Here we go again with tariff headlines front and center. The Trump administration on Tuesday evening released a list of 10% tariffs on $200 billion in Chinese goods, broadening trade war conditions with Beijing. The tariffs will not go into effect immediately but will undergo a two-month review process, with hearings Aug. 20-23.

Immediately after the news broke on Tuesday evening, U.S. equity futures turned sharply lower. Asian equity markets followed, opening in the red overnight and closing 1.5% lower across the key Asian equity markets. European equity markets have followed suit and are red across the board with President Trump currently on his European/NATO tour. At present, U.S. equity futures are lower by roughly 1% on the heels of trade war escalation probabilities.

The tariff headlines have halted what has been a rather strong market rally in the U.S. as of late. The major averages completed a 4-day rally prior to the news with the S&P 500 brushing up against 2,800. Economic data won’t save the market rally today, as the calendar is rather light with only Producer Price Index finding some semblance of relevancy against the backdrop of tough tariff talks.

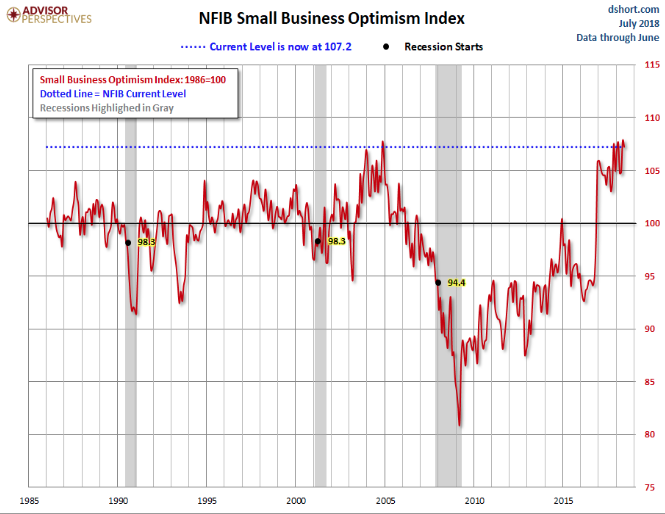

Yesterday’s highlighted economic data was another feather in the cap for economic bulls. The latest issue of the NFIB Small Business Economic Trends showed continued strength. The headline number for June came in at 107.2, down 0.6 from the previous month. Here is an excerpt from the opening summary of the news release.

“The Small Business Optimism Index posted its sixth highest reading in survey history for the month of June, at 107.2, down 0.6 from May. Since December 2016, the Index has averaged an unprecedented 105.4, well above the 45-year average of 98 and rivaling the all-time high of 108.0 in July 1983.

Small business owners continue to report astounding optimism as they celebrate strong sales, the creation of jobs, and more profits,” said NFIB President and CEO Juanita Duggan. “The first six months of the year have been very good to small business thanks to tax cuts, regulatory reform, and policies that help them grow.”

Economic data points to an economy picking up steam in the second quarter. Global growth appeared to wane in the first quarter, but the world economy has showed signs regaining its footing during the second quarter. Worries that an escalating trade war between the U.S. and China, could dent global growth certainly explains and examples investors’ sensitivity to trade headlines.

The newly announced U.S. tariffs not yet implemented but in process, on China have largely been telegraphed for several weeks now. Tuesday nights headline announcement and investor reactions around the world on Wednesday likely example that many were optimistic that threats would not find process. With the process of further tariffs now underway, investors are weighing risks of the unknown to come. The announcement has come at what may prove to be a less optimal time, as earnings season kicks-off with banks reporting on Friday.

Bank stocks and the broader financial sector stocks have underperformed the benchmark in 2018. But bank analyst Dick Bove isn’t in the bear camp when it comes to the sector. According to the chief strategist at Hilton Capital Management on CNBC’s “Trading Nation” on Monday, second-quarter earnings should shock financials back into rally mode.

“In terms of looking at the earnings for the quarter, you know loan volume is up. Margins are going to be flattish, but positive. Loan losses are not likely to be very bad. Expenses are going to be controlled,” Bove said.

Bove acknowledged the disconnect between the banks’ strong fundamentals and disappointing stock performance. He blames buyback announcements from many of the nation’s largest financial institutions.

“When the companies comes to you and say we’re going to pay you back, in the case of Citigroup, $60B over a three-year period, you have to ask yourself, ‘Why couldn’t you use that in the business?’” said Bove. “The companies are giving a very negative message.”

Where Dick Bove finds the banking and financials ready to march higher in the back half of the year, Instinet’s senior equity trader Frank Cappelleri is found with a similar opinion. Cappelleri has a favorite in the bank sector as well.

“Wells Fargo got hit especially hard” earlier this year, Cappelleri told CNBC’s on Monday, pointing to a 25% drop from its year-to-date peak in late January to trough in mid-April. Since then, it’s been doing much better than the XLF here, outperforming.”

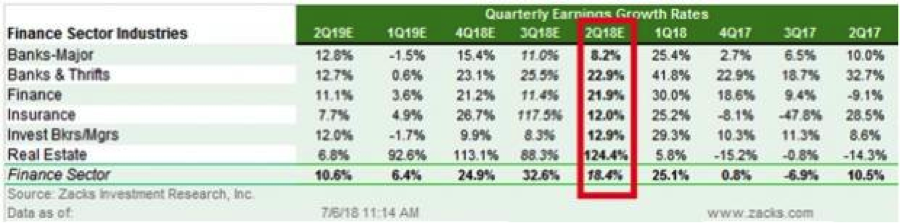

As shown in the chart, earnings are expected to be strong. More importantly, they are expected to be even stronger in Q3 and Q4. But this makes it all the more relevant for investors to focus on reported guidance when the banks release their quarterly reports and commentary. Michael Bapis of Hightower Advisors also finds favor in the banking sector that is expected to show strong earnings growth this quarter.

As shown in the chart, earnings are expected to be strong. More importantly, they are expected to be even stronger in Q3 and Q4. But this makes it all the more relevant for investors to focus on reported guidance when the banks release their quarterly reports and commentary. Michael Bapis of Hightower Advisors also finds favor in the banking sector that is expected to show strong earnings growth this quarter.

“We’re very bullish on the space. It’s kind of flown under the radar this year; it’s lagged the rest of the sectors. There’s a rising interest rate environment. There is fiscal tax stimulus. That’s only going to help them. We expect earnings to be positive at the end of the week. If that changes, then obviously the whole sector would get hit, but we would buy on any weakness, and we would continue to own the space going forward.”

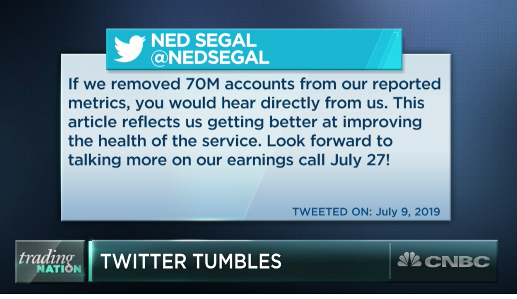

Another one of Michael Bapis’ picks is Twitter (TWTR). Twitter shares have moved lower over the last couple of days after rising consistently throughout 2018, even as trade rhetoric has disrupted the broader market. On Monday, shares fell by as much as 10% on fake account elimination news. Since going public in November 2013, Twitter shares have fallen by more than 8% some 19 times, exampling the belief in the business model, but maybe not so much of a belief in the valuation.

Twitter shares fell sharply on Monday on reports it had suspended as many as 70 million fake accounts in May and June. Nearly half of those losses were pared on assurances from the firm’s chief financial officer. Its drop takes it back to levels seen. Michael Bapis sees little of Monday’s sell-off affecting the company’s long-term prospects.

“We look at it as a light breather,” Bapis said on Monday’s “Trading Nation.” “We think going forward you still use the verb ‘tweet’ and until somebody changes that we’re cautiously optimistic on the company.”

Finom Group also likes what shares of Twitter may offer near-term in the way of pulling back. Fundamentally speaking, the company has been hitting on all cylinders. Where previous years the focus had been on average month users, the tide has since shifted to rationalizing user growth with revenue growth. Like Facebook, the platform is quite unique and finds advertisers the ability to market their brand and products more directly to consumers.

Revenue from the latest quarter was up 21% year over year, and the company expects to be profitable for 2018 after beating analysts’ estimates in the Q1 2018 period. In a world where investors may be of the opinion that Twitter is battling Facebook for ad revenues, the reality is most vendors are forced to use both mediums to market their products and brand.

When we take a look at the technicals, we still see that shares of TWTR are well above the 50-day moving average.

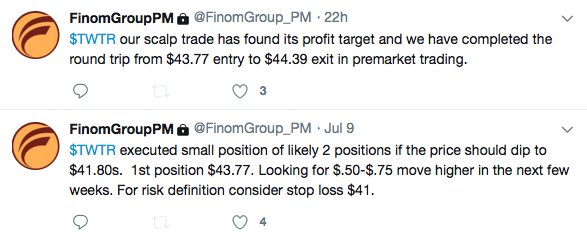

There may be some further room for the stock to fall, especially as markets pullback as a whole. Finom Group would look for trading opportunities in the name given its propensity for wild intraday and weekly swings. We recently traded the name on Monday’s dip as displayed in the screenshot below from our private Twitter feed.

Heading into Friday’s bank earnings, global and U.S. equities look like they are going into retreat. It’s likely that White House officials and advisors will be out and about in the news today, discussing the recent tariff announcement and as such these conversations may prove market moving. Expect trading to be heavy today and volume to be higher than recent days given the aforementioned.