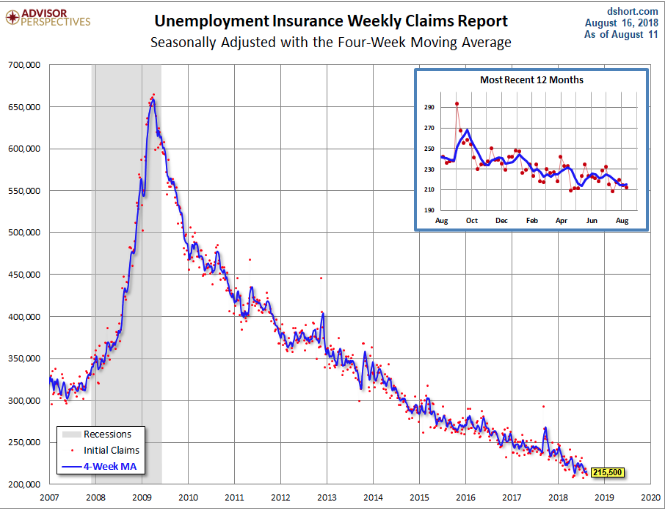

Two of the most critical economic data points have shown that the economy is continuing to show improvement. The U.S. is a consumer driven economy and as such labor and employment remains atop the economic indicator reports for Finom Group. Initial jobless claims were released yesterday and as they are every Thursday. Initial jobless claims are a measure of layoffs in the United States. The data showed that initial jobless claims fell in early August and returned near a post-recession low. New claims declined by 2,000 to 212,000 in the seven days from Aug. 5 to Aug. 11. Economists polled by MarketWatch had forecast a 215,000 reading.

Millions of new jobs have been created since 2010, which puts more money in Americans’ pockets and in turn back into the economy. This week’s report was the record 180th straight week of sub-300K claims, the 45th straight week where claims were at or below 250K (longest streak since 1970), and the 6th straight week that claims were at or below 220K (longest streak since 1969). Below is a chart of jobless claims since the Great Recession, quite a remarkable chart at that.

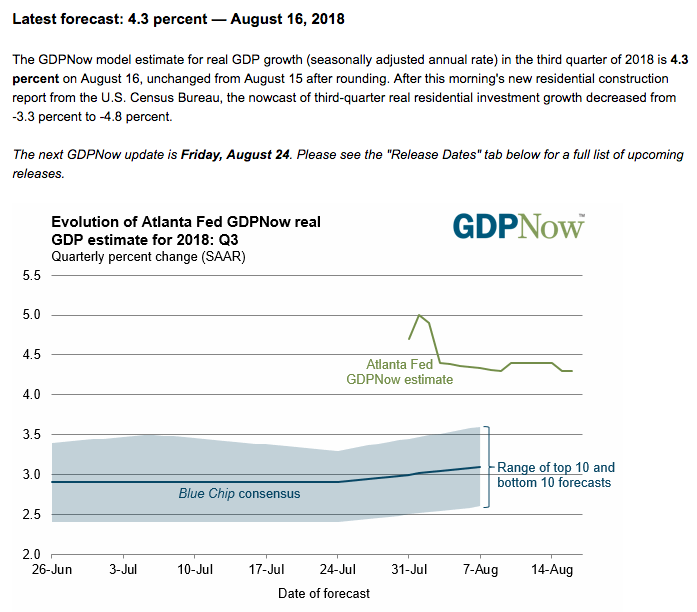

Coupled with this week’s strong retail sales report, showing retail sales grew 6.4% YOY, jobless claims hovering around all-time record lows portends well for Q3 2018 GDP. Many economists believe the economy will grow above 3% in the quarter on strong consumer spending and labor market conditions. According to the Atlanta Federal Reserve’s GDPNow forecast model, the U.S. economy is growing at a 4.3% annualized rate in the third quarter. (See screenshot below)

The model raised its forecast on personal consumption expenditures growth in the third quarter to 3.1% from 2.9% after the July figures on retail sales. And nowhere was it more representative of improving retail sales and consumer spending than in the Q2 2018 earnings report for Wal-Mart (WMT) on Thursday. Wal-Mart Inc. reported same-store sales growth at the strongest levels in more than a decade.

U.S. saw same-store sales jump 4.5% during the second quarter, with traffic and ticket growth of more than 2%. Sales of $128.0 billion beat the FactSet consensus of $126.0 billion. At the same time, operating income fell to $5.75 billion from $5.97 billion last year, and expenses rose to $26.7 billion from $25.9 billion year-over-year.

Wal-Mart executives said that online grocery is giving that segment of the business a boost, attracting new customers and driving existing customers to add an extra item to their baskets. E-commerce growth was 40% for the quarter and the company expects growth to be 40% for the year.

“We believe Wal-Mart is fiercely holding its own in the competition vs. Amazon which is highly relevant given that 86% of Wal-Mart shoppers also shop at Amazon, based on Cowen research,” wrote Cowen & Co. analysts led by Oliver Chen in a Thursday note.

On the heels of strong corporate earnings and improving economic data from the prior week and on a YOY basis, equities rallied sharply on Thursday. The Dow Jones Industrial Average surged 396.32 points, or 1.6%, to 25,558.73. It was the blue-chip index’s strongest one-day performance since April 10, when it surged 429 points. The S&P 500 index advanced 22.32 points, or 0.8%, to 2,840.69, led by telecommunications services, consumer staples and financials. The Nasdaq Composite Index added 32.41 points, or 0.4%, to 7,806.52. Although the earnings and data backdrop proved of value to investors yesterday, the reconvening of trade talks between the U.S. and China was also highly relevant to investors, boosting confidence that a deal would get done.

White House economic advisor Larry Kudlow confirmed Thursday that the U.S. and China will resume trade talks later this month, but warned that President Donald Trump has a strong resolve to make sure the administration gets a good deal.

“The Chinese government, in its totality, must not underestimate President Trump’s toughness and willingness to continue this battle to eliminate tariffs and nontariff barriers and quotas, to stop the theft of intellectual property and to stop the forced transfer of technology,” Kudlow said in a “Squawk Box” interview. “Those are the asks that we’ve been making now for quite some time.”

The mid-level talks will likely be about “how exactly are they going to deal with the RMB (renminbi),” said Robin Brooks, chief economist at the Institute of International Finance, referring to another name for the yuan. On Friday morning in Asia, the dollar traded to 6.89 against the Chinese yuan and just shy of 7, a level last expressed in May 2008.

Undoubtedly, resuming talks between the U.S. and China has improved investor sentiment. More importantly and in keeping with the fundamental market outlook for 2018, the underpinning of the markets remain corporate earnings. Corporate earnings are driven by the demand of goods/services and facilitated by the consumer. So what is Goldman Sachs suggesting about the consumer? Let’s take a look!

Goldman Sachs just carried out a survey of 2,000 consumers. The survey revealed that consumer optimism is at record highs while pessimism is at record lows. To be clear, this survey first began in 2005.

“The impact of strong demand drivers and strong consumer sentiment is evident in consumer spending,” writes Goldman’s consumer analyst Matthew Fassler. He adds, “We remain confident in the trajectory of the consumer recovery, as drivers of spending remain solid. We note signs of moderating momentum from May through July, and soft patches in housing, but remain constructive on the outlook for discretionary.”

With a strong outlook for the consumer, Goldman Sachs suggests investors buy the following stocks with a Conviction Buy rating:

- Wyndham Hotels & Resorts – GS upside potential of 44%

- Aramark Holdings – GS upside potential of 38%

- Las Vegas Sands – GS upside potential of 31%

- Mondelez International – GS upside potential of 23%

While Goldman Sachs is validating its case for the consumer and consumer discretionary stocks, Jim Cramer is pounding the table for oil stocks. In his latest rant on the CNBC “Mad Money” show, the host offered the following:

“Everyone hates the oils, which means it is time to buy the oils because oil’s going from $70 to $80. Everybody is all crazy about them. Royal Dutch is really good.”

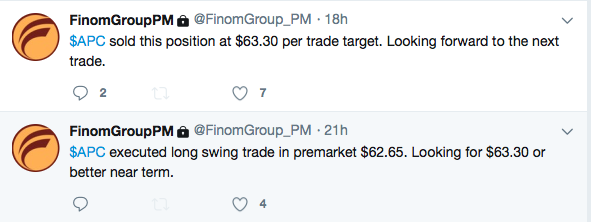

In discussing the oils, Cramer likes Royal Dutch Shell and Marathon Petroleum Corporation. Finom Group’s chief market strategist Seth Golden agrees with both Goldman Sachs and Cramer’s picks so far as sector highlights. Oil prices are trending higher in 2018 and consumer spending is trending in kind. Retail sales suggest both sectors will be out-performers in 2018. As such, Anadarko Petroleum (APC) and Target (TGT) continue to be Golden’s picks. Just yesterday, Finom Group profited from the dip the most recent dip in shares of APC with a swing trade alert to subscribers, as displayed in the screenshot below.

U.S. equity futures are modestly highly ahead of the opening bell on Wall Street Friday. After a strong market surge on Thursday, it’s likely that Friday’s trade will produce low volumes and a moderated performance for all indices.

In closing out this daily market dispatch, Finom Group recognizes and celebrates the life and art of Aretha Franklin. It is as she once famously said, “Music changes, and I’m gonna change right along with it.”