index ETFs noted in the graphic below offer:

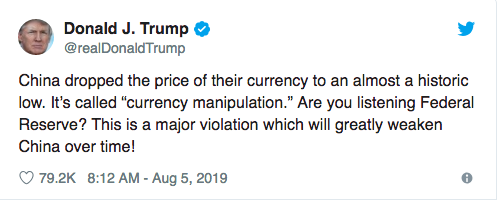

In retaliation of the White House Administration threatening even more tariffs on China late last week and post U.S. delegates returning from negotiations with their Chinese counterparts, China made the conscious decision to not support its currency overnight Sunday and into Monday morning.

There had been a tendency in the markets to think that both China and the U.S. wanted and needed a deal and that the desire to put one in place would soon lead to an agreement, said Paul Christopher, head of global market strategy for Wells Fargo Investment Institute.

“We think China’s moves today signal that they are prepared to use a variety of measures and push these negotiations well into 2020. There’s not going to be an easy deal here for the U.S.

The weakening yuan, meanwhile, also stirred memories of a messy 2015 devaluation of the currency that sent shock waves through global financial markets over several months.”

We have been of the opinion that some great deal would be difficult to achieve between the two diametrically opposed parties for some time now, but that doesn’t mean deescalation could not be achieved. Finom Group has suggested throughout this year-long ordeal that at some point, trade relations would simply revert to the previous status quo with some improvements on intellectual property protections and increased agricultural purchases on the part of China. In return, the U.S. would repeal certain of the implemented tariffs over time.

The aforementioned is status quo because from one White House Administration to the next, checks and balances for such an agreement with China are extremely limited. Secondly, the exercising of tariffs is not one which is widely accepted as a form of reducing trade imbalances and not likely to be continued from one Administration to the next. But with respect to the removal of support from China in relation to the Yuan Sunday, of course this served to disturb the President of the United States…

It’s quite likely that the removal of support for it’s currency was nothing more than a warning to the White House Administration from China. After all, one tariff threat from the U.S. could have been foreseen to have born a response. The fact that on Monday night, China increased the support for the Yuan, boosting it back above the critical 7-crack valuation, lends itself to supporting the notion of a warning having been delivered. And that message was received loud and clear in the bond and equity markets on Monday as bonds soared to their highest level of the year and equity markets came under sharp selling pressure. But what now?

Well, in “response to the response”, the U.S. Treasury Dept. officially labeled China as a currency manipulator.

“Secretary Mnuchin, under the auspices of President Trump, has today determined that China is a Currency Manipulator,” the Treasury Department said in a release. “As a result of this determination, Secretary Mnuchin will engage with the International Monetary Fund to eliminate the unfair competitive advantage created by China’s latest actions.”

The formal designation is the first since President Bill Clinton’s administration in 1994 .

“In recent days, China has taken concrete steps to devalue its currency, while maintaining substantial foreign exchange reserves despite active use of such tools in the past,” the Treasury Department added. “The context of these actions and the implausibility of China’s market stability rationale confirm that the purpose of China’s currency devaluation is to gain unfair competitive advantage in international trade.”

So what does it REALLY mean the U.S. Treasury Dept. can do based on the designation? Nothing, nothing but talk and jawbone to be frank. There’s no immediate threat of penalties/sanctions on China. U.S. law requires a long period of bilateral negotiations. Also 1988 Trade Act being cited where Treasury does not have legal basis to apply penalties (just talk). There’s literally nothing the U.S. can do other than threaten label and attempt other means for which to “correct” China’s behavior with regards to its currency market participations.

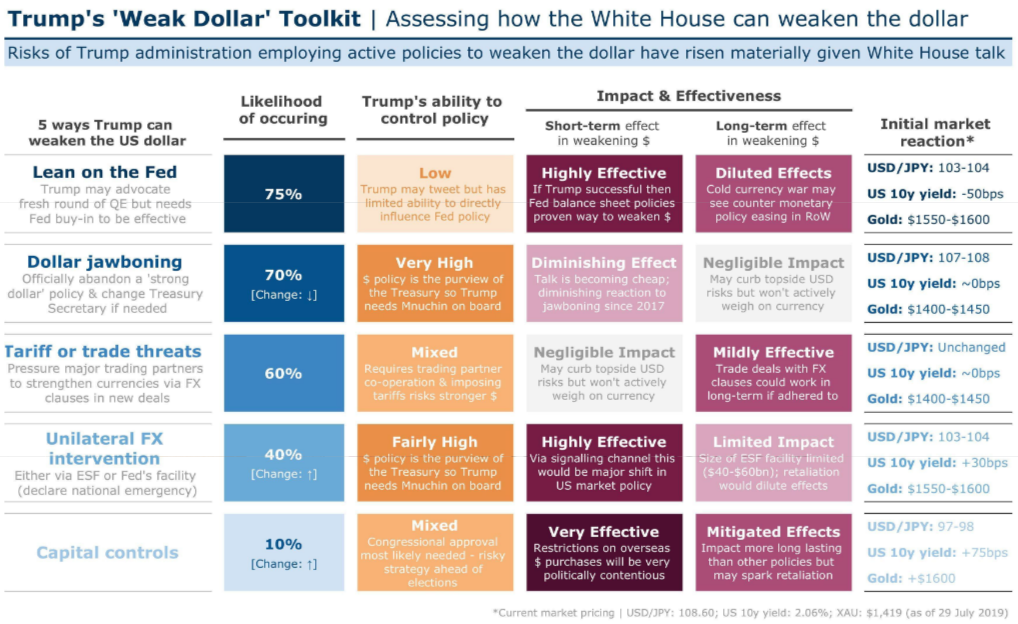

The weakening of the Yuan against the U.S. Dollar serves two purposes presently. First, it can offset the impact of imposed tariffs. Second, it can draw the ire of the White House Administration which has limited ability to course correct the move in the currency market directly. The chart below identifies the means for which the White House Administration can weaken the U.S. Dollar.

Unfortunately, the trade feud is widely seen as having worsened. This is leading many economists and strategists to change their view on when the tensions will ease or when a deal can be reached. Goldman Sachs no longer believes the world’s two largest economies will be able to resolve their long-running trade dispute before the U.S. presidential election in 2020. Analysts at Goldman Sachs, led by Chief Economist Jan Hatzius, said in a research note published late Monday that they had expected the latest spat.

“News since President Trump’s tariff announcement last Thursday indicates that U.S. and Chinese policymakers are taking a harder line, and we no longer expect a trade deal before the 2020 election.

While we had previously assumed that President Trump would see making a deal as more advantageous to his 2020 re-election prospects, we are now less confident that this is his view.

Chinese policymakers are increasingly inclined not to make major concessions and instead are prepared to wait until after the 2020 U.S. presidential election to resolve the dispute if necessary.”

And with regards to the latest currency manipulator designation, here is what Goldman Sachs had to say on the matter…

- While symbolically significant given that this designation was last used 25 years ago, in and of itself we think it is unlikely to result in actions on the scale of recent tariffs or other US sanctions.

- As a practical matter we do not expect it to have major consequences on its own.

- Hatzius sees a 75% chance of a rate cut by the Fed in September and a 50% chance in October, following the reduction last week. He had previously only expected two cuts this year.

So with the markets reeling and all three major averages breaking through key support levels, is it time to step in and buy, especially with the backdrop of increased tariffs looming about? With that in mind, the best way to answer that question is, “What’s your time horizon and risk tolerance.”?

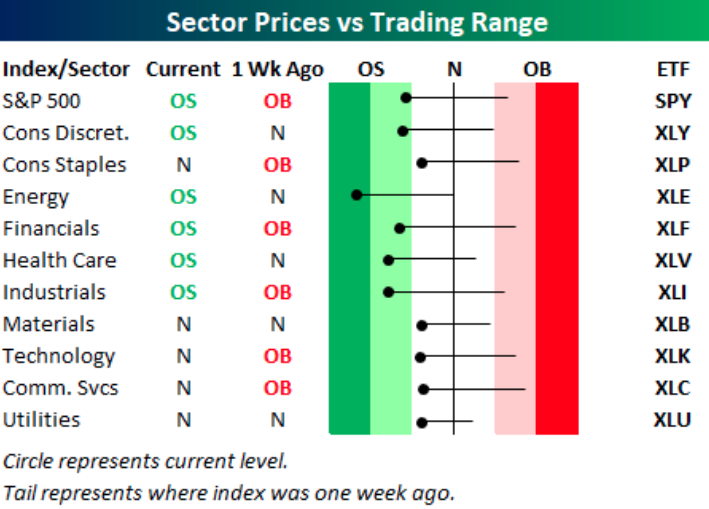

Where once the S&P 500 sectors were mostly in overbought territory, they are now teetering on oversold territory. As we often remind investors, sectors can remain overbought and/or oversold for far longer than many anticipate. Only five sectors are oversold at this point, but all of them are below their 50-day moving averages.

While the current market distribution/drawdown phase seems painful and likely to never return to it’s uptrend, we encourage investors/traders to reflect on the normalcy of such market moves. The reality is that the market has expressed, on average, three 5% pullbacks annually and on average post the Great Financial Crisis.

While it may seem as though the S&P 500 has been slow to make new highs and it certainly has been, the benchmark index did indeed breakout of an 18-month consolidation period. It’s easy to forget this key point of fact as market turmoil and apparent headwinds present themselves with great potency as volatility seeps into the markets once again.

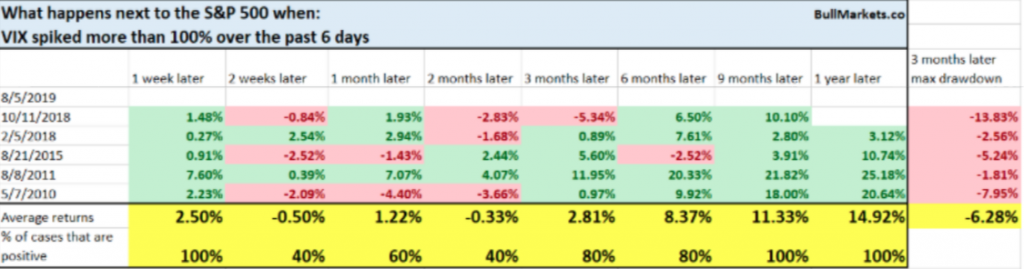

“Volatility is back!” That’s what the media suggests and what most have been saying since last week and with the VIX having risen by roughly 100% in just the last 6 trading days. Volatility is ever-present in the market and it never leaves; volatility simply rises and falls. The fact that it falls for longer periods of time than it rises leads people to suggest or feel as though volatility “is gone”. Therefore, that which has left, must all of a sudden “be back”. Nonetheless, the VIX has risen mightily in recent trading days. What does it mean and what should you do as a trader in recognizing such a move with history as a guide? (Table from Troy Bombardia)

This coincided with short term bottoms in the S&P 500 (up 1 week later) that were later retested or saw lower lows. The lower lows are indicated in the offset column, 3 months later. What this suggests is that any near-term rebound might be utilized to continue lightening up on risk exposure.

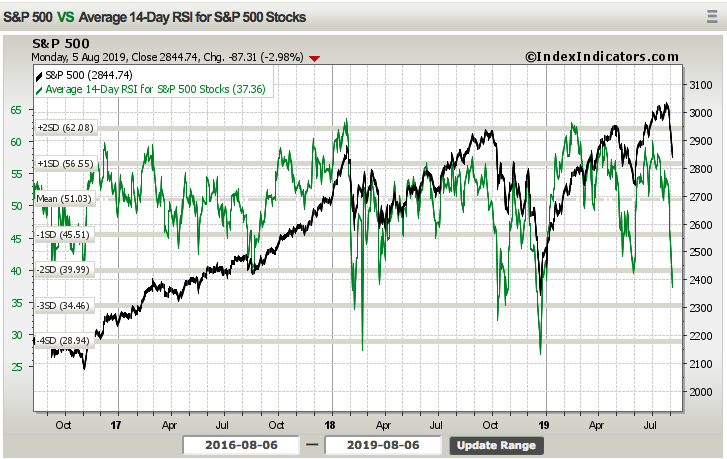

Combined with the VIX spike over the last 6 days, from depressed levels that serve to magnify the move, the S&P 500 14-day RSI suggest a near-term bounce in equity markets.

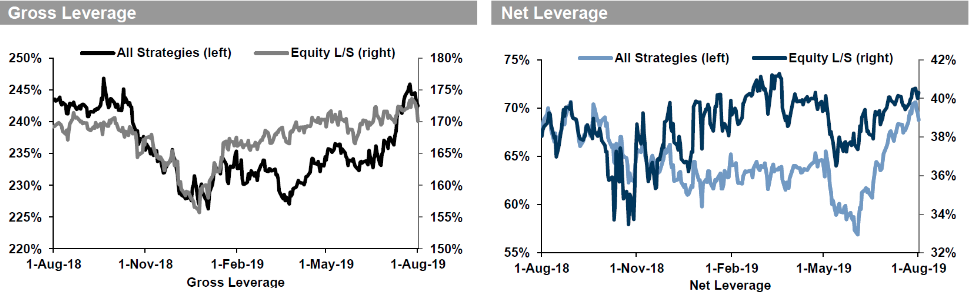

Market breadth has quickly deteriorated and oversold conditions have presented themselves. Keep in mind, oversold does not mean a sustained reversal or reversion to the uptrend is afoot. After all, we are already seeing gross and net equity leverage from long/short funds turning lower. This is likely the case across trend following CTAs as well.

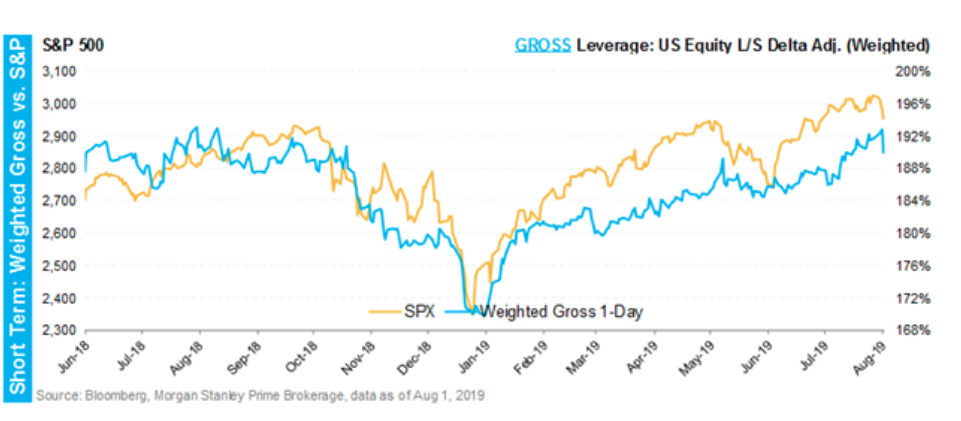

Morgan Stanley shows a similar delveraging of risk at prime brokerages. PBs’ data confirms what we see from others; gross and net small deleveraging in the last week, but still near 12-month highs.

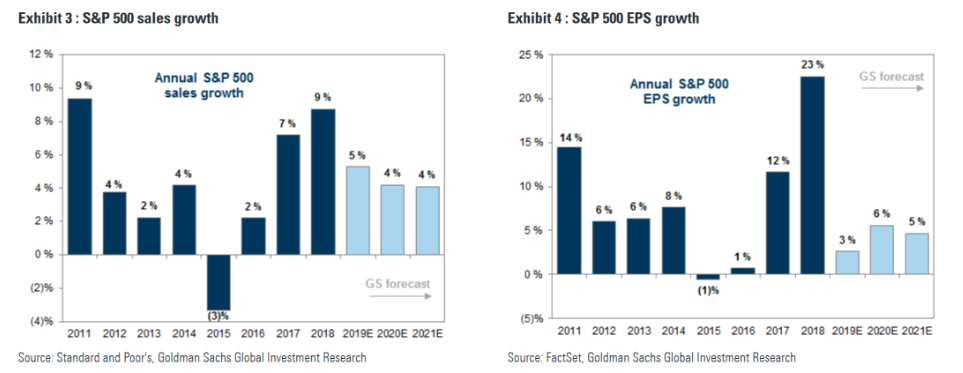

As investor attention has been diverted away from earnings season recently, it’s important not to lose focus on what drives markets over time, earnings. With that being said, earnings continue to come in better than analysts’ estimates and forecasts for the Q2 2019 earnings season are being revised higher. FactSet Data now sees a Q2 earnings decline of -1% vs. the prior week forecast of -2.7 percent. Goldman Sachs also denotes the improvement on a week-to-week basis as we continue to head toward the end of earnings season. The firm sees FY19 EPS growth that is modest, but growth nonetheless. (See chart below)

While earnings are growing in 2019, modestly and even under the pressure of slowing global growth that may prove to slow further and institutional investors are reducing exposure to equities in favor of bonds, don’t forget what corporations are doing.

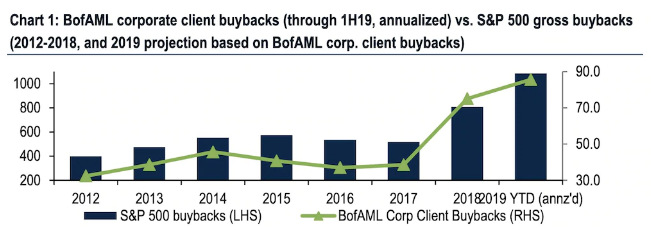

Corporate buyback activity in the first half of 2019 suggests investors could see more than $1 trillion in S&P 500 repurchases this year, according to Bank of America Merrill Lynch. Financial firms have bought back the most stock so far this year, and are expected to authorize more repurchases after many received the Fed’s approval, BAML said.

Here’s what needs to be considered now that August has produced a greater than 5% pullback in the S&P 500 and with respect to August typically being a month for which returns are negative: August is historically a huge month for buybacks, according to Goldman Sachs latest data! Let’s face it, corporations have been the biggest buyers of equities for the last two years. Corporations enjoy repurchasing their own shares so much that they’re on track to break the $1 trillion threshold.

Last point of the day we’d like to offer as we await the latest JOLT survey due out Tuesday morning. The economic backdrop remains supportive of another 6-9 months of expansionary conditions. The present conditions can erode rather quickly should tariff threats turn into tariff impositions on September 1st, as denoted in the latest notes from Morgan Stanley.

“As we view the risk of further escalation as high, the risks to the global outlook are decidedly skewed to the downside,” Morgan Stanley chief economist Chetan Ahya said.

The firm believes a global recession will come in about nine months if the trade war further escalates through the U.S. raising tariffs to 25% “on all imports from China for 4-6 months,” Ahya said. “We would see the global economy entering recession in three quarters.”

Analysts, strategists and economists are often, quite often found with errand forecasts and hypothesis on the market and economy. As new information is delivered and considered, sentiment and forecast adjust to the information to deliver a newer narrative. It’s a reaction to the new information that questions the foresight of the prior forecasts. Given the constant revisions to forecasts, just because new forecasts and hypothesis are new, doesn’t mean they are improved and more effective than the prior. Just saying 😉 !