One day the markets are rallying and the next day the markets are sinking. While the direction seems ever changing, the themes are pretty consistent of late, Turkish lira, trade tariffs and emerging market contagion risks. Yesterday, investors decided that in the absence of “more” favorable market news, it would be a risk-off day. By and large, Finom Group believes U.S. investors were simply following the risk-off atmosphere led by overseas markets. Once those overseas markets closed, however, Wall Street found itself able to rally off the intraday lows.

Turkey and the Turkish leader has been the predominant fear gripping investors in the last 2-week period. Finom Group believes such fears are overblown, very much misunderstood for correlation and likely to be proven as such with time. But what are economists saying about the matter. Agathe Demarais, principal economist at the Economist Intelligence Unit offered the following just yesterday on the subject.

“The factors that are driving the lira down appear mostly country-specific and so the slump in the lira should not trigger a full-blown currency crisis in most other emerging market.”

“The Turkey crisis is largely idiosyncratic, although its triggers are often external factors,” said TD Securities strategists led by Christian Maggio, head of EM strategy.”

Overall, analysts aren’t as concerned about contagion risk. Nonetheless, because the crisis Turkey is facing is unique to its circumstances, they will keep watching for signs of deterioration in other currencies that are driven by similar but idiosyncratic factors. History doesn’t repeat itself very often, but it does have a way of extrapolating fear from like situations of yesteryear. That is largely what economists who call upon history as a guide for the future present and what winds up grabbing headlines. The media tends to polarize what will gain the most clicks, views and retweets, right? As it pertains to the Turkish lira crisis, economists are harkening back to the Asian currency crisis of 1997. The chart below identifies how the S&P 500 performed during that period and how fear drove investor activity more so than actual damage projected to be caused by the Asian crisis.

As depicted in the chart from 1997-1998 of the S&P 500 above, the U.S. stock market made a very sharp decline, after which it quickly recaptured previous levels. Contagion fears are almost always short-lived and found with great error. Turkey is not a big economy. The U.S. economy is $19 trillion. The Turkish economy is $857 billion, less than 5% the U.S.’ size. The U.S. has singular companies that are bigger than the totality of the Turkish economy. And no, the Turkish situation is not even comparable to the tiny economy of Greece that caused so much market turmoil from 2010-2011. Turkey is not a part of the EU and would therefore not lend itself to similar concerns of disengaging from a large economic union. Everything put forth here, within this narrative, is largely absent media dialogue and consideration, unfortunately!

With Turkey out of the way, for now, let’s not forget that China’s yuan is what investors should more prominently focus on. For now, the yuan is showing stabilization, for now. As such, again one can see the media’s role in the market. It seems to find a way to find “the fear” that preys upon unsuspecting investors. Moving on…

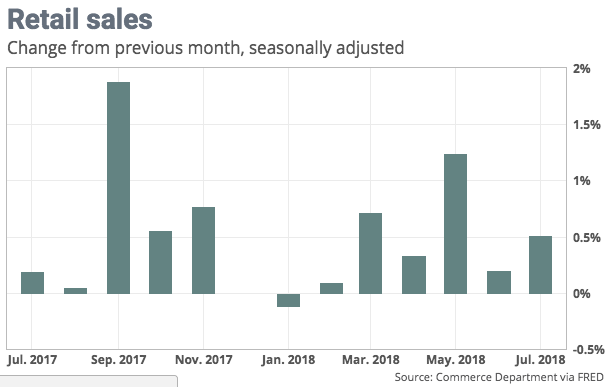

Speaking of economic data, as if we should focus on drivers of the U.S. economy right? Yesterday’s reported retail sales came in much stronger than anticipated. Having said that, revisions to the prior month offset the strength as investors found themselves selling retail stocks and the sector as a whole.

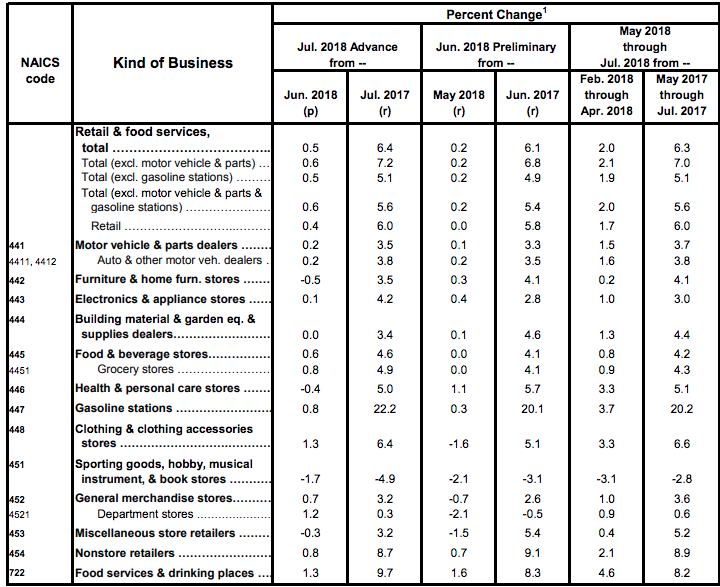

The Census Bureau’s Advance Retail Sales Report for July was released this morning. Headline sales came in at 0.5% MoM to one decimal and was better than the Investing.com forecast of 0.2%. Core sales (ex Autos) came in at 0.59% MoM (to two decimals). Revisions were made to May and June figures.

“Advance estimates of U.S. retail and food services sales for July 2018, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $507.5 billion, an increase of 0.5 percent (±0.4 percent) from the previous month, and 6.4 percent (±0.5 percent) above July 2017. Total sales for the May 2018 through July 2018 period were up 6.3 percent (±0.5 percent) from the same period a year ago. The May 2018 to June 2018 percent change was revised from up 0.5 percent (±0.4 percent) to up 0.2 percent (±0.2 percent)*.

Retail trade sales were up 0.4 percent (±0.5 percent)* from June 2018, and 6.0 percent (±0.5 percent) above last year. Gasoline Stations were up 22.2 percent (±1.6 percent) from July 2017, while Nonstore Retailers were up 8.7 percent (±1.4 percent) from last year.”

Although the July report of retail sales showed a continued strength in retail sales, the June period was revised downward from an initial reading of .5% MoM growth to .2% MoM growth. Nonetheless, the trend is strong for retail sales and has strengthened since the 1st quarter of 2018, as depicted in the chart below.

Retail sales have increased 6.4% over the past 12 months, close to the long-run average since 1980.

“The July retail sales report indicates that the momentum heading into the third quarter remains solid, which bodes well for consumer demand and overall economic growth,” said Gregory Daco, chief U.S. economist at Oxford Economics.”

When we look further under the hood of the monthly retail sales report, here is what concerns Finom Group’s chief market strategist Seth Golden:

- Department store sales are growing so very meagerly at 1.2% MoM, but only .3% YOY. That’s troublesome.

- Nonstore/digital sales are growing .8% MoM, but a strong 8.7% YoY.

- Taking the two factors into consideration, the conclusion to draw is that department store or physical storefronts are losing market share to digital sales at a continued, alarming pace.

- Investors need to look at both the number of physical storefront closures, (Mattress Firm recently announced bankruptcy protection and store closures) as well as inventory level decisions by the major chain store retailers.

- The retail “apocalypse” as its been caused is real, vibrant and ongoing despite the pause in retail quarterly reports.

- Not all retailers are created equal; some are more advantaged by their respective in-store offerings than others.

- Physical store retailing will continue to come under pressure and renew the 2017 fears in the not too distant future as inventory reductions give way to the inevitable and further store closures.

With July’s robust retail sales report on Wednesday, investors were also delivered one of the bigger department store retailer’s results in the way of Macy’s Q2 2018 quarterly report. The results were actually quite positive, beating analysts’ estimates on both the top and bottom line, but…

Macy’s reported adjusted earnings of 70 cents per share, blowing past the FactSet consensus of 50 cents per share. Sales of $5.57 billion also exceeded the $5.55 billion FactSet consensus, though the top-line figure represented a decline from the year-earlier $5.64 billion. Yes, sales are still in decline for the department store retailer after a great many initiatives have been put forth to return the company to sales growth.

Macy’s also raised its guidance, telling investors now to expect adjusted EPS of $3.95 to $4.15 for fiscal 2018, up from previous guidance of $3.75 to $3.95. Sales are expected to range from flat to 0.7% growth. And same-store sales on an owned-plus-licensed basis are expected to increase 2% to 2.5%, with same-store sales on an owned basis 20 to 30 basis points below that. The FactSet consensus is for EPS of $3.86 and same-store-sales growth of 1.6%.

Shares of M have soared since hitting a floor in the upper teens last year. One can easily blame the reaction to positive results in Q2 on profit taking, but that may be found erroneous as time unfolds. As Macy’s has not yet returned to sales growth, even with margins expanding, investors are likely to take profits after such a massive run. But recall Seth Golden’s denotations about inventory levels for department store retailers. Now, here is what Macy’s offered on its conference call yesterday concerning margins and inventory levels:

“Gross margin in the quarter was $2.25 billion or 40.4% of net sales, 80 basis points higher than last year, benefiting from our much-improved inventory position this year, as well as our strong sales performance. We ended the quarter with inventory down 40 basis points on a comparable basis. This year-over-year decline in inventory is less than it was in the first quarter, as we cycled the clearance of excess inventory during the second quarter of 2017 creating a more difficult comparison.”

Inventory level reductions positively affect all aspects of the supply and logistic chain for a retailer. The operation reduces expenditures greatly and subsequently reduce costs per sold good. As such, gross margins tend to improve. But the underlying problem is the reasoning for reducing inventory. This is the problem that needs fixing and based on Macy’s results, inclusive of a plethora of anniversaried initiatives, there seems to be no solution in reach. Moreover, with all that Macy’s has done to reduce costs and monetize real estate assets, cash flows are stagnating.

Having said all of that, shares of Macy’s may retrench momentarily and return to previous momentum in favor of achieving upwardly revised guidance. Longer-term, Macy’s faces the consistent and inevitable decline in market share being expressed in most every monthly retail sales report over the last 4 years. By the measure of growing retail sales, Macy’s is greatly underperforming the market, verifying its lost and continual losing market share. It’s a real problem that some investors focus on, even as shares of M have performed well over the last few quarters. Here is how Neil Saunders, managing director of GlobalData Retail colors Macy’s outlook:

“The sales numbers are strengthening, but they are doing so off the back of a very strong consumer economy, and it remains the case that Macy’s growth is below that of the retail market. When factoring in the bump from the state of the consumer, by our calculations, it is still losing market share across a number of categories.”

We’re not here to “poo poo” Macy’s results, but rather to level set the near term results with the long-term outlook. Seth Golden suggests the long-term outlook for Macy’s has limited upside and could mirror the likes of J.C. Penney by 2021. Golden forecasted the onslaught for retailer that was 2017 in his notes to clients as early as October of 2016.

“What the team at focusedstocktrader.com and I are concerned about is the downward trend in retail sales. My colleague Seth Golden notes in his institutional report that, besides the April 1.2% outlier, sales have been anything but inspiring.”

From that quote in 2016 and through 2017, the retail sector stocks were rocked by store closures and lost market share. While stock prices have recovered to some degree or another, market shares have not, not a bit for brick and mortar retailers. Asset sales and inventory reductions can only last so long!