Welcome to another trading week. In appreciation to all of our Basic membership level participants and daily readers of finomgroup.com content, we offer the following excerpts from our Weekly Research Report. Our weekly report is extremely detailed and has proven to help guide investors and traders during all types of market conditions with thoughtful insights and analysis, graphs, studies, and historical data/analogues. We encourage our readers to upgrade to our Contributor membership level to receive our Weekly Research Report and State of the Market Videos and take advantage of this ongoing promotional event today! With that have a great trading week, be in touch and take a look at some of the materials in this weekend’s published Research Report!

Research Report Excerpts #1

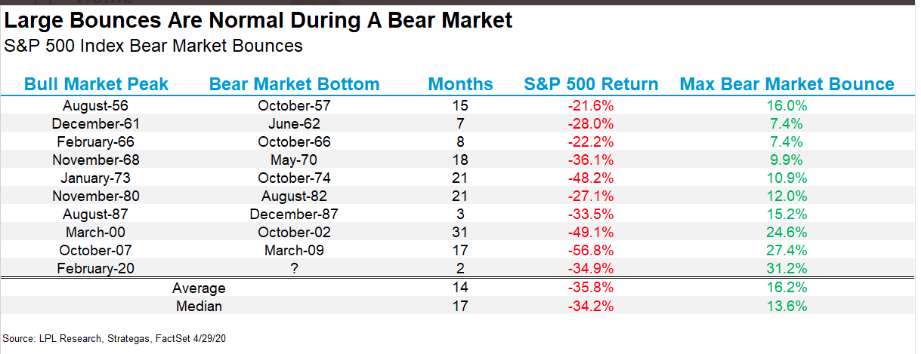

As noted above and probably lost in the shuffle, our forecast for market consolidation is coming to fruition with back-to-back weekly losses for the S&P 500. This is not to offer a “We told you so“, but simply to remind investors and traders of the commonality of bear markets and to reiterate how consolidation CAN take place: Consolidation can take place for both price and/or time. We emphasized this two weeks ago, and now recognize that the market has consolidated for both price and time with consecutive weekly declines. Hasn’t quite felt that way though, right? Here is what we offered to subscribers in our Special Research Report issued just ahead of Easter Sunday. We encourage review of past works as frequently as time permits:

Ahead of us lay earnings season and some degree of uncertainty as to when the U.S. economy will embark upon normalizing. Such uncertainty may not lend itself well to markets, which will also key off what is expected to be a decline in earnings for the interim and alongside a lack of usual corporate guidance. These are tall obstacles for investor sentiment to overcome, which may prove a driving force for equity market consolidation near-term. With all that being said, we believe investors/traders are best served by remaining flexible, exercising cautious optimism for long-term returns and beginning to look for opportunities to deploy capital on market pullbacks. Folks, there is a ton of cash on the sidelines that will eventually be put to work and it may just take a greater degree of certainty.

We’ve definitely witnessed some degree of consolidation from the market in both time and price, but not much! In two weeks we’ve only dropped ~1.5%, while exacting the strongest bear market rally in history at over 31 percent.

Research Report Excerpts #2

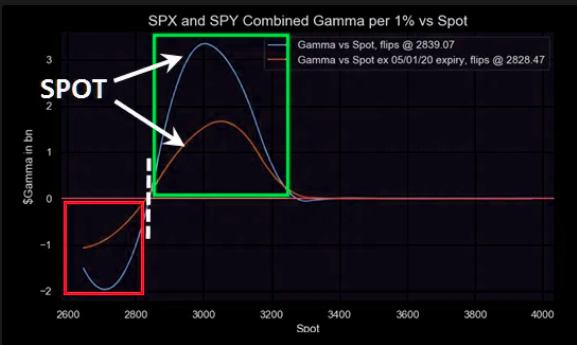

With that in mind, here are some parsings from Nomura’s market quant specialist Charlie McElligott pared with his Gamma Zone chart:

“The extent / velocity of the selloff in Spooz (SPY/ES) matters because 1) it has seen us trade back below the trigger level where the CTA position signal would yet-again pivot back “short[…] below 2805 goes back -100% short.” –Charlie McElligott of Nomura

Research Report Excerpts #3

Can we please not correlate the markets’ ability to move higher simply due to buyback levels. As if this correlation ever made any sense in the first place! Here are corporate buybacks with the S&P 500’s returns for that particular year. The correlation is very, weakly positive at 0.08. It is clearly not the driving force it’s made out to be. Having said that, we don’t exonerate that buybacks do have minimal benefits, as referenced.

As shown in the chart above, the largest buyback period from 2003-2007 was in 2007, yet the S&P 500 only garnered a 4% return.

Research Report Excerpts #4

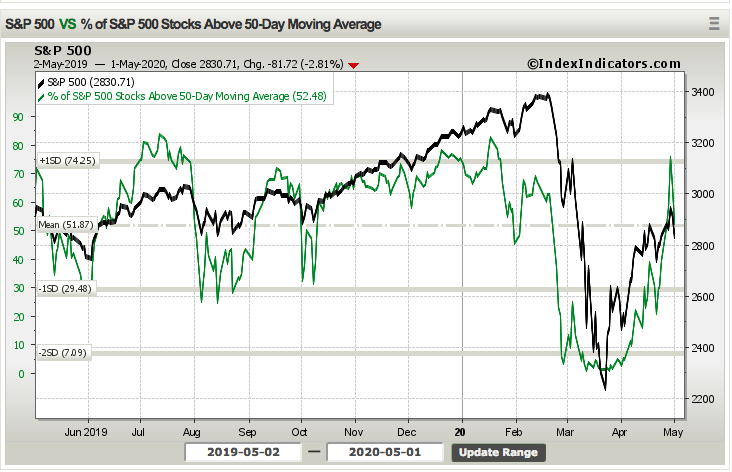

At the end of the week that was, more than 50% of stocks are now trading above their 50-DMA, identifying broadening and improving market breadth, with small-caps outperforming large-caps. Additionally, this breadth indicator is making both higher highs and higher lows through the relief rally. Lastly, look at sector performance for the month of April, which identifies offensive, cyclical sectors outperforming defensive sectors. This is what investors want to see from sector performance to identify that it is less likely a full re-test of the low would take place and investors are found with improved risk appetite.

Research Report Excerpts #5

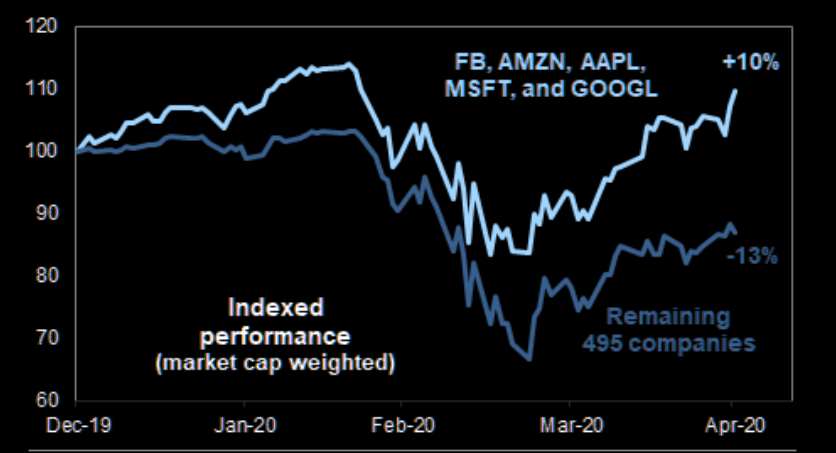

- David Kostin: “Narrow breadth is always resolved the same way: The relative outperformance of market leaders eventually gives way to underperformance. The five stocks has upside potential of just 3% to GS analyst price targets vs. 10% for the other 495 firms.”

David Kostin’s “outlook” for FAANMG is just that, a forecast. We understand that forecasts are moving targets, meant to be revised as Kostin has revised his entire market forecast more recently.

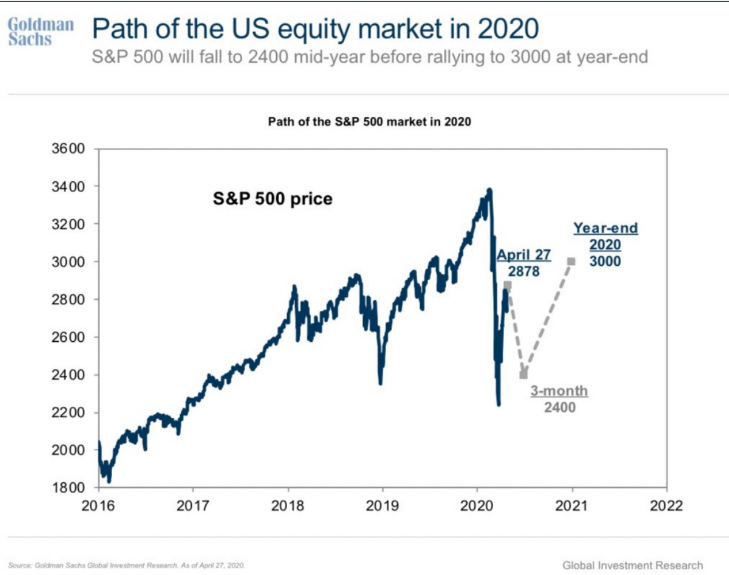

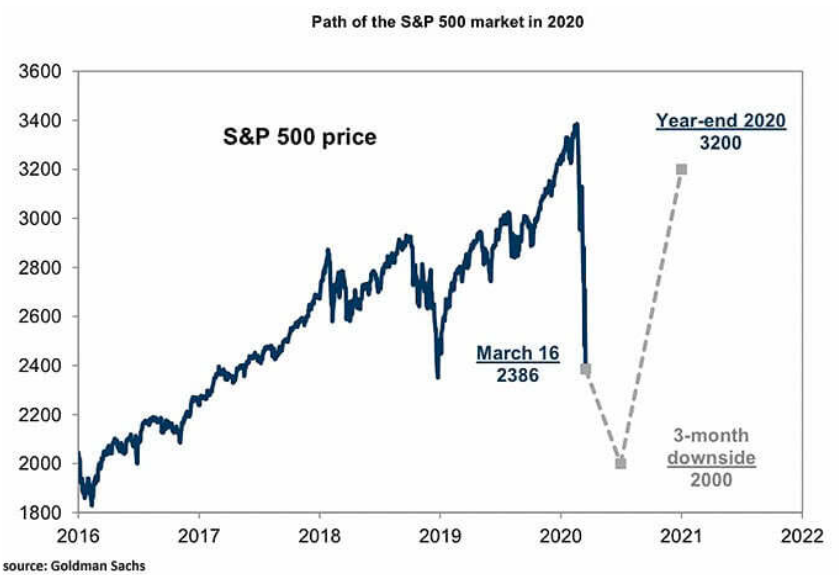

That’s Kostin’s latest (April 27) forecast for the S&P 500, which was revised from the early April forecast as follows:

Moving targets, folks; nothing more and nothing less. Take them to be pieces of information as they make up the pie known as due diligence.

Research Report Excerpts #6

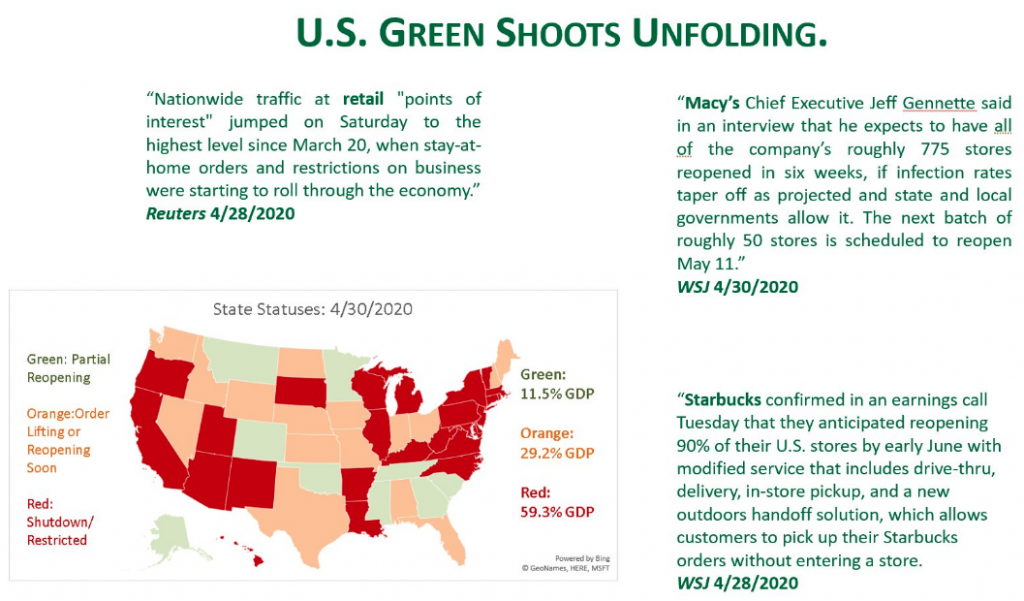

So here’s the deal! Yes, we anticipate further consolidation of the relief rally within the next 30 days. With this understanding, we remain with a heavy cash position after generating 40 positive trades for Finom Group Premium and Master Mind Options members over the month of April. We anticipated, in much the same manner we have heralded market consolidation and further consolidation ahead, the relief rally that has developed. The profitable trades completed afford us the opportunity to buy on the dip, which we also anticipate exercising. While we can’t define the depth or duration of market consolidation anticipated, and encourage investors to avoid the attempt at doing so themselves, many of our indicators have turned more bullish and in accordance with a reopening of the economy in stages. While April’s market recovery was robust, the pandemic is just beginning to make itself felt in US economic data, and the road to recovery will undoubtedly be marked by fits and starts. We’re not out of the woods just yet, but we are making positive strides.

“Bank of America Corp. is starting to see consumer spending edge higher after plunging with the start of the coronavirus lockdown.

The nascent increase, which follows a 30% drop, is showing up as consumers buy more groceries, restaurant meals, clothing and gasoline, Chief Executive Officer Brian Moynihan said in an interview Friday on CNBC. U.S. aggregate spending averaged about $50 billion over the past four weeks, comparable to levels in the fall of 2017, he said.”

Research Report Excerpts #7

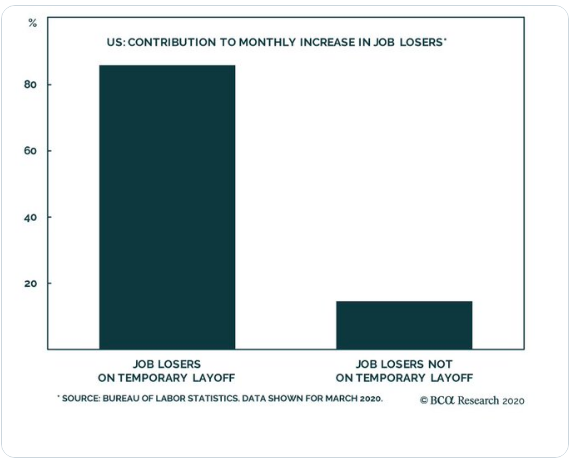

The potential bright side of a collapsing labor market, however proves to be that job losses have been due to temporary layoffs; so assuming companies can get most of these workers back full-time, the hit to the labor market will not be as dramatic as initially feared.

This may have proven to be one of the reasons that in the face of dire jobless claims data through the month of April, the market didn’t flinch, but in fact rallied. And as we continue into the coming trading week with a litany of economic data, it will be pared with earnings releases.

Research Report Excerpts #8

Anybody desire to do the math on the YoY analysts FY2020 EPS projections? Well, let’s take a crack at it: We will use the going projections and round the numbers for ease of use as follows:

- Q1 is trending -14% EPS. (rounded up) Q2 + Q3 + Q4 (below)

- -14 + -37 + -20 + -10 = -81% EPS contraction SaaR.

- Now divide the -81% by 4 quarters and the result = -20.25% YoY EPS contraction

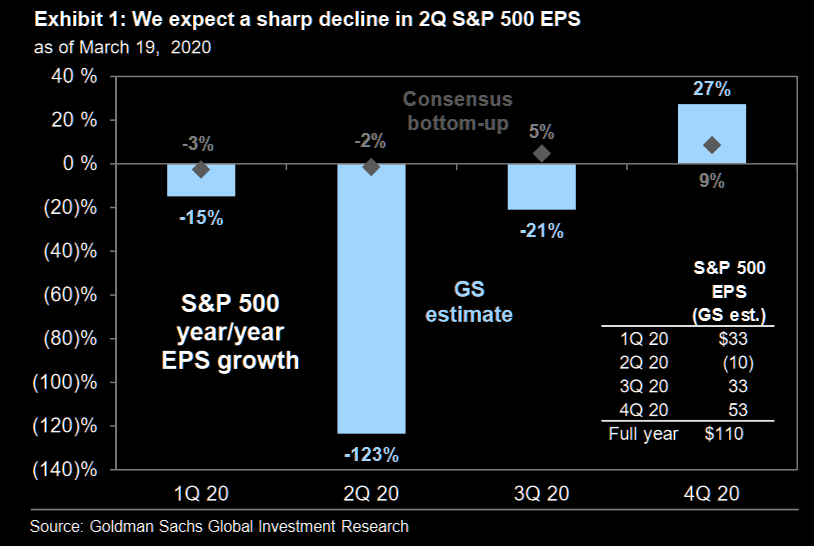

The good news here is that Q1 estimates are actually coming in better than expected and even the full year estimates are better than that from Goldman Sachs. The firm has a FY2020 EPS forecast decline of 33 percent, as outlined below:

“We now forecast S&P 500 EPS of $110 in 2020, a decline of 33% from 2019. On a quarterly basis, this reflects year/year growth of -15%, -123%, -21% and +27%. We have cut our 2020 earnings forecast three times in 30 days (-37% in total) as the magnitude of the economic slowdown has become increasingly apparent.”

We hope you enjoyed some of our excerpts from this weekend’s Research Report! Take advantage of our ongoing promotion and upgrade to our Contributor Membership and lock in the current month rate! Have a great trading week everybody!