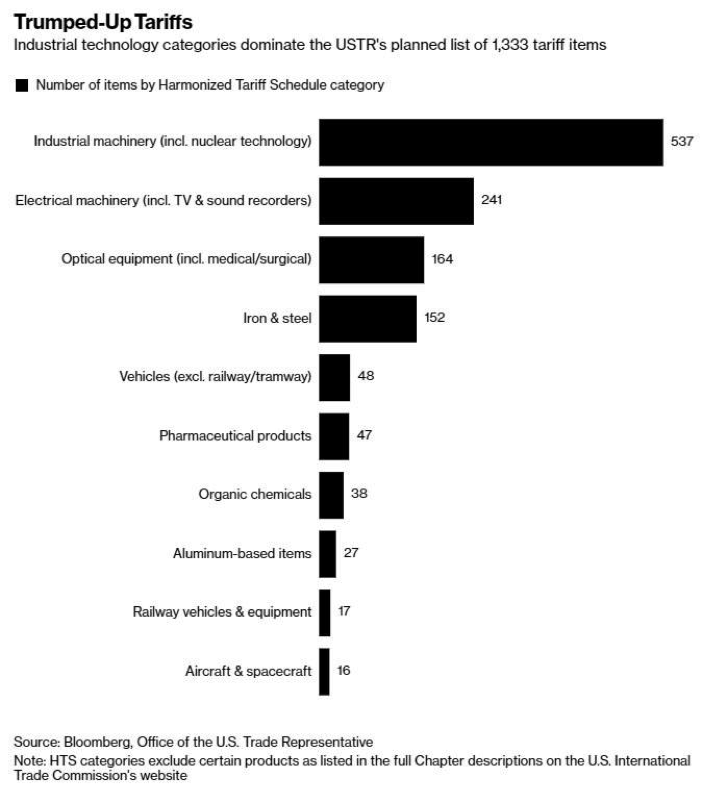

Oh boy, here we go again with the markets reacting to yet another proclamation and/or request for increasing the dollar value of tariffs on China. The news came after a strong U.S. equity market performance Thursday, after the market closed. President Donald Trump said he has instructed the United States Trade Representative to consider $100 billion in additional tariffs against China. The current tariffs proposed on China and according to Bloomberg are shown in the table below:

“In light of China’s unfair retaliation, I have instructed the USTR to consider whether $100 billion of additional tariffs would be appropriate under section 301 and, if so, to identify the products upon which to impose such tariffs,” Trump said in a statement.

The United States is still prepared to have discussions in further support of our commitment to achieving free, fair, and reciprocal trade and to protect the technology and intellectual property of American companies and American people,” Trump said in a statement.”

The S&P 500’s 3-day rally that ended yesterday with a thud in the after hours, as equity futures tumbled in response to the latest trade war rhetoric, is now in jeopardy of reversing to some degree. While White House officials continue with an attempt to level set tariff proclamation rhetoric aimed at China, the President continues to elevate the subject matter, and equity markets react in quick order. Having said that and in the wake of the latest elevated verbiage, the Hang Seng finished its overnight session higher by greater than 1% to 29,844.

One would be hard pressed to find support for the proclaimed tariffs, even if in principle and in response to illegal and unethical trade practices have gone without a response to China for decades. A trade war between the U.S. and China represents the greatest threat to the world economy, the chairman of J.P. Morgan Chase International said on Friday.

“I think it’s the greatest danger today to the world economy,” Jacob Frenkel told CNBC’s Steve Sedgwick at the European House Ambrosetti Forum when asked about the rapidly mounting import tariffs being proposed by the Trump administration and Beijing.

“It’s still not a trade war — I would say there were some skirmishes, and there are skirmishes,” Frenkel said. “I think we should all remember the disaster of 1931 — always good intentions, to protect American jobs, and the result was a catalyst to the Great Depression. We should avoid it at all costs.”

Now that the update concerning the U.S.-China trade dispute is out of the way…but I kid, I kid. Markets will likely continue to contend with the issue through the Friday trading session with bouts of fits and starts. The macro-factor that has become an ongoing sage between the two titanic nations will likely continue to loom large amongst investors for weeks to come, even as the effects of the subject matter numb with time.

“According to a CNBC article, J.P. Morgan US equity strategist Dubravko Lakos-Bujas stated in a note that markets are overreacting to the macro trends and most of this reaction is technical in nature and has nothing to do with fundamentals. He stated that fundamental long-term investors should consider this sell-off as an opportunity to buy at the dip.”

The market has a defined way in which it deals with repetitive stimuli. For as long as the same stimuli is discussed and without realized consequences or determinations, markets tend to look past the stimuli that, in this case is trade war rhetoric. Oppenheimer Funds chief investment officer Krishna Memani stated that the trade issues with China would not settle in a day. This stock market volatility is being driven by traders who are trying to guess if there could be a trade war or increased protectionism at a time when increasing interest rates are raising concerns about inflation. Thus, they are reacting to even the slightest positive or negative news.

While we are aware that tariff talks/threats/rhetoric will repeat throughout Friday’s trading session, investors will have other subject matter to focus on as well. Traders are looking ahead to two big economic events Friday, the release of U.S. March payroll data and a speech by Federal Reserve Chairman Jerome Powell who is expected to play down the notion that the economy is overheating and/or the notion that the Fed will accelerate rate hikes in 2018. The Fed chairman is likely to continue to stress that there are no signs of runaway inflation, and maintain a wait-and-see stance, said Andrew Hollenhorst, U.S. economist at Citigroup.

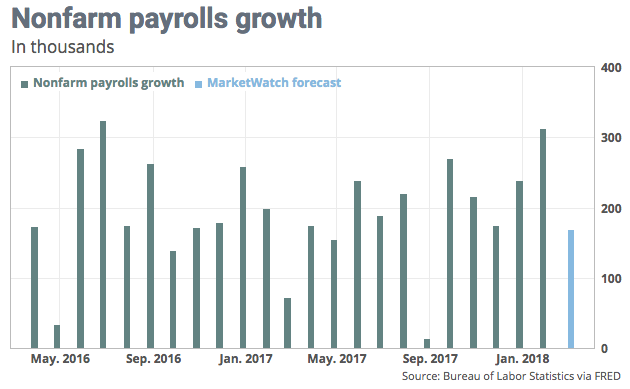

With mounting investor concerns for Friday’s trade, a positive week on Wall Street hangs in the balance. As of Friday, the Dow is looking at a gain of 1.7% for the week, while the S&P 500 is poised to gain 0.8 percent. A weekly advance for the Nasdaq is on the line, with the index up just 0.2% as of Thursday’s close. March nonfarm payrolls data are due at 8:30 a.m. Eastern Time. Economists polled by MarketWatch are forecasting an increase of 170,000, below February’s strong 313,000 gain.

Economists forecast a 0.2% rise in hourly pay in March, which would grow the annual gain to 2.7%, from 2.6 percent. The unemployment rate already sits at a 17-year low of 4.1% and it’s widely expected to dip below 4% in the near term.

In the 5:00 a.m. Eastern Time trading hour, U.S equity futures are sharply lower, although not in peril at the moment. Naturally, volatility and the VIX are higher in the pre-market with the VIX reading above 20 yet again, up some 8% thus far. Volatility fell sharply over the last two trading sessions, but continues to plague a market that has become destabilized due to a number of macro factors that have little-nothing to do with actual corporate fundamentals. At finomgroup.com, we continue to trade the volatility complex daily and weekly with strong results. Despite the elevated levels of volatility that have persisted this week, Finom Group has outlined 3 separate, short-volatility trades through its private Twitter feed as outlined below.

Given the ramp in volatility already taking place in today’s trading session, we believe another short trade will present itself. Become a subscriber today and join receive our trade alerts! Also, listen to Seth Golden’s latest discussion on market volatility and macro-factors with David Lincoln in this YouTube video .

Friday will prove to be another interesting trading day to end what has been a very volatile trading week. The S&P 500 remains above its 200-day moving average after a 3-day rally on Wall Street and begs of investors to focus on the fundamental backdrop of corporate earnings that will come into greater focus next week, as earnings season kicks-off. Have a great trading day and weekend all!